Global Grain Protectants Market Size, Share, And Industry Analysis Report By Product Type (Chemical Insecticides, Biological Protectants, Integrated Pest Management Solutions), By Grain Type (Wheat, Corn (Maize), Rice, Barley, Others), By Application Method (Fumigation, Spraying, Dusting, Grain Coating), By End User (Farmers and On-farm Storage, Commercial Grain Storage Facilities, Food Processing Companies, Government Reserve Agencies), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180896

- Number of Pages: 211

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

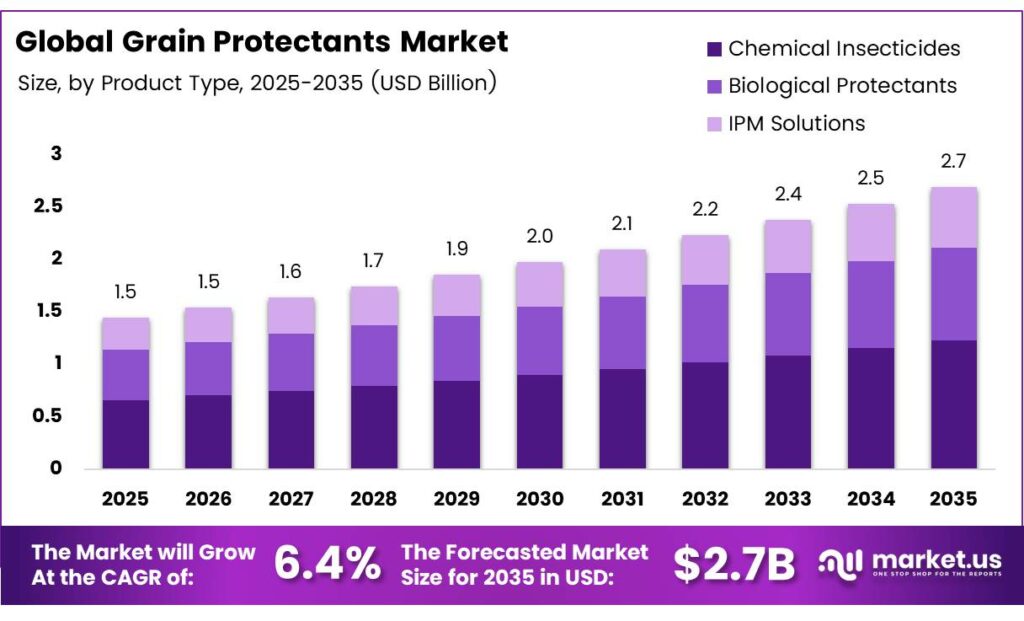

The Global Grain Protectants Market size is expected to be worth around USD 2.7 billion by 2035 from USD 1.5 billion in 2025, growing at a CAGR of 6.4% during the forecast period 2026 to 2035.

The grain protectants market covers chemical, biological, and integrated solutions that protect stored grains from insects, fungi, and pests. Farmers, commercial storage operators, and food processors rely on these products to reduce post-harvest losses. Consequently, demand continues to grow as global food supply chains face increasing pressure.

Post-harvest grain losses remain a critical concern for food security worldwide. Storage pests destroy significant volumes of wheat, corn, rice, and barley each year. Therefore, grain protectants play a central role in preserving grain quality and maintaining safe nutritional standards across supply chains.

- China exported $2,278,740.76K and 562,492,000 kg of HS 380810 insecticides in 2024, reflecting China’s dominant role as a global supplier of grain protection chemicals. This volume confirms that formulated insecticide production scales with rising global storage demand.

- The European Union exported $1,392,536.44K and 68,137,300 kg of HS 380810 insecticides in 2024, making it one of the largest regional trade blocs in this product flow. This highlights Europe’s strong manufacturing base for grain protectant formulations serving international markets. UPL EBITDA of ₹81.2 billion, up 47% from ₹55.2 billion in FY2024, reflecting strong revenue growth in crop protection markets that benefit from these compliance-driven purchasing trends.

Rapid expansion of large-scale centralised grain storage infrastructure across Asia, Africa, and Latin America accelerates market growth. Governments in developing nations invest heavily in national grain reserves to buffer food supply shocks. Additionally, private agribusiness operators expand cold storage and silo networks, creating strong demand for fumigation and chemical protectant systems.

