Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- US Market Expansion

- North America Growth

- By Type Analysis

- By Launching Platform Analysis

- By Range Analysis

- By Propulsion Engine Analysis

- By Overhead Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

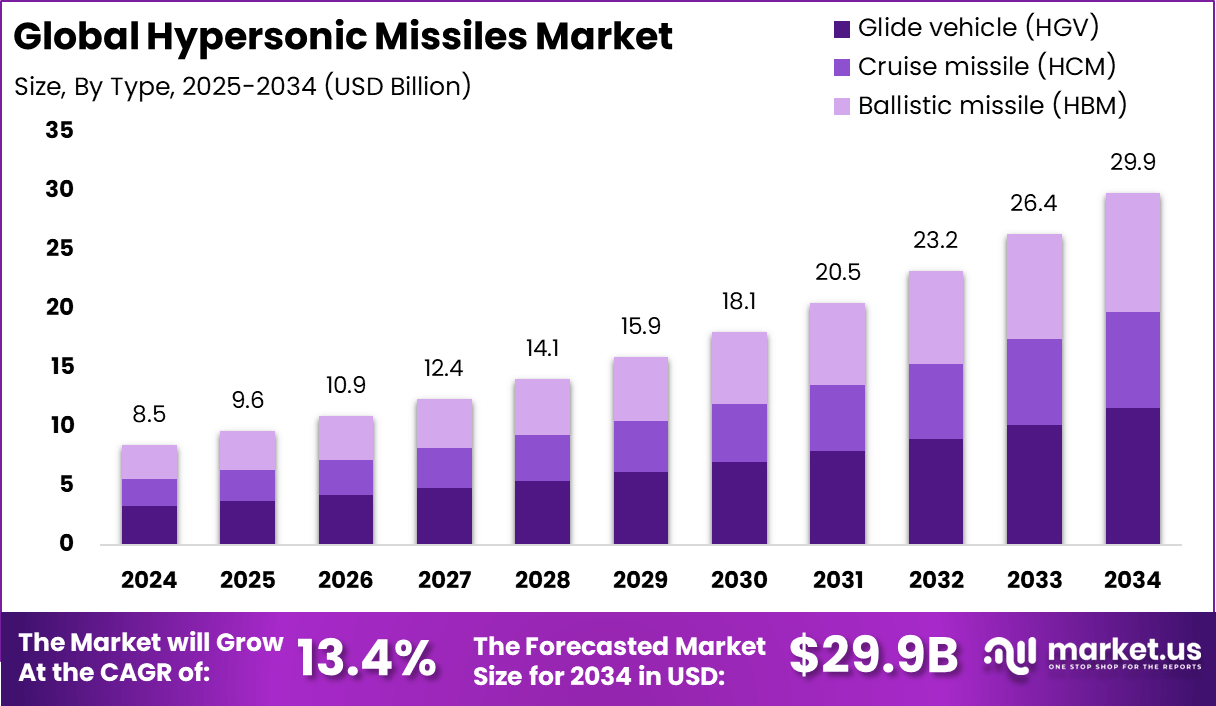

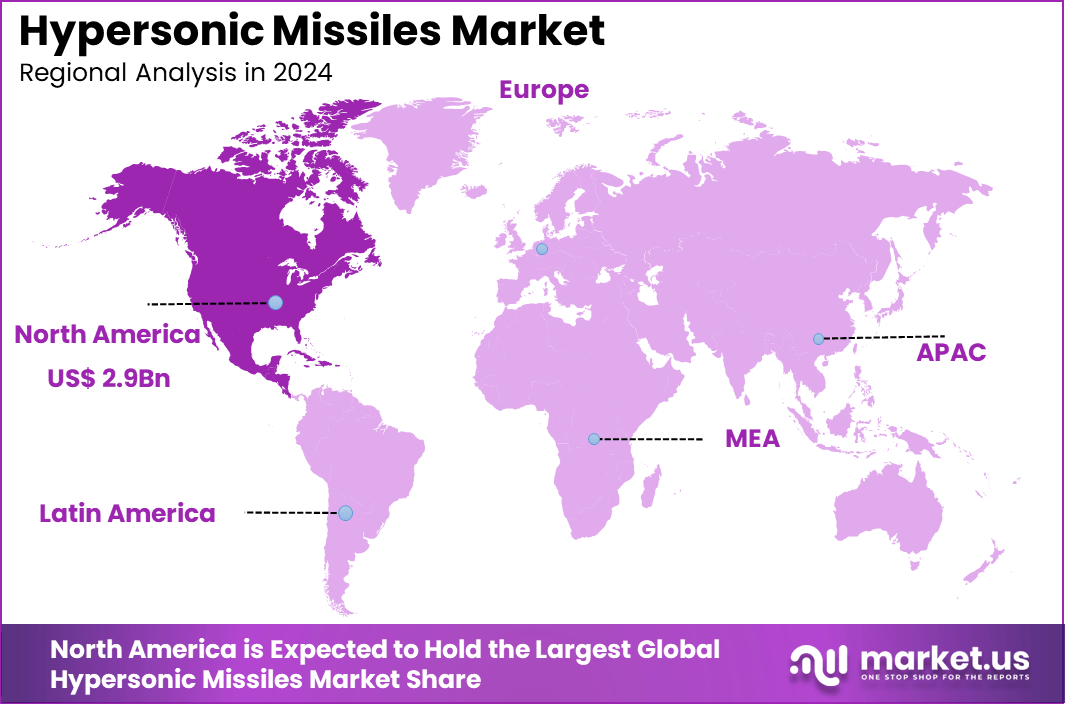

The Global Hypersonic Missiles Market size is expected to be worth around USD 29.9 Billion By 2034, from USD 8.5 billion in 2024, growing at a CAGR of 13.4% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 34.6% share, holding USD 2.9 Billion revenue.

Hypersonic missiles are advanced weapons capable of traveling at speeds exceeding Mach 5, or five times the speed of sound. These missiles combine high velocity with maneuverability, making them difficult to detect and intercept. There are primarily two types: hypersonic glide vehicles (HGVs), which are launched from a rocket before gliding towards their target, and hypersonic cruise missiles, which are powered throughout their flight by high-speed engines such as scramjets.

The hypersonic missiles market is experiencing significant growth due to increased defense spending and technological advancements. Key drivers of the hypersonic missiles market include the increasing need for precision strike capabilities and the development of advanced propulsion systems. Technological advancements in materials science, guidance systems, and propulsion technologies are enhancing the performance and reliability of hypersonic weapons.

The adoption of hypersonic missile technology is influenced by the strategic advantages it offers, such as rapid response times and the ability to evade existing missile defense systems. Countries are investing in hypersonic capabilities to maintain a competitive edge and to strengthen their deterrence strategies. The development of counter-hypersonic defense systems is also becoming a priority, further fueling research and investment in this domain.

The business benefits of investing in hypersonic missile technology include access to lucrative defense contracts, the potential for technological spillovers into civilian applications, and the opportunity to lead in a high-growth sector. Companies that develop expertise in hypersonic technologies may also find applications in aerospace, transportation, and materials engineering, broadening their market reach.

Key Takeaways

- The Global Hypersonic Missiles Market is projected to grow from USD 8.5 billion in 2024 to USD 29.9 billion by 2034, marking a sharp CAGR of 13.4% over the forecast period from 2025 to 2034.

- North America led the market in 2024, accounting for over 34.6% share, which translated to USD 2.9 billion in revenue, supported by escalating defense budgets and strategic R&D.

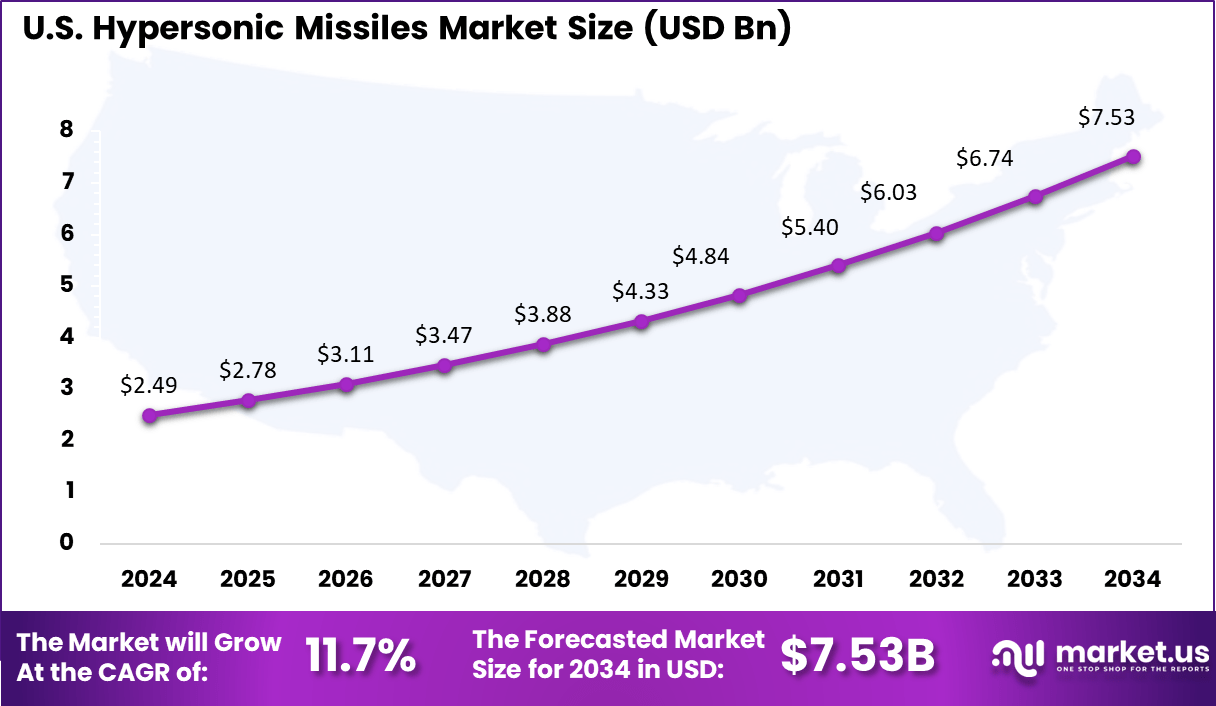

- The U.S. Hypersonic Missiles Market reached USD 2.49 billion in 2024 and is forecasted to grow to USD 7.53 billion by 2034, expanding at a CAGR of 11.7%, driven by strong investments in deterrence and long-range strike capabilities.

- The Hypersonic Glide Vehicle (HGV) segment captured 38.7% share in 2024, establishing dominance due to its maneuverability and advanced evasion capabilities against missile defense systems.

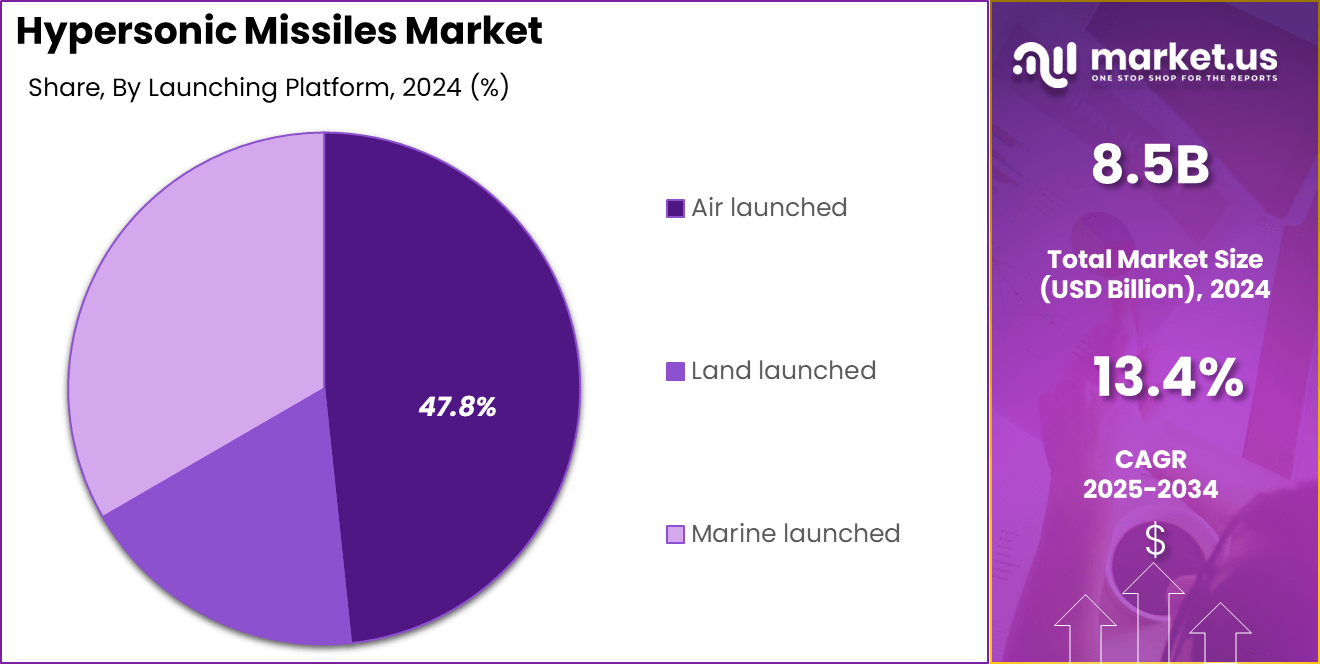

- In terms of launch mode, the air-launched category secured over 47.8% of the market in 2024, fueled by its adaptability, rapid deployment potential, and integration with next-gen aircraft.

- The Long Range (Above 2,000 km) category held a commanding 60.4% share in 2024, reflecting rising geopolitical tensions and the demand for strategic deep-strike precision weaponry.

- On the propulsion front, Liquid and Solid-Fueled Rockets held 32.5% share in 2024, driven by their proven performance in speed, range, and reliability under hypersonic conditions.

- The Conventional warhead segment led the market, capturing more than 54.8% share in 2024, as countries increasingly prefer non-nuclear but high-impact hypersonic systems for flexible combat strategies.

Analysts’ Viewpoint

Investment opportunities in the hypersonic missiles market are abundant, with significant funding directed towards research and development, testing facilities, and production capabilities. Governments are collaborating with defense contractors and technology firms to accelerate the deployment of hypersonic weapons.

For instance, the U.S. Department of Defense has increased its budget allocations for hypersonic programs, reflecting the strategic importance of these weapons in modern warfare. The regulatory environment for hypersonic missiles is complex, as existing arms control agreements may not adequately address the unique characteristics of these weapons.

The rapid development and deployment of hypersonic technologies are prompting discussions on the need for updated international treaties and export control regimes to prevent proliferation and to maintain strategic stability. Engagement among nations is essential to establish norms and agreements that govern the use of hypersonic weapons.

US Market Expansion

The U.S. Hypersonic Missiles Market is experiencing strong momentum, driven by rising defense modernization efforts and intensifying global strategic competition. In 2024, the market has been valued at approximately USD 2.49 Billion, reflecting increasing investments in next-generation weapon technologies.

This growth trajectory is expected to accelerate, reaching around USD 2.78 Billion in 2025 and surging to nearly USD 7.53 Billion by 2034. The expansion is being projected at a robust CAGR of 11.7% during the period from 2025 to 2034.

North America Growth

In 2024, North America held a dominant market position, capturing more than a 34.6% share of the global hypersonic missiles market and generating approximately USD 2.9 billion in revenue. This regional dominance has been primarily fueled by the United States’ aggressive investments in next-generation defense capabilities, particularly hypersonic strike and glide technologies.

As geopolitical tensions intensify and global defense strategies shift toward rapid-response weaponry, the U.S. Department of Defense has accelerated funding for hypersonic programs such as the Air-Launched Rapid Response Weapon (ARRW), the Long-Range Hypersonic Weapon (LRHW), and the Conventional Prompt Strike (CPS) system.

These initiatives have not only driven significant R&D expenditure but also positioned the U.S. as a technological front-runner in this field. Major defense contractors like Lockheed Martin, Raytheon Technologies, and Northrop Grumman are actively collaborating with U.S. defense agencies, creating a robust ecosystem of innovation, prototyping, and field testing across the region.

By Type Analysis

In 2024, the Hypersonic Glide Vehicle (HGV) segment held a dominant position in the global hypersonic missiles market, capturing more than a 38.7% share. This leadership is attributed to the increasing demand for maneuverable, high-speed weapons capable of evading advanced missile defense systems.

HGVs are launched atop a carrier missile and, after separation, glide unpowered at hypersonic speeds towards their targets, allowing for unpredictable trajectories and reduced detection time. Their ability to maneuver during flight makes them particularly effective against fixed missile defense installations, enhancing their strategic value in modern warfare.

The prominence of the HGV segment is further reinforced by substantial investments in research and development by major military powers. For instance, the United States, China, and Russia have been actively testing and deploying HGV systems to bolster their strategic deterrence capabilities. The integration of advanced materials and guidance systems has been pivotal in enhancing the performance and reliability of these vehicles, making them a focal point of next-generation missile programs.

Moreover, the global security landscape has witnessed a surge in demand for hypersonic capabilities. The ability to deliver swift and precise strikes from great distances serves as a powerful deterrent against potential adversaries. This strategic utility has prompted nations to prioritize the development and deployment of hypersonic glide vehicles.

By Launching Platform Analysis

In 2024, the air-launched segment held a dominant position in the global hypersonic missiles market, capturing more than a 47.8% share. This leadership is attributed to the increasing demand for rapid-response capabilities and the strategic advantage of deploying hypersonic weapons from airborne platforms.

Air-launched hypersonic missiles offer enhanced flexibility, allowing for quick deployment and the ability to strike high-value targets with minimal warning. The integration of these missiles into existing aircraft fleets reduces the need for extensive infrastructure modifications, making them a cost-effective solution for modernizing military arsenals.

The prominence of the air-launched segment is further reinforced by substantial investments in research and development. For instance, the United States has been actively testing the AGM-183A Air-Launched Rapid Response Weapon (ARRW), aiming to enhance its long-range strike capabilities. Similarly, other nations are exploring air-launched hypersonic systems to bolster their defense postures.

Moreover, the air-launched approach mitigates some of the challenges associated with ground or sea-based launches, such as the need for specialized launch platforms or the vulnerability to pre-emptive strikes. By leveraging existing air assets, militaries can achieve a higher degree of operational readiness and adaptability. This versatility is particularly crucial in contested environments where traditional launch methods may be compromised.

By Range Analysis

In 2024, the Long Range (Above 2,000 km) segment held a dominant position in the global hypersonic missiles market, capturing more than a 60.4% share. This leadership is attributed to the strategic emphasis on developing missiles capable of striking distant targets with unprecedented speed and precision.

Long-range hypersonic missiles offer significant advantages in modern warfare, including the ability to penetrate advanced air defense systems and deliver rapid responses over vast distances. Nations are investing heavily in these systems to enhance their deterrence capabilities and maintain a strategic edge in global military dynamics.

The prominence of the Long Range segment is further reinforced by substantial investments in research and development. For instance, the United States has been actively pursuing the development of the Long-Range Hypersonic Weapon (LRHW) system, aiming to bolster its long-range precision strike capabilities. Similarly, other countries are accelerating their hypersonic programs to achieve strategic parity.

Moreover, the global security landscape has witnessed a surge in demand for long-range hypersonic capabilities. The ability to deliver swift and precise strikes from great distances serves as a powerful deterrent against potential adversaries. This strategic utility has prompted nations to prioritize the development and deployment of long-range hypersonic missiles, recognizing their role in shaping future combat scenarios.

By Propulsion Engine Analysis

In 2024, the Liquid and Solid-Fueled Rockets segment held a dominant position in the global hypersonic missiles market, capturing more than a 32.5% share. This leadership is attributed to the established reliability, high thrust-to-weight ratios, and rapid acceleration capabilities of these propulsion systems.

Solid-fueled rockets offer advantages such as simplicity, storability, and quick launch readiness, making them suitable for tactical applications. Liquid-fueled rockets, on the other hand, provide controllable thrust and higher specific impulse, which are beneficial for strategic missions requiring precise maneuvering.

The prominence of this segment is further reinforced by substantial investments in research and development. For instance, North Korea’s Hwasong-16B missile, tested in 2024, utilizes a solid-fueled propulsion system, demonstrating advancements in solid propellant technology.

Similarly, China’s development of the YF-209 liquid-fueled rocket engine, designed for reusability and commercial applications, highlights the ongoing innovation in liquid propulsion systems . These developments underscore the strategic importance of liquid and solid-fueled rockets in modern missile programs.

By Overhead Analysis

In 2024, the Conventional segment held a dominant position in the global hypersonic missiles market, capturing more than a 54.8% share. This leadership is attributed to the increasing demand for precision-guided, non-nuclear strike capabilities that minimize collateral damage.

Conventional hypersonic missiles offer strategic flexibility, allowing for rapid response to emerging threats without the geopolitical ramifications associated with nuclear weapons. Their deployment aligns with modern military doctrines emphasizing proportionality and precision in conflict scenarios.

The prominence of the Conventional segment is further reinforced by substantial investments in research and development. For instance, the United States has been actively pursuing the development of the Long-Range Hypersonic Weapon (LRHW) system, aiming to bolster its long-range precision strike capabilities. Similarly, other countries are accelerating their hypersonic programs to achieve strategic parity.

Moreover, the global security landscape has witnessed a surge in demand for hypersonic capabilities. The ability to deliver swift and precise strikes from great distances serves as a powerful deterrent against potential adversaries. This strategic utility has prompted nations to prioritize the development and deployment of hypersonic missiles powered by reliable propulsion systems.

Key Market Segments

By Type

- Glide vehicle (HGV)

- Cruise missile (HCM)

- Ballistic missile (HBM)

By Launching Platform

- Air launched

- Land launched

- Marine launched

By Range

- Long Range (Above 2000 km)

- Short Range (Up to 1000 km)

By Propulsion Engine

- Liquid and solid-fueled rockets

- Turbojets

- Ramjet

- Ducted rocket

- Scramjet

- Dual-combustion ramjet

By Overhead

- Conventional

- Nuclear

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Rising Geopolitical Tensions Fueling Demand for Hypersonic Missiles

The global hypersonic missile market is experiencing significant growth, driven by escalating geopolitical tensions and the pursuit of strategic military advantages. Nations such as the United States, China, and Russia are heavily investing in hypersonic technologies to enhance their defense capabilities.

These missiles, capable of traveling at speeds exceeding Mach 5, offer rapid response options and are challenging to intercept, making them highly desirable in modern warfare scenarios. The urgency to develop and deploy such weapons is underscored by recent advancements and tests conducted by these countries, reflecting a competitive arms race in hypersonic capabilities.

Furthermore, the integration of hypersonic missiles into existing military platforms is becoming a focal point for defense strategies. For instance, the U.S. Navy’s initiative to retrofit the USS Zumwalt with hypersonic weapons exemplifies the commitment to incorporating these advanced systems into naval operations.

Restraint

High Development and Operational Costs Impeding Market Expansion

Despite the strategic advantages offered by hypersonic missiles, their development and deployment are hindered by substantial financial constraints. The intricate technologies required for hypersonic flight, including advanced propulsion systems and heat-resistant materials, necessitate extensive research and testing, leading to elevated costs.

Moreover, the unit cost of hypersonic missiles remains considerably high compared to traditional missile systems. The Congressional Budget Office estimated that producing 300 units of the AGM-183A Air-launched Rapid Response Weapon (ARRW) would result in a unit cost of approximately $14.9 million per missile.

Opportunity

Technological Innovations and Collaborative Efforts Enhancing Market Potential

The hypersonic missile market presents significant opportunities through technological advancements and international collaborations. Innovations in materials science, propulsion, and guidance systems are paving the way for more efficient and cost-effective hypersonic weapons.

For instance, companies like Stratolaunch have achieved milestones in reusable hypersonic flight testing, demonstrating the feasibility of cost reduction through reusability. These advancements not only improve performance but also make hypersonic technologies more accessible to a broader range of military applications.

Additionally, collaborative programs between nations are accelerating the development of hypersonic capabilities. Joint initiatives, such as the U.S.-Australia SCIFiRE program, exemplify how international partnerships can pool resources and expertise to overcome technical challenges.

Challenge

Overcoming Technical Barriers and Ensuring Operational Reliability

The development of hypersonic missiles is fraught with technical challenges that impact their operational reliability. One significant issue is the thermal stress experienced during hypersonic flight, which can affect the structural integrity of the missile and the functionality of onboard systems.

Managing the extreme heat generated at speeds above Mach 5 requires advanced materials and cooling technologies, which are still under development. These technical hurdles necessitate rigorous testing and validation to ensure mission success.

Furthermore, the integration of hypersonic missiles into existing defense infrastructures poses logistical and strategic challenges. Ensuring compatibility with current launch platforms, command and control systems, and defense doctrines requires comprehensive planning and adaptation.

Growth Factors

Strategic Investments and Geopolitical Imperatives

The hypersonic missile market is witnessing robust growth, driven by significant investments and escalating geopolitical tensions. Nations such as the United States, China, and Russia are allocating substantial resources to develop and deploy hypersonic technologies, aiming to enhance their strategic military capabilities.

These investments are not only focused on research and development but also on integrating hypersonic systems into existing defense infrastructures, thereby reinforcing national security and deterrence postures. The urgency to achieve technological superiority in this domain is further amplified by the rapid advancements and testing successes reported by these countries.

Emerging Trends

Reusability and Collaborative Development

A notable trend in the hypersonic missile sector is the shift towards reusability, aimed at reducing costs and enhancing operational efficiency. Companies like Stratolaunch have achieved significant milestones by successfully conducting multiple hypersonic flight tests using the same reusable Talon-A vehicle.

These advancements demonstrate the feasibility of developing cost-effective hypersonic systems, which can be rapidly deployed and recovered, thereby increasing the frequency of testing and operational readiness. In addition to technological innovations, international collaborations are playing a pivotal role in accelerating hypersonic missile development.

Joint initiatives between allied nations facilitate the sharing of expertise, resources, and technological advancements, thereby overcoming complex challenges associated with hypersonic technologies. Such collaborative efforts not only expedite the development process but also promote standardization and interoperability among allied forces, enhancing collective defense capabilities.

Business Benefits

Enhanced Strategic Capabilities and Market Opportunities

The integration of hypersonic missiles into military arsenals offers significant strategic advantages, including rapid response capabilities and the ability to penetrate advanced defense systems. These attributes make hypersonic weapons highly desirable for modern military operations, where speed and precision are critical.

From a business perspective, the growing demand for hypersonic technologies presents lucrative opportunities for defense contractors and technology firms. Companies engaged in the development of hypersonic systems are poised to benefit from increased government contracts and funding.

For instance, startups like Castelion have secured substantial investments to advance hypersonic missile technologies, reflecting the market’s potential for growth and innovation. This trend underscores the expanding commercial landscape associated with hypersonic missile development.

Key Player Analysis

In the hypersonic missiles market, Aerojet Rocketdyne Holdings Inc plays a critical role with its propulsion systems that support advanced missile development, especially in scramjet and solid rocket motors. The Boeing Company has remained active in research partnerships, contributing to hypersonic vehicle platforms and defense contracts in the U.S. market.

BrahMos Aerospace Pvt. Ltd, a joint venture between India and Russia, continues to advance the BrahMos-II, aiming for Mach 7 speed, showing strong regional growth in South Asia. These firms are actively pushing global capabilities in high-speed missile programs.

Denel Dynamics, a key player from South Africa, supports regional defense modernization by investing in precision missile technologies, including hypersonic capabilities under study. General Dynamics Corporation is focused on system integration for advanced munitions and platforms that may include hypersonic compatibility.

Lockheed Martin Corporation leads the U.S. hypersonic defense landscape with programs like the AGM-183 ARRW and collaborations with DARPA, highlighting its aggressive stance in rapid weapons development. Northrop Grumman Corporation strengthens this effort with key support in sensors and propulsion innovation.

Top Key Players in the Market

- Aerojet Rocketdyne Holdings Inc

- The Boeing Company

- Brahmos Aerospace Pvt. Ltd

- Denel Dynamics

- General Dynamics Corporation

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- J.S.C. Tactical Missiles Corporation

- Raytheon Technologies

- SAAB

- Thales Group

- Others

Recent Developments

- In May 2025, Stratolaunch successfully completed two hypersonic flight tests using its reusable Talon-A vehicle. These tests support the U.S. Department of Defense’s Multi-Service Advanced Capability Hypersonic Test Bed (MACH-TB) program.

- In December 2024, India conducted a successful test of a hypersonic missile developed by the Defence Research and Development Organisation (DRDO). The missile demonstrated capabilities of carrying payloads over 1,500 km at speeds exceeding Mach 5.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 8.5 Bn |

| Forecast Revenue (2034) | USD 29.9 Bn |

| CAGR (2025-2034) | 13.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Type (Glide vehicle (HGV), Cruise missile (HCM), Ballistic missile (HBM)), By Launching Platform (Air launched, Land launched, Marine launched), By Range (Long Range (Above 2000 km), Short Range (Up to 1000 km)), By Propulsion Engine (Liquid and solid-fueled rockets, Turbojets, Ramjet, Ducted rocket, Scramjet, Dual-combustion ramjet), By Overhead (Conventional, Nuclear) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Aerojet Rocketdyne Holdings Inc, The Boeing Company, Brahmos Aerospace Pvt. Ltd, Denel Dynamics, General Dynamics Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, J.S.C. Tactical Missiles Corporation, Raytheon Technologies, SAAB, Thales Group, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |