Global Intravenous Hydration Therapy Market By Service (Energy Boosters, Immune Boosters, Hydration, Beauty/ Aesthetics, Detoxification, Longevity/ Antiaging, Performance/ Athletics, Migraine & Pain Relief, Flu/Stomach and Others), By Component (Medicated and Non-medicated), By Provider (Physical Providers and Mobile Providers), By End-use (Hospitals & Clinics, Wellness Centers and Spas, Home Healthcare and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180762

- Number of Pages: 342

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

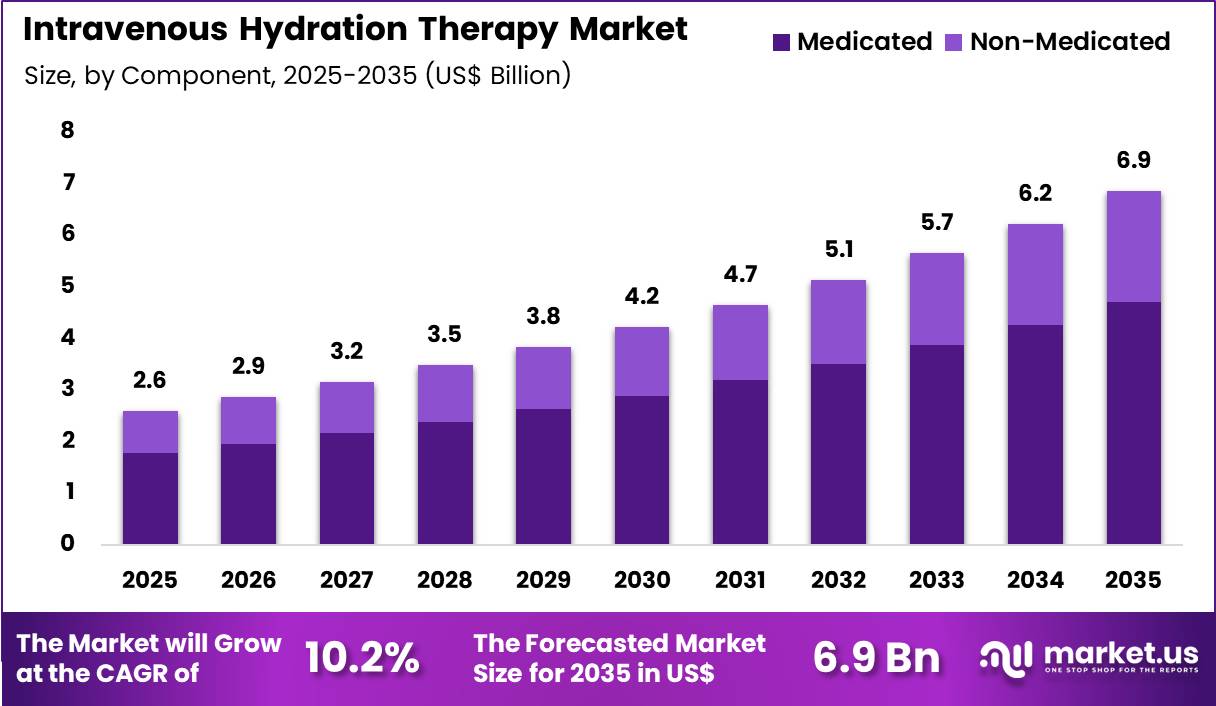

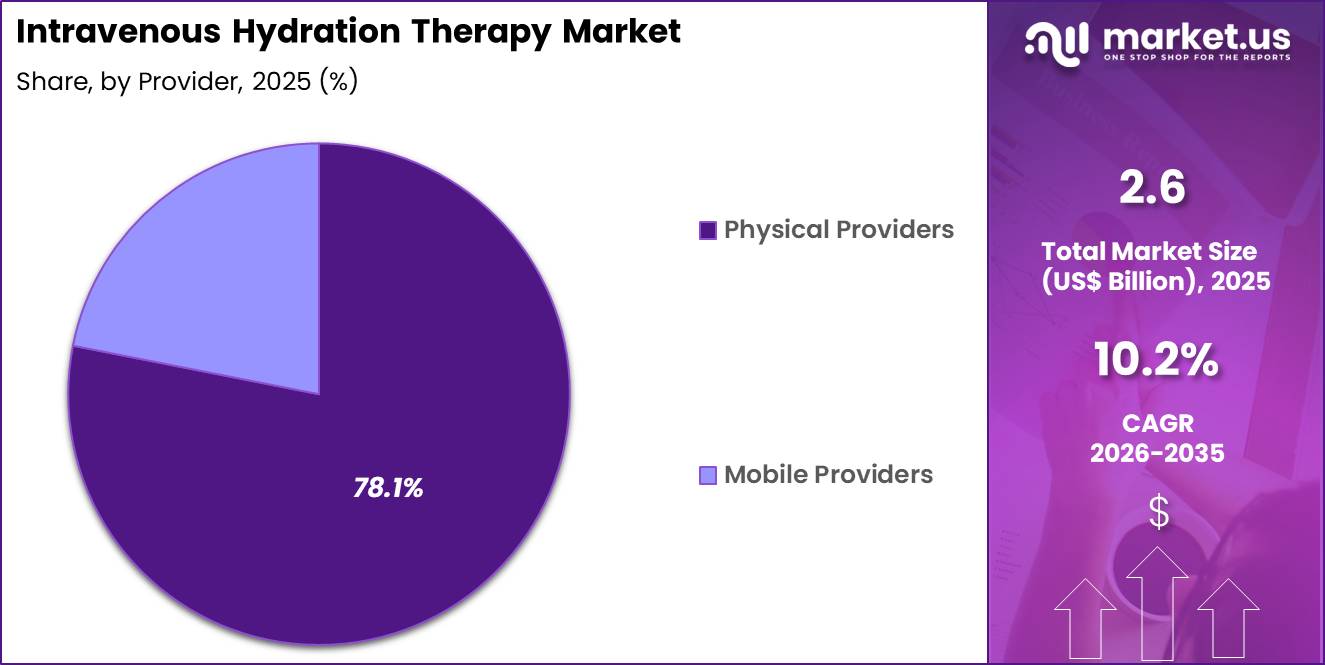

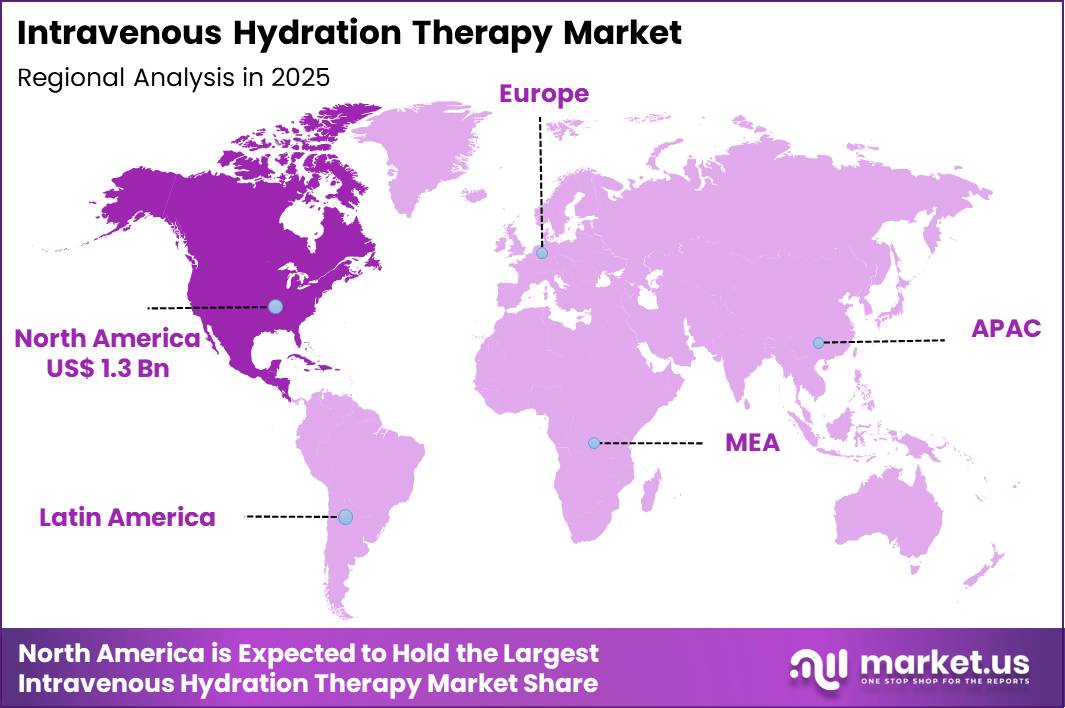

The Global Intravenous Hydration Therapy Market size is expected to be worth around US$ 6.9 Billion by 2035 from US$ 2.6 Billion in 2025, growing at a CAGR of 10.2% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 48.6% share with a revenue of US$ 1.3 Billion.

Increasing demand for rapid hydration and nutrient replenishment in both medical and wellness contexts drives the Intravenous Hydration Therapy market as providers and consumers recognize its superior absorption and immediate therapeutic effects compared to oral intake.

Hospitals and outpatient clinics increasingly administer IV hydration fluids to manage dehydration in acute gastroenteritis, heat exhaustion, or postoperative recovery, restoring electrolyte balance and preventing complications in vulnerable patients. These therapies support oncology care by delivering antiemetics, chemotherapy adjuncts, and fluids to counteract treatment-induced nausea and fluid loss.

Emergency departments utilize IV hydration for severe migraines, hangover recovery, and alcohol withdrawal, providing swift symptom relief and stabilizing patients. Wellness and performance clinics offer elective IV vitamin drips containing vitamin C, B-complex, glutathione, and electrolytes to enhance energy levels, immune function, and recovery after intense physical exertion or jet lag.

In aesthetic and anti-aging practices, practitioners provide customized IV cocktails to improve skin radiance, reduce oxidative stress, and promote detoxification in clients seeking proactive health optimization. In June 2025, Vellum Health secured Series A financing led by FCA Venture Partners and simultaneously launched a technology-enabled mobile IV care platform.

The service combines trained clinical staff with digital scheduling and remote coordination tools to deliver bedside intravenous treatments, with plans to expand operations across additional regions in the United States.

Providers and wellness operators pursue opportunities to expand mobile and on-demand IV services that integrate telehealth consultations and personalized nutrient formulations, broadening applications in corporate wellness programs and high-performance athletic recovery. Developers advance portable infusion pumps and pre-mixed nutrient bags that enhance safety and convenience in non-clinical settings.

These innovations facilitate specialized drips for hangover relief, athletic endurance support, and immune boosting during cold and flu season. Opportunities emerge in preventive IV protocols for travelers and frequent flyers, addressing dehydration and fatigue from long-haul flights.

Companies invest in standardized, pharmaceutical-grade ingredients to ensure safety and consistency across elective therapies. In August 2025, ChromaDex introduced pharmaceutical-grade intravenous Niagen, a formulation containing nicotinamide riboside chloride.

The product is positioned as an alternative to conventional NAD+ IV therapies, supporting cellular health and metabolic function through a clinically standardized compound. In March 2025, beOnd Airlines partnered with The Elixir Clinic to provide passengers with optional IV VitaDrip therapy linked to flight bookings.

The wellness service is available for travelers on select routes connecting Dubai, the Maldives, and Zurich, offering hydration and recovery support before or after long-haul travel. Recent trends emphasize concierge-style services, evidence-based formulations, and hybrid medical-wellness models, positioning IV hydration therapy as a versatile tool for both acute care and proactive health maintenance.

Key Takeaways

- In 2025, the market generated a revenue of US$ 2.6 Billion, with a CAGR of 10.2%, and is expected to reach US$ 6.9 Billion by the year 2035.

- The service segment is divided into energy boosters, immune boosters, hydration, beauty/ aesthetics, detoxification, longevity/ antiaging, performance/ athletics, migraine & pain relief, flu/stomach and others, with energy boosters taking the lead with a market share of 27.1%.

- Considering component, the market is divided into medicated and non-medicated. Among these, medicated held a significant share of 68.5%.

- Furthermore, concerning the provider segment, the market is segregated into physical providers and mobile providers. The physical providers sector stands out as the dominant player, holding the largest revenue share of 78.1% in the market.

- The end-use segment is segregated into hospitals & clinics, wellness centers and spas, home healthcare and others, with the hospitals & clinics segment leading the market, holding a revenue share of 44.6%.

- North America led the market by securing a market share of 48.6%.

Service Analysis

Energy booster services accounted for 27.1% of growth within service and dominate the intravenous hydration therapy market due to increasing consumer interest in rapid fatigue recovery and improved physical performance. Many individuals seek IV vitamin therapies containing vitamin B complex, vitamin C, and electrolytes to address tiredness and dehydration.

Clinics offering hydration therapy report rising demand from professionals, athletes, and travelers who look for quick recovery solutions. Segment growth is expected to strengthen as lifestyle factors such as long working hours and travel-related fatigue increase globally. Wellness trends continue to promote intravenous nutrient therapy for faster nutrient absorption compared to oral supplements.

Medical professionals also incorporate IV energy therapy into recovery programs for dehydration and fatigue management. Demand is anticipated to expand as wellness clinics promote customized vitamin infusion programs. Growing awareness through health influencers and wellness marketing further supports expansion of energy booster services.

Component Analysis

Medicated IV therapies accounted for 68.5% of growth within component and dominate the market because these formulations include essential vitamins, minerals, and therapeutic drugs used for clinical treatment. Hospitals and clinics frequently administer medicated IV infusions to treat dehydration, electrolyte imbalances, infections, and nutritional deficiencies.

Healthcare data from the U.S. Centers for Disease Control and Prevention indicate that intravenous fluid therapy remains a routine treatment in hospitals for patients experiencing severe dehydration and illness. Segment growth is projected to strengthen as healthcare providers adopt targeted infusion protocols for faster recovery.

Physicians increasingly recommend vitamin-based infusion therapies to support immune function and fatigue management. Demand is likely to increase as medical facilities expand infusion therapy programs. Rising awareness of rapid intravenous nutrient delivery further reinforces adoption in both clinical and wellness settings.

Provider Analysis

Physical providers accounted for 78.1% of growth within provider type and dominate the intravenous hydration therapy market due to their established clinical infrastructure and patient trust. Hospitals, clinics, and specialized infusion centers provide supervised IV therapy services with trained medical professionals.

Patients prefer physical healthcare settings because they offer safety monitoring and regulated treatment environments. Segment growth is expected to accelerate as infusion therapy clinics expand across urban healthcare networks. Licensed medical supervision improves treatment reliability and patient confidence.

Healthcare providers also offer personalized hydration treatments tailored to medical conditions. Demand is anticipated to rise as wellness clinics and hospitals integrate IV therapy into broader preventive health programs. Expansion of outpatient infusion centers further strengthens the role of physical providers in this market.

End-Use Analysis

Hospitals and clinics accounted for 44.6% of growth within end use and dominate the intravenous hydration therapy market due to their high patient volume and access to trained healthcare professionals. Medical facilities regularly administer IV fluids to treat dehydration, infections, gastrointestinal illnesses, and postoperative recovery conditions.

Hospital-based infusion therapy programs support controlled dosing and patient monitoring during treatment. Segment growth is projected to strengthen as healthcare providers emphasize faster recovery and improved hydration management for patients. Hospitals also treat large numbers of emergency cases involving dehydration and electrolyte imbalance.

Clinical guidelines encourage intravenous fluid administration for patients who require rapid hydration. Demand is likely to increase as outpatient clinics expand infusion therapy services to manage chronic conditions and fatigue-related health issues.

Key Market Segments

By Service

- Energy Boosters

- Immune Boosters

- Hydration

- Beauty/ Aesthetics

- Detoxification

- Longevity/ Antiaging

- Performance/ Athletics

- Migraine & Pain Relief

- Flu/Stomach

- Others

By Component

- Medicated

- Non-medicated

By Provider

- Physical Providers

- Mobile Providers

By End-use

- Hospitals & Clinics

- Wellness Centers and Spas

- Home Healthcare

- Others

Drivers

Increasing revenue in Infusion Systems at ICU Medical is driving the market.

ICU Medical’s Infusion Systems segment, which includes products essential for intravenous hydration delivery, exhibited consistent expansion over the recent years. Net sales for this segment totaled $617.4 million in 2022. The figure rose to $629.0 million in 2023, representing a 1.9% increase. In 2024, revenue advanced to $652.4 million, reflecting a 3.7% growth from the prior year.

Full-year 2025 net sales reached $684.2 million, achieving a 4.9% rise compared to 2024. This progression underscores sustained demand for reliable infusion devices in clinical and outpatient settings. Healthcare facilities increasingly integrate these systems to support efficient fluid administration protocols.

The revenue growth facilitates ongoing enhancements in pump technology and connectivity features. Providers benefit from scalable solutions that align with volume-based care models. This driver bolsters market confidence and encourages broader adoption of advanced hydration technologies.

Restraints

Supply shortages of sodium chloride 0.9 percent IV solutions is restraining the market.

Disruptions in the production of critical IV fluids have imposed significant challenges on hydration therapy availability. The Centers for Disease Control and Prevention issued an alert on October 30, 2024, regarding supply interruptions of intravenous solutions stemming from damage to Baxter International’s manufacturing facility. This event followed Hurricane Helene’s impact in late September 2024, exacerbating national shortages.

The Food and Drug Administration added sodium chloride 0.9% injection to its drug shortages list in October 2024. Hospitals and clinics faced rationing measures, delaying elective hydration procedures and complicating emergency care. The shortage persisted through early 2025, affecting over 50% of U.S. healthcare facilities according to federal reports.

Providers shifted to alternative formulations, incurring additional costs and logistical burdens. The restraint highlighted vulnerabilities in single-source manufacturing dependencies. Resolution occurred on August 8, 2025, when the FDA announced the shortage’s end. This period constrained overall market fluidity and innovation investments during 2024-2025.

Opportunities

Expansion of franchise networks in wellness IV hydration is creating growth opportunities.

Prime IV Hydration & Wellness achieved systemwide revenue of $100 million in 2025. This milestone accompanied the opening of over 200 operating locations nationwide by year-end. The franchise model enables rapid scalability in urban and suburban markets seeking on-demand hydration services.

Opportunities emerge for customized therapy menus targeting athletes, professionals, and wellness enthusiasts. Integrated mobile units extend reach to events and corporate settings without fixed infrastructure needs. The growth supports development of proprietary vitamin-infused formulations under medical oversight.

Partnerships with fitness centers and spas amplify cross-promotional channels. Investors recognize the model’s resilience amid rising preventive health trends. Such expansion fosters job creation in nursing and administrative roles. This opportunity positions the sector for diversified revenue beyond traditional clinical environments.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic shifts influence the intravenous hydration therapy market through clinic operating costs, patient discretionary spending, and healthcare service pricing. Inflation raises expenses for IV fluids, vitamins, sterile kits, and clinical staffing, which pressures margins for wellness clinics and medical providers.

Higher interest rates reduce capital availability for new clinic openings and mobile therapy services. Geopolitical tensions disrupt global supply of saline bags, infusion sets, and pharmaceutical ingredients, which creates procurement uncertainty. Current US tariffs on imported medical disposables and packaging materials increase supply costs and challenge pricing strategies for providers.

These financial pressures can slow expansion of boutique hydration centers and elective wellness services. At the same time, providers improve supplier diversification and strengthen domestic sourcing to secure reliable inventories. Rising consumer interest in preventive health, recovery therapies, and outpatient treatments continues to support steady and confident market growth.

Latest Trends

FDA clearances for Plum Solo and Plum Duo precision IV pumps is driving the market.

ICU Medical secured U.S. Food and Drug Administration 510(k) clearances for the Plum Solo and Plum Duo infusion pumps on April 7, 2025. These devices introduce a new category of compact, single- and dual-channel systems optimized for ambulatory and bedside hydration delivery. The Solo model supports one infusion line with intuitive touchscreen controls for simplified operation.

The Duo variant enables simultaneous administration of multiple fluids, enhancing efficiency in complex therapy regimens. Both incorporate wireless connectivity for real-time monitoring and data integration into electronic health records. The clearances classify them as Class II devices under product code MRZ for infusion pumps.

Clinical evaluations demonstrated equivalence to predicate devices without new safety concerns. The launch addresses demands for lightweight, portable options in home and hospital transitions. Providers anticipate reduced setup times and improved patient mobility with these innovations. This development accelerates the integration of smart infusion technologies into standard hydration practices.

Regional Analysis

North America is leading the Intravenous Hydration Therapy Market

North America accounted for 48.6% of the intravenous hydration therapy market in 2025 as healthcare providers expanded infusion services to address dehydration, nutrient deficiencies, and recovery needs across hospitals and outpatient wellness clinics. Rising demand for rapid rehydration treatments in emergency departments and urgent care facilities strengthened utilization of intravenous fluid therapies.

The Centers for Disease Control and Prevention reported in 2023 that the United States recorded more than 2.8 million emergency department visits associated with heat related illnesses between 2018 and 2022, underscoring the continued clinical importance of rapid hydration treatment in acute care settings.

Hospitals and mobile infusion providers increasingly introduced specialized hydration services to support patients recovering from infections, gastrointestinal illness, and chronic fatigue conditions. Growing interest in preventive wellness therapies also encouraged consumers to seek vitamin infused hydration treatments offered by outpatient clinics.

Medical providers expanded home based infusion programs that allow patients to receive fluid therapy without hospital admission. Healthcare networks have also strengthened clinical protocols that rely on intravenous fluids for electrolyte balance and postoperative recovery.

Technological improvements in infusion pumps and sterile fluid preparation have improved safety and treatment efficiency. These developments collectively contributed to steady expansion of hydration therapy services across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience notable growth during the forecast period as expanding healthcare infrastructure and rising awareness of hydration related health conditions increase demand for clinical fluid administration services. Many countries in the region are strengthening emergency and primary healthcare systems to address heat stress, infectious diseases, and dehydration associated with extreme climate conditions.

The World Health Organization reported in 2023 that heat related illnesses are increasing globally as climate change intensifies extreme temperature exposure, creating greater need for effective clinical rehydration treatments in vulnerable populations. Governments across countries such as India, China, and Southeast Asian nations are investing in hospital capacity and emergency medical response programs to manage climate related health risks.

Hospitals and outpatient care providers are expanding infusion services to treat dehydration linked to gastrointestinal infections, dengue fever, and other regional illnesses. Increasing healthcare access and urbanization are also enabling more patients to receive clinical fluid replacement therapies when needed.

Private wellness clinics across major cities are introducing nutrient infusion services aimed at fatigue recovery and general health support. Regional pharmaceutical manufacturers are strengthening supply chains for sterile intravenous fluids and infusion equipment. These combined developments are expected to support sustained expansion of clinical hydration therapy services across Asia Pacific in the coming years.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key companies in the Intravenous Hydration Therapy market expand their presence by introducing personalized nutrient infusion programs, mobile treatment services, and wellness-focused IV clinics that deliver treatments at homes, hotels, and fitness centers.

Firms invest in partnerships with healthcare professionals and licensed nurses to strengthen clinical credibility while improving patient access to rapid hydration therapies. The rising demand for preventive wellness services and quick recovery solutions among athletes, travelers, and health-conscious consumers also encourages companies to broaden service portfolios and digital appointment platforms.

Baxter International represents a notable participant in the Intravenous Hydration Therapy market and operates as a global healthcare company headquartered in Illinois that develops infusion systems, IV solutions, and hospital care products used worldwide. The company focuses on advanced infusion technologies and reliable fluid delivery systems that support hospitals and outpatient treatment centers.

Industry competitors also strengthen growth through regional clinic expansion, targeted wellness marketing, and technology-enabled monitoring tools that improve treatment convenience. These initiatives help organizations capture rising demand for on-demand hydration services and broaden the reach of the Intravenous Hydration Therapy market.

Top Key Players

- Baxter

- B. Braun SE

- Otsuka Pharmaceutical Co., Ltd.

- Grifols, S.A.

- JW Life Science Corporation

- Amanta Healthcare

- NexGen Health

- Core IV Therapy, LLC

- Cryojuvenate UK Ltd.

- Drip Hydration

- REVIV

Recent Developments

- In August 2025, NEXTDRIP Mobile IV Therapy expanded its services by opening a new location in Burbank, California. The facility supports the delivery of mobile intravenous hydration treatments provided by licensed clinicians, allowing clients to receive personalized wellness therapies for hydration, recovery, energy, and immune support at home, workplaces, or events.

- In August 2025, AquaPulse IV introduced a mobile IV therapy service in Fredericksburg, Virginia. The service delivers customized intravenous hydration and vitamin infusions directly to homes, offices, and event locations, focusing on improving hydration levels, supporting immune health, and aiding post-activity recovery.

- In August 2025, a group of registered nurses launched a mobile IV hydration service covering the Atlanta Perimeter region. The business provides on-site IV therapy treatments designed to address dehydration, fatigue, migraines, and recovery needs through convenient in-home or workplace visits.

Report Scope

Report Features Description Market Value (2025) US$ 2.6 Billion Forecast Revenue (2035) US$ 6.9 Billion CAGR (2026-2035) 10.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Service (Energy Boosters, Immune Boosters, Hydration, Beauty/ Aesthetics, Detoxification, Longevity/ Antiaging, Performance/ Athletics, Migraine & Pain Relief, Flu/Stomach and Others), By Component (Medicated and Non-medicated), By Provider (Physical Providers and Mobile Providers), By End-use (Hospitals & Clinics, Wellness Centers and Spas, Home Healthcare and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Baxter, B. Braun SE, Otsuka Pharmaceutical, Grifols, JW Life Science, Amanta Healthcare, NexGen Health, Core IV Therapy, Cryojuvenate UK, Drip Hydration, REVIV. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Intravenous Hydration Therapy MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Intravenous Hydration Therapy MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Baxter

- B. Braun SE

- Otsuka Pharmaceutical Co., Ltd.

- Grifols, S.A.

- JW Life Science Corporation

- Amanta Healthcare

- NexGen Health

- Core IV Therapy, LLC

- Cryojuvenate UK Ltd.

- Drip Hydration

- REVIV

Our Clients

- 180762

- March 2026