Global J-Beauty Products Market Size, Share, Growth Analysis By Product (Skincare, Haircare, Color Cosmetics, Others), By Type (Conventional, Organic), By Distribution Channel (Specialty Stores, Hypermarkets/Supermarkets, E-commerce, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 180131

- Number of Pages: 247

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

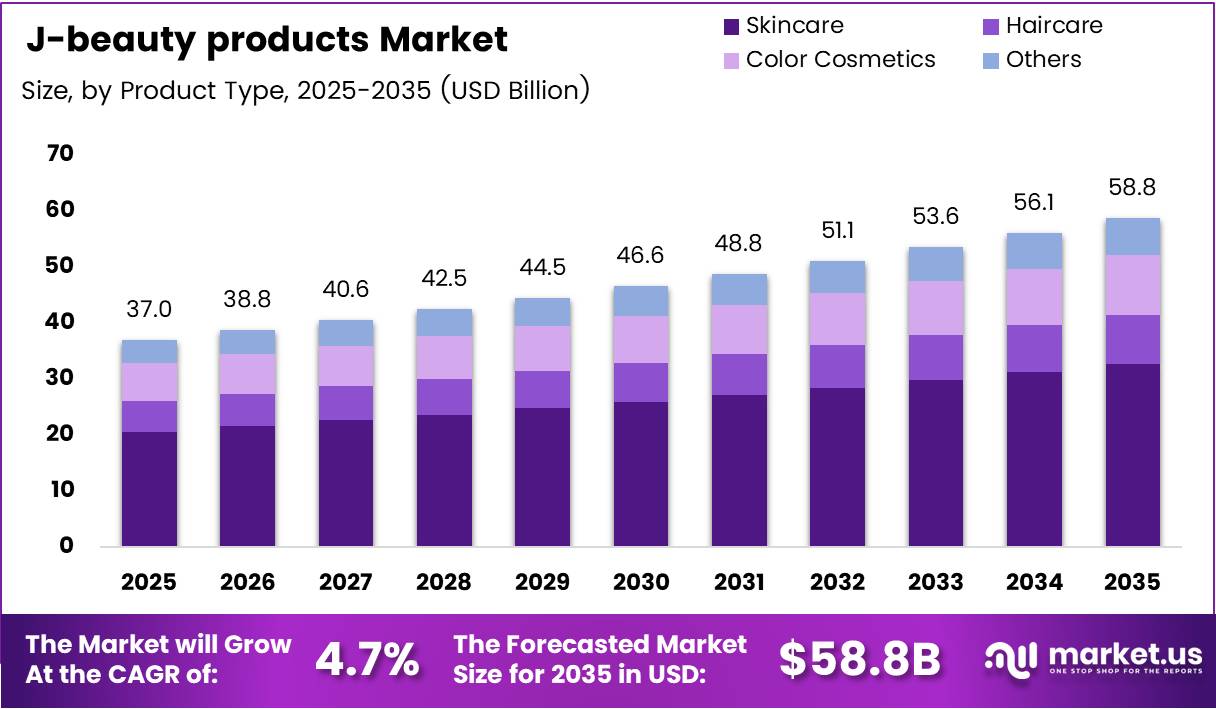

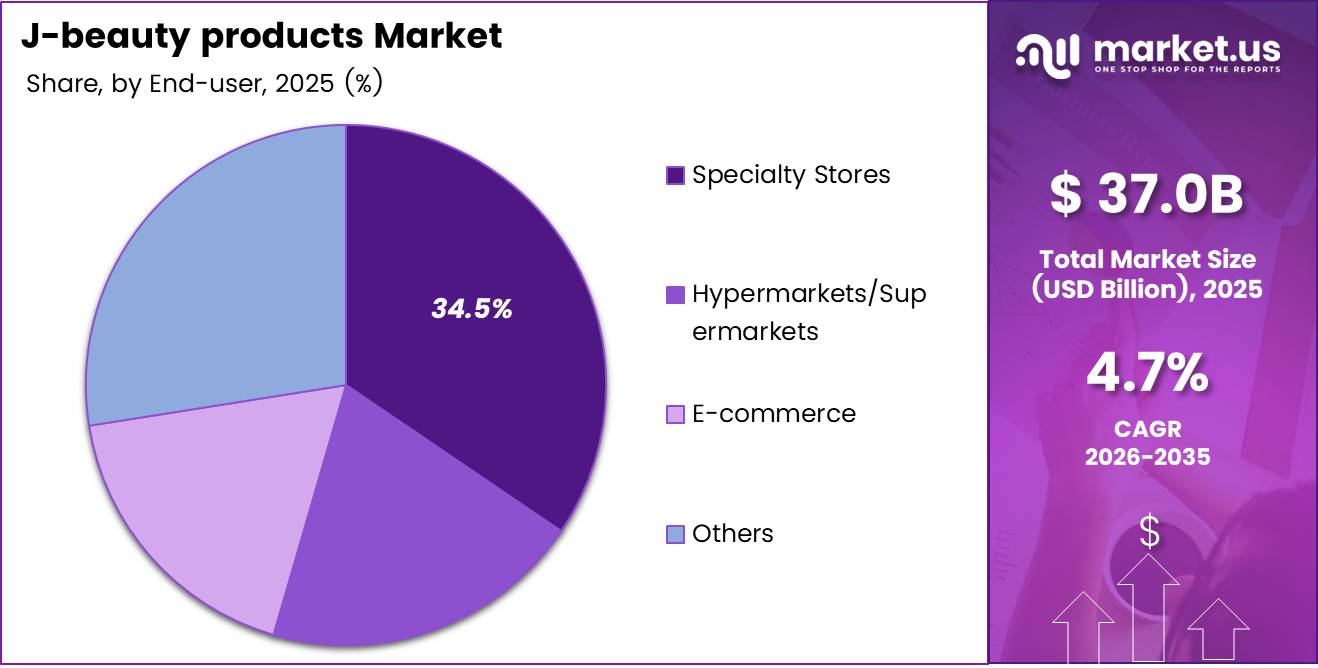

Global J-Beauty Products Market size is expected to be worth around USD 58.8 Billion by 2035 from USD 37.0 Billion in 2025, growing at a CAGR of 4.7% during the forecast period 2026 to 2035.

J-Beauty, or Japanese beauty, refers to skincare, haircare, and cosmetic products developed under Japan’s distinct philosophy of skin health, ingredient science, and minimalist routines. This market spans conventional and organic formulations distributed through specialty stores, e-commerce platforms, and mass retail. Its appeal extends well beyond Japan, with authentic product formulations now reaching consumers across North America, Europe, and Southeast Asia.

The market’s 4.7% CAGR reflects deliberate, sustained buyer conversion rather than short-term trend cycling. Consumers who discover Japanese skincare tend to build long-term routines around it, which creates stable repeat-purchase behavior and a strong base for brand loyalty. This structural feature makes J-Beauty less vulnerable to market swings than trend-driven beauty categories.

Government support in Japan has reinforced this trajectory. Japan’s Ministry of Economy, Trade and Industry tracks cosmetics exports as a strategic trade category, and Japan’s export promotion bodies — including JETRO — actively facilitate cross-border retail partnerships. This institutional backing gives Japanese cosmetics brands a structural export advantage that most competing beauty industries lack.

Skincare holds the commanding position in this market, driven by Japan’s culturally embedded emphasis on skin protection, hydration layering, and UV defense. The J-Beauty philosophy treats skincare as preventive health, not cosmetic enhancement — a framing that resonates strongly with premium consumers globally who prioritize long-term skin outcomes over immediate aesthetic effects.

In June 2024, J-Beauty brand Shikō partnered with STRIIIKE studio in Beverly Hills, marking a direct expansion of Japanese beauty retail into the U.S. lifestyle market. This type of experiential retail move signals that Japanese brands now treat Western markets as primary growth fronts, not secondary export destinations — a strategic shift with long-term revenue implications.

According to the Ministry of Economy, Trade and Industry, Japan’s cosmetics exports reached ¥646.6 billion in 2023, more than double the ¥285.1 billion recorded in 2018. This doubling over five years shows that international demand for J-Beauty has moved beyond niche status — it now reflects a structural shift in how global consumers allocate their beauty spend.

According to the Japan External Trade Organization, China accounted for approximately 46% of Japan’s total cosmetics exports in 2023. This concentration signals both the depth of J-Beauty penetration in Greater China and a geographic risk — diversification into North America and Europe is not just a growth strategy but a supply-chain and revenue resilience imperative.

Key Takeaways

- The Global J-Beauty Products Market was valued at USD 37.0 Billion in 2025 and is forecast to reach USD 58.8 Billion by 2035.

- The market advances at a CAGR of 4.7% during the forecast period 2026 to 2035.

- By Product, Skincare leads with a 55.6% share, reflecting Japan’s skincare-first beauty culture.

- By Type, Conventional products dominate with a 67.3% share due to established formulation trust and wide retail availability.

- By Distribution Channel, Specialty Stores hold the largest share at 34.5%, driven by consumer preference for curated J-Beauty retail experiences.

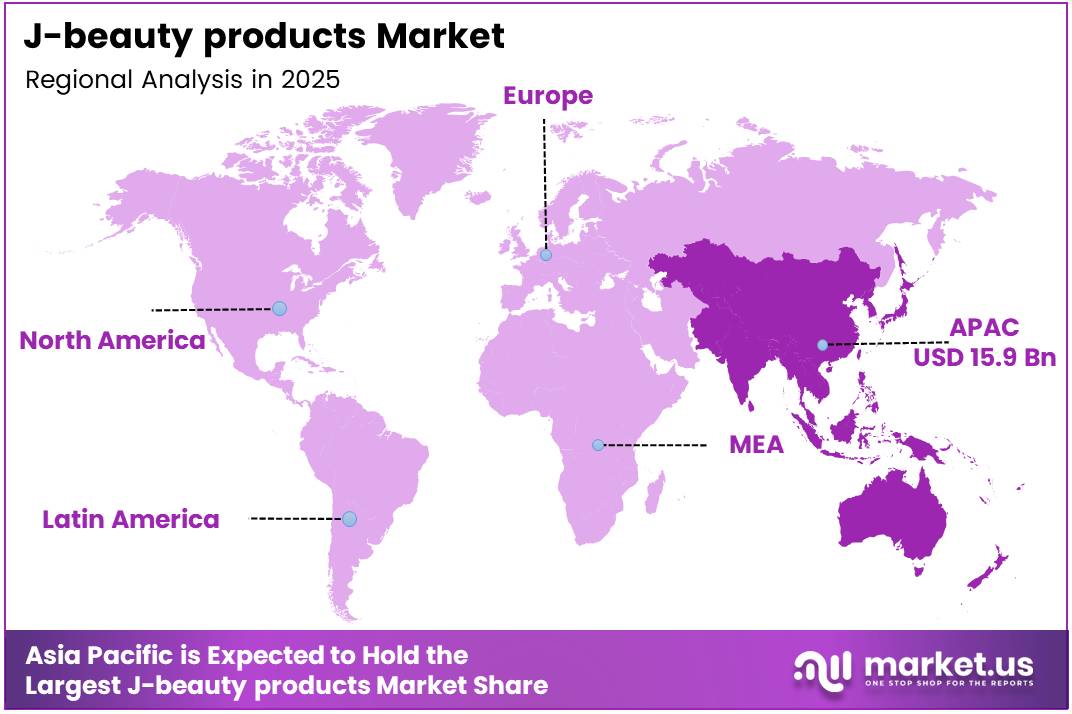

- Asia Pacific dominates regionally with a 43.10% share, valued at USD 15.9 Billion, anchored by Japan’s home market strength and regional cultural alignment.

- Japan’s cosmetics exports more than doubled from ¥285.1 billion in 2018 to ¥646.6 billion in 2023, reflecting accelerating global trade in J-Beauty products.

- China accounts for around 46% of Japan’s cosmetics exports, making it the single largest overseas buyer of J-Beauty products.

Product Analysis

Skincare dominates with 55.6% due to Japan’s skin-health-first beauty culture.

In 2025, Skincare held a dominant market position in the By Product segment of the J-Beauty Products Market, with a 55.6% share. According to the Japan Cosmetic Industry Association, skincare products accounted for approximately 50% of total cosmetics spending among Japanese consumers in 2023, confirming that this domestic preference directly fuels global product development and export priorities.

Haircare serves as the second-largest revenue pillar in J-Beauty, distinguished by scientifically formulated damage-repair and scalp-care products. Japanese haircare brands command premium positioning globally because their formulations address scalp health as a root-cause issue, not just surface aesthetics. This functional differentiation gives haircare products stronger retention rates among loyal users.

Color Cosmetics carries a smaller but strategically significant share within J-Beauty’s product portfolio. Japanese color cosmetics appeal to consumers seeking lightweight coverage that works synergistically with skincare layers. Consequently, buyers often purchase J-Beauty makeup as an extension of their skincare routine, which increases average basket size and cross-category attachment rates.

Others in the product mix include fragrance, body care, and specialty treatment products rooted in Japanese botanical traditions. These sub-categories attract niche but high-spending consumer segments seeking authentic Japanese formulation philosophies. Their growth serves as an early-stage indicator of how broadly the J-Beauty philosophy can extend beyond core facial skincare.

Type Analysis

Conventional dominates with 67.3% due to formulation trust and broad retail access.

In 2025, Conventional products held a dominant market position in the By Type segment of the J-Beauty Products Market, with a 67.3% share. Japanese conventional cosmetics have earned this position through decades of rigorous dermatological testing and clinical validation — standards that consumers and dermatologists internationally recognize as credible. This trust is a structural advantage competitors cannot replicate quickly.

Organic products represent the fastest-developing type segment within J-Beauty, aligned with rising global consumer interest in clean and plant-based formulations. Japanese organic cosmetic brands differentiate through ingredient transparency and traditional botanical sourcing, such as rice bran and fermented extracts. However, scaling organic lines while maintaining J-Beauty’s quality standards creates formulation complexity that limits how fast this segment can grow.

Distribution Channel Analysis

Specialty Stores dominate with 34.5% due to curated J-Beauty retail expertise.

In 2025, Specialty Stores held a dominant market position in the By Distribution Channel segment of the J-Beauty Products Market, with a 34.5% share. Specialty retail dominates because J-Beauty products require consumer education — the multi-step routine philosophy and layering techniques are best communicated by trained in-store staff. This educational retail model creates higher conversion rates than self-service mass retail.

Hypermarkets/Supermarkets provide J-Beauty brands with volume reach and household-name brand visibility across mid-market consumer segments. However, the mass retail environment compresses price premiums and limits the consultative selling that J-Beauty products depend on. Brands using this channel typically feature their most accessible entry-level SKUs to preserve premium positioning elsewhere.

E-commerce channels expand J-Beauty’s global footprint by removing geographic barriers to product access. According to the Ministry of Economy, Trade and Industry, online channels accounted for over 30% of cosmetics purchases in Japan in 2023. This shift confirms that digital commerce now functions as a primary discovery and purchase engine, not a supplementary one — particularly for consumers outside Japan seeking authentic products.

Others, including direct-to-consumer brand websites and salon professional channels, serve as high-intent, high-loyalty distribution endpoints. Consumers purchasing through brand-direct channels typically have stronger product knowledge and higher lifetime value. Additionally, professional salon channels reinforce J-Beauty’s credibility as a results-driven rather than trend-driven category.

Key Market Segments

By Product

- Skincare

- Haircare

- Color Cosmetics

- Others

By Type

- Conventional

- Organic

By Distribution Channel

- Specialty Stores

- Hypermarkets/Supermarkets

- E-commerce

- Others

Drivers

Minimalist Skincare Philosophy and Dermatologically Proven Japanese Formulations Drive Global Consumer Adoption

Japanese beauty philosophy centers on skin-barrier preservation and long-term skin health rather than cosmetic masking. This approach attracts consumers globally who have shifted from heavy-coverage cosmetics to protective, restorative skincare regimens. The structural consequence is that J-Beauty builds product loyalty at the routine level, not the single-product level — a more durable commercial foundation.

Demand for dermatologically tested formulations gives J-Beauty a credibility advantage in markets where consumers cross-reference clinical claims before purchasing. Japanese cosmetic science uses advanced delivery systems, UV technology, and fermented ingredient biotechnology that most global brands cannot match at equivalent price points. According to the Japan Cosmetic Industry Association, over 70% of Japanese women use sunscreen year-round — a behavioral norm that has driven decades of innovation in lightweight, daily-use UV protection products now exported globally.

Cross-border e-commerce platforms have converted global J-Beauty interest into accessible purchasing behavior. In June 2024, KOSÉ Corporation opened its first stand-alone Maison KOSÉ retail store in Los Angeles, combining brand discovery with direct sales in one of the world’s most competitive beauty retail markets. This move signals that Japanese brands now invest in physical-market presence as a conversion strategy, not just export logistics — which accelerates consumer acquisition at the premium end of the market.

Restraints

Premium Pricing and Limited Western Brand Awareness Create a Dual Barrier to Mass-Market Penetration

Japanese skincare products occupy a premium price tier that restricts entry for cost-sensitive consumer segments in Western and emerging markets. The high cost reflects genuine R&D investment, stringent manufacturing standards, and premium ingredient sourcing — but this justification does not reduce price sensitivity among buyers comparing J-Beauty to more aggressively marketed global alternatives at lower price points.

Outside East Asia, J-Beauty competes directly with K-Beauty for consumer mindshare — and K-Beauty currently commands significantly greater marketing investment and influencer infrastructure in North America and Europe. According to the Statistics Bureau of Japan, more than 60% of Japanese women use skincare products daily. However, this deep domestic engagement has not yet translated into equivalent brand recognition abroad, where J-Beauty remains a premium niche rather than a mainstream category.

Limited retail penetration outside specialty beauty stores creates a visibility gap that premium pricing alone cannot bridge. Consumers unfamiliar with J-Beauty’s philosophy rarely encounter it through mass retail channels. Moreover, the educational requirement — explaining multi-step routines and layering science — demands marketing investment that smaller Japanese brands lack the international budget to deploy at scale against global cosmetics conglomerates.

Growth Factors

Clean Beauty Packaging, Men’s Grooming Expansion, and Global Retail Partnerships Open New Revenue Channels for J-Beauty

Japanese cosmetic brands hold a structural advantage in the clean beauty packaging movement because eco-conscious, refillable design has long been embedded in their product development culture. According to the Japan Cosmetic Industry Association, approximately 55% of Japanese consumers prefer skincare products containing natural or botanical ingredients — a domestic preference that now mirrors global demand trends and gives J-Beauty brands authentic sustainability credentials rather than reactive compliance.

According to the Ministry of Economy, Trade and Industry, approximately 40% of Japanese men now use facial skincare products regularly. This participation rate confirms that men’s grooming is no longer an emerging sub-category in Japan — it is an active revenue segment. Gender-neutral product line extensions allow J-Beauty brands to address this buyer group without repositioning their core identity, which lowers entry cost and expands addressable market simultaneously.

In June 2024, the Maison KOSÉ store in Los Angeles introduced personalized skincare consultations and interactive beauty experiences — a retail model that converts casual browsers into committed J-Beauty users. Collaborations between Japanese cosmetic brands and established global retail chains and online marketplaces replicate this consultative model at scale, creating new distribution reach without requiring brands to build independent retail infrastructure in unfamiliar markets.

Emerging Trends

Fermented Ingredients, Skinimalism, and Social Media-Driven Routine Education Redefine J-Beauty’s Global Consumer Proposition

“Skinimalism” — the philosophy of fewer, higher-efficacy products applied in a deliberate sequence — aligns precisely with Japanese multi-step hydration routines that prioritize skin health over cosmetic layering. This convergence between global consumer preference and J-Beauty’s foundational philosophy creates a favorable positioning window for brands that authentically represent the approach rather than adapting it retroactively for Western audiences.

Fermented skincare ingredients — including galactomyces, sake extracts, and bifida ferment lysate — are now a recognized product differentiator in global premium skincare markets. According to Statista Consumer Insights, around 44% of Japanese consumers discover beauty products through social media before purchasing. This digital discovery behavior means that fermented ingredient science, when communicated through social media tutorials and influencer demonstrations, reaches high-intent buyers efficiently and at lower acquisition cost than traditional retail advertising.

Japanese cosmetic innovators lead development of beauty tech tools including skin diagnostic devices, smart UV monitors, and app-connected skincare systems. These devices extend the J-Beauty relationship beyond product purchase into ongoing skin management — a recurring engagement model that deepens brand loyalty and creates data-driven personalization opportunities. Early movers in beauty tech gain a compounding advantage as device ecosystems create switching costs that pure product brands cannot replicate.

Regional Analysis

Asia Pacific Dominates the J-Beauty Products Market with a Market Share of 43.10%, Valued at USD 15.9 Billion

Asia Pacific holds a 43.10% share of the J-Beauty Products Market, valued at USD 15.9 Billion. Japan’s home market anchors this dominance through high per-capita cosmetics spending, deep retail infrastructure, and a culturally embedded daily skincare routine. Neighboring markets in South Korea, China, and Southeast Asia reinforce regional strength through strong cultural alignment with Japanese beauty values and established cross-border trade flows.

North America J-Beauty Products Market Trends

North America represents the highest-potential Western expansion market for J-Beauty brands, driven by premium consumer segments that actively seek dermatologically validated skincare alternatives to domestic brands. Physical retail entries like the Maison KOSÉ store in Los Angeles and influencer-driven social media exposure have accelerated brand awareness. However, shelf presence in mainstream retail remains limited, creating a gap between consumer interest and purchase conversion.

Europe J-Beauty Products Market Trends

Europe’s J-Beauty penetration is strongest in the UK, Germany, and France, where premium beauty consumers show documented interest in international skincare formats. EU cosmetic regulations align closely with Japanese quality standards, reducing the compliance burden for Japanese brands entering European retail. Additionally, European consumers’ familiarity with multi-step skincare routines — particularly in skincare-focused Northern European markets — creates a receptive buyer base for J-Beauty education.

Latin America J-Beauty Products Market Trends

Latin America presents an early-stage but structurally promising entry opportunity for J-Beauty brands, particularly in Brazil and Mexico where premium beauty consumption is expanding. E-commerce platforms have outpaced physical retail as the primary channel for imported beauty brands in the region. Cultural affinity for skin whitening and UV protection products creates direct alignment with core J-Beauty product categories, especially sunscreen and brightening serums.

Middle East and Africa J-Beauty Products Market Trends

The Middle East and Africa market for J-Beauty products remains at an early adoption stage, with the Gulf Cooperation Council countries representing the most commercially viable entry point. GCC consumers’ high per-capita beauty spend and preference for luxury-positioned international brands align with J-Beauty’s premium pricing structure. South Africa serves as a secondary access point to Sub-Saharan Africa, though broader regional distribution infrastructure requires further development before meaningful scale is achievable.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Shiseido Co., Ltd. positions itself as the global ambassador of Japanese prestige beauty, operating across skincare, makeup, and fragrance through an integrated R&D and retail platform. Its strategy centers on premium brand building in Western and Chinese markets through both retail partnerships and proprietary research facilities. This dual investment in brand equity and formulation science creates defensible positioning that private-label competitors cannot easily replicate.

L’Oréal Groupe engages with J-Beauty through its Japanese brand acquisitions and its established distribution infrastructure across over 150 countries. Its competitive advantage in this market lies in applying global marketing scale to Japan-originated product science — a combination that accelerates J-Beauty’s reach into mass and mid-market segments that pure Japanese brands rarely penetrate independently. This scale advantage also enables faster retail shelf expansion in emerging markets.

Procter & Gamble Company competes in J-Beauty-adjacent segments through its SK-II brand, which builds its entire identity on Japanese fermentation science and premium positioning. P&G’s strategic strength is translating J-Beauty’s technical credibility into globally scalable marketing narratives that resonate with luxury skincare consumers across Asia Pacific and North America. SK-II’s brand story functions as a conversion engine that justifies premium price points in mass global retail environments.

Kao Corporation operates across skincare, haircare, and hygiene with a research-driven product development model rooted in Japanese consumer science. In September 2025, Kao reported increased sales in its skincare and cosmetics division, driven by luxury skincare performance and expanded global operations. This growth confirms that Kao’s strategy of combining science-backed formulations with selective international distribution is producing measurable commercial results at a global scale.

Key Players

- Shiseido Co., Ltd.

- L’Oreal Groupe

- Procter & Gamble Company

- Kao Corporation

- Lion Corporation

- POLA ORBIS HOLDINGS INC.

- FANCL CORPORATION

- CANMAKE

- Kosé Corporation

Recent Developments

- April 2025 — Marubeni Corporation completed the acquisition of Japanese skincare and cosmetics brand ETVOS to build a broader Beauty & Health business platform in Japan. This acquisition signals institutional capital’s confidence in J-Beauty brand consolidation as a viable domestic growth strategy.

- September 2025 — Kao Corporation reported increased sales in its skincare and cosmetics division, driven by strong hair care and luxury skincare product performance. The company expanded global operations and product offerings, reinforcing its position as one of Japan’s most internationally active cosmetic manufacturers.

- November 2025 — A Japanese company signed an agreement to acquire the trademark for Obagi in Japan, securing permanent licensing and distribution rights across consumer, clinical, and salon channels. This acquisition extends J-Beauty’s reach into the clinical skincare segment, where brand credibility commands strong price premiums.

- December 2024 — REI Cosmetic Japan began full-scale domestic sales of vegan cosmetic brand “Cocoon,” with international rollout commencing in September 2025. This launch reflects consumer appetite for eco-friendly and plant-based J-Beauty products as a complement to Japan’s existing botanical formulation heritage.

Report Scope

Report Features Description Market Value (2025) USD 37.0 Billion Forecast Revenue (2035) USD 58.8 Billion CAGR (2026-2035) 4.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Skincare, Haircare, Color Cosmetics, Others), By Type (Conventional, Organic), By Distribution Channel (Specialty Stores, Hypermarkets/Supermarkets, E-commerce, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Shiseido Co., Ltd., L’Oreal Groupe, Procter & Gamble Company, Kao Corporation, Lion Corporation, POLA ORBIS HOLDINGS INC., FANCL CORPORATION, CANMAKE, Kosé Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Shiseido Co., Ltd.

- L'Oreal Groupe

- Procter & Gamble Company

- Kao Corporation

- Lion Corporation

- POLA ORBIS HOLDINGS INC.

- FANCL CORPORATION

- CANMAKE

- Kosé Corporation

Our Clients

- 180131

- Feb 2026