Key Takeaways

- The Global Grain Protectants Market is valued at USD 1.5 billion in 2025 and is projected to reach USD 2.7 billion by 2035 at a CAGR of 6.4% during the forecast period 2026 to 2035.

- Chemical Insecticides dominate with a 59.2% market share in 2025.

- Wheat leads the segment with a 35.8% share.

- Fumigation holds the largest share at 44.7%.

- Farmers and On-farm Storage represent the dominant segment at 48.6%.

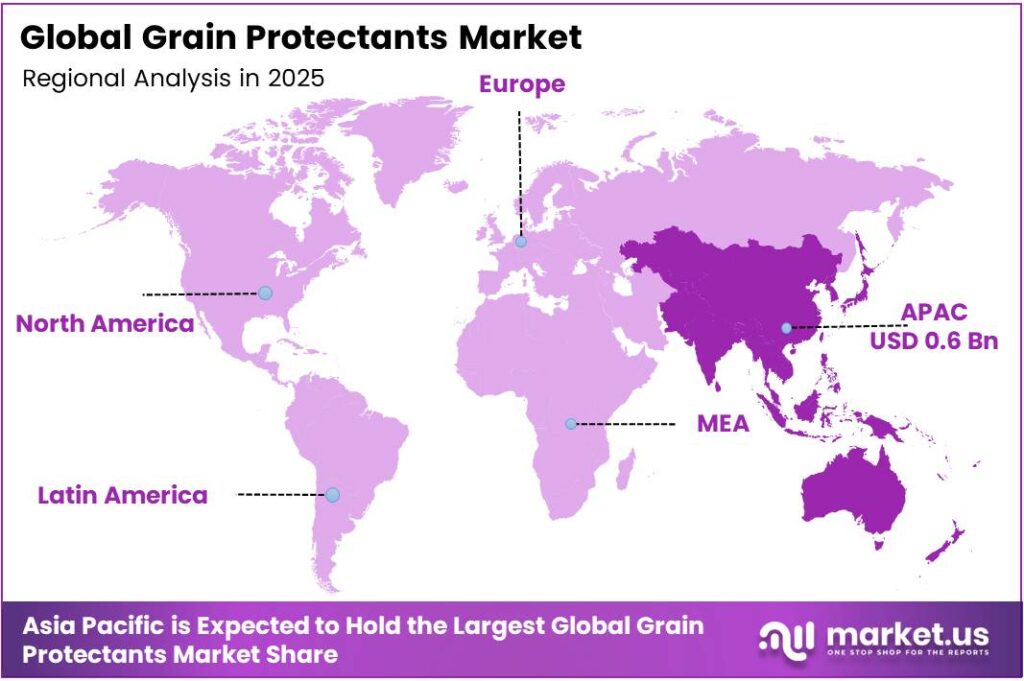

- Asia Pacific dominates the regional landscape with a 38.3% market share, valued at USD 0.6 billion.

By Product Type Analysis

Chemical Insecticides dominate with 59.2% due to proven efficacy and widespread availability.

In 2025, Chemical Insecticides held a dominant market position in the By Product Type segment of the Grain Protectants Market, with a 59.2% share. Farmers and storage operators prefer chemical insecticides because of their fast action, long shelf life, and cost-effectiveness. Moreover, well-established supply chains make these products readily accessible across all major grain-producing regions.

Biological Protectants represent a rapidly growing segment as consumer demand shifts toward safer, residue-free grain products. These solutions include microbial agents, plant-based extracts, and natural compounds. Additionally, regulatory pressure to reduce synthetic chemical residues encourages larger farms and certified grain producers to adopt biological alternatives.

Integrated Pest Management Solutions combine chemical, biological, and physical control methods into a unified grain protection strategy. IPM adoption grows steadily among commercial storage operators seeking to minimise resistance development in pest populations. Consequently, these solutions offer a balanced approach that extends product effectiveness while meeting stricter food safety compliance requirements.

By Grain Type Analysis

Wheat dominates with 35.8% due to high global production volumes and extended storage cycles.

In 2025, Wheat held a dominant market position in the By Grain Type segment of the Grain Protectants Market, with a 35.8% share. Wheat requires extended storage periods of up to 12 months, creating continuous demand for effective grain protection. Moreover, wheat’s global importance as a staple food makes storage loss prevention a top priority for governments and commercial operators alike.

Corn (Maize) represents the second largest grain segment due to its high susceptibility to aflatoxin-producing fungi during storage. Corn producers rely heavily on fumigation and chemical protectant treatments. Additionally, expanding ethanol production and animal feed industries increase the volume of corn held in long-term commercial storage facilities.

Rice storage demands specialised protectant solutions due to the grain’s sensitivity to moisture and weevil infestation. Asian markets drive the majority of rice protective consumption. Barley and Others including sorghum and oats, complete the segment, with growing demand tied to expanding craft beverage industries and diversified food processing applications worldwide.

By Application Method Analysis

Fumigation dominates with 44.7% due to its deep penetration and effectiveness in sealed storage systems.

In 2025, Fumigation held a dominant market position in the By Application Method segment of the Grain Protectants Market, with a 44.7% share. Fumigation using phosphine or methyl bromide delivers comprehensive pest control across bulk grain storage. Consequently, large commercial silos and government reserve facilities rely on fumigation as their primary grain protection method.

Spraying remains a widely adopted method for surface treatment of grain storage structures and grain surfaces before loading. Farmers and cooperative storage operators use spraying equipment for routine maintenance treatments. Moreover, spraying methods integrate easily into existing farm infrastructure without requiring major capital investment in specialised application equipment.

Dusting and Grain Coating complete the application segment, each serving specific needs. Dusting applies dry formulations directly to grain during handling and transfer. Grain Coating involves applying protective layers during processing or before bagging. Additionally, grain coating gains traction as a precision method that minimises chemical use while maintaining effective pest and fungal control.

By End User Analysis

Farmers and On-farm Storage dominate with 48.6% due to large volumes of grain handled at the farm level.

In 2025, Farmers and On-farm Storage held a dominant market position in the By End User segment of the Grain Protectants Market, with a 48.6% share. Smallholder and large-scale farmers store significant grain volumes on-site before sale or processing. Therefore, farm-level grain protection represents the single largest demand channel for chemical and biological protectant products globally.

Commercial Grain Storage Facilities form the second largest end-user segment, driven by the expansion of private silos and cooperative storage networks. These facilities operate under strict food safety compliance requirements. Additionally, commercial operators invest in advanced fumigation systems and monitoring technology to meet regulatory standards and protect large grain inventories.

Food Processing Companies use grain protectants to maintain raw material quality within their supply chains. These companies require low-residue formulations that comply with end-product safety regulations. Government Reserve Agencies represent a strategically important segment, purchasing protective solutions at scale to maintain national food security buffer stocks across multiple countries.

Key Market Segments

By Product Type

- Chemical Insecticides

- Biological Protectants

- Integrated Pest Management Solutions

By Grain Type

- Wheat

- Corn (Maize)

- Rice

- Barley

- Others

By Application Method

- Fumigation

- Spraying

- Dusting

- Grain Coating

By End User

- Farmers and On-farm Storage

- Commercial Grain Storage Facilities

- Food Processing Companies

- Government Reserve Agencies

Emerging Trends

Modified Atmosphere, Blockchain Traceability, and Organic Demand Reshape Grain Protection

Modified atmosphere storage gains traction as a complementary solution alongside chemical protectants. Operators use controlled oxygen and carbon dioxide levels to suppress pest populations without chemical residues. The European Union exported $294,265.12K of HS 380810 insecticides to Brazil in 2024, reflecting cross-regional supply chains serving grain-producing markets that adopt multi-method storage approaches.

Rising consumer demand for organically certified grains drives natural protectant adoption across multiple markets. Food retailers and processors increasingly source certified organic grain supplies to meet growing health-conscious consumer preferences. Moreover, this shift encourages grain storage operators to invest in botanical and bio-based formulations that preserve organic certification status throughout the supply chain.

Blockchain technology enters grain storage management as a traceability tool for protectant residue levels. Food companies and regulators use blockchain records to verify compliant chemical application throughout storage and transport. Additionally, consolidation through mergers between chemical manufacturers and application service providers streamlines supply chains and improves traceability infrastructure at scale.

Drivers

Escalating Food Demand, Stricter Regulations, and Infrastructure Expansion Drive Market Growth

Escalating global food demand intensifies pressure on post-harvest storage systems worldwide. Rapid population growth in Asia, Africa, and Latin America increases the volume of grain that must move through storage infrastructure. Therefore, grain protectants become essential tools for reducing storage losses and ensuring that harvested grain reaches consumers in safe, high-quality condition.

- Stricter government mandates on aflatoxin and mycotoxin contamination standards push storage operators to adopt more effective protectant solutions. Regulatory agencies in major grain-importing regions set enforceable maximum residue limits that non-compliant exporters cannot bypass. The United States exported $1,761,815.15K and 60,698,500 kg of HS 380810 insecticides in 2024, signalling sustained commercial demand driven by compliance-based purchasing in major agricultural economies.

Rapid expansion of large-scale centralised grain storage infrastructure creates consistent demand for professional-grade protectant systems. Governments and private investors build new silos and cold storage networks across South and Southeast Asia, Sub-Saharan Africa, and South America. Additionally, increasing adoption of Integrated Pest Management strategies by organised farmers drives demand for diversified protectant product portfolios that combine chemical and biological solutions.

Restraints

High Capital Costs and Pest Resistance Development Limit Market Adoption and Efficacy

High capital expenditure associated with advanced fumigation and application systems creates a significant barrier for smallholder farmers and small cooperative storage facilities. Professional fumigation equipment, gas monitoring systems, and sealed storage infrastructure require upfront investments that many farm-level operators cannot afford. Consequently, a large segment of the global farming population continues to rely on less effective or informal grain protection methods.

- Development of physiological resistance in target pest populations to conventional chemical insecticides represents a growing threat to market efficacy. Stored grain beetles, weevils, and moths exposed repeatedly to the same active ingredients develop resistance over multiple generations. Moreover, Bayer Crop Science reported sales of €22,259 million in 2024, reflecting the scale of investment major agribusiness firms direct toward crop and grain protection innovation.

Regulatory restrictions on certain chemically active ingredients further constrain product availability in key markets. The phaseout of methyl bromide and increasing scrutiny of organophosphate compounds limit the chemical toolkit available to grain storage operators. Additionally, the time and cost required to register new protectant formulations across multiple national regulatory frameworks slow the pace at which innovative solutions reach end users.

Growth Factors

Bio-Based Formulations, Smart Technology, and Untapped Markets Accelerate Expansion

Commercialisation of novel botanical and bio-based grain protectant formulations opens new revenue streams for agrochemical companies. Essential oil-based solutions, diatomaceous earth, and microbial insecticides gain acceptance as effective alternatives to synthetic chemicals. Therefore, product developers increase R&D investment in bio-based formulations that meet both efficacy standards and organic certification requirements demanded by food supply chains.

- Integration of smart sensor technology with precision protectant application equipment transforms storage management practices. IoT-enabled sensors monitor grain temperature, humidity, and pest activity in real time, triggering targeted protectant deployment only when necessary. India exported $1,555,610.10K and 173,009,000 kg of HS 380810 insecticides in 2024, demonstrating that large agrarian economies actively scale their protectant supply capacity to meet both domestic and export market growth.

Untapped market potential in developing nations with rudimentary storage facilities represents a significant long-term growth opportunity. Countries across Sub-Saharan Africa and South Asia lose between 20% and 40% of harvested grain to storage pests annually. Additionally, strategic partnerships between protectant manufacturers and grain cooperatives create direct-to-farmer distribution channels that extend market reach into previously underserved rural communities.

Regional Analysis

Asia Pacific Dominates the Grain Protectants Market with a Market Share of 38.3%, Valued at USD 0.6 Billion

Asia Pacific leads the global grain protectants market with a 38.3% share, valued at USD 0.6 billion in 2025. The region’s dominance reflects massive grain production volumes across China, India, and Southeast Asia. Moreover, the rapid expansion of organised grain storage infrastructure and government food security programs drives sustained demand for fumigation and chemical protectant solutions throughout the region.

North America represents a mature and technology-advanced grain protectants market. Large-scale commercial grain storage operators adopt precision application systems and integrated pest management programs. Additionally, BASF Agricultural Solutions reported North America, underscoring the significant agrochemical investment activity that sustains grain protection product development and distribution across the US and Canadian markets.

Latin America shows strong and accelerating demand for grain protectant solutions, driven by Brazil and Argentina’s position as leading global grain exporters. Brazil imports significant volumes of formulated insecticide products to protect its soy, corn, and wheat harvests. Moreover, increasing adoption of modern storage infrastructure by large agribusiness operators in the region creates growing demand for professional-grade grain protection systems.

The Middle East and Africa region presents high growth potential for grain protectant suppliers. Many countries in Sub-Saharan Africa suffer major post-harvest grain losses due to inadequate storage systems and limited access to effective protectant products. Additionally, government and international aid programs invest in improving grain storage infrastructure, creating new entry points for protectant suppliers targeting smallholder farmer distribution networks.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bayer AG operates as one of the world’s leading crop science companies with a broad grain protection portfolio spanning insecticides, fungicides, and integrated pest management tools. The company invests significantly in R&D to develop next-generation stored grain solutions. Moreover, Bayer’s global distribution network enables it to serve grain storage operators across developed and emerging agricultural markets effectively.

Syngenta Group maintains a comprehensive crop protection product range that includes solutions specifically designed for post-harvest grain storage applications. The company focuses on developing formulations that meet stringent international food safety residue standards. Additionally, Syngenta partners with grain cooperatives and commercial storage operators to deliver technical support alongside its product portfolio in key grain-producing regions.

BASF SE brings strong chemistry expertise and a broad agricultural solutions portfolio to the grain protectants market. The company develops both conventional chemical insecticides and newer bio-based formulations for stored grain applications. Furthermore, BASF’s established regulatory capabilities allow it to navigate complex multi-market registration requirements efficiently, supporting broad international distribution of its grain protection products.

Corteva Agriscience focuses on science-driven crop protection solutions that combine efficacy with sustainable formulation practices. The company targets both large-scale commercial storage operators and organised farmer cooperatives with tailored grain protectant programs. Consequently, Corteva’s investment in digital agronomy platforms supports precision grain protection recommendations that improve product effectiveness and help end users optimise application timing and dosage.

Top Key Players in the Market

- Bayer AG

- Syngenta Group

- BASF SE

- Corteva Agriscience

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- Nufarm

- UPL Limited

- Central Life Sciences

- Detia Degesch Group

Recent Developments

- In February 2026, Bayer announced it was developing the first new post-emergent mode of action for broadleaf weed control in three decades. This small molecule discovery is still in early development and is expected to reach the market toward the end of the decade. It is showing effectiveness at controlling grasses, including those resistant to glyphosate.

- In 2025, Syngenta signed a Memorandum of Understanding with French greentech company Amoéba to develop and commercialise a groundbreaking biofungicide derived from the lysate of the Willaertia magna C2c Maky amoeba. This novel product, which received EU approval for its active substance.

Report Scope

Report Features Description Market Value (2025) USD 1.5 Billion Forecast Revenue (2035) USD 2.7 Billion CAGR (2026-2035) 6.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Chemical Insecticides, Biological Protectants, Integrated Pest Management Solutions), By Grain Type (Wheat, Corn (Maize), Rice, Barley, Others), By Application Method (Fumigation, Spraying, Dusting, Grain Coating), By End User (Farmers and On-farm Storage, Commercial Grain Storage Facilities, Food Processing Companies, Government Reserve Agencies) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Bayer AG, Syngenta Group, BASF SE, Corteva Agriscience, FMC Corporation, Sumitomo Chemical Co., Ltd., Nufarm, UPL Limited, Central Life Sciences, Detia Degesch Group Customization Scope Customisation for segments, region/country-level will be provided. Moreover, additional customisation can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Bayer AG

- Syngenta Group

- BASF SE

- Corteva Agriscience

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- Nufarm

- UPL Limited

- Central Life Sciences

- Detia Degesch Group

Our Clients

- 180896

- March 2026