Quick Navigation

Report Overview

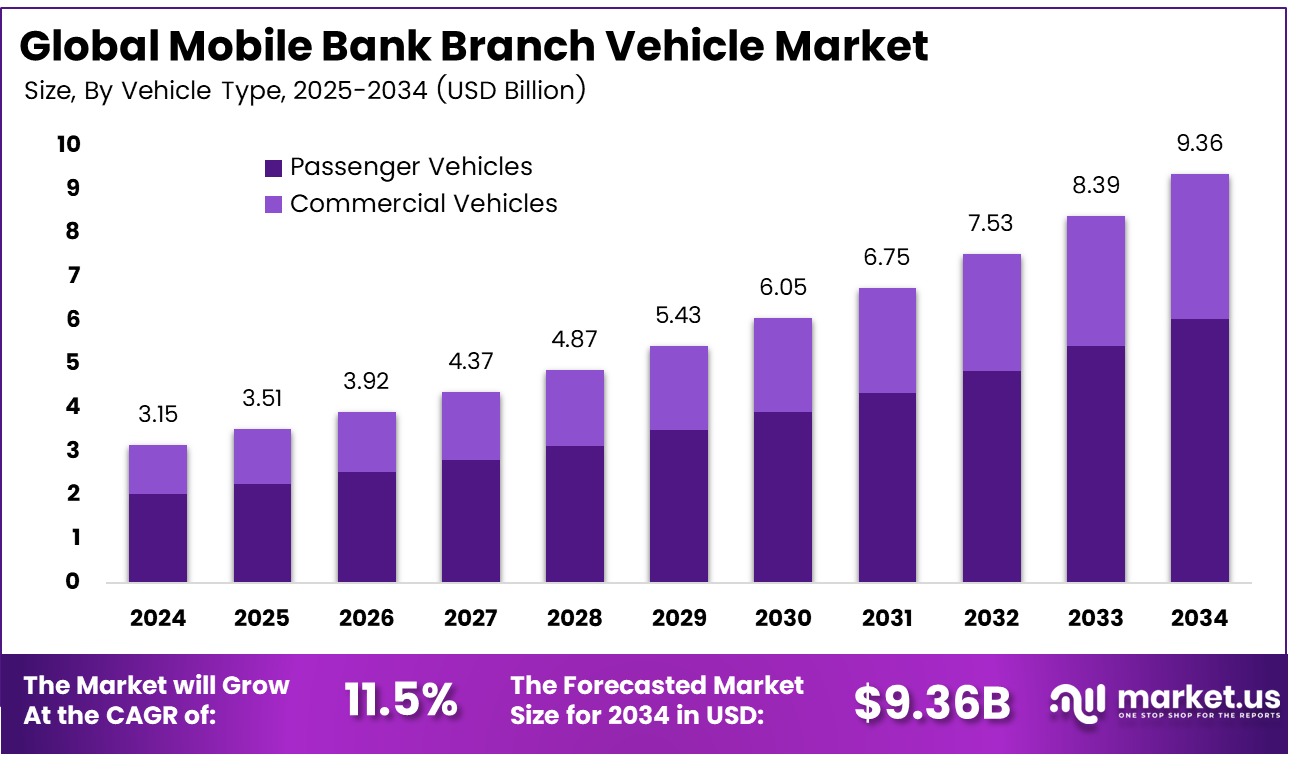

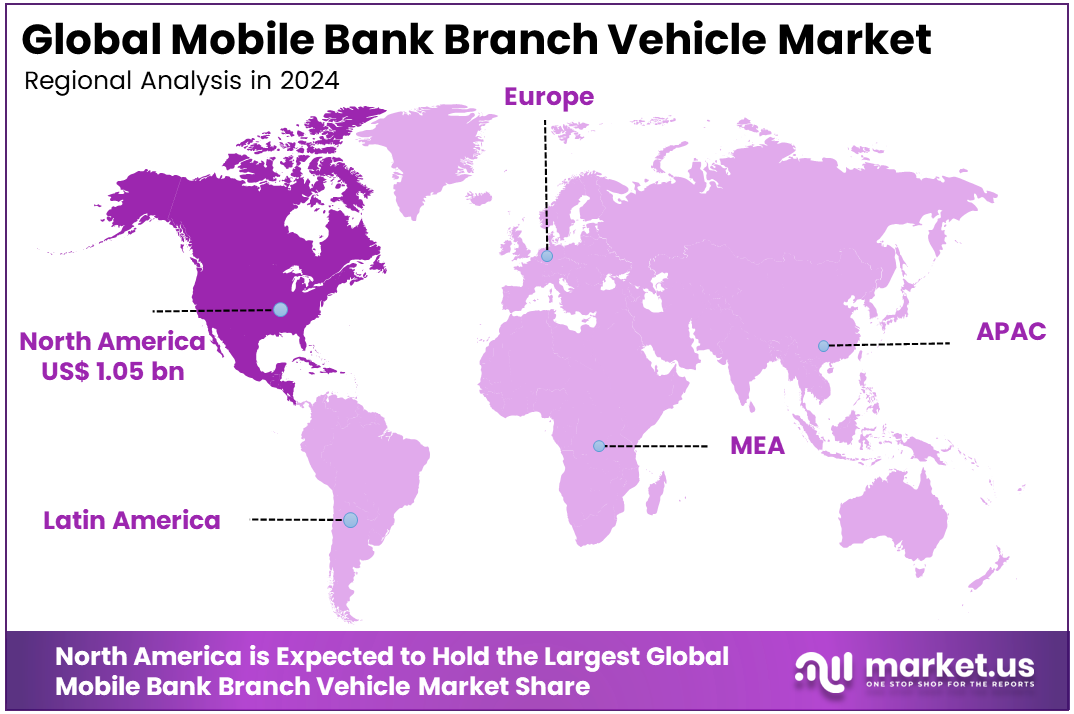

The Global Mobile Bank Branch Vehicle Market size is expected to be worth around USD 9.36 billion by 2034, from USD 3.15 billion in 2024, growing at a CAGR of 11.5% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 33.5% share, holding USD 1.05 billion in revenue.

Mobile bank branch vehicles deliver banking right where people live and work through trucks or vans fitted like small branches. Customers open accounts, deposit cash, withdraw money, and get advice without traveling far. These units park in neighborhoods, markets, or events to serve folks who lack nearby fixed spots. 82% of people still prefer branch access alongside apps, proving vehicles bridge the gap well. They run on generators or batteries for power and link to main systems for real-time updates. Simple design keeps costs low while meeting daily needs effectively.

Rural areas and remote towns lack branches, so vehicles fill that void with easy access to cash services. People save time and travel by handling tasks locally, and 24% expect fewer trips to fixed sites for basics. Natural disasters or roadblocks make them vital for quick recovery aid. Busy urban workers grab services during lunch or events without queues. Population shifts to the outskirts boost the push as banks follow customers. Fuel efficiency and flexible routes cut operating hurdles, too.

The market for mobile bank branch vehicles is driven by the need to deliver full banking services where fixed branches are not practical, especially in rural and semi-urban areas. Banks use these vehicles to open accounts, collect deposits, provide basic lending, and support government and bank programs aimed at improving access to formal finance. Real deployments, such as Bank on Wheels initiatives, show that on-site service can build trust with cash-heavy customers and support community outreach during local events or disruptions while reducing travel time for residents.

Demand grows in spots with poor internet or no branches, where folks need hands-on help for cash and advice. 85.4% of users choose mobile options for round-the-clock reach and less hassle. Seniors and low-tech users rely on them for trust and face-to-face talks. Event-based stops like fairs draw crowds for quick sign-ups. Areas with high unbanked rates see steady pull as vehicles build habits. Travel cuts and wait times drop make them a daily pick over apps.

For instance, in October 2025, Stellar Industries, Inc. ramped up its mobile bank branch vehicle production in Garner, Iowa, by hiring key sales talent and elevating Tim Worman to Director of Product Management. This move sharpens their edge in custom work truck builds for banks reaching rural customers, keeping North American manufacturers ahead in flexible financial outreach.

Key Takeaway

- In 2024, the Passenger Vehicles segment held a dominant market position, capturing a 64.5% share of the Global Mobile Bank Branch Vehicle Market.

- In 2024, the Rural Banking segment held a dominant market position, capturing a 42.7% share of the Global Mobile Bank Branch Vehicle Market.

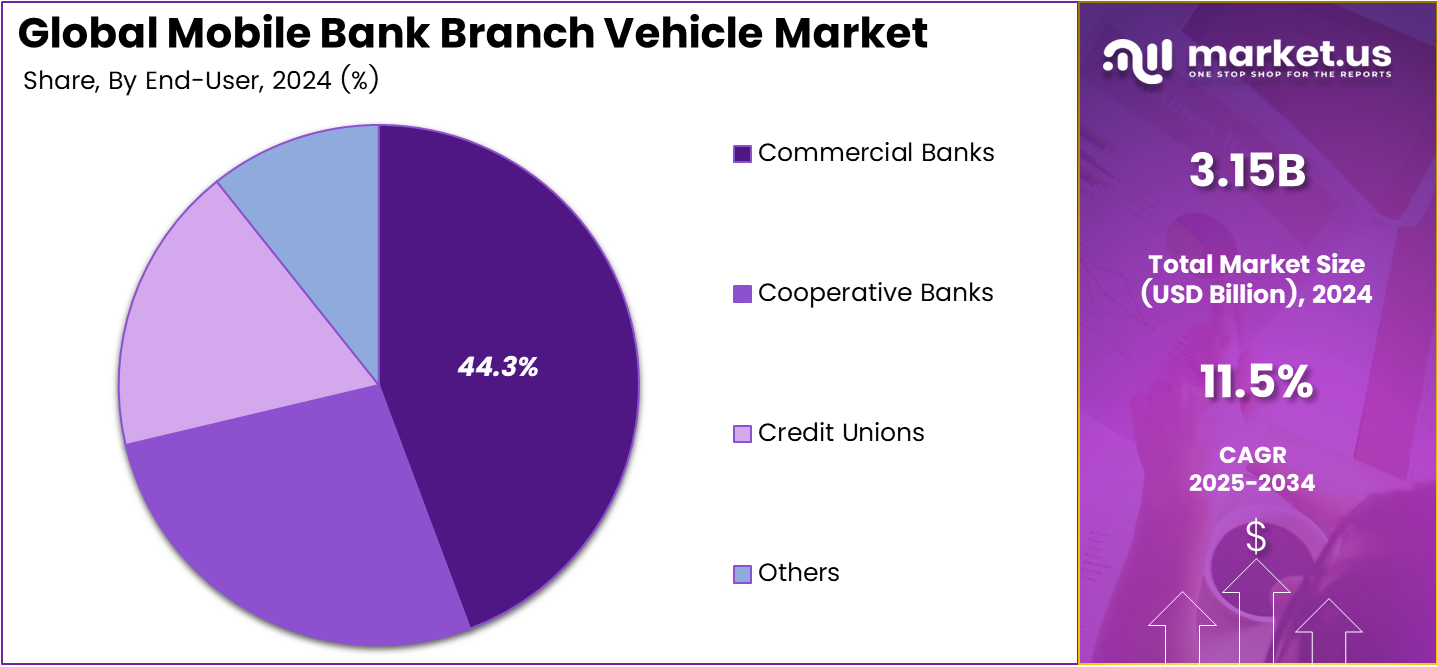

- In 2024, the Commercial Banks segment held a dominant market position, capturing a 44.3% share of the Global Mobile Bank Branch Vehicle Market.

- In 2024, the Diesel segment held a dominant market position, capturing a 40.2% share of the Global Mobile Bank Branch Vehicle Market.

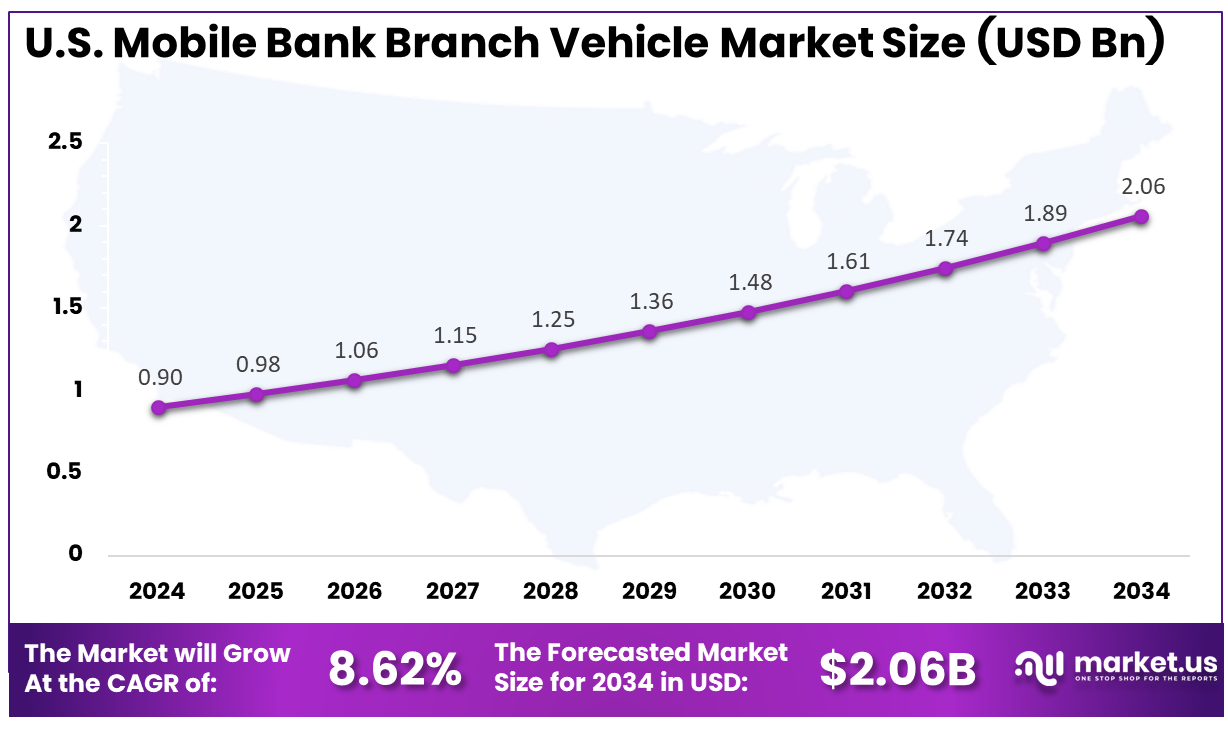

- The U.S. Mobile Bank Branch Vehicle Market was valued at USD 0.90 Billion in 2024, with a robust CAGR of 8.62%.

- In 2024, North America held a dominant market position in the Global Mobile Bank Branch Vehicle Market, capturing more than a 33.5% share.

Role of Generative AI

Generative AI enhances mobile bank branch vehicles by powering voice assistants for quick customer queries and creating instant paperwork for loans or IDs during stops. A Reserve Bank of India report highlights how it boosts banking operations efficiency by up to 46%, freeing staff for personal advice in remote spots. This tech scans fraud patterns on the spot, ensuring safe transactions even off-grid. Banks integrate it via onboard laptops and Wi-Fi, making services smoother and faster for users who value face-to-face help. Overall, AI turns these vehicles into smart, responsive units that adapt to local needs without heavy staffing.

Adoption picks up as AI handles data analysis on the move, with studies noting 73% of bank employee time is open to such automation. It personalizes offers based on quick scans of customer history, building trust in areas slow to go digital. Vehicles equipped with these tools see less wait time, drawing more footfall from hesitant users. Simple interfaces mean even basic smartphone owners benefit, as AI explains options in plain language. This shift eases workload pressures, letting tellers focus on complex cases while tech covers routine tasks effectively.

Investment and Business Benefits

Building custom vehicles with teller spots and ATMs pays off in underserved zones hungry for service. Low entry costs beat full branches, letting fleets expand step by step. Tie-ups for rural outreach or emergency fleets tap reliable demand. Retrofit kits upgrade old vans cheaply for new lines. Maintenance networks grow with parts supply chains. Returns come from steady fees and new accounts in high-need areas.

Vehicles slash expenses on land and staff by serving multiple sites weekly. 52.1% of customers cut time on errands, sticking longer with the bank. On-road chats yield insights for better products and cross-sells. Quick pivots to hot spots grab market share fast. Data from visits sharpens targeting over digital guesses. Teams stay sharp with varied duties, lowering turnover.

Regional Analysis

In 2024, North America held a dominant market position in the Global Mobile Bank Branch Vehicle Market, capturing more than a 33.5% share, holding USD 1.05 billion in revenue. This dominance stems from widespread branch closures in rural US areas, pushing banks to deploy mobile units for essential services like deposits and loans. Strong infrastructure supports efficient routes across vast landscapes, while regulations promote financial inclusion in underserved spots. Banks blend these vehicles with apps to cut costs and reach isolated communities effectively. Demand rises as operators prioritize reliable, on-demand access over fixed builds.

For instance, in November 2025, Stellar Industries Inc. continues dominating mobile specialty vehicle manufacturing with recent advancements in service cranes and power units compatible with EV chassis. Their expertise positions them as key suppliers for mobile bank branches, supporting North American banks’ expansion into rural and underserved areas through reliable, customizable vehicles.

U.S. Mobile Bank Branch Vehicle Market Size

The market for Mobile Bank Branch Vehicle within the U.S. is growing tremendously and is currently valued at USD 0.90 billion; the market has a projected CAGR of 8.62%. The market expands due to rising demand for banking access in rural and underserved areas hit by branch closures. Banks turn to these mobile units to deliver deposits, loans, and ATMs right at community doorsteps, blending physical service with digital tools. Regulatory pushes for financial inclusion fuel adoption, while fuel-efficient designs cut operating costs. Vast landscapes make rolling branches a practical fix for connectivity gaps.

For instance, in October 2025, MBF Industries, Inc. delivered a state-of-the-art 30-foot mobile bank branch on a Freightliner M2-106 chassis to PNC Bank for its Birmingham, Alabama program, launched October 8. This “bank on wheels” brings full banking services, including account openings, loans, and debit cards, directly to underserved neighborhoods on a biweekly route. The custom vehicle enhances community access and financial inclusion, showcasing U.S. leadership in mobile banking innovation.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Vehicle Type Analysis

In 2024, the Passenger Vehicles segment held a dominant market position, capturing a 64.5% share of the Global Mobile Bank Branch Vehicle Market. This dominance is due to their compact size and ability to carry essential banking equipment like teller windows and ATMs. Banks favor them for regular routes to smaller communities where larger trucks face access issues. This choice keeps operations smooth and cost-effective on everyday roads. The setup allows quick deployment without major infrastructure needs.

These vehicles blend reliability with flexibility for banking tasks. Drivers handle daily schedules across varied terrains while keeping passenger comfort in mind for staff. Maintenance stays straightforward, supporting frequent use. Over time, this dominance reflects practical needs over flashy options. Banks see steady returns from such grounded picks in real-world settings.

For instance, in January 2025, Stellar Industries, Inc. showcased new utility-focused chassis options at Work Truck Week that adapt well to passenger vehicle bases for banking. These designs emphasize compact builds with added interior space for teller setups, making them ideal for daily rural routes without sacrificing mobility.

Application Analysis

In 2024, the Rural Banking segment held a dominant market position, capturing a 42.7% share of the Global Mobile Bank Branch Vehicle Market. In these areas, people value personal interactions for services like account openings or loan advice despite digital advances. Mobile units drive straight to villages, saving residents hours on travel. This approach bridges gaps left by distant fixed branches. It fosters trust through direct contact in underserved spots.

The focus on rural needs drives this segment’s lead. Units park at markets or community spots, handling cash transactions on site. Local customs shape service delivery, making it feel tailored. Banks gain loyalty by showing up reliably. This hands-on method proves vital where signals falter or tech literacy lags.

For instance, in April 2025, Mobile Facilities, Inc. delivered a 29-foot mobile branch unit tailored for rural outreach. The vehicle features off-grid power and satellite links to serve remote villages, allowing full deposit and loan services where fixed branches cannot reach.

End-User Analysis

In 2024, the Commercial Banks segment held a dominant market position, capturing a 44.3% share of the Global Mobile Bank Branch Vehicle Market. They deploy these vehicles to extend reach into areas beyond digital coverage, such as farming regions. This tactic builds customer ties without the expense of permanent sites. It balances outreach with efficiency in competitive landscapes. Banks track success through new account growth from these efforts.

These banks integrate mobile units into broader strategies. Staff offers full services, from deposits to financial counseling, right at the doorstep. The model adapts to local demands, keeping operations lean. Over the years, it has proven a smart way to hold ground against fintech rivals. Reliability wins in community-focused banking.

For instance, in September 2025, Farber Specialty Vehicles secured a contract for bank-ready command-style vehicles adaptable for commercial use. These units offer integrated digital kiosks and branding space, helping banks extend services to new customer segments efficiently.

Key Market Segments

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles

- Heavy Commercial Vehicles

By Application

- Rural Banking

- Disaster Relief

- Events & Exhibitions

- Urban Banking

- Others

By End-User

- Commercial Banks

- Cooperative Banks

- Credit Unions

- Others

By Power Source

- Diesel

- Electric

- Hybrid

- Others

Power Source Analysis

In 2024, the Diesel segment held a dominant market position, capturing a 40.2% share of the Global Mobile Bank Branch Vehicle Market. They deliver consistent torque for rugged paths and extended trips between stops. Built-in generators ensure ATMs run during power cuts, a key perk in remote zones. Fuel availability keeps downtime low across routes. Operators appreciate the proven durability in tough conditions.

Diesel’s edge lies in long-range capability and simpler servicing. Vehicles cover more ground per fill-up, cutting refuel stops. This suits schedules packed with multiple villages daily. While greener options emerge, diesel holds firm for now due to infrastructure fit. It matches the practical side of mobile banking demands.

For instance, in February 2025, LDV, Inc. launched a diesel-powered van series with enhanced torque for long-haul banking routes. These models provide reliable fuel efficiency on rough terrain, ensuring uninterrupted ATM operations in power-scarce rural zones.

Emerging Trends

Modern vehicles now include ATMs, cash recyclers, and ramps for wheelchairs, moving past basic teller services to full setups with Wi-Fi for app support. Mobile banking app usage rose 18 points from 2020 to 2023, reaching 57%, so these units blend physical visits with digital guidance seamlessly. Customers expect hybrid options, and vehicles deliver by offering on-site app demos or troubleshooting. This trend fits the push for inclusive service in spots with spotty signals, keeping banking hands-on yet tech-forward.

Contactless payments and AI chatbots drive the next wave, with 48% of users checking apps daily, positioning vehicles as hybrid touchpoints for rural drives. Stronger 5G connections enable faster onboard processing, like instant approvals or video calls to experts. Expect solar panels for off-grid power and eco-friendly designs to match green banking goals. These changes make vehicles vital for areas left behind by pure apps, ensuring no one misses out on modern finance. Staff training on these tools keeps the service warm and reliable.

Growth Factors

Smartphone spread fuels demand, as folks seek banking without long journeys, and ease of use leads with 90.6% influence on adoption per research. Vehicles shine where networks falter, providing direct help that apps alone cannot match. Security matters too, with privacy concerns at 86% impact on choices, so robust checks build lasting trust. Low-cost data plans pair well, letting users start digital habits via vehicle visits. This combo pulls in first-timers who prefer seeing services in action before committing.

Financial inclusion drives further uptake, as local rollouts speed service in remote zones, with life compatibility next at 89.7%. Governments stress outreach, and vehicles answer by parking where need is highest, like farming hamlets. User education sessions onboard turn skeptics into regulars, while simple designs suit all ages. Reliability in bad weather or poor roads adds appeal, making banks responsive to real-life hurdles. These factors together create a steady pull, especially for underserved groups, gaining confidence step by step.

Market Dynamics

Drivers - Financial Inclusion Push

Banks increasingly rely on mobile banking vehicles to extend financial access to remote or underserved areas. These vehicles act as mobile branches, delivering essential services such as account openings, deposits, withdrawals, and loan applications to people who otherwise have no nearby banking infrastructure. This has proven especially useful in rural regions where permanent branches are unviable due to low population density or lack of supporting infrastructure.

Government-led financial inclusion initiatives are accelerating this demand, prompting more banks to invest in mobile service units. These vehicles help meet citizens’ banking needs where physical reach remains limited, often becoming the first touchpoint for formal financial services. Their practicality and impact highlight how grounded customer needs are driving consistent adoption across emerging markets.

For instance, in September 2025, Tata Motors signed a deal with Indian Bank to finance commercial vehicles easily. This helps banks buy mobile units for rural outreach. The move supports more people getting bank services in remote spots. It fits the push to include unbanked areas in finance networks. Banks now reach villages faster with these vehicles.

Restraint - Rise of Digital Banking

As smartphone use spreads and online banking platforms become more reliable, many consumers shift to digital-only channels for everyday transactions. This shift lowers the relevance of physical banking options, including mobile units, especially in urban or semi-urban regions with high digital literacy. With more customers preferring apps for tasks like transfers or bill payments, banks redirect investments toward digital transformation instead of mobile fleets.

The decline in physical visits also leads to branch closures and a shrinking need for in-person banking support. For cost-conscious banks, maintaining mobile vehicles begins to seem redundant when digital alternatives offer faster and cheaper service delivery. Consequently, the continued rise of digital banking presents a major restraint for mobile banking vehicle expansion.

For instance, in October 2025, Stellar Industries grew fast by buying Elliott Equipment for work trucks. Yet digital apps cut the need for physical bank vehicles. Their focus shifts to service accessories as phones handle most banking. Customers use online tools daily, slowing mobile branch demand. Firms adapt to tech trends over road units.

Opportunities - Rural Service Gaps

Large segments of rural and semi-rural populations remain outside the reach of reliable internet or electricity infrastructure, leaving gaps that traditional and digital banking models struggle to fill. Mobile banking vehicles bridge this divide, allowing financial institutions to seamlessly deliver cash, credit, and advisory services even in low-connectivity environments. Their presence builds trust with local communities while supporting government welfare disbursements and agricultural finance programs.

These mobile branches are evolving with features like onboard ATMs, solar-powered systems, and digital kiosks, making them self-sufficient and adaptable to rugged field conditions. As rural commerce grows and demand for quick financial access increases, the continued presence of such vehicles helps banks secure long-term customer loyalty and expand into untapped geographies.

For instance, in January 2025, MSV developed rugged mobile clinics adaptable for rural financial kiosks. Vehicles target connectivity voids with onboard power for cash services. They support agricultural finance in low-infrastructure zones. Evolving designs build loyalty among village customers. Persistent rural needs fuel specialized builds.

Challenges - High Setup Costs

Developing and deploying mobile banking vehicles involves major upfront costs, covering design customization, financial equipment, and onboard technology systems. The complexity of integrating secure networks and digital solutions into each vehicle increases costs, making it a significant hurdle for smaller or regional banks. Additionally, fuel, maintenance, and staff costs further increase the total cost of ownership.

Security represents another key concern, as mobile branches handle cash and sensitive data on the move. Banks must invest in advanced surveillance, compliance systems, and data protection measures, all of which increase operational budgets. These financial and logistical challenges often deter wider adoption, limiting participation mainly to large institutions with deep resources.

For instance, in February 2025, Summit Bodyworks leads in custom medical and outreach vehicles from chassis up. High costs hit as they add tech like ATMs for bank units. Fuel and maintenance strain smaller buyers in this market. Security features raise prices further for mobile ops. Big players push ahead despite budget hurdles.

Key Players Analysis

One of the leading players in September 2025, Mobile Facilities, Inc., upgraded its lineup with new 23– to 40-foot mobile bank branches on Ford and Freightliner chassis, adding wireless security and climate control for standalone ops. These hit rural routes hard, giving ATMs and teller windows where fixed spots can’t go. Their focus on light, easy-drive units keeps U.S. firms leading the pack.

Top Key Players in the Market

- Stellar Industries, Inc.

- Mobile Facilities, Inc.

- Farber Specialty Vehicles

- Matthews Specialty Vehicles

- La Boit Specialty Vehicles

- LDV, Inc.

- Summit Bodyworks

- MSV (Mobile Specialty Vehicles)

- Gerflor Group

- Winnebago Industries, Inc.

- BYD Company Limited

- Isuzu Motors Limited

- Ford Motor Company

- Mercedes-Benz (Daimler AG)

- Nissan Motor Corporation

- Tata Motors Limited

- IVECO S.p.A.

- MAN Truck & Bus AG

- Renault Group

- Volkswagen AG

- Others

Recent Developments

- In May 2025, BankDhofar launched a branded “Bank on Wheels” van across Oman urban and rural zones, but the chassis tech draws from partners like Isuzu Motors for reliable off-grid runs. Loaded with biometrics and Wi-Fi, it handles account opens and loans face-to-face. This shows truck makers like Isuzu fueling global mobile banking growth.

- In November 2025, MBF Industries (MSV Mobile Specialty Vehicles) handed over a 40-foot mobile branch to First Alliance Credit Union, packing full banking services like deposits and loans into one rolling unit. This build targets neighborhoods far from branches, letting members handle everything on-site without trips to town. From their U.S. base, MBF keeps proving why these vehicles make sense for community banks chasing real access.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 3.15 Billion |

| Forecast Revenue (2034) | USD 9.36 Billion |

| CAGR (2025-2034) | 11.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Vehicle Type (Passenger Vehicles, Commercial Vehicles), By Application (Rural Banking, Disaster Relief, Events & Exhibitions, Urban Banking, Others), By End-User (Commercial Banks, Cooperative Banks, Credit Unions, Others), By Power Source (Diesel, Electric, Hybrid, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Stellar Industries, Inc., Mobile Facilities, Inc., Farber Specialty Vehicles, Matthews Specialty Vehicles, La Boit Specialty Vehicles, LDV, Inc., Summit Bodyworks, MSV (Mobile Specialty Vehicles), Gerflor Group, Winnebago Industries, Inc., BYD Company Limited, Isuzu Motors Limited, Ford Motor Company, Mercedes-Benz (Daimler AG), Nissan Motor Corporation, Tata Motors Limited, IVECO S.p.A., MAN Truck & Bus AG, Renault Group, Volkswagen AG, Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |