Quick Navigation

Report Overview

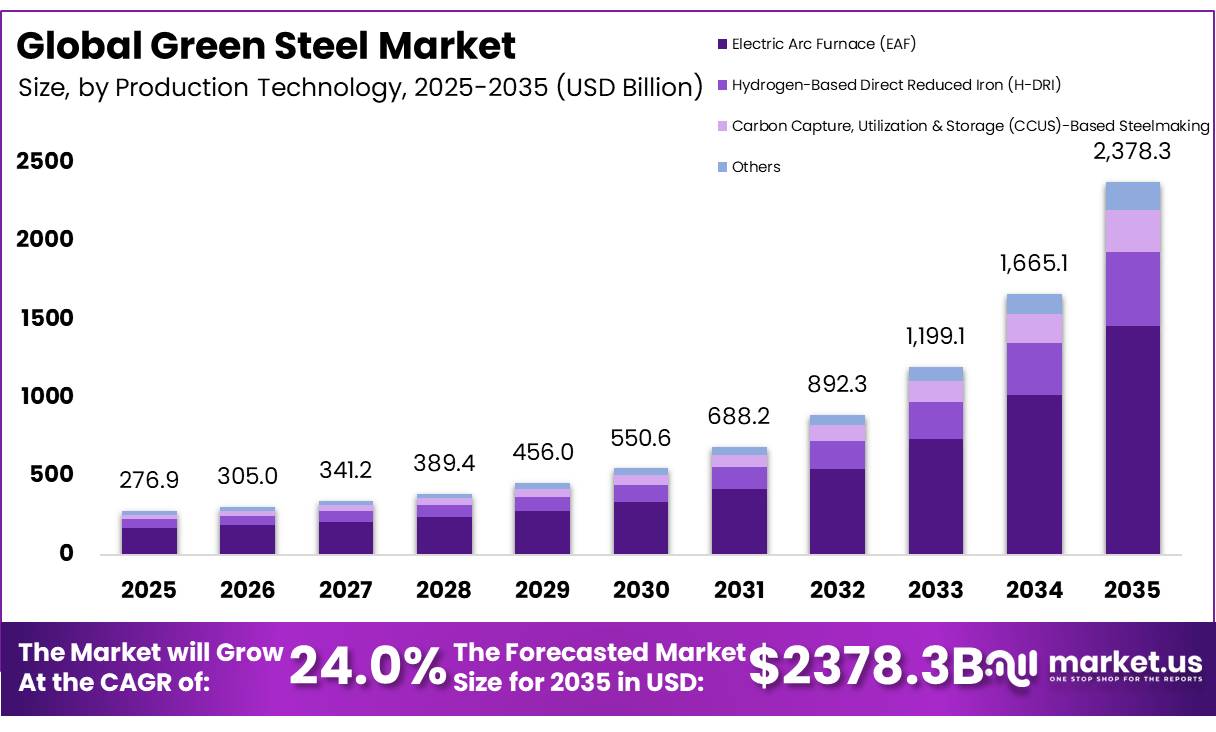

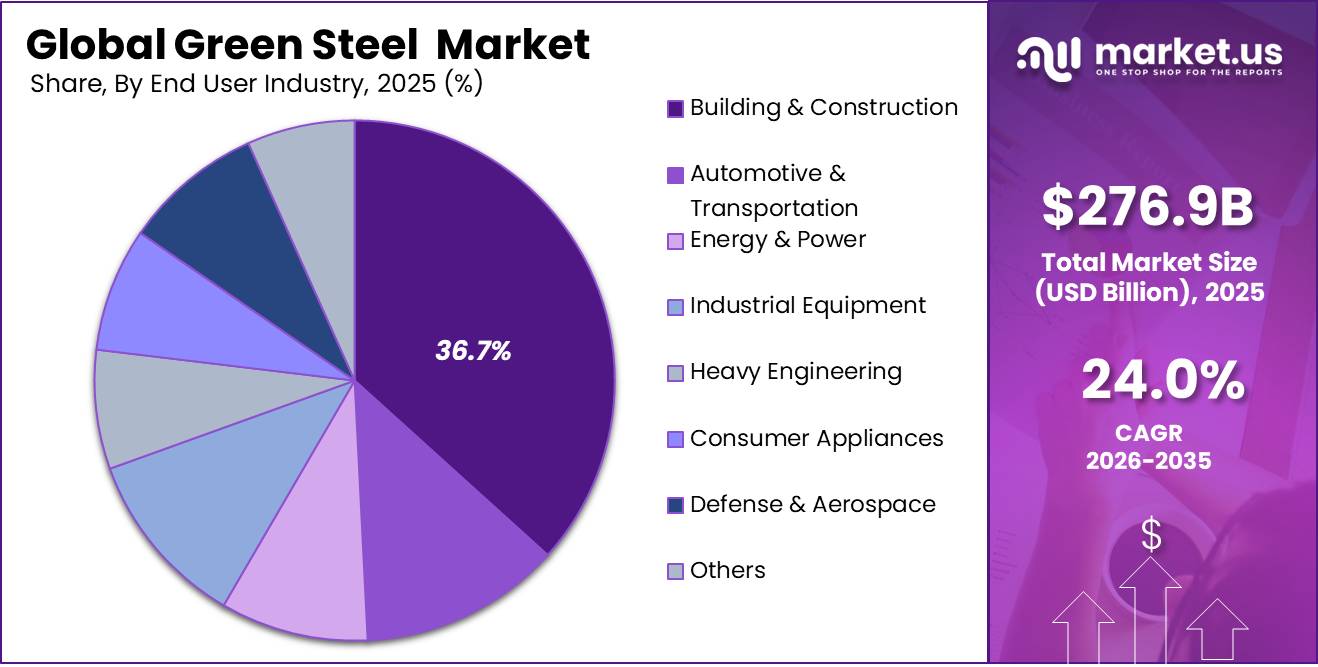

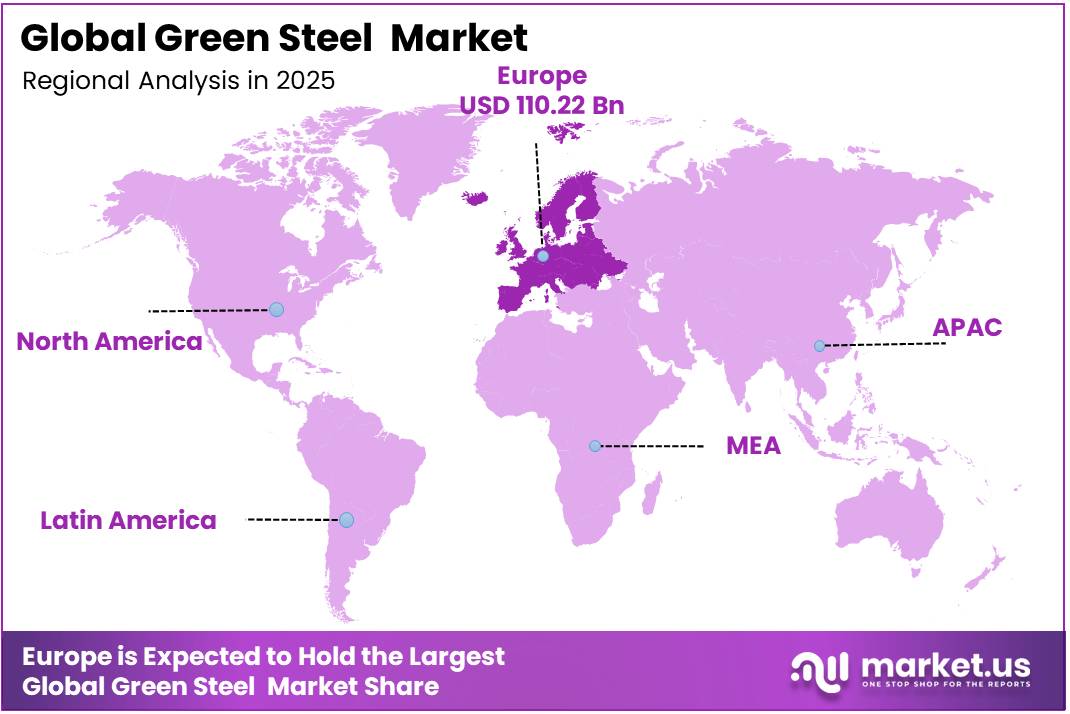

In 2025, the Global Green Steel Market was valued at USD 276.9 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 24.0%, reaching about USD 2378.3 billion by 2035. In 2025, Europe led the market, achieving over 39.8% share with a revenue of USD 110.22 Billion.

The global green steel market includes the production, commercialization, and end-use adoption of steel made using production pathways that eliminate or near-eliminate fossil carbon emissions compared to the traditional blast furnace basic oxygen furnace (BF-BOF) process, which has been the standard in the industry for over a century.

- According to the International Energy Agency (IEA, 2025), the steel industry is expected to require significant investment in low-emissions production technologies through 2050 as global steel demand continues to grow, with industry forecasts projecting crude steel production of around 2–2.4 billion tonnes annually by mid-century.

Key Takeaways

- The Global Green Steel market was valued at USD 276.9 billion in 2025.

- The market is projected to grow at a CAGR of 24.0% and is estimated to reach USD 2378.3 billion by 2035.

- By production technology, Electric Arc Furnace (EAF) accounted for a leading 61.4% share of the market in 2025.

- By product type, Flat Steel accounted for a leading 38.6% share of the market in 2025.

- On the basis of end-use industry, Building & Construction accounted for a leading 36.7% share.

- On the basis of region, Europe accounted for a leading 39.8% share of the market in 2025.

The market is supported by three main production techniques: hydrogen direct reduced iron combined with electric arc furnace processing (H₂ DRI-EAF), electric arc furnace steelmaking using scrap and powered by renewable energy, and emerging pathways including molten oxide electrolysis (MOE).

Green steel addresses this emissions liability directly by offering steel that meets the same strength and size standards as traditional steel, allowing automotive OEMs, construction contractors, and heavy machinery producers to fulfill their Scope 3 emission reduction goals that are now part of their supplier agreements and investor reports.

- In 2025, the world produced approximately 1,849 million tonnes of crude steel and consumed around 1,718.2 million tonnes of finished steel. As governments and industries work to reduce emissions from steelmaking, this vast steel demand is accelerating the shift toward green steel produced using low-carbon technologies, supporting long-term market growth.

Main factors are driving the use of green steel. First, the EU’s Carbon Border Adjustment Mechanism (CBAM) requires steel imports to have verified carbon certificates. Second, the U.S. Inflation Reduction Act aims to cut emissions from heavy manufacturing, which helps reduce the costs of using hydrogen in steelmaking.

Green Steel Market Segmentation

Production Technology Type Analysis

Electric Arc Furnace (EAF) production technology represents the dominant Segment in the Market.

Electric Arc Furnace (EAF) represents the dominant segment in the green steel market, accounting for a 61.4% share due to well-established recycling infrastructure and lower energy demands relative to primary ore processing. The economics reinforce the choice recycled steel requires up to 75% less energy than conventional blast furnace processing, allowing producers to decarbonize existing operations without committing capital to hydrogen production infrastructure that the market is not yet ready to support at scale.

- World Steel Association data show that EAFs accounted for 29.1% of global crude steel production, while the average carbon intensity of scrap-based EAF steel was approximately 0.70 tonnes of CO₂ per tonne of crude steel, compared with 2.32 tonnes for the conventional blast furnace-basic oxygen furnace route.

Hydrogen-based direct reduction iron, paired with electric arc furnace processing, is a growing segment between 2026 and 2035. This rapid growth is due to the world’s shift away from utilizing fossil fuels in metal production and the implementation of severe carbon price regulations around the world. The proliferation of large-scale water electrolyzers powered by unique renewable energy networks is the primary cause for this technology’s rapid advancement. This enables steelmakers to generate extremely pure steel without utilizing any metallurgical coal.

Product Type Analysis

Flat steel is the Most Widely Used Green Steel in the market.

Flat steel, accounting for 38.6% of the green steel market, represents the dominant product segment because steel is in high demand in the automotive and appliance industries, with hot-rolled, cold-rolled, galvanized, and coated steel being widely utilized in automobile body parts, car frames, and home appliances.

- In 2025, the World Steel Association reported that global apparent steel use is expected to reach 75 billion tonnes, with manufacturing industries remaining major consumers of flat steel products.

Long steel goods such as structural beams, rebar, and wire rods are predicted to expand the most between 2026 and 2035. This rapid expansion is being driven by new policies that promote the use of environmentally friendly materials in public projects, as well as building codes that mandate low-carbon materials for infrastructure.

End Use Industry Analysis

Green Steel Are Mostly Utilized in the Building and Construction Sector.

The building and construction sector segment, accounting for 36.7% of the green steel market, remains the dominant end-use industry category due to the increasing usage of green building standards such as LEED and BREEAM around the world, as well as severe carbon content requirements in many nations. For example, huge public projects in major economies now require a minimum amount of low-carbon materials in all major construction work.

- In 2025, the Global Status Report for Buildings and Construction (UNEP/GlobalABC) stated that the buildings and construction sector accounts for around 34% of global energy demand and 37% of energy- and process-related CO₂ emissions, highlighting the need for low-carbon construction materials such as green steel.

The Automotive & Transportation segment is the fastest-growing segment in the green steel market as vehicle manufacturers accelerate efforts to reduce emissions across their entire supply chains. Automakers are increasingly sourcing low-carbon steel to meet corporate climate goals and comply with stricter environmental regulations, particularly in Europe and North America.

Key Market Segments

Production Technology

- Electric Arc Furnace (EAF)

- Hydrogen-Based Direct Reduced Iron (H-DRI)

- Carbon Capture, Utilization & Storage (CCUS)-Based Steelmaking

- Others

Product Type

- Flat Steel

- Long Steel

- Structural Steel

- Reinforcement Steel (Rebar)

- Others

End User Industry

- Building & Construction

- Automotive & Transportation

- Energy & Power

- Industrial Equipment

- Heavy Engineering

- Consumer Appliances

- Defense & Aerospace

- Others

Drivers

Automotive OEM Scope 3 Mandates & Green Steel Offtake Agreements

Steel is responsible for 30–70% of a vehicle’s Scope 3 embedded emissions depending on model architecture, making it the single largest decarbonizable material input for automakers competing under SBTi-aligned net-zero commitments. The automotive sector accounts for approximately 40% of green steel end-use demand in 2026, making it the dominant commercial demand catalyst by application segment. Volkswagen Group, Mercedes-Benz, BMW, and Volvo Cars have each publicly committed to sourcing low-carbon or green steel as part of their Scope 3 emissions reduction strategies under the SBTi framework, with Mercedes-Benz having taken an equity stake in H2 Green Steel as early as May 2021 to secure supply-chain positioning.

The commercial math for OEMs is increasingly supportive: transitioning to green steel adds an estimated USD 100–200 to the average vehicle’s total cost of goods a sub-1% bill-of-materials increase that is absorptive within normal model pricing cycles while cutting embodied carbon in manufacturing by approximately 50%. EY Parthenon analysis calibrates the cost impact even more granularly: the green steel premium translates to only a 4.1% increase in automotive manufacturing costs and 3.7% in infrastructure costs at current premium levels, well below procurement decision thresholds for OEM sustainability programs.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU CBAM Full Enforcement & Carbon Pricing Architecture | +2.8% | EU core; spillover to Turkey, India, South Korea, Brazil (CBAM-exposed exporters) | Short Term (≤2 years) |

| Hydrogen-Based DRI Cost Trajectory & Electrolyzer Scale-Up | +3.2% | MENA, Australia, India (low-cost renewables); EU project pipeline | Medium Term (2–4 years) |

| Automotive OEM Scope 3 Mandates & Green Steel Offtake Agreements | +2.2% | EU automotive corridor; North America OEM spillover; Japan & South Korea | Short-to-Medium Term |

| EAF Expansion & Circular Economy Scrap Utilization | +1.8% | EU (dominant); North America EAF-strong markets; India nascent scrap ecosystem | Short Term (≤2 years) |

| National Green Steel Policy Frameworks & Fiscal Incentives | +2.4% | India (APAC demand leader); Germany/EU (supply-side capex catalyst); US IRA residual effect | Medium Term (2–4 years) |

| Corporate Net-Zero Commitments & ESG-Driven Demand Pull | +1.6% | Global; Construction/infrastructure-heavy APAC; EU green building taxonomy aligned | Long Term (≥4 years) |

Restraints

Prohibitive CapEx Burden & Project Financing Bottlenecks

Converting just 30% of Europe’s listed steelmakers’ crude steel production to the H₂-DRI/EAF route requires between EUR 12.1 billion and EUR 20.2 billion in total capital investment an outlay exceeding those companies’ average annual CapEx by a factor of 1.2x to 2.0x, and representing 3.3 to 5.4 times the annual CapEx of the same companies when global steel operations are included in the scope.

Project financing risk is amplified by the novelty premium embedded in first-of-kind H₂-DRI/EAF projects commercial lenders require a 200–350 basis point spread above conventional industrial lending rates to underwrite technology execution risk, hydrogen supply price risk, and offtake concentration risk in long-term green steel contracts, pushing weighted average cost of capital for project finance to 9–13% in Europe versus 6–8% for equivalent BF-BOF brownfield capex.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green Hydrogen Cost Gap & Infrastructure Deficit | -3.5% | EU, India, APAC (H₂-DRI pipeline markets); MENA partial offset | Medium Term (2–4 years) |

| Prohibitive CapEx Burden & Project Financing Bottlenecks | -2.8% | EU primary; North America secondary; India nascent project stage | Medium Term (2–4 years) |

| China Steel Overcapacity & Cheap Import Price Suppression | -2.4% | Global (non-EU); South/Southeast Asia worst exposed; India, Turkey, MENA | Short Term (≤2 years) |

| Steel Scrap Scarcity & Quality Contamination Constraints | -1.9% | India (acute); EU (emerging by 2030); APAC (structural) | Short-to-Medium Term |

| Fragmented Certification, MRV Gaps & Standards Incompatibility | -1.6% | Global trade flows; EU-India-APAC bilateral corridors specifically | Medium Term (2–4 years) |

| Renewable Energy Intermittency & Grid Infrastructure Constraints | -1.3% | India, South/Southeast APAC; EU grid constraint zones (Germany, Poland) | Short Term (≤2 years) |

Opportunity

Carbon Credit Monetization via India’s Live CCTS Market

For a mid-sized integrated steel plant producing 2 MT/year that reduces emission intensity by 0.5 tCO₂e/tfs above its CCTS target, the annual carbon credit generation is approximately 1 Mt CO₂e which at an ICM exchange price of INR 800–1,200/tCO₂e represents INR 800–1,200 crore in incremental annual revenue per plant, a cash contribution that materially shifts green steel project IRRs without any change to operational production.

The LSE Grantham Institute’s analysis of the CCTS confirms that the green steel taxonomy creates “de facto, a state-supported green premium” paid out to lower-carbon producers yet as of mid-2026, only 89 certified steel units have been awarded green steel status covering 12.34 MT of production, meaning that 164 of the 253 obligated CCTS units have not yet optimized their production to green certification thresholds, leaving a structurally unmonetized arbitrage gap between their current emission intensity and the certification threshold that can be extracted through relatively modest process upgrades and renewable energy procurement.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Green Iron Trade Architecture | +3.4% | MENA & Australia (supply); EU, Japan, South Korea (demand); India pivot market | Medium Term (2–4 years) |

| Carbon Credit Monetization via India’s CCTS | +2.6% | India primary; APAC carbon market linkage corridors | Short Term (≤2 years) |

| Green Steel Public Procurement Scale-Up | +2.9% | India (largest untapped), EU, Japan, South Korea | Short-to-Medium Term |

| Digital Scrap Intelligence & Traceability Platform Play | +1.8% | EU & India primary; APAC scrap corridor (Japan, South Korea, Turkey) | Short Term (≤2 years) |

| Green Steel M&A Roll-Up of Certified Mid-Tier Producers | +2.1% | India core; EU secondary (distressed EAF assets); North America bolt-on | Medium Term (2–4 years) |

| CCUS-Augmented Retrofit Monetization for Blast Furnace Assets | +1.7% | India (BF-heavy installed base); EU brownfield assets; China ETS-exposed producers | Medium-to-Long Term |

Challenges

First-of-Kind Plant Execution & Scale-Up Risk

DIW Berlin’s study on investment costs for green steel finds that FOAK H₂-DRI projects systematically run 20–35% above initial feasibility-stage CapEx estimates, driven by three compounding cost vectors: electrolyzer system lead times of 18–30 months that extend project development timelines and inflate interest-during-construction charges; site-specific integration complexities between renewable power procurement, hydrogen storage, and DRI shaft furnace operations that introduce USD 80–150 million in unbudgeted balance-of-plant costs; and first-cycle operational yield variability where initial product quality deviations of ±8–15% from grade specification require process re-optimization periods of 6–18 months before continuous premium-grade output is achievable.

The commercial consequence for offtake-secured projects is particularly acute: long-term green steel supply agreements signed at fixed EUR/tonne premium levels assume immediate post-commissioning delivery of certified grade-compliant product, while FOAK operational reality imposes a 12–24 month ramp-up period during which quality specifications are inconsistently met, exposing producers to contractual penalty clauses, customer certification suspension, and revenue shortfalls of USD 40–80 million per year relative to steady-state operating assumptions a structural FOAK risk premium that rational lenders must price into project finance cost of capital, further widening the financing gap documented in the Restraints module.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| DR-Grade Iron Ore Supply Deficit | -2.3% | Global H₂-DRI markets; EU, MENA, India DRI-heavy producers | Long Term (≥4 years) |

| Green Hydrogen & Metallurgy Talent Shortage | -1.7% | EU, India, Australia (high-ambition deployment markets); MENA greenfield hubs | Medium Term (2–4 years) |

| First-of-Kind Plant Execution & Scale-Up Risk | -2.0% | EU (H₂-DRI pipeline); North America (FOAK investments); India (capacity ramp) | Medium Term (2–4 years) |

| Policy Inconsistency & ESG Investment Retreat | -2.2% | North America (IRA reversal); EU (subsidy policy volatility); Global FID pipeline | Short Term (≤2 years) |

| Stranded BF-BOF Asset Transition & Capital Lock-In | -1.5% | Global (BF-BOF-heavy); EU transition corridor; India BF-BOF-dominant majors | Long Term (≥4 years) |

| Green Premium Price Volatility & Contract Stability Risk | -1.4% | EU (premium market); Global bilateral offtake contracts; APAC OEM supply chains | Medium Term (2–4 years) |

Geopolitical Impact Analysis

Geopolitical Conflicts Disrupt Supply Chains and Raw Materials.

The ongoing military conflicts in Ukraine and the Middle East have greatly affected how quickly the global green steel market is developing. These wars have limited traditional supply chains and created major obstacles in the clean energy systems needed for green steel production. The conflict in major industrial regions such as Dnipropetrovsk and Zaporizhzhia has disrupted the supply of high-quality raw materials, including pig iron and other metals needed for steel production.

At the same time, political tensions and trade limits in different regions have made energy prices more unstable. High electricity and gas costs across Europe have made it harder for industries that use a lot of energy to stay economically viable. Since the green steel market relies a lot on hydrogen direct reduced iron (H₂ DRI-EAF) systems, the high cost of electricity is slowing down the development of large-scale electrolyzer plants. This has led some companies to put off their final investment plans or move their clean technology projects to areas where the power supply is more reliable.

Regional Analysis

Europe Held the Largest Share of the Global Green Steel Market.

In 2025, Europe dominated the global green steel market, holding about 39.8% of the total global consumption. Europe’s pricing policies make traditional steel production methods, like those using blast furnaces, too expensive to continue. Europe is investing heavily in new technologies, which helps big industries adopt hydrogen-based direct reduced iron (H₂ DRI-EAF) systems.

The rest of the world is divided into North America, Asia Pacific, Latin America, and the Middle East & Africa. North America is a key area, mainly because of the U.S. Inflation Reduction Act, which gives strong financial support for using clean hydrogen. On the other hand, the Asia Pacific region, especially countries like China and India, has the biggest chance for long-term growth because of fast urban development.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global green steel market is a highly consolidated, oligopolistic structure within localized regions, transitioning from the historically fragmented nature of the conventional global steel industry. Even though there are still thousands of traditional steel plants around the world, the high costs and advanced technology needed to produce steel with nearly zero emissions have led to most of the green steel production being controlled by a small number of well-funded existing companies and new, specialized firms focused on this type of steel.

The green steel market structure for low-carbon steel is divided between adapting industrial heavyweights and specialized, ground-up greenfield producers. Tier 1 companies like ArcelorMittal, Nucor, Nippon Steel, and POSCO dominate early volume by retrofitting blast furnaces, scaling renewable-powered Electric Arc Furnaces, and developing hydrogen technologies.

The Major Players In The Industry

-

- ArcelorMittal

- Nucor Corporation

- Nippon Steel Corporation

- POSCO

- JFE Steel Corporation

- JSW Steel

- H2 Green Steel

- Liberty Steel Group

- HBIS Group

- Boston Metal

- Emirates Steel Arkan

- Tenaris

- Tata Steel

- Salzgitter AG

- Thyssenkrupp Steel

- Other Key Players

Key Development

- In April 2026, H2 Green Steel (Stegra) enhanced its ability to produce large amounts of green hydrogen-based direct reduced iron (H₂ DRI-EAF). The company improved its delivery plans to help create nearly zero-emission supply chains for the automotive industry, working with European car manufacturers.

- In March 2026, ArcelorMittal increased its efforts to make steel with lower carbon emissions by speeding up investments in clean power grids, carbon capture systems, and hydrogen technology. These steps are meant to gradually cut down emissions from its main steel production facilities.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 276.9 Bn |

| Forecast Revenue (2035) | USD 2378.3 Bn |

| CAGR (2026-2035) | 24.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Production Technology (Electric Arc Furnace (EAF), Hydrogen-Based Direct Reduced Iron (H-DRI), Carbon Capture, Utilization & Storage (CCUS)-Based Steelmaking, Others), By Product Type (Flat Steel, Long Steel, Structural Steel, Reinforcement Steel (Rebar), Others), By End User Industry (Building & Construction, Automotive & Transportation, Energy & Power, Industrial Equipment, Heavy Engineering, Consumer Appliances, Defense & Aerospace, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | ArcelorMittal, Nucor Corporation, Nippon Steel Corporation, POSCO, JFE Steel Corporation, JSW Steel, H2 Green Steel, Liberty Steel Group, HBIS Group, Boston Metal, Emirates Steel Arkan, Tenaris, Tata Steel, Salzgitter AG, Thyssenkrupp Steel, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |