Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- US Market Size

- North America Growth

- Technology Insights

- Range Insights

- Threat Type Insights

- Domain Insights

- Key Market Segments

- Emerging Trends

- Business Benefits

- Driver

- Restraint

- Opportunity

- Challenge

- Regional Analysis

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

The Global Missile Defense Systems (MMDS) Market size is expected to be worth around USD 51.2 Billion By 2034, from USD 29.7 billion in 2024, growing at a CAGR of 5.6% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 40% share, holding USD 11.88 Billion revenue.

Missile Defense Systems (MMDS) are advanced technologies designed to detect, track, intercept, and neutralize incoming missiles, including ballistic, cruise, and hypersonic types. These systems are integral components of national defense strategies, providing a protective shield against potential missile threats. MMDS encompass various platforms, such as ground-based interceptors, naval defense systems, and space-based sensors, all coordinated through sophisticated command and control networks

The Missile Defense Systems Market (MMDS Market) is experiencing significant growth, driven by increasing defense budgets, technological advancements, and rising geopolitical tensions. The primary drivers of the MMDS market include escalating defense expenditures, advancements in radar and sensor technologies, and the growing prevalence of missile threats.

Nations are increasingly allocating substantial resources to enhance their defense capabilities, leading to the procurement of sophisticated missile defense systems. Additionally, the integration of artificial intelligence and machine learning into these systems has enhanced their effectiveness and adaptability, further propelling market growth.

The demand for MMDS is predominantly influenced by regional security concerns, technological advancements, and defense modernization initiatives. Countries facing heightened security threats are prioritizing the acquisition of advanced missile defense systems to safeguard their territories. The increasing complexity of missile threats necessitates the development and deployment of more sophisticated defense solutions, thereby driving market demand.

Key Takeaways

- The Global Missile Defense Systems (MMDS) Market is projected to reach USD 51.2 Billion by 2034, rising from USD 29.7 Billion in 2024, at a CAGR of 5.6% between 2025 and 2034.

- In 2024, North America dominated the global landscape with over 40% market share, generating nearly USD 11.88 Billion in revenue.

- The U.S. MMDS Market stood at approximately USD 11.2 Billion in 2024 and is forecasted to reach USD 16.1 Billion by 2034, advancing at a CAGR of 3.7%.

- By technology, Weapon Systems lead with a 42% share, highlighting heavy defense investments in interceptors and kinetic kill vehicles.

- Medium-range missile defense systems accounted for 35% of the market, driven by growing threats from tactical ballistic missiles.

- Supersonic missiles represented the top threat type, comprising 45% of deployments due to their increasing use in regional conflicts and strategic deterrence needs.

- The Ground-based segment held the largest domain share at 48%, favored for its cost-effectiveness and rapid deployability across multiple terrains.

Analysts’ Viewpoint

The adoption of technologies such as artificial intelligence, machine learning, and advanced radar systems is transforming the MMDS landscape. These technologies enable real-time threat assessment, precise targeting, and efficient interception of incoming missiles. The incorporation of space-based sensors and satellite communication systems further enhances the capabilities of missile defense systems, making them more effective and reliable.

Nations are adopting MMDS to bolster their defense capabilities, deter potential adversaries, and ensure national security. The ability to intercept and neutralize missile threats provides a strategic advantage, enhancing a nation’s defense posture. Furthermore, the integration of advanced technologies into these systems improves their efficiency and effectiveness, making them more attractive to defense planners.

The MMDS market presents numerous investment opportunities, particularly in the development and production of advanced missile defense technologies. Companies specializing in radar systems, interceptor missiles, and command and control infrastructure stand to benefit from the growing demand for sophisticated defense solutions.

US Market Size

The US Missile Defense Systems (MMDS) Market is valued at approximately USD 11.2 Billion in 2024 and is predicted to increase from USD 13.4 Billion in 2029 to approximately USD 16.1 Billion by 2034, projected at a CAGR of 3.7% from 2025 to 2034.

North America Growth

In 2024, North America held a dominant position in the Missile Defense Systems (MMDS) market, capturing more than a 40% share and generating approximately USD 11.8 billion in revenue. This leadership can be attributed to the United States’ substantial defense budget, which significantly surpasses that of other nations.

Furthermore, North America’s strategic defense alliances, notably with NATO, have facilitated collaborative efforts in missile defense, enhancing interoperability and resource sharing among member nations. The region’s emphasis on innovation and technological advancement continues to drive the evolution of missile defense systems, ensuring that North America maintains its leadership in this critical sector.

Technology Insights

In 2024, the Weapon System segment held a dominant market position in the Missile Defense Systems (MMDS) sector, capturing more than a 42% share. This leadership is primarily attributed to the escalating global demand for advanced interceptors, anti-aircraft missiles, and directed energy weapons, which are integral components of modern missile defense architectures.

The increasing frequency and sophistication of missile threats, including hypersonic and cruise missiles, have necessitated the development and deployment of robust weapon systems capable of neutralizing such advanced threats.

Furthermore, the substantial investments by defense agencies worldwide in upgrading their arsenals to counter evolving missile technologies have significantly bolstered the Weapon System segment’s market share.

For instance, the U.S. Department of Defense has been accelerating the production of Patriot missile systems, leading to a surge in demand for associated components like PAC-3 seekers. Similarly, European nations are enhancing their defense capabilities, with companies like MBDA ramping up production of advanced systems such as the SAMP-T to meet the growing requirements of their military forces.

Range Insights

In 2024, the Medium Range Air Defense (MRAD) system segment held a dominant market position, capturing more than 52.5% of the global air defense system market share. This leadership is primarily attributed to the strategic balance MRAD systems offer between the shorter-range, tactical capabilities of Short Range Air Defense (SHORAD) systems and the extensive coverage provided by Long Range Air Defense (LRAD) systems.

MRAD systems are increasingly favored for their versatility in defending against a wide array of aerial threats, including cruise missiles, unmanned aerial vehicles (UAVs), and aircraft, within a range typically between 1,000 and 3,000 kilometers. The growth of the MRAD segment is further supported by advancements in radar and sensor technologies, which enhance the detection and tracking capabilities of these systems.

Such technological improvements enable MRAD systems to effectively integrate with air, land, and sea-based defense platforms, creating unified defense networks that facilitate coordinated responses to aerial threats. For instance, Poland’s Armed Forces received their first battery of the Wisla medium-range air-defense system in June 2023, demonstrating the increasing adoption of MRAD systems in national defense strategies.

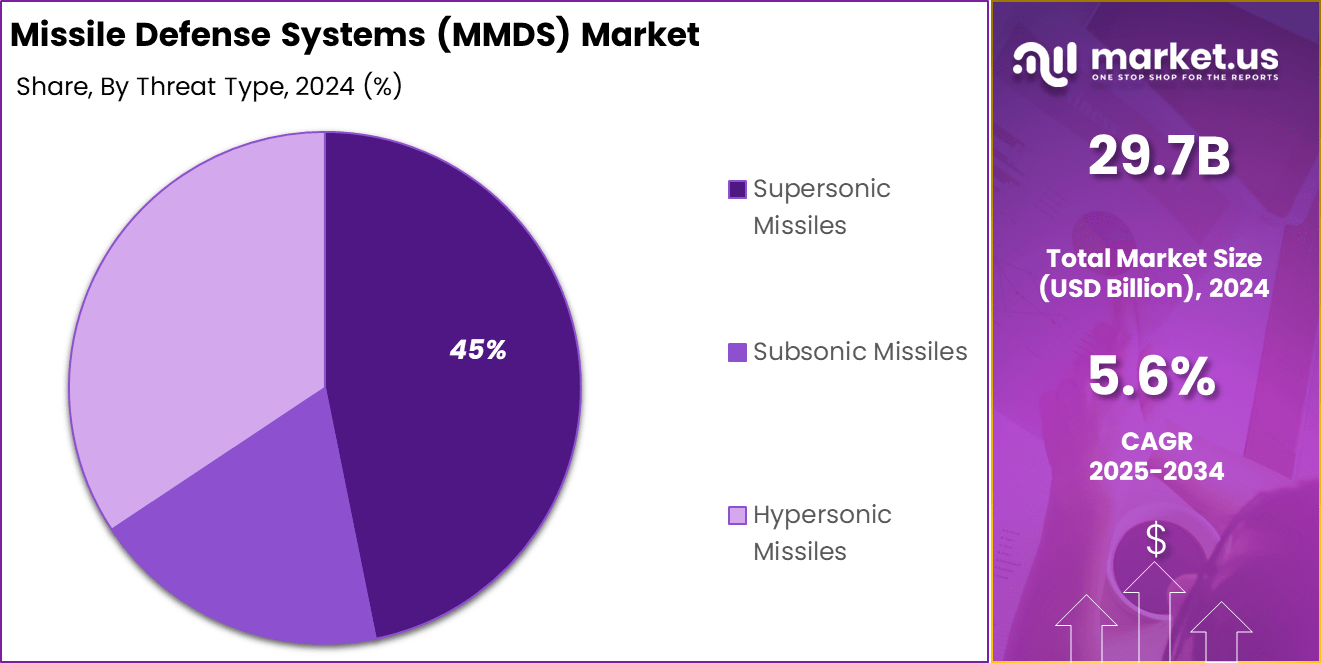

Threat Type Insights

In 2024, the Supersonic Missiles segment held a dominant market position in the Missile Defense Systems (MMDS) sector, capturing more than a 45% share. This leadership is primarily attributed to the widespread deployment and operational effectiveness of supersonic missile systems across various military applications.

Supersonic missiles, characterized by speeds ranging from Mach 2 to Mach 5, offer a balanced combination of speed, range, and maneuverability, making them suitable for a diverse array of missions, including air-to-air combat, anti-ship operations, and precision strikes against ground targets.

The extensive adoption of supersonic missile systems can be observed in several key defense platforms. For instance, the BrahMos missile, a joint venture between India and Russia, has been integrated into the naval, air, and land forces of both nations, demonstrating its versatility and effectiveness.

Similarly, the development of the Super Sonic Strike Missile (3SM) Tyrfing by Kongsberg Defence & Aerospace, intended for deployment by the German and Norwegian navies, underscores the continued investment in supersonic missile technology.

Domain Insights

In 2024, the Ground segment held a dominant market position in the Missile Defense Systems (MMDS) sector, capturing more than a 48% share. This leadership is primarily attributed to the strategic importance of ground-based defense systems in safeguarding critical national infrastructure, military bases, and urban centers from a diverse array of missile threats.

Ground-based systems, encompassing fixed installations, portable units, and vehicle-mounted platforms, offer flexibility and scalability, enabling rapid deployment and integration into existing defense architectures.

The substantial market share of the Ground segment is further supported by ongoing advancements in radar technologies, interceptor capabilities, and command and control systems, which enhance the effectiveness of ground-based missile defense solutions.

For instance, the United States has been actively enhancing its Ground-based Midcourse Defense (GMD) system to counter intercontinental ballistic missile threats, while European nations are investing in advanced systems like the IRIS-T SLM to bolster regional defense capabilities.

Key Market Segments

By Technology

- Fire Control System

- Weapon System

- Countermeasure System

- Command & Control System

By Range

- Short

- Medium

- Long

By Threat Type

- Subsonic Missiles

- Supersonic Missiles

- Hypersonic Missiles

By Domain

- Ground

- FIxed

- Portable

- Vehicle

- Air

- Aircraft

- UAVs

- Marine

- Warships

- Submarine

- Space

- Satellite

Emerging Trends

The Missile Defense Systems (MMDS) market is experiencing significant advancements, driven by the increasing complexity of global missile threats. A notable trend is the integration of Artificial Intelligence (AI) and Machine Learning (ML) into defense systems. These technologies enhance real-time decision-making, predictive maintenance, and threat analysis, thereby improving the efficiency and responsiveness of missile defense operations.

Another emerging trend is the emphasis on interoperability and network-centric warfare. Modern defense strategies prioritize systems that can seamlessly integrate with allied forces, enabling coordinated responses to missile threats. This approach is exemplified by initiatives like the European Sky Shield Initiative, which aims to create a unified air defense network across multiple nations.

Business Benefits

Investing in advanced Missile Defense Systems offers substantial business benefits, particularly in the defense and aerospace sectors. The growing demand for sophisticated defense solutions has opened avenues for companies to develop and deploy cutting-edge technologies, leading to increased revenue streams.

Furthermore, partnerships between governments and private enterprises facilitate research and development, driving innovation and technological advancements within the industry. Additionally, the strategic importance of missile defense systems enhances the geopolitical influence of nations investing in such technologies. By establishing robust defense capabilities, countries can bolster their security, deter potential adversaries, and strengthen alliances.

Driver

Escalating Global Missile Threats

The growth of the Missile Defense Systems (MMDS) market is primarily driven by the increasing sophistication and frequency of missile threats worldwide. Nations such as China, Russia, and North Korea have significantly advanced their missile capabilities, including the development of hypersonic missiles that travel at speeds exceeding Mach 5.

Furthermore, the proliferation of unmanned aerial vehicles (UAVs) and cruise missiles has expanded the spectrum of aerial threats, necessitating the deployment of comprehensive and integrated missile defense systems. The United States’ proposed “Golden Dome” initiative exemplifies this trend, aiming to establish a multi-layered defense architecture capable of countering diverse missile threats.

Restraint

High Development and Operational Costs

Despite the pressing need for advanced missile defense systems, their development and deployment are hindered by substantial financial constraints. The research, development, testing, and maintenance of sophisticated missile defense technologies require significant investment, often amounting to billions of dollars. For instance, the United States’ “Golden Dome” project is estimated to cost up to $175 billion, raising concerns about its affordability and sustainability.

Moreover, the high unit costs of interceptor missiles, such as the Standard Missile-3 (SM-3), which can range from $10 million to nearly $30 million per unit, further exacerbate budgetary pressures. These financial challenges are particularly acute for developing nations, which may struggle to allocate sufficient resources for the acquisition and maintenance of advanced missile defense systems, thereby limiting market growth in certain regions.

Opportunity

Integration of Artificial Intelligence and Advanced Technologies

The integration of artificial intelligence (AI) and machine learning (ML) into missile defense systems presents significant opportunities for market expansion. AI-powered algorithms enhance threat detection, tracking, and interception capabilities by processing vast amounts of data in real-time, enabling quicker and more accurate responses to missile threats.

Additionally, advancements in directed energy weapons (DEWs), such as high-energy lasers, offer cost-effective alternatives to traditional kinetic interceptors. DEWs can engage multiple targets with minimal operational costs, providing a scalable solution to counter a wide array of missile threats. The ongoing research and development in these areas are expected to drive innovation and open new avenues for growth in the missile defense systems market.

Challenge

Technological Complexity and Integration Issues

The development of missile defense systems involves the integration of various complex technologies, including radar systems, interceptors, command and control units, and communication networks. Ensuring seamless interoperability among these components is a significant technical challenge, often leading to delays and increased costs.

Furthermore, the rapid evolution of missile technologies necessitates continuous upgrades and adaptations of defense systems to maintain efficacy. This dynamic environment requires sustained investment in research and development, as well as the flexibility to incorporate emerging technologies, such as AI and DEWs, into existing defense architectures. Addressing these challenges is crucial for the successful deployment and operation of effective missile defense systems.

Regional Analysis

Europe

Europe ranks as the second-largest market for MMDS, driven by collaborative defense initiatives and a collective commitment to enhancing regional security. The European Sky Shield Initiative, launched in 2022, exemplifies this unified approach, with 24 European countries participating as of 2025. This initiative aims to establish a ground-based integrated European air defense system, including anti-ballistic missile capabilities.

Germany’s procurement of the Arrow 4 missile system in May 2025 is a significant contribution to this collective defense effort, providing a high-altitude defense layer that complements existing systems like IRIS-T SLM and Patriot.

Asia-Pacific (APAC)

The Asia-Pacific region is experiencing rapid growth in the MMDS market, projected to exhibit the highest compound annual growth rate (CAGR) from 2025 to 2030. This surge is primarily driven by escalating geopolitical tensions, particularly concerning territorial disputes in the South China Sea and the Korean Peninsula.

Nations such as Japan, South Korea, and India are intensifying their defense capabilities through the acquisition and development of advanced missile defense systems. India’s procurement of the S-400 Triumf missile defense system from Russia, valued at over USD 5.5 billion, underscores the region’s commitment to enhancing its defense infrastructure.

Latin America

In Latin America, the MMDS market remains relatively nascent but is gradually expanding due to increasing concerns over regional security and the proliferation of missile technologies. Countries such as Brazil and Argentina are exploring opportunities to bolster their defense capabilities through the acquisition of advanced missile defense systems.

Collaborations with international defense contractors and participation in regional defense initiatives are expected to drive the growth of the MMDS market in this region. However, economic constraints and political considerations may influence the pace of development and adoption of such systems.

Middle East and Africa (MEA)

The Middle East and Africa region presents a complex landscape for the MMDS market, characterized by varying levels of defense spending and strategic priorities. Countries like Saudi Arabia and the United Arab Emirates have made significant investments in advanced missile defense systems, such as the THAAD and Patriot systems, to counter perceived threats from regional adversaries.

These investments are part of broader efforts to modernize military capabilities and enhance national security. Conversely, nations in sub-Saharan Africa exhibit limited engagement in the MMDS market, primarily due to economic constraints and competing development priorities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

RTX Corporation, through its Raytheon division, has significantly advanced missile defense capabilities. In May 2025, Raytheon delivered the 13th AN/TPY-2 radar to the U.S. Missile Defense Agency. This radar features Gallium Nitride (GaN) technology, enhancing sensitivity, range, and surveillance capacity, and supports hypersonic missile defense missions.

Boeing continues to strengthen its missile defense portfolio. In July 2024, Boeing announced the acquisition of Spirit AeroSystems, aiming to enhance its defense and commercial operations . Boeing’s missile defense systems include the Aegis Ballistic Missile Defense, Avenger, and Ground-based Midcourse Defense.

Lockheed Martin has made notable strides in missile defense. In March 2025, the U.S. Army awarded Lockheed Martin a contract worth up to $4.94 billion to produce Precision Strike Missiles (PrSM), set to replace the Army Tactical Missile System (ATACMS).

Top Key Players Covered

- RTX Corporation

- The Boeing Company

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- MBDA Inc.

- BAE Systems plc

- Tactical Missile Corporation

- Israel Aerospace Industries Ltd.

- ASELSAN A.S.

- Kongsberg Gruppen ASA

- Saab AB

- Rheinmetall AG

- Roketsan A.S.

- Defense Research and Development Organization (DRDO)

- Others

Recent Developments

- May 2025: Northrop Grumman invested $50 million into Firefly Aerospace to advance the production of their co-developed medium launch vehicle, named Eclipse. This collaboration combines Northrop’s Antares platform with Firefly’s Alpha rocket technology, aiming to enhance launch capabilities for defense applications.

- May 2025: The U.S. Department of Defense increased Palantir’s contract for the Maven Smart System (MSS) from $480 million to nearly $1.3 billion through 2029. This expansion reflects growing demand for advanced data analytics and AI-driven decision-making tools in missile defense operations.

- January 2025: The Pentagon directed the Missile Defense Agency to cease development of the AN/TPY-6 radar intended for Guam’s missile defense. Instead, efforts will focus on integrating existing systems like Aegis, THAAD, and LTAMDS to enhance the island’s defense architecture against evolving threats.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 29.7 Bn |

| Forecast Revenue (2034) | USD 51.2 Bn |

| CAGR (2025-2034) | 5.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Technology (Fire Control System, Weapon System, Countermeasure System, Command & Control System), By Range (Short, Medium, Long), By Threat Type (Subsonic Missiles, Supersonic Missiles, Hypersonic Missiles), By Domain (Ground (Fixed, Portable, Vehicle), Air (Aircraft, UAVs), Marine (Warships, Submarine), Space (Satellite)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | RTX Corporation, The Boeing Company, Lockheed Martin Corporation, Northrop Grumman Corporation, MBDA Inc., BAE Systems plc, Tactical Missile Corporation, Israel Aerospace Industries Ltd., ASELSAN A.S., Kongsberg Gruppen ASA, Saab AB, Rheinmetall AG, Roketsan A.S., Defense Research and Development Organization (DRDO), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |