Quick Navigation

Report Overview

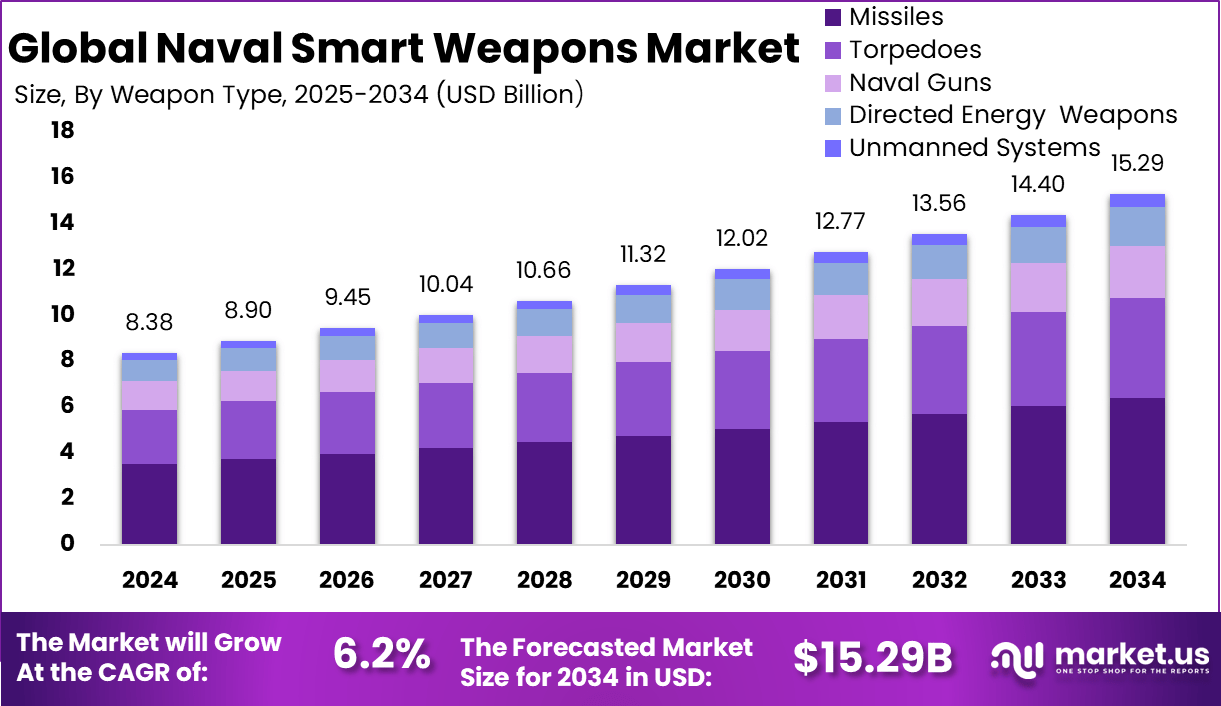

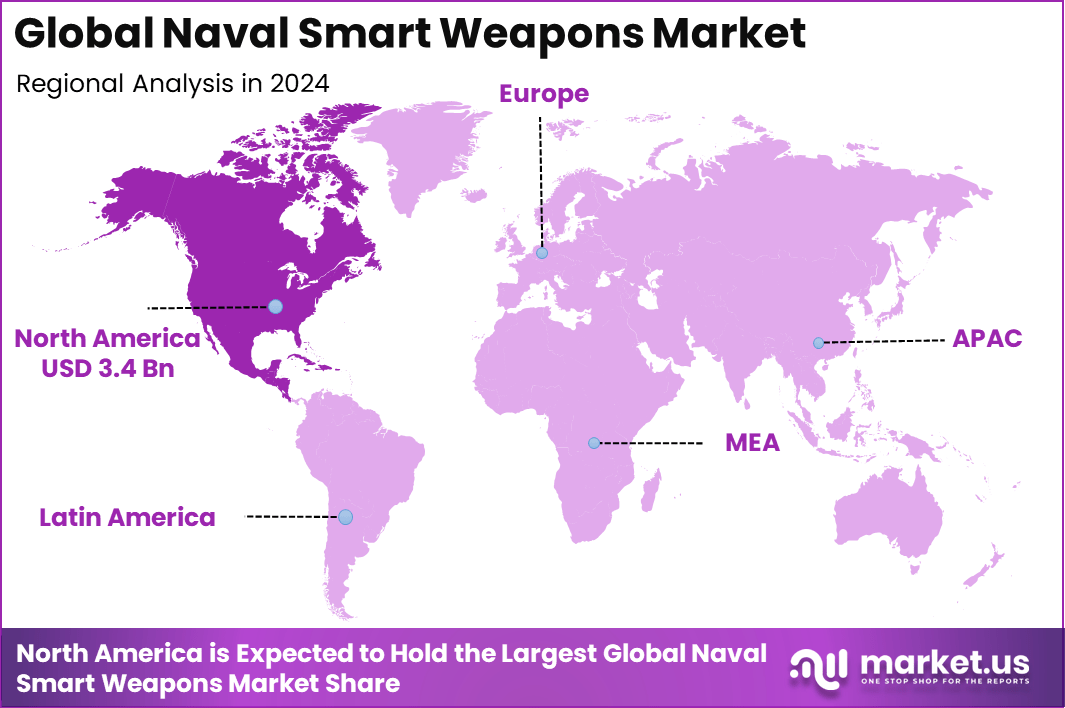

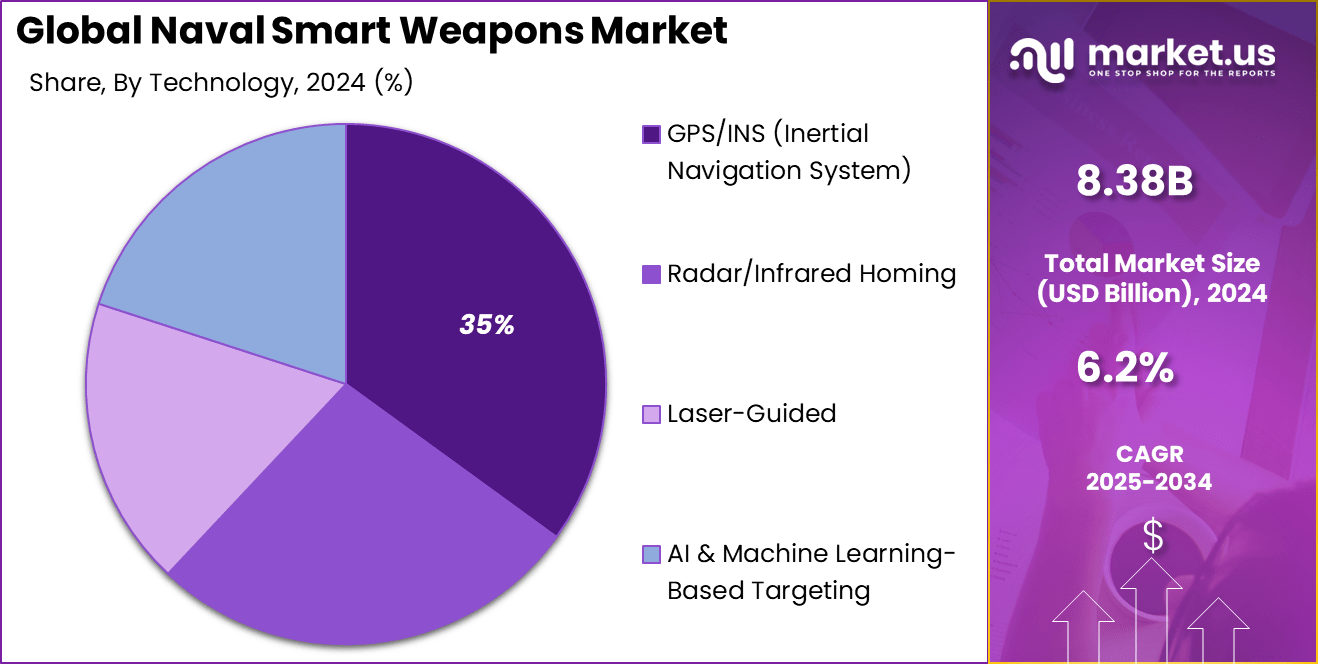

The Global Naval Smart Weapons Market size is expected to be worth around USD 15.29 billion by 2034, from USD 8.38 billion in 2024, growing at a CAGR of 6.2% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 41% share, holding USD 3.4 billion in revenue.

Naval smart weapons are advanced, precision-guided munitions specifically engineered for maritime warfare. These systems integrate cutting-edge technologies such as artificial intelligence (AI), satellite navigation, laser guidance, and real-time data processing to enhance targeting accuracy and operational efficiency. Their primary objective is to deliver precise strikes against designated targets while minimizing collateral damage and ensuring mission success in complex maritime environments.

The global naval smart weapons market is experiencing significant growth, driven by escalating geopolitical tensions and the imperative for modernized naval capabilities. Several key factors are propelling the growth of the naval smart weapons market. Firstly, the intensification of maritime disputes and the need for enhanced sea-based deterrence capabilities have led to increased investments in advanced naval weaponry.

Secondly, the integration of AI and machine learning technologies has revolutionized targeting systems, enabling more autonomous and accurate operations. Lastly, the development of hypersonic missiles and other next-generation weapon systems has further stimulated market expansion.

The demand for naval smart weapons is surging globally, particularly in regions with significant maritime interests. North America currently holds the largest market share, attributed to substantial defense budgets and ongoing modernization programs Meanwhile, the Asia-Pacific region is anticipated to witness the fastest growth, fueled by regional security concerns and increased naval expenditures.

For instance, In May 2025, Australia renewed calls for a dedicated Coast Guard to reduce strain on the Royal Australian Navy amid rising Indo-Pacific tensions. The move reflects a growing focus on maritime security and increased reliance on smart naval weapons to bolster national defense and regional stability.

Key Takeaways

- In 2024, the missiles segment emerged as the leading category, accounting for a 42% share of the market.

- The GPS/INS (Inertial Navigation System) segment secured a 35% share, reflecting the increasing adoption of integrated guidance technologies that enhance strike accuracy and weapon system reliability across variable maritime environments.

- Among platforms, the surface ships segment commanded a 44% share in 2024. This strong position can be attributed to the expanding modernization programs across naval fleets globally, where smart weapon integration into destroyers, frigates, and carriers remains a top strategic priority.

- Regionally, North America led the global naval smart weapons market, contributing over 41% share in 2024. The region’s dominance is underpinned by sustained defense budgets, technological superiority, and rapid deployment of next-gen maritime warfare systems.

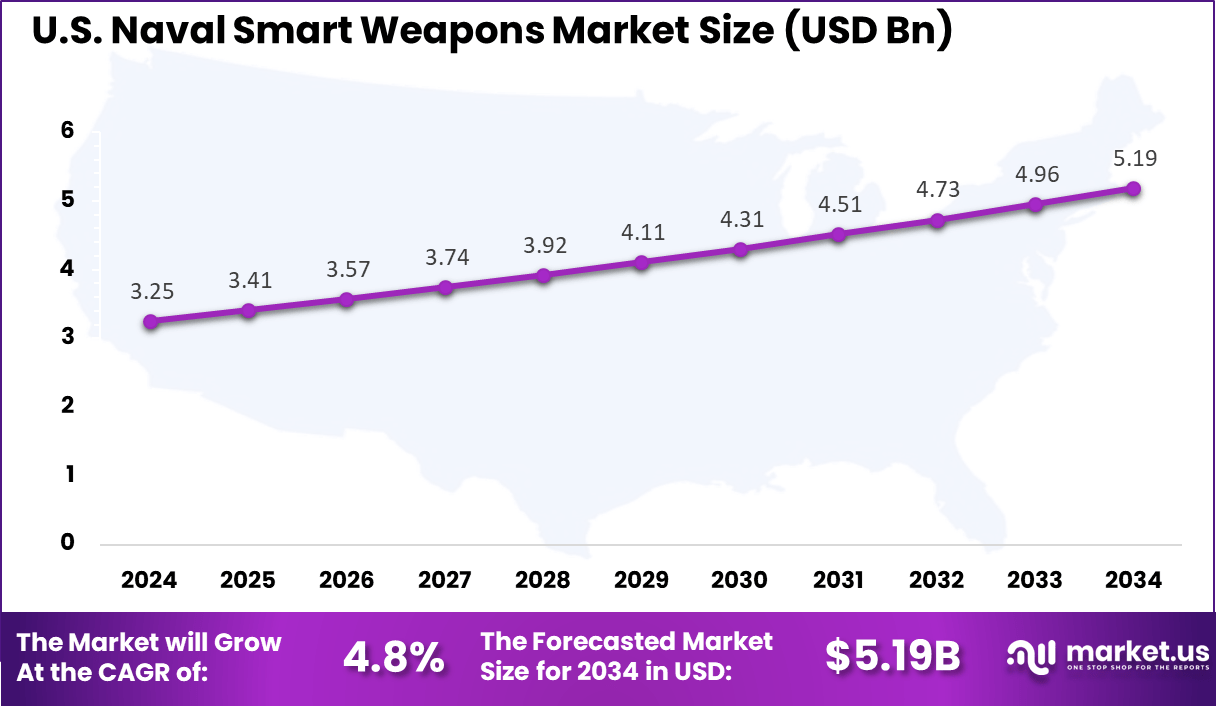

- The U.S. Naval Smart Weapons Market alone was valued at USD 3.25 billion in 2024, with a steady growth trajectory projected at a 4.8% CAGR, supported by ongoing naval modernization efforts, increased R&D initiatives, and evolving maritime security threats in key strategic zones.

US Market Expansion

The market for Naval Smart Weapons within the U.S. is growing tremendously and is currently valued at USD 3.25 billion, the market has a projected CAGR of 4.8%. This market is growing tremendously due to increasing defense allocations, technological advancements, and the strategic pivot toward great-power competition.

The U.S. Naval force is prioritizing the integration of AI-enabled munitions, precision-guided missiles, and unmanned platforms to enhance lethality, survivability, and rapid response in contested maritime environments. This growth is further fueled by modernization programs and collaborative defense initiatives aimed at maintaining naval superiority and deterring emerging threats.

For instance, In December 2024, Palantir Technologies and Anduril Industries formed a strategic consortium to advance AI-driven naval smart weapons in the U.S. defense sector. By merging AI analytics with autonomous systems, the alliance aims to boost situational awareness, real-time decision-making, and precision targeting – signaling a firm U.S. push to sustain technological dominance in naval warfare.

North America Growth

In 2024, North America held a dominant market position in the Naval Smart Weapons Market, capturing more than a 41% share, holding USD 3.4 billion in revenue. The market for naval smart weapons within North America is experiencing significant growth driven by substantial defense spending, technological innovation, and a heightened focus on maritime security amid evolving global threats.

The region’s naval forces are actively modernizing their arsenals with advanced precision-guided munitions, autonomous systems, and integrated AI capabilities. The region benefits from strong NATO partnerships that enhance cooperation and joint military operations. Industry-led collaborations and alliances with top defense companies promote the development and application of innovative technologies, positioning North America as the most significant and fastest-growing naval smart weapon market.

For instance, In March 2025, EDGE Group and CMN Naval partnered to co-develop AI-enabled next-gen warships, integrating autonomous systems to boost combat efficiency and mission performance. This move highlights the defense industry’s shift toward intelligent naval platforms, designed to reduce crew dependency, support faster decisions, and adapt to complex maritime threats with greater precision.

Weapon Type Insights

In 2024, the missiles segment held a dominant position in the naval smart weapons market, capturing over 42% of the total market share. This leadership is attributed to the increasing demand for precision-guided munitions capable of engaging both surface and underwater targets. Advanced missile systems, such as anti-ship and cruise missiles, are being integrated into naval platforms, enhancing their combat capabilities.

The prominence of the missiles segment is further reinforced by continuous innovations and upgrades in missile technology. The integration of advanced guidance systems, including GPS and inertial navigation systems, has revolutionized naval warfare, allowing for more accurate and effective targeting.

Additionally, the development of hypersonic missiles, such as the Mako Multi-Mission Hypersonic Missile, which is compatible with fifth-generation fighters and naval platforms, underscores the strategic importance of missile systems in modern naval operations.

For instance, in March 2025, Ukraine unveiled its extended-range R-360 Neptune missile, designed for deep-strike capabilities against strategic targets within Russia. This development highlights a growing trend among nations to invest in indigenous smart weapon systems with extended reach and precision, which is driven by the need for strategic deterrence and operational autonomy in high-threat maritime and land-based environments.

Furthermore, the strategic deployment of missile systems, such as the U.S. Navy’s plan to arm ships with Patriot interceptor missiles in response to potential threats from hypersonic weapons, highlights the critical role of missiles in ensuring maritime security. These developments indicate a sustained investment in missile technology, solidifying the segment’s leading position in the naval smart weapons market.

Technology Insights

In 2024, the GPS/INS (Inertial Navigation System) segment held a dominant position in the naval smart weapons market, capturing over 35% of the total market share. This prominence is attributed to the increasing demand for precision-guided munitions capable of operating effectively in contested environments where GPS signals may be degraded or denied.

The integration of GPS with INS provides a robust navigation solution, ensuring accuracy and reliability in targeting, even under challenging conditions. This dual-system approach enhances the effectiveness of naval smart weapons, making them more resilient to electronic warfare tactics employed by adversaries.

The strategic importance of GPS/INS technologies is further underscored by ongoing advancements in navigation systems. For instance, the development of quantum-assured magnetic navigation has demonstrated positioning accuracy surpassing that of strategic-grade INS in both airborne and ground-based trials.

Such innovations offer alternative navigation solutions that are less susceptible to jamming and spoofing, thereby enhancing the operational capabilities of naval forces. As the threat of GPS denial becomes more pronounced, the reliance on integrated navigation systems like GPS/INS is expected to grow, solidifying their leading position in the naval smart weapons market.

For instance, in April 2025, Anello Photonics unveiled an advanced maritime inertial navigation system (INS) designed to provide highly accurate positioning and navigation for naval smart weapons and autonomous platforms. This system enhances weapon guidance reliability, particularly in GPS-denied environments, and also improves mission success rates and operational resilience for naval forces operating in contested or challenging maritime theaters.

Platform Insights

In 2024, the surface ships segment held a dominant position in the naval smart weapons market, capturing over 44% of the total market share. This prominence is attributed to the increasing demand for advanced weapon systems on naval platforms, driven by the need for enhanced maritime security and the modernization of naval fleets.

Surface ships, including destroyers, frigates, and corvettes, serve as primary platforms for deploying a variety of smart weapons, such as missiles, naval guns, and directed energy weapons. The versatility and adaptability of these vessels make them ideal for integrating cutting-edge technologies, thereby enhancing their combat capabilities and operational effectiveness.

In April 2025, Saronic unveiled its latest range of autonomous surface ships designed to enhance naval operational capabilities. The new models include the Saronic ASV-120 and ASV-180, both equipped with advanced autonomous navigation, surveillance, and modular payload options. These vessels are tailored for missions such as maritime patrol, reconnaissance, and mine countermeasures, reflecting the growing demand for unmanned platforms in modern naval warfare.

The strategic importance of surface ships is further underscored by ongoing investments in naval modernization programs across various countries. For instance, the U.S. Navy’s initiatives to equip ships with advanced missile systems and directed energy weapons highlight the emphasis on enhancing surface combatants’ capabilities.

Similarly, other nations are focusing on upgrading their naval fleets to address emerging threats and maintain maritime dominance. The integration of smart weapons into surface ships not only improves their offensive and defensive capabilities but also ensures interoperability with other naval assets, thereby contributing to a cohesive and responsive maritime force.

Key Market Segments

By Weapon Type

- Missiles

- Torpedoes

- Naval Guns

- Directed Energy Weapons

- Unmanned Systems

By Technology

- GPS/INS (Inertial Navigation System)

- Radar/Infrared Homing

- Laser-Guided

- AI & Machine Learning-Based Targeting

By Platform

- Surface Ships

- Submarines

- Aircraft Carriers & Amphibious Assault Ships

- Unmanned Naval Vessels

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Emerging Trends

The naval smart weapons landscape is undergoing a significant transformation, driven by advancements in artificial intelligence (AI), autonomous systems, and precision-guided technologies. Modern naval forces are increasingly integrating AI-powered targeting systems and autonomous platforms, such as unmanned surface vessels (USVs) and drones, to enhance operational efficiency and reduce human risk.

These technologies enable real-time data processing and decision-making, allowing for more precise and effective engagement of targets. For instance, the U.S. Navy’s initiatives like the Ghost Fleet Overlord and Project 33 focus on deploying autonomous vessels capable of executing complex missions with minimal human intervention.

Another notable trend is the development of directed energy weapons (DEWs), including laser-based systems, which offer cost-effective and precise targeting capabilities. These weapons can engage multiple threats with high accuracy and minimal collateral damage. The integration of DEWs into naval platforms signifies a shift towards more sustainable and efficient defense mechanisms

Business Benefits

The adoption of smart weapons in naval operations presents substantial business advantages, particularly in terms of cost-efficiency and operational effectiveness. Precision-guided munitions reduce the number of weapons required to neutralize targets, leading to significant savings in ammunition expenditure.

Moreover, the decreased need for large crew complements on autonomous vessels translates to lower personnel costs and reduced risk to human life. These factors contribute to a more streamlined and economically sustainable defense strategy. Furthermore, the integration of advanced technologies into naval weaponry stimulates innovation and growth within the defense industry.

Companies specializing in AI, robotics, and advanced materials find new opportunities to collaborate and develop cutting-edge solutions tailored for maritime applications. This boosts technological innovation while reinforcing the defense industrial base. It delivers lasting economic and strategic gains for all stakeholders engaged in naval smart weapons development.

Driver

Escalating Defense Expenditures and Naval Modernization

The global naval smart weapons market is experiencing significant growth, primarily driven by increased defense spending and concerted efforts toward naval modernization. Nations worldwide are allocating substantial budgets to enhance their maritime capabilities, recognizing the strategic importance of advanced naval weaponry in contemporary warfare.

For instance, the United Kingdom has announced a £1.5 billion initiative to construct new weapons and explosives factories, aiming to bolster its defense readiness in response to evolving global threats. This surge in investment is not isolated. Countries such as China and India are also amplifying their defense budgets, focusing on the development and procurement of sophisticated naval systems.

The emphasis on acquiring precision-guided munitions, advanced missile systems, and AI-integrated platforms underscores a global trend toward modernizing naval forces to address emerging security challenges effectively.

Restraint

High Development and Operational Costs

Despite the promising growth trajectory, the naval smart weapons market faces significant restraints due to the high costs associated with the development, production, and maintenance of advanced weapon systems. The integration of cutting-edge technologies, such as artificial intelligence and advanced sensor systems, necessitates substantial financial investment, which can be prohibitive for some nations.

Moreover, the operational costs, including training personnel, system upgrades, and maintenance, further strain defense budgets. These financial challenges are particularly acute for developing countries, where budgetary constraints may limit the adoption and deployment of sophisticated naval weaponry, thereby impacting the overall market growth.

Opportunity

Integration of Artificial Intelligence and Autonomous Systems

The integration of artificial intelligence (AI) and autonomous systems presents a significant opportunity for the naval smart weapons market. AI-driven technologies enhance decision-making capabilities, improve targeting accuracy, and enable real-time data analysis, thereby increasing the effectiveness of naval operations.

Furthermore, AI integration facilitates the development of predictive maintenance systems, optimizing operational efficiency and reducing downtime. As AI technologies continue to evolve, their application in naval smart weapons is expected to expand, offering enhanced capabilities and operational advantages in maritime defense strategies.

Challenge

Cybersecurity Threats to Naval Smart Weapons

The increasing reliance on digital technologies and networked systems in naval smart weapons introduces significant cybersecurity challenges. These sophisticated systems are vulnerable to cyberattacks, which can compromise operational integrity, lead to unauthorized access, or disrupt critical functions.

Ensuring the cybersecurity of naval smart weapons requires continuous investment in robust security protocols, regular system updates, and comprehensive threat assessments. The complexity of safeguarding these systems is compounded by the need to protect against both external threats and potential internal vulnerabilities, making cybersecurity a critical concern in the deployment and operation of advanced naval weaponry.

Key Player Analysis

The Boeing Company has significantly enhanced its naval smart weapons portfolio through strategic acquisitions and substantial contracts. In 2024, Boeing secured a $7.5 billion contract from the U.S. Air Force to produce Joint Direct Attack Munition (JDAM) kits, converting conventional bombs into precision-guided munitions.

Lockheed Martin Corporation continues to lead in naval smart weapons innovation. The unveiling of the Mako Multi-Mission Hypersonic Missile in 2024, compatible with fifth-generation fighters like the F-35, underscores its commitment to advanced weaponry. Furthermore, the successful integration of the Long Range Anti-Ship Missile (LRASM) onto the F-35B enhances the platform’s strike capabilities.

RTX Corporation, through its Raytheon division, has solidified its position in the naval smart weapons market with key contracts and product deliveries. In May 2025, Raytheon was awarded a $580 million contract for the Next Generation Jammer Mid-Band system, enhancing electronic warfare capabilities.

Top Key Players Covered

- The Boeing Company

- Lockheed Martin Corporation

- RTX Corporation

- BAE Systems PLC

- Rheinmetall AG

- THALES

- L3Harris Technologies Inc.

- Northrop Grumman Corporation

- Textron Inc.

- General Dynamics Corporation

- MBDA

- Leonardo SpA

- Others

Recent Developments

- In May 2025, RTX’s Raytheon division delivered its 250th Rolling Airframe Missile (RAM) launcher to the U.S. Navy. This milestone underscores the growing demand for rapid-response, close-in defense systems capable of intercepting incoming threats such as anti-ship missiles and aerial vehicles, thereby enhancing fleet survivability and mission readiness.

- In March 2025, Lockheed Martin completed flight tests integrating the Long-Range Anti-Ship Missile (LRASM) onto the F-35B Lightning II fighter jet. This milestone enhances the aircraft’s strike capabilities against high-value maritime targets, reinforcing its role in naval deterrence and long-range precision engagement strategies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 8.38 Bn |

| Forecast Revenue (2034) | USD 15.29 Bn |

| CAGR (2025-2034) | 6.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Weapon Type (Missiles, Torpedoes, Naval Guns, Directed Energy Weapons, Unmanned Systems), By Technology (GPS/INS (Inertial Navigation System), Radar/Infrared Homing, Laser-Guided, AI & Machine Learning-Based Targeting), By Platform (Surface Ships, Submarines, Aircraft Carriers & Amphibious Assault Ships, Unmanned Naval Vessels) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | The Boeing Company, Lockheed Martin Corporation, RTX Corporation, BAE Systems PLC, Rheinmetall AG, THALES, L3Harris Technologies Inc., Northrop Grumman Corporation, Textron Inc., General Dynamics Corporation, MBDA, Leonardo SpA, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |