Global Ileostomy Market By Product Type (Ileostomy Bags, Ileostomy Accessories and Ileostomy Irrigation Supplies), By Indication (Inflammatory Bowel Disease, Colorectal Cancer, Bowel Obstruction, Familial Adenomatous Polyposis and Others), By End User (Hospitals, Ambulatory Surgical Centers (ASCs), Home Care Settings and Specialty Clinics), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182435

- Number of Pages: 377

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

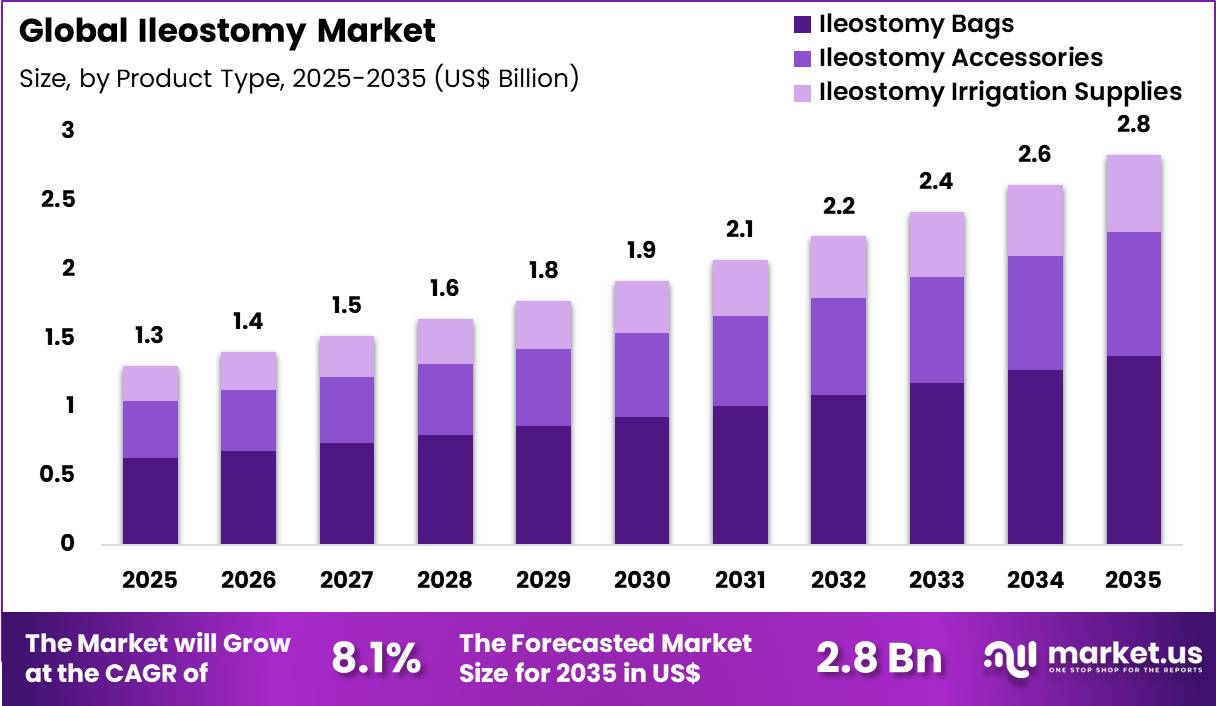

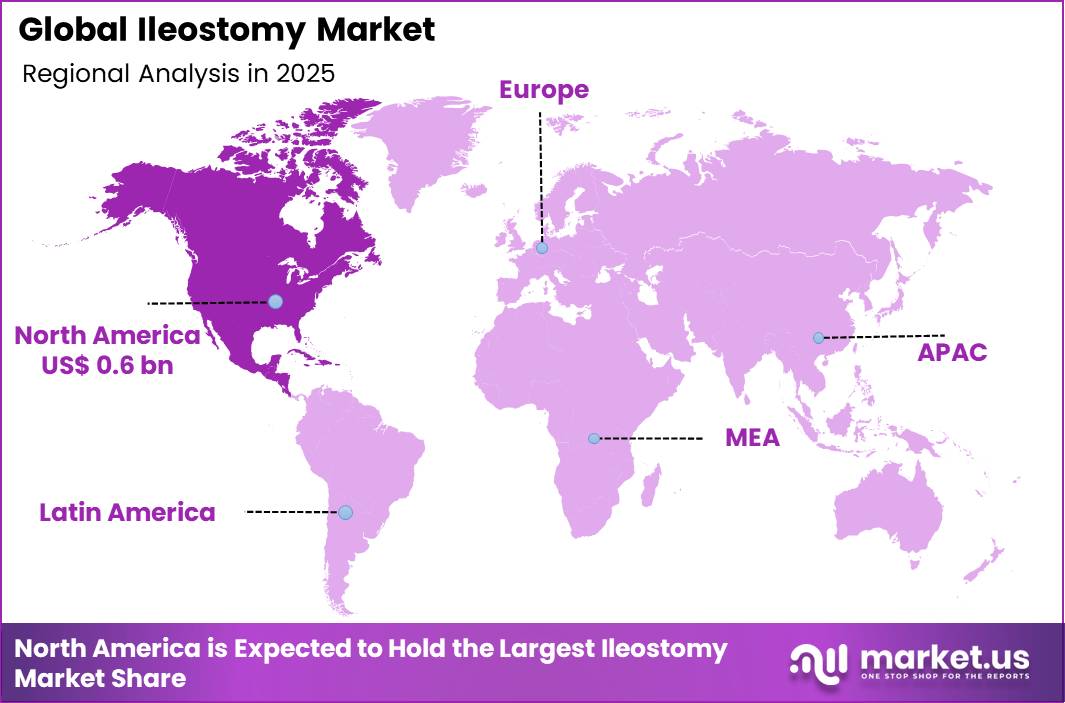

The Ileostomy Market size is expected to be worth around US$ 2.8 Billion by 2035 from US$ 1.3 Billion in 2025, growing at a CAGR of 8.1% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 42.2% share with a revenue of US$ 0.6 Billion.

Increasing prevalence of colorectal cancer, inflammatory bowel diseases, and trauma-related bowel resections drives the Ileostomy market as surgeons perform more diverting ileostomies to protect distal anastomoses and improve patient outcomes in complex abdominal procedures.

Colorectal surgeons increasingly create temporary loop ileostomies following low anterior resection for rectal cancer, diverting fecal stream to reduce anastomotic leak risk and facilitate safer healing in patients undergoing neoadjuvant chemoradiation.

These stomas support permanent end ileostomies in cases of total colectomy for ulcerative colitis or familial adenomatous polyposis, providing definitive fecal diversion when sphincter preservation proves impossible or undesirable. In emergency settings, trauma surgeons fashion ileostomies after bowel perforation or mesenteric vascular injury, controlling contamination and stabilizing patients for staged reconstruction.

Ileostomies also enable continent diversion options in select patients, where surgeons construct ileal pouches or continent cutaneous reservoirs to restore voluntary continence after proctocolectomy. Palliative ileostomies offer relief from malignant bowel obstruction in advanced cancers, improving quality of life by bypassing obstructed segments in patients with limited life expectancy.

Manufacturers pursue opportunities to develop advanced skin barriers and pouching systems that enhance adhesion and skin protection, expanding applications in post-operative care where stoma output and peristomal skin changes require adaptable solutions.

These advancements support moldable technologies that conform to irregular or retracted stomas, simplifying appliance changes and reducing leakage incidents in the early postoperative period. Opportunities emerge in digital health integrations that track output volume, hydration status, and peristomal skin health, enabling remote monitoring for patients transitioning to home care.

Companies invest in patient education tools and ergonomic pouch designs that improve comfort and discretion for active individuals. In late 2025, Convatec released findings from a global Delphi consensus study focused on moldable ostomy technologies.

The results supported increased adoption of adaptable skin barriers that can conform to changes in stoma size after surgery, reducing the need for manual adjustments and simplifying post-operative care routines.

Recent trends emphasize patient-centered ostomy management, improved barrier adaptability, and supportive digital tools, positioning the market for growth in enhanced quality of life and reduced complications for ileostomy patients across surgical indications.

Key Takeaways

- In 2025, the market generated a revenue of US$ 1.3 Billion, with a CAGR of 8.1%, and is expected to reach US$ 2.8 Billion by the year 2035.

- The product type segment is divided into ileostomy bags, ileostomy accessories and ileostomy irrigation supplies, with ileostomy bags taking the lead with a market share of 48.5%.

- Considering indication, the market is divided into inflammatory bowel disease, colorectal cancer, bowel obstruction, familial adenomatous polyposis and others. Among these, inflammatory bowel disease (ibd)held a significant share of 43.6%.

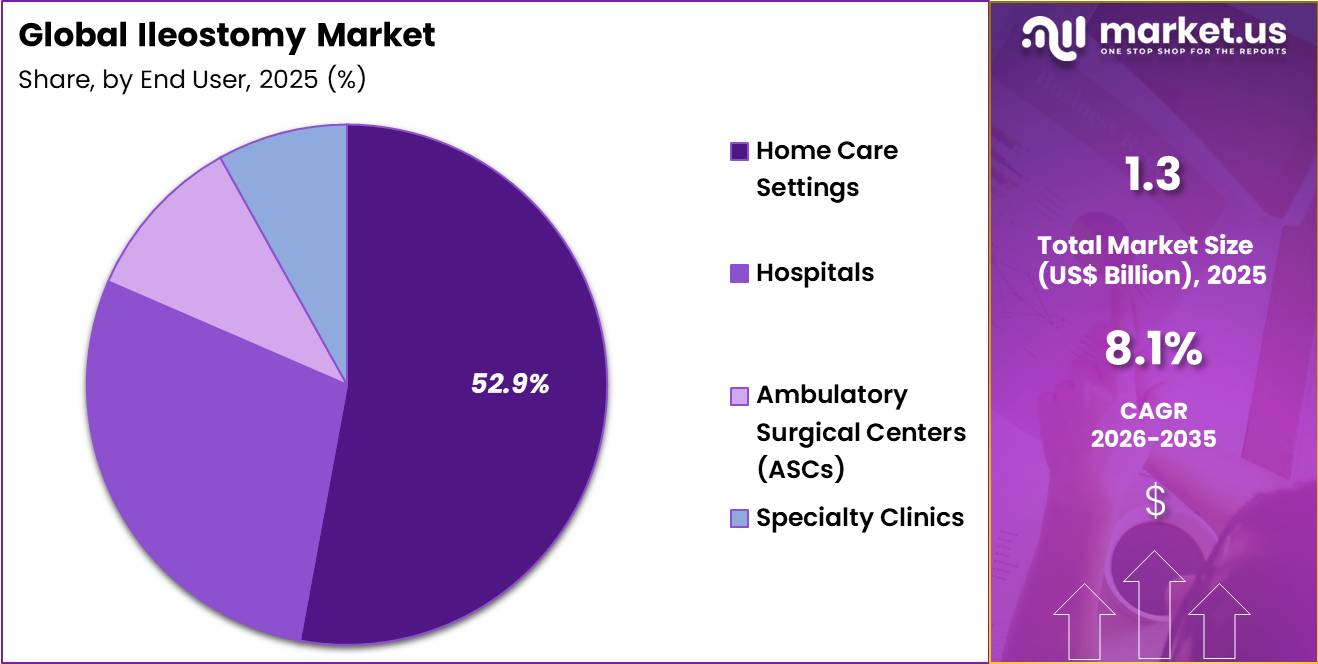

- Furthermore, concerning the end user segment, the market is segregated into hospitals, ambulatory surgical centers (ASCs), home care settings and specialty clinics. The home care settings sector stands out as the dominant player, holding the largest revenue share of 52.9% in the market.

- North America led the market by securing a market share of 42.2%.

Product Type Analysis

Ileostomy bags accounted for 48.5% of growth within product type and dominate the ileostomy market because they are the primary collection system required for daily stoma management after surgery.

Every ileostomy patient depends on pouching systems for waste collection, odor control, leakage prevention, and skin protection, which keeps demand consistently high across short-term and long-term care pathways. NIDDK notes that after ileostomy or colostomy surgery, patients use an ostomy pouch attached around the stoma to collect intestinal contents and gas, which confirms the essential role of this product category.

The segment is expected to grow steadily because patients replace bags frequently, unlike many accessories that have longer usage cycles. Manufacturers also continue to improve wear time, adhesive performance, comfort, and discretion, which supports wider adoption of premium pouching systems.

Demand is likely to remain strong as healthcare providers place greater emphasis on patient comfort, skin integrity, and independent stoma care. Rising ostomy procedure volumes and better survival outcomes in chronic bowel conditions are projected to expand the long-term user base.

Home-based care trends also favor ileostomy bags because they simplify routine self-management outside institutional settings. As product innovation and repeat purchase frequency remain central to this market, ileostomy bags are anticipated to retain their dominant position.

Indication Analysis

Inflammatory bowel disease accounted for 43.6% of growth within indication and dominates the ileostomy market because severe Crohn’s disease and ulcerative colitis often require bowel surgery when medication fails or complications progress. NIDDK states that ostomy surgery may be needed when part or all of the bowel is diseased, injured, or missing, and this directly aligns with advanced IBD treatment pathways.

The underlying patient pool also remains substantial. The Crohn’s & Colitis Foundation reported in 2023 that nearly 1 in 100 Americans has IBD, and in 2024 it estimated that 100,429 American youth under age 20 are living with the disease.

This disease burden is expected to support continued procedural demand, especially in cases involving refractory inflammation, strictures, fistulas, or colectomy-related care. IBD patients often require long-term management and repeat clinical monitoring, which increases sustained consumption of ileostomy products after surgery.

The segment is projected to expand further as diagnosis rates improve and more patients gain access to specialist gastroenterology and colorectal care. Severe disease progression, younger diagnosis age in some patients, and greater awareness of surgical intervention are likely to reinforce this indication’s lead.

As chronic inflammatory bowel conditions continue to create a large and recurring need for diversion procedures, IBD is estimated to remain the dominant application segment in the ileostomy market.

End-User Analysis

Home care settings accounted for 52.9% of growth within end user and dominate the ileostomy market because most patients manage their stoma on a day-to-day basis after discharge rather than in acute care facilities.

NIDDK explains that ostomy nurses help patients choose a pouching system and support ongoing care after surgery, which reflects the shift from hospital treatment to self-management at home.

This care model is expected to strengthen as healthcare systems continue to reduce inpatient stays and encourage recovery in lower-cost settings. Home use drives steady demand for pouches, barriers, and maintenance products because patients must manage output, hygiene, and skin care continuously.

The segment also benefits from rising patient education, telehealth follow-up, and stronger availability of user-friendly ostomy supplies. Historical CDC data further illustrates the relevance of ostomy support in home health populations, reporting that 3.0% of home health care patients had a colostomy or ileostomy.

Patients are likely to prefer home care because it offers greater privacy, routine comfort, and independence once post-surgical recovery stabilizes. As more healthcare providers build structured discharge planning and ostomy training around at-home management, home care settings are projected to remain the leading end-user segment in the ileostomy market.

Key Market Segments

By Product Type

- Ileostomy Bags

- Ileostomy Accessories

- Ileostomy Irrigation Supplies

By Indication

- Inflammatory Bowel Disease

- Colorectal Cancer

- Bowel Obstruction

- Familial Adenomatous Polyposis

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Home Care Settings

- Specialty Clinics

Drivers

Rising incidence of colorectal cancer requiring permanent ileostomy creation is driving the market.

Colorectal cancer remains a leading indication for permanent ileostomy formation following total proctocolectomy or abdominoperineal resection. Surgical volumes have increased in response to earlier detection through screening programs and extended survival rates post-resection.

The driver aligns with population aging and higher lifetime risk of colorectal malignancy in developed regions. Surgeons perform conventional end ileostomies or loop ileostomies depending on disease extent and sphincter preservation feasibility.

Facilities report consistent procedural demand in colorectal and surgical oncology departments. The trend supports multidisciplinary tumor board decisions favoring ostomy over low anterior resection in select low-rectal cases. Enhanced preoperative counseling improves patient preparation and postoperative adaptation.

The expansion reflects sustained need for reliable fecal diversion in advanced or recurrent disease. This factor maintains steady utilization of ostomy appliances and accessories in long-term management. Overall, oncologic indications sustain core procedural volume and associated market activity.

Restraints

High lifetime cost burden of ostomy supplies for permanent ileostomies is restraining the market.

Patients with permanent ileostomies incur ongoing expenses for pouches, skin barriers, pastes, and accessories throughout their remaining lifespan. Insurance coverage frequently includes annual or lifetime caps that fail to match cumulative needs.

The restraint contributes to financial strain among older adults on fixed incomes or those with limited supplemental benefits. Many individuals ration supplies or select lower-cost alternatives that compromise skin integrity. The factor moderates demand for premium adhesive systems and convexity options

. Providers encounter challenges securing prior authorization for specialized products. The dynamic influences adherence to manufacturer-recommended change schedules. This constraint limits broader adoption of advanced pouching systems designed for extended wear.

The limitation persists in constraining market penetration for higher-value consumables. Economic barriers continue to shape purchasing patterns in chronic ostomy care.

Opportunities

Development of continent ileostomy reservoirs and continent diversion techniques is creating growth opportunities.

Surgeons are refining continent ileostomy procedures including the Barnett continent internal reservoir and Kock pouch configurations for select patients. These techniques provide fecal continence without external pouching through an internal reservoir and nipple valve mechanism.

Opportunities arise for improved quality of life in motivated patients willing to perform intermittent self-catheterization. The framework supports reduced skin complications and clothing restrictions associated with conventional ileostomies. Developers can pursue training programs and simulation modules for safe technique dissemination.

The development facilitates collaboration between colorectal surgeons and enterostomal therapists for patient selection. Such advancements attract interest from younger patients seeking body image preservation. The opportunity fosters differentiation through superior functional outcomes in appropriate candidates.

Stakeholders anticipate gradual expansion in centers with specialized expertise. This progression positions participants for innovation in continent diversion options.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic trends and geopolitical shifts are actively influencing demand, pricing, and supply continuity in the ileostomy market. Rising healthcare expenditure and aging populations support procedure volumes and long-term product usage, while inflation increases the cost of ostomy bags, adhesives, and related consumables, putting pressure on patient affordability and reimbursement systems.

Currency volatility and trade disruptions further complicate procurement for hospitals and home care providers that rely on imported medical-grade polymers and components. Geopolitical tensions also affect global supply chains, leading to delays in product availability and higher logistics costs across regions.

Current US tariffs on imported ostomy supplies and raw materials increase input costs for manufacturers and elevate prices for end users, particularly in markets dependent on international sourcing.

Tariff-driven cost escalation can limit accessibility for patients requiring continuous care, yet it also pushes companies to localize production and diversify suppliers. At the same time, industry concerns highlight that tariffs may restrict device availability and slow innovation in essential care products.

Despite these challenges, strong clinical demand, increasing awareness, and expanding domestic manufacturing capabilities are expected to support stable and resilient market growth over time.

Latest Trends

Increased utilization of loop ileostomy for temporary fecal diversion is driving the market.

Loop ileostomies have become the preferred method for proximal diversion during low anterior resection and restorative proctocolectomy with ileal pouch-anal anastomosis. These stomas facilitate early postoperative anastomotic assessment and protect downstream anastomoses from fecal stream exposure.

The 2024-2025 period reflects widespread adoption of protective loop ileostomy in rectal cancer surgery protocols. Surgeons benefit from straightforward creation and reversal procedures with low morbidity. The trend aligns with evidence-based guidelines recommending diversion in high-risk pelvic anastomoses.

Facilities report reduced clinical anastomotic leak rates with protective stomas in place. The increased deployment supports standardized reversal timing at 8-12 weeks postoperatively. Early closure protocols demonstrate safety in selected patients.

The advancement stimulates demand for compatible pouching systems during the diversion period. Overall, this protective strategy strengthens surgical safety and sustains accessory consumption during the temporary phase.

Regional Analysis

North America is leading the Ileostomy Market

North America accounted for 42.2% of the ileostomy market in 2025 as healthcare systems expanded colorectal surgery programs and long-term stoma care management for patients with inflammatory bowel disease and colorectal cancer.

The region continues to report a high burden of gastrointestinal disorders requiring surgical intervention, with the American Cancer Society estimating about 153020 new colorectal cancer cases in the United States in 2023, supporting sustained demand for ostomy procedures including ileostomy.

Hospitals across the United States and Canada are strengthening multidisciplinary colorectal care pathways that integrate surgery, postoperative care, and long-term patient support. Surgeons are increasingly adopting minimally invasive and robotic-assisted techniques that improve surgical precision and reduce recovery time.

Specialized ostomy care nurses and outpatient clinics are improving patient education, helping individuals manage stoma care effectively and reduce complications. Medical device companies are introducing advanced pouching systems, skin barriers, and accessories that enhance comfort and quality of life.

Growing awareness of chronic bowel diseases has also encouraged earlier diagnosis and treatment, increasing procedure volumes. Healthcare reimbursement support and patient assistance programs are improving access to ostomy care products. These developments collectively supported steady expansion of ileostomy care solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness strong expansion during the forecast period as healthcare infrastructure improves and awareness of gastrointestinal diseases increases across the region. Countries such as China, India, Japan, and South Korea are expanding colorectal surgery capabilities to address rising incidence of digestive disorders and cancer.

The World Health Organization reported that colorectal cancer ranks among the top causes of cancer-related deaths globally, highlighting the growing need for surgical treatment and postoperative care solutions. Hospitals across the region are investing in advanced surgical technologies and expanding access to specialized gastrointestinal care.

Increasing urbanization and lifestyle changes are contributing to higher prevalence of inflammatory bowel diseases, driving demand for surgical interventions. Governments are strengthening public healthcare systems and promoting early disease screening programs.

Medical device manufacturers are introducing affordable ostomy products tailored to regional healthcare needs. Training programs for healthcare professionals are improving expertise in stoma care and patient management. These developments are expected to accelerate adoption of ileostomy care products and services across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Ileostomy Market expand growth by developing advanced ostomy appliances, improving skin-friendly adhesive technologies, and strengthening patient support programs that enhance long-term usability and comfort.

Companies collaborate with hospitals, stoma care nurses, and home healthcare providers to improve post-surgical care and product adoption among patients. They also invest in discreet pouch designs, odor control systems, and digital education platforms that help patients manage daily liv

ing more effectively. Coloplast A/S represents a prominent participant in the Ileostomy Market and operates as a Denmark-based medical device company that develops ostomy care products, continence solutions, and wound care technologies for patients worldwide.

The company focuses on user-centric product design and clinical collaboration to improve patient outcomes and quality of life. Industry competitors continue to introduce innovative ostomy solutions, expand distribution networks, and strengthen clinical support services to drive adoption and sustain long-term market growth.

Top Key Players

- Smith & Nephew

- Convatec Inc.

- 3M Healthcare (Solventum)

- B. Braun Melsungen AG

- Coloplast

- Hollister Incorporated

- Salts Healthcare

- Flexicare Medical Ltd.

- Marlen Manufacturing

- Pelican Healthcare

Recent Developments

- In March 2026, Hollister Incorporated secured a three-year group purchasing agreement with Premier, Inc. for its enterostomal therapy products. The contract expands access to its CeraPlus portfolio, which incorporates ceramide-infused barriers designed to support and protect peristomal skin following surgery.

- During 2025, Coloplast expanded the rollout of its Heylo digital monitoring system, developed to detect early signs of leakage in ostomy care. The technology uses a sensor layer placed beneath the barrier to identify moisture and notify users through connected mobile devices, helping improve patient confidence and day-to-day management.

Report Scope

Report Features Description Market Value (2025) US$ 1.3 Billion Forecast Revenue (2035) US$ 2.8 Billion CAGR (2026-2035) 8.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Ileostomy Bags, Ileostomy Accessories and Ileostomy Irrigation Supplies), By Indication (Inflammatory Bowel Disease, Colorectal Cancer, Bowel Obstruction, Familial Adenomatous Polyposis and Others), By End User (Hospitals, Ambulatory Surgical Centers (ASCs), Home Care Settings and Specialty Clinics) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Smith & Nephew, Convatec Inc., 3M Healthcare, B. Braun Melsungen AG, Coloplast, Hollister Incorporated, Salts Healthcare, Flexicare Medical Ltd., Marlen Manufacturing, Pelican Healthcare. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Smith & Nephew

- Convatec Inc.

- 3M Healthcare (Solventum)

- B. Braun Melsungen AG

- Coloplast

- Hollister Incorporated

- Salts Healthcare

- Flexicare Medical Ltd.

- Marlen Manufacturing

- Pelican Healthcare

Our Clients

- 182435

- March 2026