Quick Navigation

Report Overview

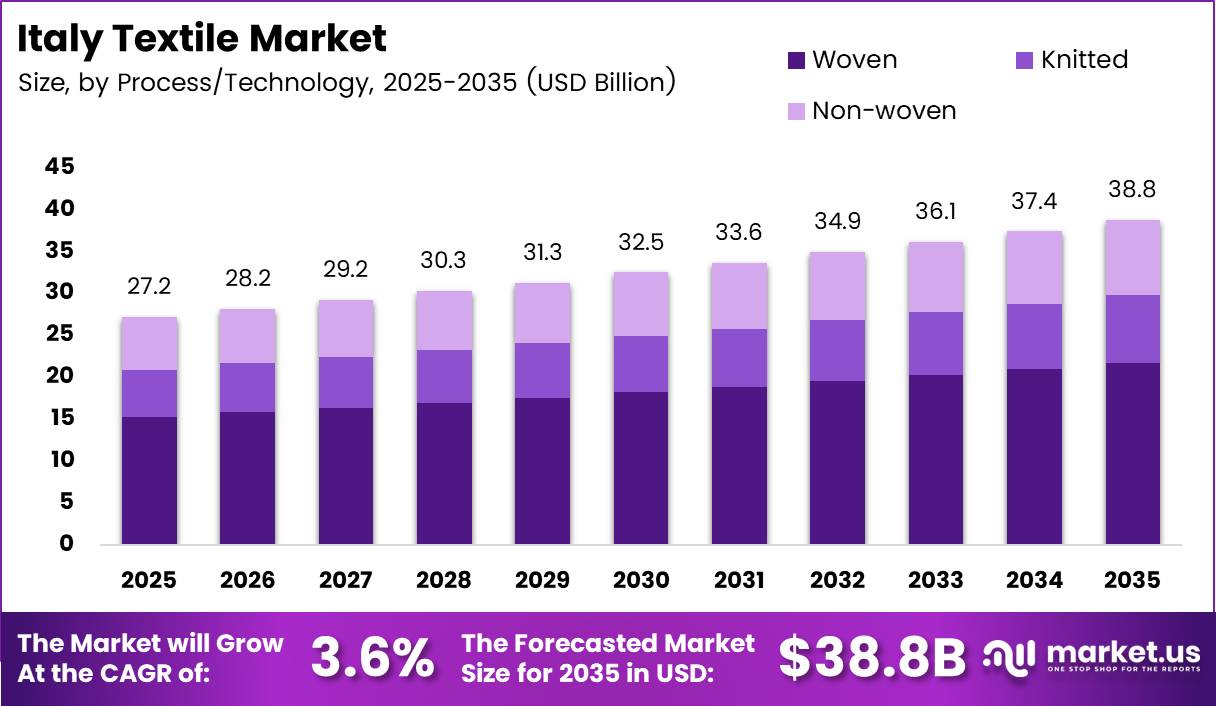

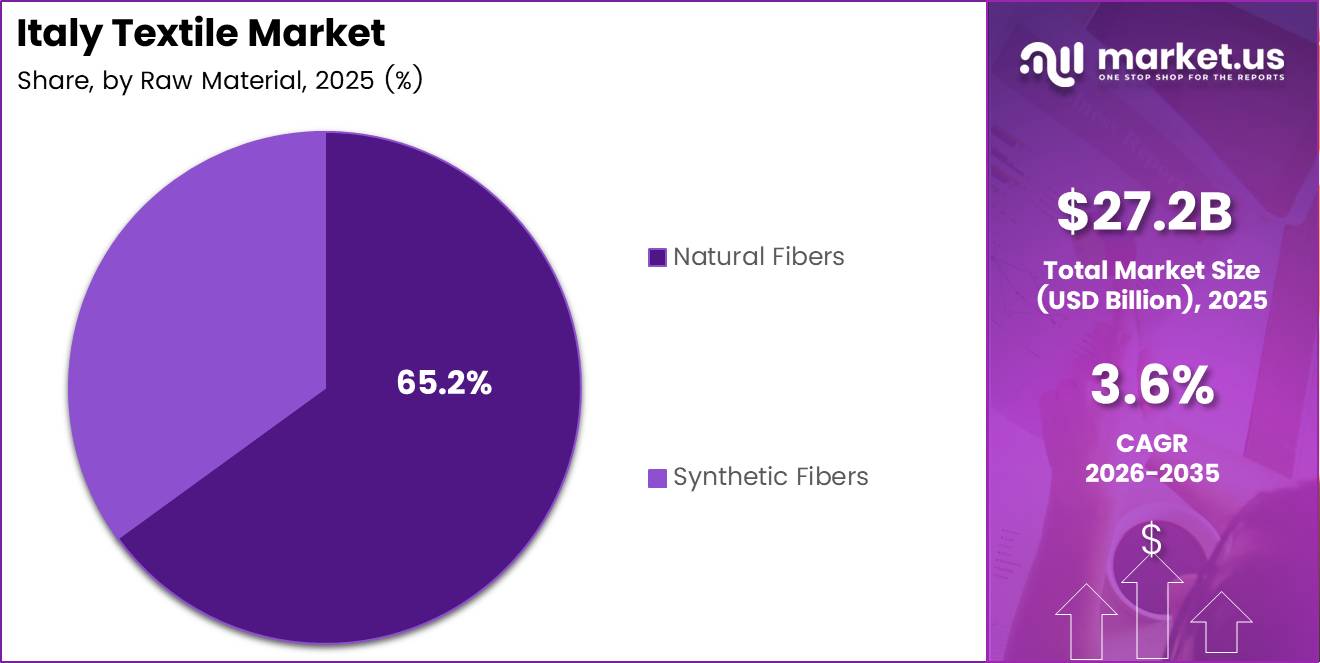

The Italy Textile Market size is expected to be worth around USD 38.8 Billion by 2035 from USD 27.2 Billion in 2025, growing at a CAGR of 3.6% during the forecast period 2026 to 2035.

Italy occupies a structurally distinct position in the global textile industry. Unlike volume-driven producers in Asia, Italy competes on craftsmanship, material quality, and brand equity. The country’s textile output is closely tied to its luxury fashion sector, which commands premium pricing and loyal export demand from North America, Europe, and the Gulf region.

The Italian textile market encompasses raw fiber processing, fabric manufacturing, technical textiles, and finished fashion goods. Natural fibers, particularly cotton, wool, and silk, form the backbone of Italy’s premium offering. Synthetic and recycled fiber segments are expanding as brands respond to sustainability requirements from international buyers and domestic policy.

Manufacturing clusters in Prato, Biella, and Como remain central to production capacity. These districts concentrate weaving, dyeing, finishing, and specialty fabric operations within tight geographic proximity. This cluster model keeps lead times short and supports the small-batch, high-value production that defines Italian textiles globally.

Government policy is actively shaping near-term investment flows. The Ministry of Enterprises and Made in Italy allocated EUR 250 million in 2025 to revitalize the fashion sector, distributed across development contracts, mini-development contracts, digital and ecological transition support, and sustainability promotion. This injection signals that policymakers treat Italian textiles as a strategic export sector, not just a legacy industry.

Technical and performance textiles represent an underpenetrated but high-growth layer of this market. Industrial, medical, and automotive applications are absorbing advanced textile materials at rates that traditional fashion-focused producers have not historically served. Manufacturers that successfully pivot into these segments diversify revenue beyond cyclical luxury spending.

According to ACIMIT, in Q1 2026 the orders index for Italian textile machinery stood at 37.3 points against a 2021 base of 100, with domestic orders rising 21% year-on-year. This domestic machinery upturn indicates that Italian producers are reinvesting in production capacity, which historically precedes output expansion within two to three quarters.

The market’s 3.6% CAGR is steady rather than spectacular, but the underlying dynamic is a quality-versus-volume shift. As global buyers pay larger premiums for verified origin and sustainable production, Italian manufacturers are positioned to capture higher margins per unit even without volume growth. For investors, this means the market’s value growth exceeds what headline tonnage figures suggest.

Key Takeaways

- The Italy Textile Market was valued at USD 27.2 Billion in 2025 and is forecast to reach USD 38.8 Billion by 2035.

- The market grows at a CAGR of 3.6% during the forecast period 2026 to 2035.

- By Raw Material, Natural Fibers dominate with a 62.4% share in 2025.

- By Process/Technology, Woven holds the leading position with a 56.1% share in 2025.

- By Application, Fashion & Apparel leads with a 51.9% share in 2025.

- The Italian government allocated EUR 250 million in 2025 to support and revitalize the domestic fashion and textile sector.

- Domestic Italian textile machinery orders rose 21% year-on-year in Q1 2026, per ACIMIT data.

Raw Material Analysis

Natural Fibers dominate with 62.4% due to luxury brand preference for premium natural inputs.

In 2025, Natural Fibers held a dominant market position in the By Raw Material segment of the Italy Textile Market, with a 62.4% share. Italy’s manufacturing identity is built on cotton, wool, and silk. These materials command premium pricing in global fashion supply chains and align with the quality positioning of Italian apparel labels.

Synthetic Fibers serve Italy’s performance, sportswear, and technical textile sectors. Polyester, nylon, and rayon enable functional properties that natural fibers cannot achieve at scale. Brands targeting athletic wear, medical textiles, and industrial applications rely on synthetic inputs to meet technical specifications while managing production costs.

Process/Technology Analysis

Woven dominates with 56.1% due to structural alignment with Italy’s premium fashion output.

In 2025, Woven held a dominant market position in the By Process/Technology segment of the Italy Textile Market, with a 56.1% share. Woven fabrics underpin the tailored garments, suiting, and structured fashion products that define Italian export categories. The process aligns with Italy’s cluster-based loom infrastructure, which has been refined over generations.

Knitted fabrics serve Italy’s casualwear, sportswear, and activewear production. Stretch properties and comfort performance drive knitted fabric adoption in categories outside formal fashion. Italian knitwear producers in Carpi and other districts supply both domestic fashion labels and international sportswear brands with specialized jersey and rib constructions.

Non-woven fabrics are the technical growth segment within Italian process technologies. Applications span medical protective wear, geotextiles, filtration, and automotive interior components. Non-woven production requires different capital equipment and process chemistry than traditional weaving or knitting, making it a distinct business model within the broader market.

Application Analysis

Fashion & Apparel dominates with 51.9% due to Italy’s global identity as a luxury fashion origin.

In 2025, Fashion & Apparel held a dominant market position in the By Application segment of the Italy Textile Market, with a 51.9% share. Italian textiles are synonymous with high fashion globally. Demand from domestic fashion houses and international luxury brands that source Italian-made fabrics sustains this segment’s structural dominance through premium pricing and brand attribution.

Industrial/Technical Textiles serve automotive, aerospace, construction, and filtration end uses. This application category is expanding as Italian producers diversify beyond cyclical fashion revenue. Technical textile margins are more stable than fashion, making this segment increasingly attractive for manufacturers seeking to reduce seasonal revenue concentration.

Household & Home Textiles capture demand for bed linens, towels, curtains, and upholstery fabrics. Italian home textile producers serve both premium domestic retail and export markets in Europe and North America. This segment benefits from Italy’s broader design reputation, with “Made in Italy” labeling supporting retail price premiums in home categories.

Medical & Healthcare Textiles cover surgical drapes, wound care materials, compression garments, and hygiene non-wovens. This application is structurally less cyclical than fashion and benefits from aging population trends in European markets. Italian producers capable of meeting EU medical device and safety standards access a defensible niche with high entry barriers.

Automotive & Transport Textiles serve seat fabrics, interior linings, acoustic insulation, and safety belt webbing. Italy’s automotive industry, centered around northern production clusters, creates captive domestic demand for specialty textile inputs. Electric vehicle production shifts are altering interior material specifications, creating both risks and retooling opportunities for automotive textile suppliers.

Key Market Segments

By Raw Material

- Natural Fibers

- Cotton

- Wool

- Silk

- Synthetic Fibers

- Polyester

- Nylon

- Rayon/Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others

By Process/Technology

- Woven

- Knitted

- Non-woven

- Spunlaid (Spunbond/Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others

Drivers

Italy’s Premium Textile Brand Equity and Established Manufacturing Clusters Drive Sustained Export Demand

Italy’s textile market derives structural pricing power from decades of verified craftsmanship. International buyers in luxury fashion, premium home furnishings, and technical apparel consistently pay above-market rates for Italian-origin fabrics. This origin premium is not marketing. It reflects real quality differentiation built into cluster-based production ecosystems in Biella, Prato, and Como.

Textile manufacturing clusters compress supply chains in ways that isolated producers cannot replicate. Fiber processors, dye houses, weavers, and finishers operate within kilometers of each other. This density reduces lead times, enables rapid product iteration, and supports the small-batch flexibility that luxury brands require. Cluster geography is a competitive barrier that emerging textile nations have not overcome.

According to ACIMIT, domestic Italian textile machinery orders rose 21% year-on-year in Q1 2026. This increase signals that Italian manufacturers are actively investing in production capacity rather than deferring capital expenditure. When domestic machinery orders rise, output capacity follows within two to four quarters. For buyers planning 2026 to 2027 sourcing, Italian supply availability is expanding, not contracting.

Restraints

Elevated Labor and Production Costs Limit Italy’s Competitiveness in Volume-Driven Textile Segments

Italian textile manufacturing carries a cost structure that is materially higher than competing producers in Turkey, India, Bangladesh, and China. Labor costs, utility pricing, and environmental compliance expenditure combine to make Italian textiles structurally expensive to produce at scale. This limits Italy’s participation in commodity and mid-market volume segments where price, not origin, determines sourcing decisions.

Workforce aging compounds cost pressures. The skilled technicians who operate specialized looms, finishing equipment, and quality control processes in Italian mills are disproportionately concentrated in older age cohorts. Recruitment of younger workers into textile trades has been insufficient to close the replacement gap. Skills shortages delay production schedules and increase unit labor costs for specialist operations.

According to INPS data reported in 2025, the Italian government allocated EUR 110 million in wage subsidies for the fashion sector, covering both 2024 and 2025. However, only EUR 2.9 million had actually been disbursed at the time of reporting. The gap between committed support and actual disbursement means that manufacturers facing immediate payroll pressure cannot rely on government transfers to bridge short-term cash flow. This execution failure weakens the policy’s intended stabilizing effect.

Growth Factors

Sustainable Luxury Textile Production and Technical Textile Diversification Open New Revenue Streams

EU sustainability directives are converting recycled fiber adoption from a voluntary brand commitment into a compliance requirement. Italian manufacturers with established recycled wool processing in Prato, and those investing in certified organic cotton and responsible silk sourcing, are positioned ahead of the regulatory curve. Brands that qualify early for EU Green Deal-aligned sourcing programs gain procurement preference from sustainability-mandated buyers.

Technical and performance textiles represent a structurally different revenue base from fashion. Industrial filtration, medical non-wovens, automotive seat materials, and geotextiles do not follow fashion season calendars. Italian producers entering these segments stabilize annual revenue and reduce dependence on luxury spend cycles. The investment required to qualify for medical and industrial textile certifications creates barriers that protect margin once established.

According to ACIMIT, the Q1 2026 orders index for Italian textile machinery stood at 37.3 points with a backlog guaranteeing approximately 4.5 months of workload. A multi-month forward order position confirms that manufacturers are not operating hand-to-mouth. This backlog depth supports investment planning and gives producers the financial visibility needed to commit to sustainable production upgrades and technical market entry programs.

Emerging Trends

Digital Manufacturing Technologies and Traceable Sustainable Sourcing Are Redefining Italian Textile Operations

Smart manufacturing investment is accelerating across Italian textile districts. Automated weaving systems, AI-assisted quality inspection, and digital pattern cutting reduce labor dependency in steps where human skill gaps are most acute. Producers adopting these technologies offset workforce aging constraints and maintain throughput without proportional headcount increases.

Consumer demand for traceable, ethically produced textiles is shifting from preference to purchase criterion. Italian brands and their global retail partners now face direct pressure to document fiber origin, dyehouse practices, and labor conditions at every supply chain tier. Blockchain-based provenance platforms and digital product passports are entering commercial deployment, giving Italian cluster producers a verifiable origin advantage that competitors in low-cost countries cannot easily replicate.

According to ACIMIT, foreign orders for Italian textile machinery fell 7% year-on-year in Q1 2026. This decline reflects cautious global capital expenditure, but the domestic machinery upturn suggests Italian producers are self-investing independently of export market confidence. Early movers in digital textile manufacturing lock in efficiency advantages before the broader industry standardizes on automated processes, creating a performance gap that compounds over time.

Key Company Insights

Marzotto Group operates as one of Italy’s most vertically integrated textile producers, spanning wool, cotton, and synthetic fabric manufacturing across fashion and technical markets. Its breadth of fiber and process coverage gives it supply chain flexibility that smaller specialists cannot match. However, vertical integration also concentrates capital risk within Italy’s cost-heavy manufacturing environment, making margin management a continuous strategic priority.

Albini Group has built a focused competitive position in premium shirting fabrics, supplying luxury fashion houses and international shirt brands from its Bergamo base. This category specialization means Albini competes on quality and design consistency rather than volume or price. The strategic risk is concentration in a single apparel category; shifts in formal dress codes or luxury spending patterns affect revenue more directly than for diversified producers.

Miroglio Group combines textile manufacturing with retail brand ownership, giving it downstream demand visibility that pure manufacturers lack. In March 2024, Miroglio acquired Trussardi, adding a premium apparel and accessories brand to its portfolio. This vertical move into branded fashion reduces Miroglio’s dependence on third-party brand relationships and provides a direct channel to test and sell textile innovations at retail.

RadiciGroup focuses on chemical intermediates, synthetic fibers, and technical textiles, positioning it differently from Italy’s luxury fabric producers. Its nylon and polypropylene operations serve automotive, filtration, and industrial end markets that operate outside fashion cycles. This industrial diversification creates revenue stability that fashion-dependent peers lack, though it also means RadiciGroup competes in global commodity chemical markets where Italian cost structures are a persistent challenge.

Key Players

- Marzotto Group

- Albini Group

- Miroglio Group

- RadiciGroup

- Candiani Denim

- Ratti S.p.A.

- Carvico S.p.A.

- Eurojersey S.p.A.

- Pontetorto S.p.A.

- Beste S.p.A.

- Limonta S.p.A.

- Sitip S.p.A.

Recent Developments

- March 2024 – Miroglio Group acquired Trussardi, expanding its portfolio into premium apparel, leather goods, and textile-based fashion. The acquisition strengthens Miroglio’s position across the Italian luxury fashion supply chain.

- June 2025 – Kering Eyewear acquired Italian manufacturer Lenti to scale its Made-in-Italy production capabilities for high-performance lenses and optical components, reinforcing Italian manufacturing as a strategic asset for global luxury groups.

- Q1 2026 – According to ACIMIT, the orders index for Italian textile machinery stood at 37.3 points (base year 2021 = 100), with a forward order backlog of approximately 4.5 months. Foreign orders declined 7% year-on-year while domestic orders rose 21%, indicating domestic reinvestment against a cautious global machinery export environment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 27.2 Billion |

| Forecast Revenue (2035) | USD 38.8 Billion |

| CAGR (2026-2035) | 3.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Natural Fibers: Cotton, Wool, Silk; Synthetic Fibers: Polyester, Nylon, Rayon/Viscose, Acrylic, Polypropylene, Recycled Fibers, Others), By Process/Technology (Woven, Knitted, Non-woven: Spunlaid, Dry-laid Hydro-entangled, Wet-Laid, Needle-punched, 3-D Weaving & Spacer Fabrics), By Application (Fashion & Apparel, Industrial/Technical Textiles, Household & Home Textiles, Medical & Healthcare Textiles, Automotive & Transport Textiles, Others) |

| Competitive Landscape | Marzotto Group, Albini Group, Miroglio Group, RadiciGroup, Candiani Denim, Ratti S.p.A., Carvico S.p.A., Eurojersey S.p.A., Pontetorto S.p.A., Beste S.p.A., Limonta S.p.A., Sitip S.p.A. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |