Quick Navigation

Report Overview

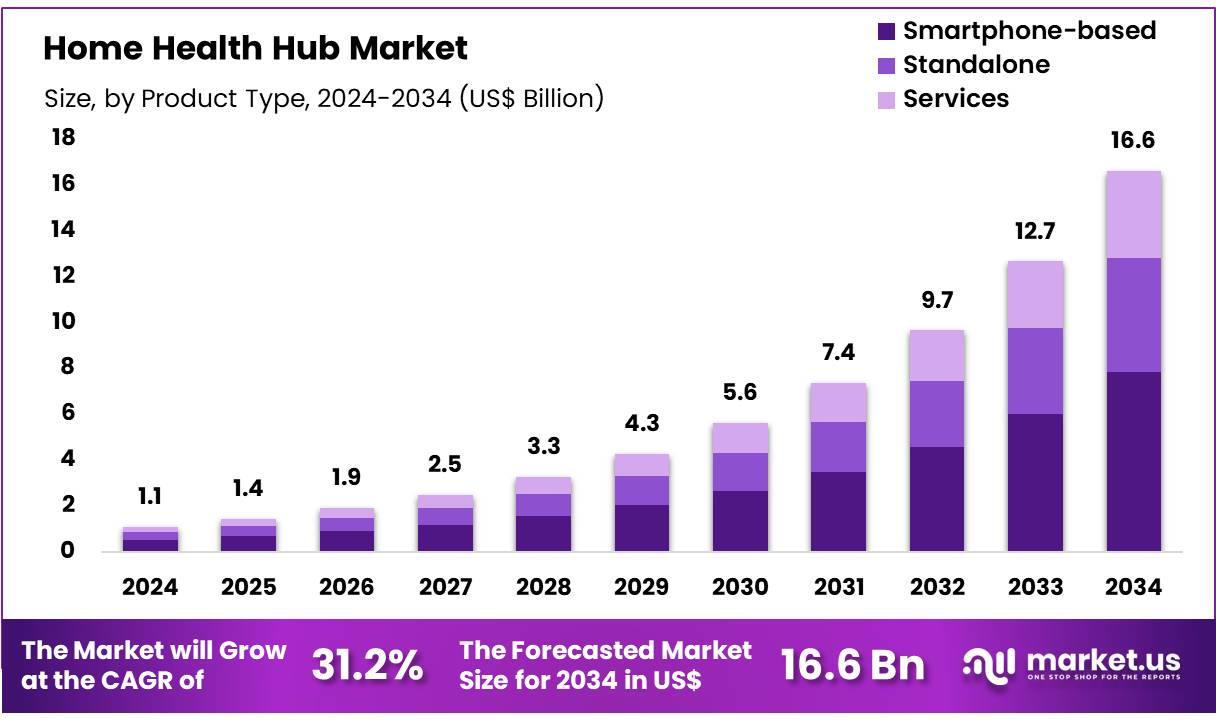

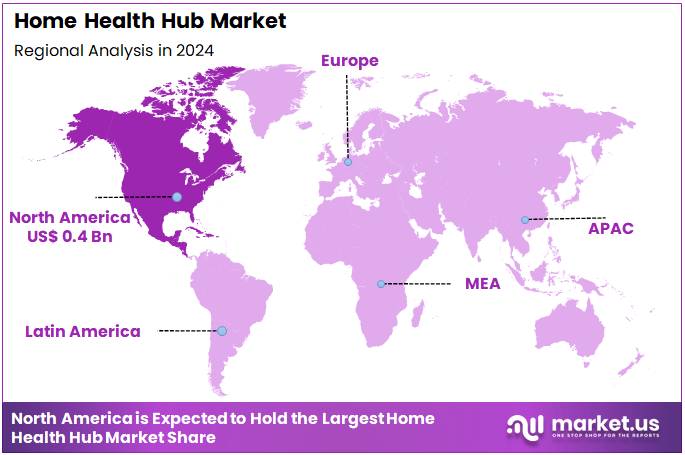

Global Home Health Hub Market size is expected to be worth around US$ 16.6 Billion by 2034 from US$ 1.1 Billion in 2024, growing at a CAGR of 31.2% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.5% share with a revenue of US$ 0.4 Billion.

Rising demand for integrated healthcare management fuels the growth of the home health hub market, which enables seamless coordination of remote patient monitoring, chronic disease management, and telehealth services. Home health hubs serve as centralized platforms that collect and transmit vital health data, facilitating real-time communication between patients and healthcare providers.

These systems support various applications, including medication adherence, emergency alerts, and personalized care plans, thereby improving patient outcomes while reducing hospital readmissions. The acquisition of Capsule Technologies, Inc. by Philips in January 2021 strengthened the development of advanced healthcare management solutions, further propelling innovation in home health hubs.

This market benefits from the increasing prevalence of chronic diseases and the aging population, which drive the need for continuous and convenient care at home. Opportunities emerge from advancements in IoT, wearable devices, and AI integration, allowing more accurate health monitoring and predictive analytics. Recent trends highlight the incorporation of multi-device compatibility and enhanced data security measures to address privacy concerns.

Additionally, healthcare providers increasingly adopt these hubs to extend care beyond traditional clinical settings, fostering patient engagement and self-management. The evolution of reimbursement policies and government support for remote healthcare also encourage widespread adoption. Home health hubs ultimately promote cost-effective care delivery by minimizing hospital visits and optimizing resource allocation. As technology advances, these hubs are set to become indispensable components of modern healthcare ecosystems, supporting preventive care and improving quality of life.

Key Takeaways

- In 2024, the market for Home Health Hub generated a revenue of US$ 1.1 billion, with a CAGR of 31.2%, and is expected to reach US$ 16.6 billion by the year 2034.

- The product type segment is divided into smartphone-based, standalone, and services, with smartphone-based taking the lead in 2024 with a market share of 47.3%.

- Considering patient monitoring type, the market is divided into high-acuity, moderate-acuity, and low-acuity. Among these, high-acuity held a significant share of 42.8%.

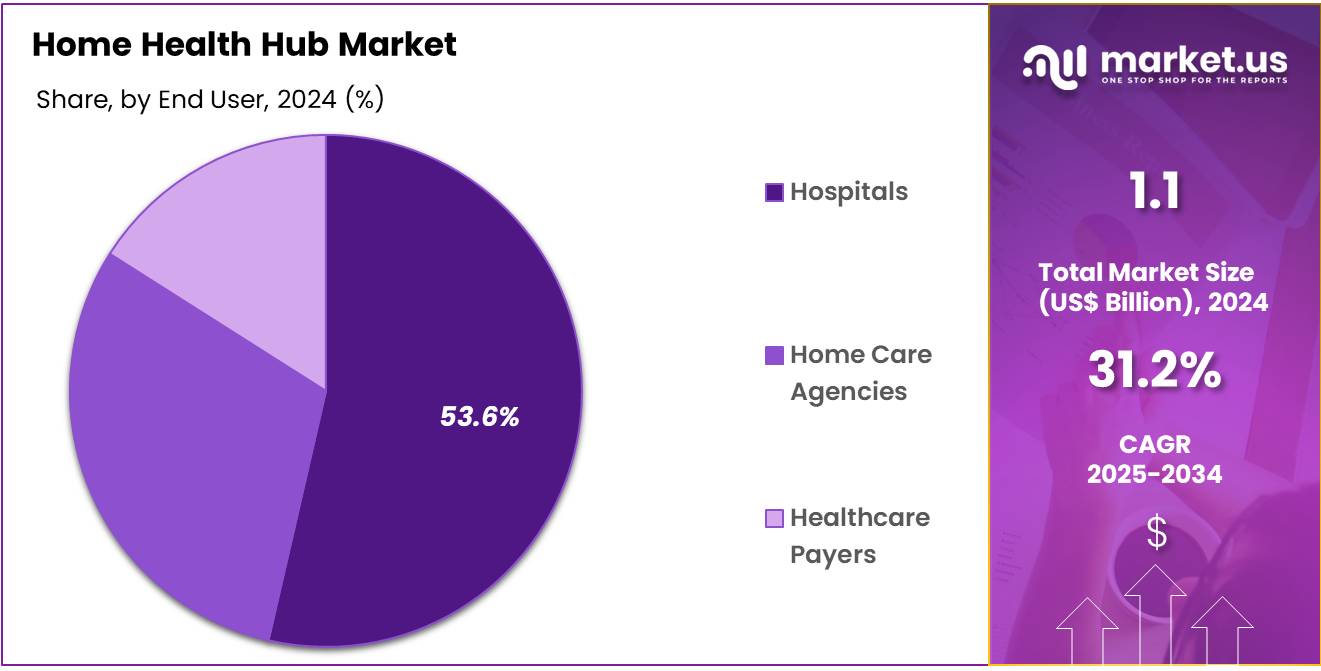

- Furthermore, concerning the end user segment, the market is segregated into hospitals, home care agencies, and healthcare payers. The hospitals sector stands out as the dominant player, holding the largest revenue share of 53.6% in the Home Health Hub market.

- North America led the market by securing a market share of 39.5% in 2024.

Product Type Analysis

The smartphone-based segment claimed a market share of 47.3%. Increasing smartphone penetration and consumer preference for mobile health solutions drive this expansion. Smartphone-based hubs offer seamless integration with wearable devices and health apps, enabling real-time health monitoring and remote consultations. These devices provide convenience, affordability, and user-friendly interfaces, attracting a broad user base.

Additionally, advancements in mobile technology and enhanced connectivity support more accurate data collection and transmission. Healthcare providers and patients alike benefit from the portability and accessibility of smartphone-based systems, accelerating adoption in both personal and clinical settings.

Patient Monitoring Type Analysis

The high-acuity held a significant share of 42.8% due to the rising demand for intensive monitoring of critically ill or complex patients outside traditional hospital settings. Increasing prevalence of chronic diseases and the aging population necessitate continuous and precise monitoring solutions. High-acuity devices provide advanced features such as multi-parameter tracking and alert systems, ensuring timely interventions.

Healthcare providers emphasize reducing hospital readmissions and improving patient outcomes, fueling investment in these sophisticated monitoring tools. Integration with telehealth platforms further amplifies the relevance and adoption of high-acuity segments in home care.

End User Analysis

The hospitals segment had a tremendous growth rate, with a revenue share of 53.6% owing to their expanding role in integrating home-based care with inpatient services. Hospitals focus on enhancing patient care continuity and reducing lengths of stay by leveraging home health hubs for remote monitoring and post-discharge follow-ups.

Increasing healthcare costs and the shift towards value-based care models encourage hospitals to adopt technologies that improve efficiency and patient satisfaction. Furthermore, hospitals possess the infrastructure and expertise to manage and analyze health data generated from these hubs, supporting clinical decision-making and personalized care strategies, thereby driving the segment’s growth.

Key Market Segments

By Product Type

- Smartphone-Based

- Standalone

- Services

By Patient Monitoring Type

- High-Acuity

- Moderate-Acuity

- Low-Acuity

By End User

- Hospitals

- Home Care Agencies

- Healthcare Payers

Drivers

Rising Geriatric Population is driving the market

The increasing global geriatric population is a significant driver for the home health hub market. As the number of older adults rises, so does the prevalence of chronic diseases and the need for continuous health monitoring and support, often best provided in a home setting. According to the United Nations’ “World Population Ageing 2023” report, the percentage of the global population aged 65 years and above is projected to increase from 10% in 2022 to 16% by 2050.

This demographic shift creates a substantial demand for solutions that enable remote health monitoring, medication management, and timely interventions, all of which are facilitated by home health hubs. The preference of many older adults to age in place further amplifies this demand, making home health hubs a crucial tool for supporting their healthcare needs and independence.

Restraints

Data Security and Privacy Concerns are restraining the market

Despite the benefits, concerns regarding data security and the privacy of patient health information can restrain the adoption of home health hubs. These hubs collect and transmit sensitive medical data, making them potential targets for cyber threats. While specific, broadly verifiable statistics from government or key players on data breaches involving home health hubs between 2022 and 2024 are not readily available, the general awareness of cybersecurity risks in healthcare is high.

Patients and healthcare providers need assurance that the data collected through these devices is secure and compliant with regulations like HIPAA in the US. Lack of trust in the security of these systems can lead to reluctance in their adoption, thus posing a challenge to the market’s growth. Addressing these security concerns through robust encryption, secure data transmission protocols, and transparent data usage policies is essential for wider acceptance.

Opportunities

Advancements in Remote Patient Monitoring Technologies create growth opportunities

Continuous advancements in remote patient monitoring (RPM) technologies are creating significant growth opportunities for the home health hub market. These advancements include more sophisticated wearable sensors, AI-powered analytics for early detection of health changes, and more user-friendly interfaces. For instance, the increasing integration of medical-grade wearables that can track vital signs with greater accuracy is enhancing the capabilities of home health hubs.

According to a December 2024 White House press release, investments in home and community-based services (HCBS) reached nearly US$37 billion, aiming to improve long-term care, which often incorporates RPM technologies. These technological improvements make home health hubs more effective in providing proactive and personalized care, driving their adoption by both patients and healthcare providers seeking to improve outcomes and reduce hospitalizations.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions and geopolitical factors can influence the home health hub market in several ways. Economic downturns might lead to increased price sensitivity among consumers, potentially affecting the adoption of newer, potentially more expensive hub technologies. Conversely, government initiatives aimed at improving healthcare access and efficiency, which can be influenced by geopolitical considerations of national health security, might provide funding or incentives that boost market growth. Geopolitical tensions could also impact supply chains for electronic components used in these devices.

However, the fundamental drivers of the market, such as the aging population and the desire for cost-effective, in-home healthcare, are likely to remain strong. The increasing emphasis on digital health solutions globally suggests that despite macroeconomic and geopolitical fluctuations, the demand for technologies that support remote patient care will continue to rise, fostering innovation and market expansion in the long term.

Current US tariffs could have a mixed impact on the home health hub market. If tariffs are levied on imported electronic components or finished home health hub devices, this could increase the cost for US-based consumers and healthcare providers. Higher prices might slow down the adoption rate, particularly for more budget-conscious individuals or smaller healthcare organizations. On the other hand, tariffs could incentivize domestic manufacturing of these devices and their components, potentially leading to growth in the US-based industry over time.

Furthermore, if tariffs affect the broader economy, they could indirectly influence healthcare spending patterns. However, the growing demand for home-based healthcare solutions, driven by factors like an aging population and technological advancements, suggests that the market will likely adapt to these changes. While tariffs might present some financial challenges in the short term, the long-term trend towards greater adoption of technology for in-home healthcare is expected to continue, potentially spurring innovation and a more resilient domestic supply chain.

Latest Trends

Integration with Telehealth Services is a recent trend in the market

A prominent recent trend in the home health hub market is its increasing integration with telehealth services. This synergy allows for seamless transitions between remote monitoring and virtual consultations with healthcare professionals.

For example, a significant percentage of Health Resources and Services Administration (HRSA)-funded health centers utilized telehealth for primary care in 2023, indicating a growing reliance on remote healthcare delivery methods that can be enhanced by home health hubs. This integration enables continuous monitoring of a patient’s condition, with the ability to have a virtual consultation triggered by concerning data or a scheduled follow-up.

This trend is improving the convenience and accessibility of healthcare, particularly for those with mobility issues or living in remote areas, further driving the demand for home health hubs that can effectively connect patients with telehealth services.

Regional Analysis

North America is leading the Home Health Hub Market

North America dominated the market with the highest revenue share of 39.5% owing to the increasing preference for aging in place and the rising adoption of remote patient monitoring technologies. The US Census Bureau data indicates a growing population aged 65 and over, a demographic that often prefers home-based care.

Furthermore, the Centers for Medicare & Medicaid Services (CMS) are promoting home healthcare through various initiatives, recognizing its potential for cost-effective and patient-centered care. The increasing availability of connected medical devices that can transmit data to a central hub in the home also contributes to market expansion. This trend supports better management of chronic conditions and reduces the need for frequent hospital visits.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the increasing geriatric population across the region and a growing awareness of the benefits of home-based healthcare. Countries like Japan have a rapidly aging population, creating a substantial need for solutions that support independent living and remote monitoring.

Furthermore, the increasing adoption of telehealth services and the rising penetration of smart home devices in Asia Pacific are expected to drive the demand for in-home health management systems. Government initiatives focused on improving healthcare accessibility and affordability will also likely contribute to the expansion of this market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the home health hub market drive growth by integrating advanced technologies such as artificial intelligence (AI), machine learning, and cloud computing into their platforms. They focus on enhancing interoperability to ensure seamless data exchange among various healthcare systems. Strategic partnerships and acquisitions enable these companies to expand their service offerings and market reach. Emphasizing user-friendly interfaces and mobile accessibility ensures improved patient and caregiver engagement. Additionally, they invest in research and development to innovate and stay ahead in a rapidly evolving market.

Philips Healthcare exemplifies a leading entity in this domain. A division of Koninklijke Philips N.V., Philips Healthcare specializes in diagnostic imaging, patient monitoring systems, and health informatics. The company offers integrated solutions that connect patients, caregivers, and healthcare providers, aiming to improve patient outcomes and streamline care delivery. Philips Healthcare’s commitment to innovation and quality service has positioned it as a trusted partner in the home health hub market.

Top Key Players

- Vivify Health, Inc

- Qualcomm Technologies, Inc

- Koninklijke Philips

- Inhealthcare

- iHealth Lab

- Honeywell International

- Capsule Technologies Inc

- AMC Health

Recent Developments

- In July 2024, Star Health and Allied Insurance Company introduced home healthcare services across more than 50 cities in India. This expansion enables patients to receive medical care in the comfort of their own homes, improving accessibility and convenience for those needing healthcare services.

- In March 2022, VEON Ltd. reported the launch of Health Hub, the first integrated digital health platform in Bangladesh by its Banglalink mobile operator. This platform aims to revolutionize healthcare delivery in the country by combining various health services into a single digital solution.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 1.1 Billion |

| Forecast Revenue (2034) | US$ 16.6 Billion |

| CAGR (2025-2034) | 31.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Smartphone-Based, Standalone, and Services), By Patient Monitoring Type (High-Acuity, Moderate-Acuity, and Low-Acuity), End User (Hospitals, Home Care Agencies, and Healthcare Payers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Vivify Health, Inc, Qualcomm Technologies, Inc, Koninklijke Philips, Inhealthcare, iHealth Lab, Honeywell International, Capsule Technologies Inc, and AMC Health. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |