Quick Navigation

Report Overview

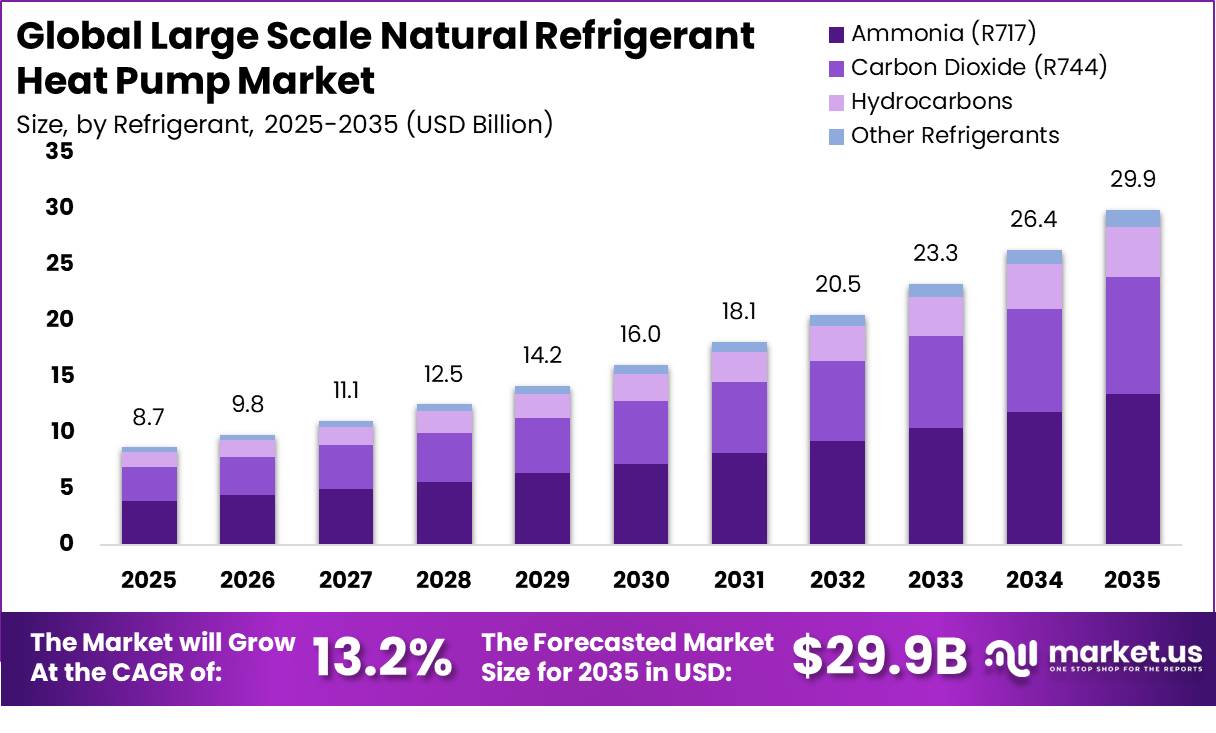

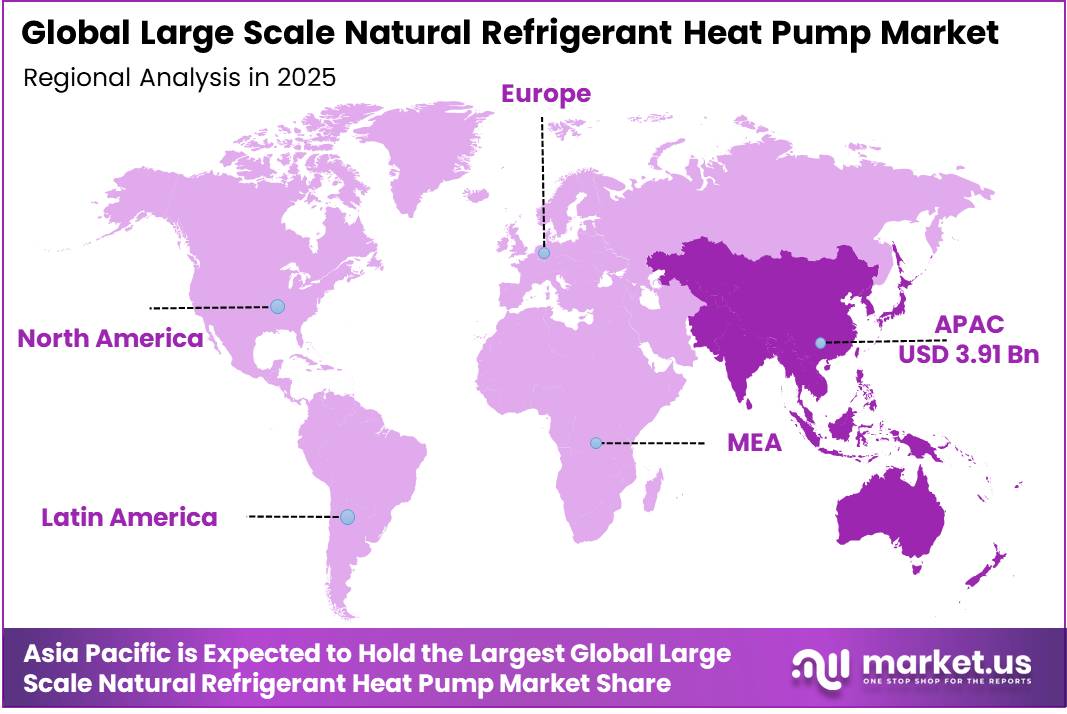

In 2025, the Global Large Scale Natural Refrigerant Heat Pump Market was valued at USD 8.7 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 13.2%, reaching about USD 29.9 billion by 2035. In 2025, Asia Pacific led the market, achieving over 45.0% share with a revenue of USD 3.91 billion.

Large-scale natural refrigerant heat pumps have emerged as an important technology within the global energy transition, offering an efficient and environmentally sustainable solution for industrial and commercial heating applications. These systems utilize natural refrigerants such as ammonia (R717), carbon dioxide (R744), and hydrocarbons, which have significantly lower global warming potential compared to conventional synthetic refrigerants.

- In May 2022, the European Union’s REPowerEU Plan aims to accelerate the deployment of clean heating technologies and reduce dependence on fossil fuels. Under this initiative, the European Commission set a target to deploy 10 million additional heat pumps by 2027 as part of broader efforts to improve energy security and reduce carbon emissions.

Key Takeaways

- In 2025, the Global Large Scale Natural Refrigerant Heat Pump Market was valued at USD 8.7 billion.

- The global market is projected to grow at a CAGR of 13.2% and is estimated to reach USD 29.9 billion by 2035.

- In 2025, the Ammonia (R717) segment dominated the market by refrigerant, accounting for 45.0% of the total market share.

- In 2025, the 201–500 kW segment held the leading position in the market by capacity, capturing 40.0% of the total share.

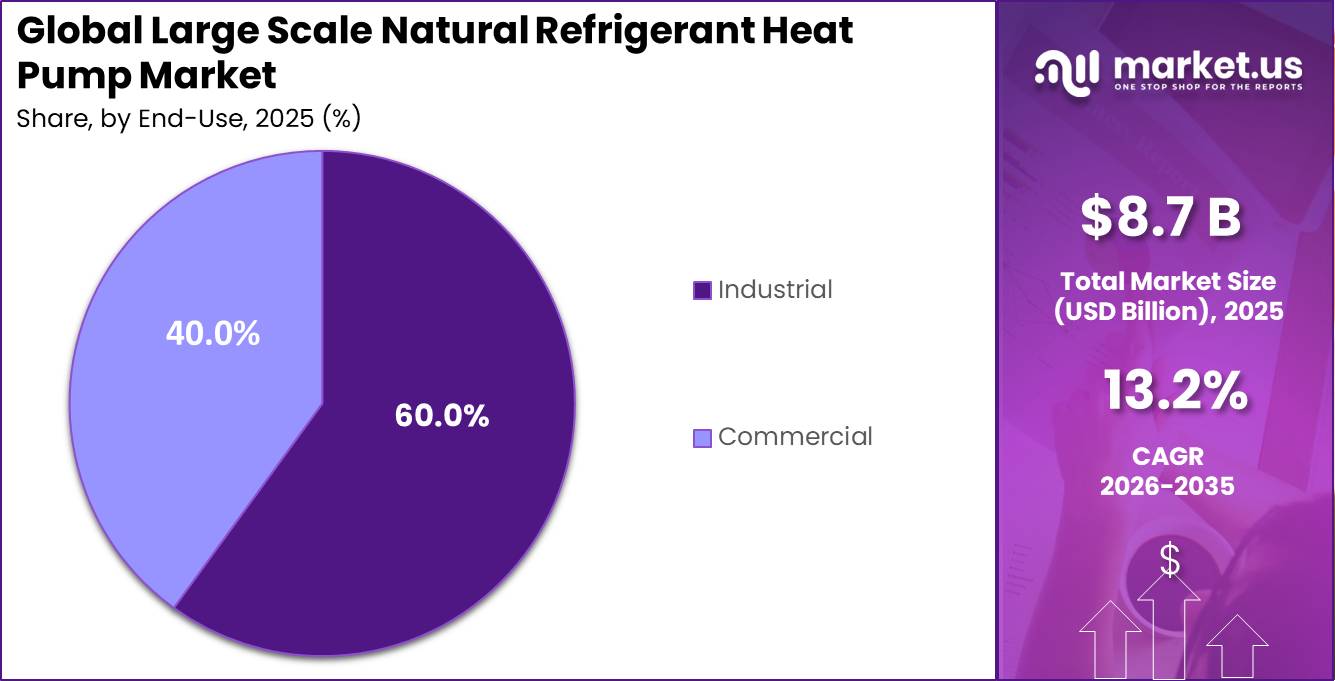

- In 2025, the Industrial segment emerged as the dominant end-use category, representing 60.0% of the market.

- In 2025, Asia Pacific led the global market, securing 45.0% of the total market share and generating approximately US$3.91 billion in revenue.

Industries such as food processing, chemicals, district heating, pharmaceuticals, paper, and manufacturing are increasingly replacing fossil-fuel-based heating systems with heat pumps powered by renewable electricity.

- According to the International Renewable Energy Agency (IRENA), global renewable power capacity increased by 585 GW in 2024 creating a stronger foundation for electrified heating technologies.

Advancements in high-temperature heat pump technology, combined with supportive policy frameworks and increasing renewable electricity availability, are expected to strengthen market adoption. As industries pursue long-term energy efficiency and emissions reduction goals, large-scale natural refrigerant heat pumps are anticipated to play an increasingly important role in the global sustainable heating ecosystem.

Market Segmentation

Refrigerant Analysis

Ammonia (R717) dominates due to its high efficiency in large-scale industrial heating applications

In 2025, Ammonia (R717) held a dominant market position, capturing more than a 45.0% share of the Large Scale Natural Refrigerant Heat Pump Market by refrigerant. The segment maintained its leadership due to ammonia’s excellent thermodynamic performance, high energy efficiency, and suitability for large-capacity heating systems. It has been widely adopted across industrial sectors where reliable and efficient heat generation is critical. Ammonia-based heat pumps are capable of delivering high-temperature output while maintaining lower operating costs, making them a preferred choice for large-scale installations.

In 2025, Carbon Dioxide (R744) is the fastest-growing segment in the Large Scale Natural Refrigerant Heat Pump Market by refrigerant due to its environmental benefits, including an extremely low global warming impact and compliance with evolving refrigerant regulations. Carbon dioxide-based heat pumps have gained increasing acceptance in commercial and industrial applications because they can efficiently provide heating, hot water, and process heat while supporting sustainability goals. Growing investments in low-carbon heating technologies and the expansion of district heating projects further contributed to the segment’s rapid growth during 2025.

Capacity Analysis

201–500 kW dominates market as it offers an ideal balance between capacity and efficiency

In 2025, 201–500 kW held a dominant market position, capturing more than a 40.0% share of the market by capacity, due to its suitability for a wide range of industrial and commercial heating applications. Systems within this capacity range provide sufficient heating output for manufacturing facilities, food processing plants, district heating networks, and large commercial buildings while maintaining operational efficiency and manageable installation costs.

As organizations continued to focus on energy-efficient heating solutions and emissions reduction initiatives during 2025, the 201–500 kW segment remained the preferred choice for many large-scale heating projects, strengthening its dominant position in the market.

501–1,000 kW is the fastest-growing segment in the market by capacity. The segment witnessed strong growth as industries increasingly sought higher-capacity heating systems capable of supporting large-scale operations and energy-intensive processes. These systems are well suited for district heating projects, industrial manufacturing facilities, chemical plants, and other applications requiring substantial and continuous heat output. Growing investments in industrial decarbonization and the transition away from fossil-fuel-based heating technologies contributed significantly to the segment’s expansion.

End Use Analysis

Industrial dominates market driven by growing demand for sustainable process heating.

In 2025, Industrial held a dominant market position, capturing more than a 60.00% share of the Large Scale Natural Refrigerant Heat Pump Market by end-use. The segment’s leadership was supported by the increasing adoption of energy-efficient heating technologies across manufacturing, food processing, chemical production, paper, and other industrial sectors. Large-scale natural refrigerant heat pumps have become an attractive solution for industrial facilities seeking to reduce carbon emissions, lower energy consumption, and comply with evolving environmental regulations.

In 2025, Commercial is the fastest-growing segment in the market by end-use. The segment experienced notable growth due to increasing investments in sustainable heating solutions across commercial buildings, hotels, healthcare facilities, educational institutions, shopping centers, and office complexes. Building owners and operators increasingly adopted natural refrigerant heat pumps to improve energy efficiency, reduce operating costs, and meet environmental sustainability goals.

List of Segments

By Refrigerant

- Ammonia (R717)

- Carbon Dioxide (R744)

- Hydrocarbons

- Other Refrigerants

By Capacity

- 20–200 kW

- 201–500 kW

- 501–1,000 kW

- Above 1,000 kW

By End-Use

- Industrial

- Commercial

Driver Analysis

Industrial electrification and waste-heat recovery improving project IRR

The JRC reports industrial heat pumps below 140°C at TRL 8 or higher, while systems up to 100°C could serve about 11% of Europe’s industrial process heat demand and technologies reaching 200°C could unlock another 26%; separate market evidence indicates high-temperature heat pumps can address roughly 37% of European industrial process heat demand below 200°C. That matters financially because a heat pump with COP near 3 delivers roughly three units of heat per unit of electricity in suitable lift conditions, making waste-heat recovery projects viable where electricity-to-gas price ratios, carbon costs, or fuel-switch incentives support payback.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| F-gas and PFAS transition accelerating natural refrigerant adoption | +2.8% | EU core, UK spill-over, North America selective, Japan/Korea advanced | Short term (≤ 2 years) |

| Industrial electrification and waste-heat recovery improving project IRR | +2.4% | EU industrial belt, U.S. manufacturing states, China coastal clusters, India selective | Medium term (2-4 years) |

| District heating decarbonization creating utility-scale heat pump demand | +2.1% | Nordics, Germany, Netherlands, France, Poland, Baltics | Medium term (2-4 years) |

| High-temperature and steam-capable systems expanding process fit | +1.9% | EU food/paper/chemicals, U.S. process industries, APAC export manufacturing hubs | Medium term (2-4 years) |

| Energy security and gas displacement supporting capex decisions | +1.6% | Europe core, Japan, Korea, import-dependent APAC markets | Short term (≤ 2 years) |

| EU manufacturing, funding, and installer ecosystem reducing execution risk | +1.3% | EU core, CEE expansion corridors | Long term (≥ 4 years) |

Restraint Analysis

Component concentration

A second structural brake is concentration in critical upstream hardware especially compressors, power electronics, heat exchangers, controls, and pressure-rated vessels because the 2026 heat-pump outlook explicitly flags supply-chain diversification as a strategic priority and identifies policy design and industrial competitiveness as limiting factors, while trade activity continues to rise and future growth is expected to concentrate in emerging economies that are also competing for the same manufacturing base.

For large-scale natural refrigerant systems, the concentration problem is sharper than for residential units: ammonia and CO2 platforms require narrower supplier qualification, longer factory acceptance cycles, and thicker engineering content, so a disruption that adds even 8–14 weeks to compressor or gas-cooler delivery can push total project lead times from roughly 9–12 months to 14–18 months, lock up working capital through milestone payments, and raise EPC contingency budgets by 3–6% of project value; the business impact is slower backlog conversion, missed district-heating construction windows, and lower manufacturer gross margin as firms carry dual-sourcing, buffer inventory, and localization costs, together translating into an estimated 1.8-point drag on baseline CAGR over the medium term.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-cost disadvantage | -2.2% | EU core, UK, parts of APAC | Short term (≤ 2 years) |

| Component concentration | -1.8% | EU, North America, APAC export corridors | Medium term (2-4 years) |

| Safety/code compliance drag | -1.5% | EU, North America core, dense urban APAC | Medium term (2-4 years) |

| Tariff and metals inflation | -1.3% | North America core, EU import channels | Short term (≤ 2 years) |

| District-heat project latency | -1.9% | Nordics, Germany, Benelux, East Asia cities | Medium term (2-4 years) |

| Demand visibility and subsidy risk | -1.6% | Europe, US, developed APAC | Short term (≤ 2 years) |

Opportunity Analysis

Data center heat monetization

This is an opportunity rather than a baseline driver because most current market forecasts already assume general decarbonization, refrigerant transition, and building electrification, but they do not fully capture a dedicated go-to-market pivot in which large natural refrigerant heat pump vendors sell integrated waste-heat-upgrading systems into the fast-growing data center buildout and then monetize not only equipment but heat offtake, controls, and long-term service revenue. The upside is material because reused data center heat could supply around 300 TWh of heating demand by 2030, equivalent to roughly 10% of European space-heating demand, while the cost to capture and supply that heat has been cited at EUR 190,000-250,000 per MW supplied versus more than EUR 730,000 per MW for new unabated gas CHP, creating room for a 15-25% lower delivered-heat cost proposition in dense urban clusters and supporting an estimated 1.5-2.0x increase in project IRR where OEMs secure heat-purchase contracts alongside equipment sales.

The real white space is that Germany and the Netherlands are moving toward heat recovery integration for new data centers and the EU Energy Efficiency Directive requires large data centers above 1 MW to implement waste-heat recovery unless unjustified, which creates a pipeline that can be captured through specialist district-energy partnerships rather than ordinary HVAC procurement; if even 3-5% of the 300 TWh recoverable pool is converted via large-scale natural refrigerant systems at average project intensities of 8-20 MWth, the addressable installed-equipment layer alone can plausibly open several billion dollars of incremental TAM beyond conventional commercial and industrial replacement cycles.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Data center heat monetization | +2.4% | Nordics, Germany, Netherlands, UK, North America core | Short term (≤ 2 years) |

| District heat platform bundling | +2.1% | EU core, Japan, South Korea, China tier-1 cities | Medium term (2-4 years) |

| High-temp food & beverage retrofits | +1.8% | EU, India, ANZ, Southeast Asia | Short term (≤ 2 years) |

| Heat-as-a-service financing | +1.6% | North America, EU, APAC emerging markets | Short term (≤ 2 years) |

| Fertilizer & PtX thermal integration | +1.4% | Middle East, India, Australia, North Africa | Medium term (2-4 years) |

| Flexibility stack with thermal storage | +1.3% | Denmark, Germany, Nordics, UK, selected US ISOs | Long term (≥ 4 years) |

Challenges Analysis

Natural Refrigerant Talent Gap

The most persistent execution risk is not demand formation but the shortage of engineers, controls specialists, commissioning teams, and safety-certified technicians able to design and deploy large ammonia, CO₂, and propane-based heat pump systems at industrial scale; this matters because natural refrigerants require tighter competence in charge management, hazard zoning, leak detection, pressure management, and thermodynamic optimization than legacy HFC equipment, and the workforce pipeline is not expanding fast enough to match the transition.

Europe alone is projected to require more than 500,000 additional trained heat pump professionals by 2030, while the broader energy labor market is already showing a 16% rise in demand for applied technical workers between 2015 and 2022 versus only 9% growth in relevant vocational graduations, creating a realistic 2026 project-level bottleneck of 3 to 6 months in engineering sign-off, 8 to 14 weeks in commissioning queue times, and 2 to 4 percentage points of avoidable underperformance in first-year system COP due to weak control tuning and operator familiarization; the resulting CAGR drag of about -1.4 percentage points reflects delayed project conversion rather than cancelled demand, and mitigation now requires OEM-led academies, bundled EPC-service models, remote diagnostics layers, standardized training around F-gas transition obligations, and tighter cross-skilling between refrigeration, boiler replacement, and industrial process-heat teams.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Natural Refrigerant Talent Gap | -1.4% | EU core, North America retrofit clusters, APAC industrial zones | Medium term (2-4 years) |

| Compressor Supply Concentration | -1.2% | EU manufacturing base, China export chains, North America project markets | Medium term (2-4 years) |

| Safety Code Harmonization Lag | -0.9% | EU regulatory hubs, US/Canada code jurisdictions, advanced APAC markets | Long term (≥ 4 years) |

| Grid And Permitting Delays | -1.1% | Europe district heating nodes, North America industrial corridors, dense APAC metros | Medium term (2-4 years) |

| Performance Integration Complexity | -1.0% | Industrial retrofit markets, public infrastructure projects, cold-climate regions | Medium term (2-4 years) |

| Compliance And Reporting Burden | -0.7% | EU core, multinational OEM footprints, import-dependent markets | Short term (≤ 2 years) |

Geopolitical Impact Analysis

Geopolitical Tensions Influencing Energy Transition and Heat Pump Demand.

The ongoing Russia–Ukraine war and continued instability in parts of the Middle East, have had a noticeable impact on the Large Scale Natural Refrigerant Heat Pump Market. These events have increased concerns about energy security, fuel supply reliability, and long-term dependence on imported fossil fuels. As a result, governments, utilities, and industrial operators are accelerating investments in energy-efficient heating technologies that can reduce exposure to volatile energy markets.

The Russia–Ukraine conflict has reshaped energy strategies across many countries, especially in Europe, where efforts to reduce reliance on imported natural gas have intensified. This shift has encouraged greater adoption of electrified heating systems, including large-scale natural refrigerant heat pumps, which offer lower emissions and improved energy efficiency. At the same time, geopolitical uncertainty has contributed to fluctuations in energy prices, affecting project costs and investment decisions across industrial sectors.

Conflicts in the Middle East have also increased concerns over global energy supply routes and fuel market stability. These developments have strengthened interest in technologies that support domestic energy resilience and reduce fuel consumption. While supply chain disruptions and higher equipment costs have created short-term challenges for manufacturers and project developers, the overall market outlook remains positive. The ongoing focus on energy independence, carbon reduction, and sustainable heating solutions is expected to support continued demand for large-scale natural refrigerant heat pumps in industrial and commercial applications worldwide.

Regional Analysis

Asia-Pacific dominates market supported by industrial growth and clean heating investments

Asia-Pacific dominated the Large Scale Natural Refrigerant Heat Pump Market in 2025, accounting for 45.0% of the global market share and generating approximately USD 3.91 billion in revenue. The region’s strong position is supported by its extensive industrial base, growing commercial infrastructure, and increasing focus on energy-efficient heating solutions. Industries such as food processing, chemicals, manufacturing, district heating, and refrigeration have increasingly adopted large-scale natural refrigerant heat pumps to improve energy efficiency and reduce emissions.

Europe represents a significant market due to its strong commitment to carbon reduction and clean heating initiatives. The region has witnessed increasing adoption of natural refrigerant heat pumps in industrial facilities, district heating projects, and commercial buildings. North America is also experiencing steady growth, supported by rising investments in energy-efficient technologies and industrial sustainability programs. Large industrial users are increasingly exploring advanced heating systems to reduce operational emissions and improve long-term energy performance.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global Large Scale Natural Refrigerant Heat Pump Market is characterized by a moderately consolidated market structure, where a relatively small group of established manufacturers holds a significant share of the market. The industry is driven by technological expertise, system efficiency, project execution capabilities, and long-term customer relationships. Due to the technical complexity of large-scale heat pump systems and the need for specialized engineering knowledge, new market entry remains relatively challenging. As a result, leading companies continue to maintain strong competitive positions across industrial and commercial heating applications.

Companies such as GEA Group Aktiengesellschaft, Johnson Controls International PLC, and Mitsubishi Electric Corporation are among the prominent players shaping the competitive landscape. These companies compete by offering advanced natural refrigerant technologies, energy-efficient heating solutions, and customized systems for industrial users. Market participants are increasingly focusing on product innovation, system performance improvements, and expansion into emerging clean heating applications.

The major players in the industry

- Johnson Controls International PLC

- Siemens Energy AG

- GEA Group Aktiengesellschaft

- Mitsubishi Electric Corporation

- MAN Energy Solutions SE

- Panasonic Holdings Corporation

- Copeland LP

- Guangdong PHNIX Eco-energy Solution Ltd.

- Star Refrigeration

- ARANER

- Mayekawa Mfg. Co., Ltd.

- Clade Engineering Systems Ltd.

- AGO GmbH Energie + Anlagen

- Lync by Watts Water Technologies, Inc.

- ALFA LAVAL

- Others

Key Development

- In May 2026, Siemens Energy increased its participation in large-scale sustainable heating and industrial decarbonization projects, supporting high-temperature heat pump applications capable of delivering temperatures above 90°C for industrial heat and district energy networks. The company continued expanding solutions for electrified heating and energy efficiency. Siemens Energy reported EUR 39.1 billion in revenue in FY2025, serving customers in more than 90 countries.

- In April 2026, Alfa Laval continued strengthening its role in the energy transition market by supporting large heat pump applications for district heating networks and industrial process heating, leveraging its heat transfer technologies and energy efficiency solutions. The company reported SEK 69.7 billion in net sales in FY2025 operated in more than 100 countries, and maintained a workforce of more than 22,000 employees globally.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 8.7 Bn |

| Forecast Revenue (2035) | USD 29.9 Bn |

| CAGR (2026-2035) | 13.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Refrigerant (Ammonia (R717), Carbon Dioxide (R744), Hydrocarbons, and Other Refrigerants), By Capacity (20–200 kW, 201–500 kW, 501–1,000 kW, and Above 1,000 kW), By End-Use (Industrial and Commercial) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Johnson Controls International PLC, Siemens Energy AG, GEA Group Aktiengesellschaft, Mitsubishi Electric Corporation, MAN Energy Solutions SE, Panasonic Holdings Corporation, Copeland LP, Guangdong PHNIX Eco-energy Solution Ltd., Star Refrigeration, ARANER, Mayekawa Mfg. Co., Ltd., Clade Engineering Systems Ltd., AGO GmbH Energie + Anlagen, Lync by Watts Water Technologies, Inc, ALPHA LAVAL, Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |