Quick Navigation

Report Overview

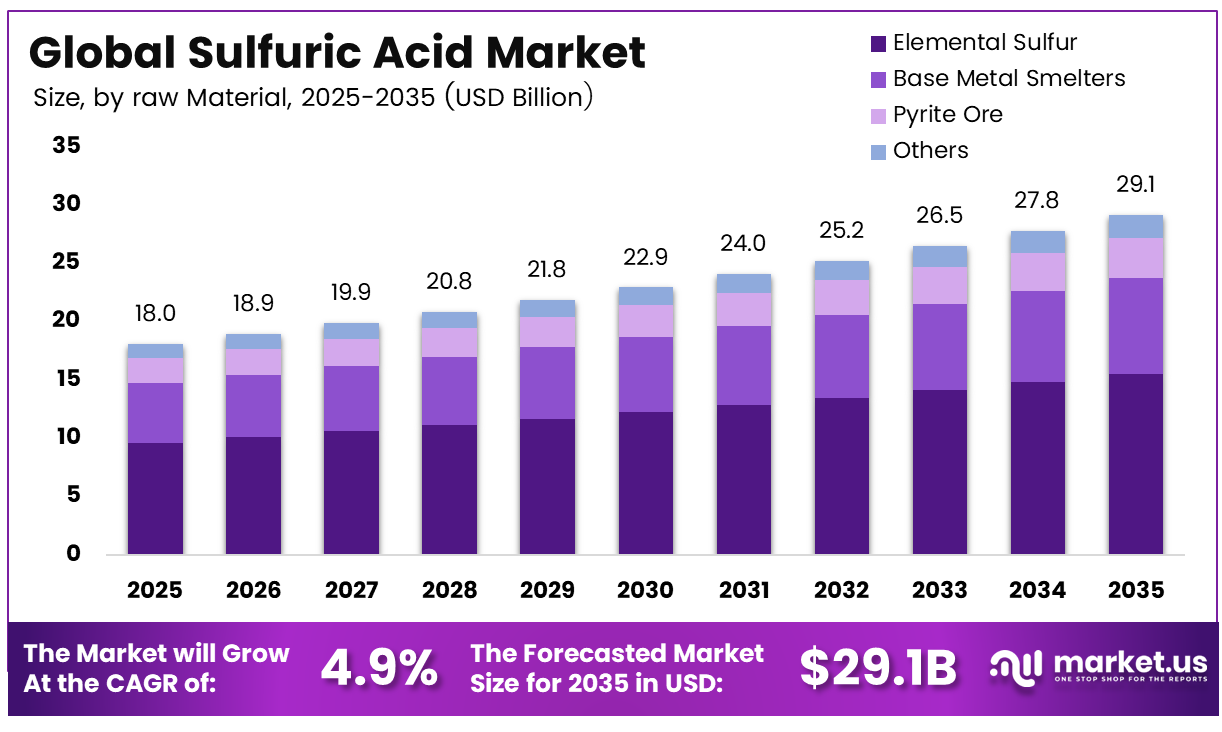

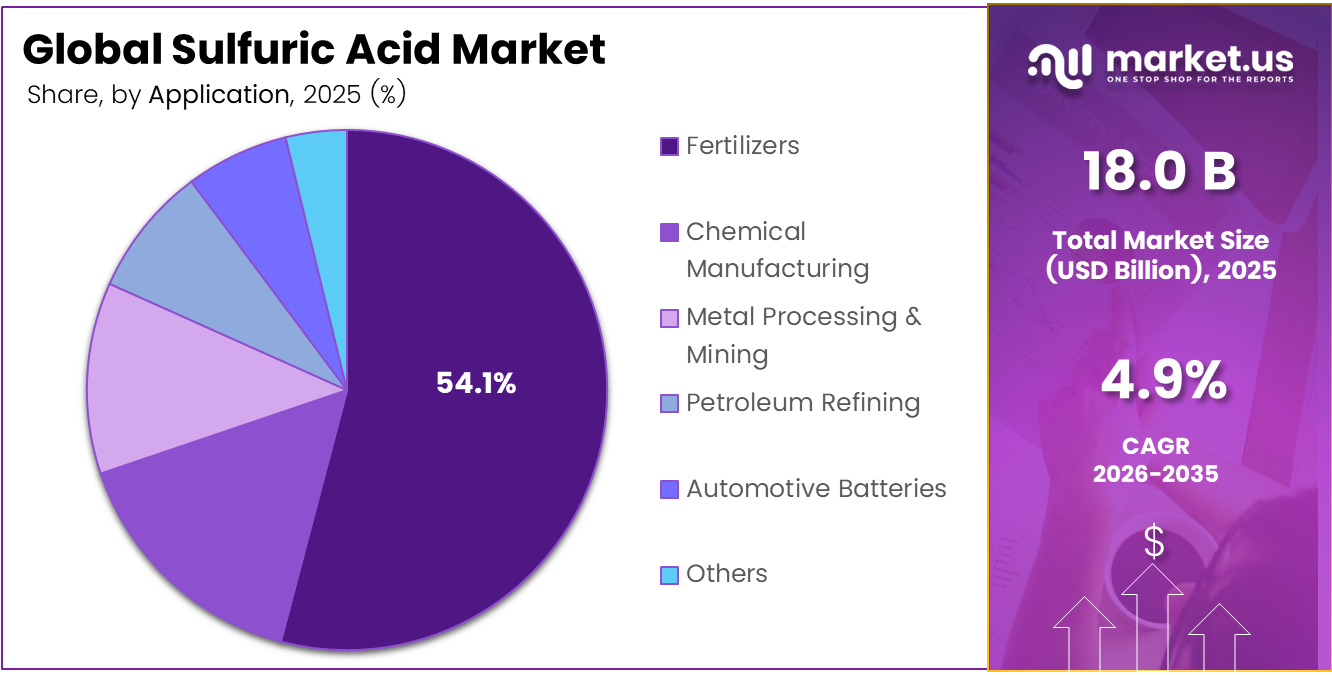

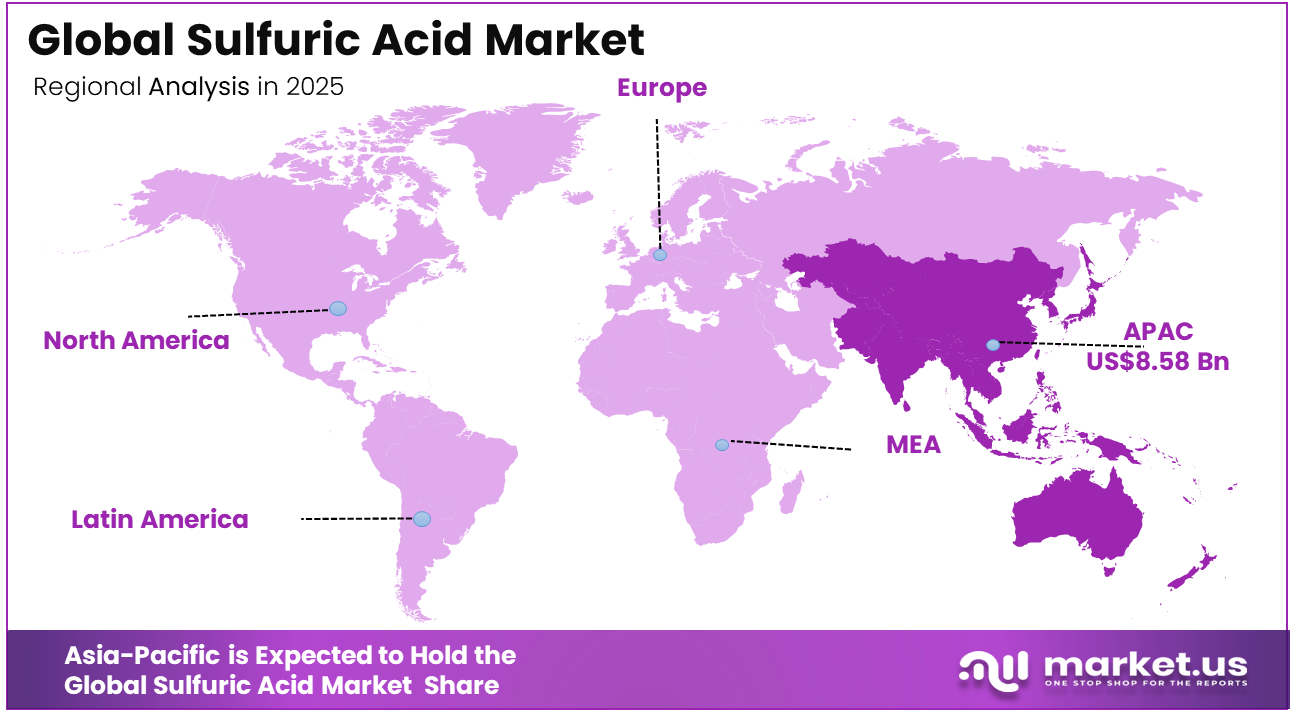

The Global Sulfuric Acid Market was valued at USD 18.0 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 4.9%, reaching about USD 29.1 billion by 2035. Asia Pacific led the market, achieving over 47.6% share with a revenue of USD 8.57 billion.

According to statistics provided by the Food and Agriculture Organization (FAO), as well as global industry monitors, downstream processes in fertilizer production account for about 50% to 54% of sulfuric acid usage across the globe. Geographically, production and commercial operations are predominantly centered in the Asia-Pacific region, with the dominating presence of 45% to 50% global share mainly owing to the development of extensive industrial and intensive farming infrastructure in countries like China and India.

The global sulfuric acid market serves as a fundamental cornerstone of the global chemical industry, where the chemical acts as an important intermediary chemical for downstream uses, including fertilizers in agriculture, metal extraction, chemicals, and refining industries. The global trends of sulfuric acid consumption remain significantly linked to the infrastructure needed for food production, as well as in developing countries that have been using the chemical in its industrial grade.

Growth in global industrialization and metallurgy led to notable increases in the baselines for metal consumption. Non-ferrous smelting processes and mining with ore leaching (copper, nickel mining in particular) account for almost 12% of the global application of the chemical. On the technology side, there is an increasing shift towards stringent emission reduction processes, ultra-low sulfur capture methods, and acid recycling processes. In the auto industry, there has been an accelerated adoption of electric mobility, thereby leading to increased demand for electrolyte fluids used in batteries.

Key Takeaways

- The global sulfuric acid market was valued at US$ 18.0 billion in 2025.

- The global sulfuric acid market is projected to grow at a CAGR of 4.9% and is estimated to reach US$ 29.1 billion by 2035.

- On the basis of raw material, elemental sulfur dominated the market, constituting 53.3% of the total market share.

- Based on the grade, the industrial grade dominated the sulfuric acid market, with a substantial market share of around 61.2%.

- Based on the application, fertilizers led the market, comprising 54.1% of the total market.

- Among the distribution channels, direct sales held a major share in the sulfuric acid market, accounting for 46.4% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the sulfuric acid market, accounting for 47.6% of the total global consumption.

Raw Material Analysis

Elemental Sulfur Represents Dominant Segment in the Market

The elemental sulfur is the topmost raw materials category in the global sulfuric acid market with an 53.3% market share, attributed to wide availability, low cost, and a more environmentally friendly processing nature in comparison with conventional products. Elemental sulfur occurs naturally as a by-product in large quantities in oil and natural gas refinement plants.

Since this raw material is sourced directly from oil and natural gas refining processes, it provides a continuous production and high-volume source of feedstock for the intensive production of high-grade phosphoric acid used in fertilizer production. The base metal smelters constitute the fastest-growing raw materials category, emerging as an important future trend in the global sulfuric acid production process.

Sulfur dioxide gas is obtained in large quantities as a by-product in the extraction process of metallic ores such as copper, zinc, and nickel. Environmental laws and carbon-capturing mandates have compelled the metallurgical industries to establish secondary acid recovery processes where hazardous tail gases will be transformed to usable sources of raw material for non-ferrous metal leaching processes.

Grade Analysis

Industrial Grade Represents the Dominant Product Segment in the Global Sulfuric Acid Market

The industrial grade is the foremost type of product available in the international market of sulfuric acid, making up an impressive market share of 61.2%. This is attributed to its extensive applications in heavy industries. This product grade possesses the lowest concentration level of 93% to 98%, making it the main chemical precursor for creating bulk chemicals, crude oil processing, and extracting metals from ores.

The rising consumption of industrial-grade sulfuric acid stems from its use in the global fertilizer sector to produce phosphoric acid used in growing crops. The growth in production facilities and ore extraction in emerging economies will sustain the dominance of industrial-grade sulfuric acid in the overall chemical market environment.

The segment of battery acid is considered to be the fastest-growing one, owing to a 10.1% share of the market. In contrast to regular industrial grades, this emerging grade has to go through tough purification in order to eliminate all possible metallic particles that might negatively affect the performance of cells or even cause short circuits.

Application Analysis

Fertilizers Are the Dominant Application Segment in the Global Sulfuric Acid Market

The application segment that holds the largest share in the global sulfuric acid market is that of fertilizers. The reason for this is that fertilizer manufacturing is an indispensable part of global agriculture and is necessary for ensuring adequate global food production pipelines, giving the segment a staggering 54.1% share of the market.

It is a requirement in producing fertilizers such as Diammonium Phosphate and Monoammonium Phosphate since phosphate rocks have to be transformed using sulfuric acid to produce phosphoric acid. The increasing need for global food production, coupled with decreasing available arable land, ensures continued optimization in fertilizer production.

Automotive Batteries is the fastest-growing market segment, accounting for 6.4% of the market share. The market suggests segment is experiencing a high and fast growth rate of 6.8% – 7.5%. Although used conventionally as a base electrolyte for lead-acid automobile batteries, the swift adoption of electric vehicle systems has created new demands within the industry. Increased manufacturing of localized battery plants and energy storage systems has necessitated large amounts of high-quality acid production.

Distribution Channel Analysis

Direct Sales Held a Major Share of the Sulfuric Acid Market

The Direct Sales category occupies the lead position in the world market of sulfuric acid by virtue of its overwhelmingly dominating 46.4% share in total market value. The popularity of this category is justified due to the sheer volume of transactions made between principal chemical producers and billion-dollar industrial complexes downstream.

Huge producers of fertilizers, synthetic chemicals, and metals benefit more from dealing with product creators directly to ensure quality control, avoid extra margins on sales via retailers, and facilitate special transportation systems for dangerous materials. Taking into consideration that the market is strongly dependent on large-scale operations, direct sales become an indispensable category.

The Contract Supply is another form of distribution that is gaining rapid momentum and is one of the most promising, taking up a significant 31.2% market share. Due to the fast capacity expansion in global battery mega factories, coupled with fluctuating prices of raw materials like elemental sulfur, industrial buyers are moving towards stable purchasing practices.

Key Market Segments

By Raw Material

- Elemental Sulfur

- Base Metal Smelters

- Pyrite Ore

- Others

By Grade

- Industrial Grade

- Technical Grade

- Battery Acid

- Oleum / Fuming Sulfuric Acid

- Reagent Grade

By Application

- Fertilizers

- Chemical Manufacturing

- Metal Processing & Mining

- Petroleum Refining

- Automotive Batteries

- Others

By Distribution Channel

- Direct sales

- Contract Supply

- Industrial Distributors

- Spot Sales

Market Dynamics

Opportunity

Battery-linked sulfuric acid demand should be treated as a market opportunity rather than a baseline growth driver because consumption is still concentrated in selected refining technologies and geographic regions. USGS has identified increasing sulfur requirements from nickel high-pressure acid leach projects used for battery material production.

This creates new demand for sulfuric acid across nickel sulfate and precursor-processing chains. Suppliers can capture this opportunity through 5- to 10-year offtake agreements that combine acid delivery with storage, onsite dilution, inventory support, and supply-reliability commitments. Indonesia, Australia, and Canada offer strong potential because a large HPAL facility may require several hundred thousand to more than 1 million tons of acid each year. Such contracts could improve margin stability by approximately 300–600 basis points compared with merchant sales while reducing exposure to seasonal fertilizer demand.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Battery materials acid offtake | +1.6% | Indonesia, Australia, China, Canada | Medium term |

| Copper leach intensity expansion | +1.4% | Chile, Peru, the US Southwest, and Central Asia | Medium term |

| Regeneration and circular acid | +1.0% | North America core, EU, Japan | Medium term |

| Merchant storage monetization | +0.9% | Coastal India, the Middle East, and EU ports | Short term |

| Battery recycling reagent supply | +0.8% | EU, China, North America | Medium term |

| Heat recovery power monetization | +0.7% | EU, North America, GCC industrial parks | Long term |

Restraint

A major market restraint is the inability of sulfuric acid producers to immediately transfer higher sulfur feedstock costs to customers. This problem is particularly severe in fertilizer and industrial contracts that are revised quarterly or semi-annually instead of tracking raw-material prices in real time.

USGS data show that the average U.S. elemental sulfur price increased from US$ 46 per metric ton in 2024 to US$ 180 per metric ton in 2025. Tampa contract prices also reached US$ 310 per long ton during the year. This sharp cost increase can reduce gross margins by around 300–500 basis points for merchant acid producers. It may also cause companies to delay maintenance spending, capacity additions, and project approvals until feedstock and selling-price conditions become more predictable.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price shock pass-through limits | -1.5% | North America imports, EU, APAC buyers | Short term |

| Hazard compliance cost burden | -1.2% | EU, North America, OECD Asia | Medium term |

| Import dependency exposure | -1.0% | North America, India, and Africa | Medium term |

| Smelter outage supply loss | -0.9% | Americas mining belts, US, EU | Short term |

| Terminal and tank scarcity | -0.8% | South America, Africa, and inland APAC | Medium term |

| Fertilizer cycle concentration | -0.7% | China, India, North America | Short term |

Driver

Battery-material refining is becoming a stronger sulfuric acid demand driver because nickel HPAL processing, precursor production, and selected battery-recycling routes consume large quantities of acid. The IEA reported that electric vehicle battery demand exceeded 750 GWh in 2023, while battery-related nickel consumption approached 370 kilotons and increased by nearly 30% year over year.

Announced investment in electric vehicle and battery manufacturing during 2022–2023 totaled almost US$500 billion, with about 40% already committed. This expansion supports long-duration acid supply agreements, specialized reagent services, and co-located infrastructure near battery-material plants. Producers operating close to Indonesia, China, Australia, and Canada can secure steadier capacity utilization and may justify investment in terminals, dedicated storage systems, dilution facilities, and captive acid production units.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phosphate fertilizer conversion demand | +1.8% | China, India, North America, MENA | Short term |

| Battery metals refining growth | +1.5% | Indonesia, China, Australia, Canada | Medium term |

| Copper leach and SX-EW demand | +1.3% | Chile, Peru, the US Southwest, Congo corridor | Medium term |

| Sulfur recovery expansion | +0.9% | Middle East, China, Central Asia, US Gulf | Medium term |

| Industrial chemical intermediates pull | +0.8% | North America core, EU, APAC manufacturing | Short term |

| Recycling and regeneration support | +0.6% | North America, the EU, and Japan | Medium term |

Challenge

Sulfuric acid producers remain vulnerable to sudden sulfur price changes because elemental sulfur availability depends mainly on refinery and gas-processing activity rather than acid-market demand. During 2025, Tampa sulfur pricing increased from about US$ 116 per long ton at the beginning of the year to US$ 270 per long ton in early April. Such movements can create an estimated 11%–18% variation in delivered sulfur costs and reduce EBITDA margins by roughly 220–420 basis points when customer contracts are adjusted with a one-quarter delay.

Imported sulfur and sulfuric acid account for around one-third of U.S. consumption, leaving coastal markets particularly exposed to international supply conditions. This volatility can widen monthly sulfuric acid price spreads by approximately US$25–US$55 per ton and encourage buyers to adopt shorter contracts, maintain larger working-capital reserves, and diversify their supplier base.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Sulfur feedstock volatility | -1.4% | North America imports, EU buyers, APAC traders | Medium term |

| Smelter-linked acid imbalance | -1.1% | Latin America copper belts, China smelter hubs, EU import nodes | Medium term |

| Hazard logistics bottlenecks | -0.9% | APAC logistics corridors, inland Africa, South America mining routes | Medium term |

| Decarbonization retrofit burden | -0.8% | EU regulatory hubs, North America core, OECD Asia | Long term |

| Concentrated end-use exposure | -0.7% | China, India, North America phosphate chain | Short term |

| Technical labor aging gap | -0.6% | North America core, EU industrial clusters, Japan | Long term |

Geopolitical Impact Analysis

Resource Nationalism and Sovereign Vulnerability

The global sulfuric acid market had become a high-stakes geopolitical struggle driven by supply disruptions, export controls, and unequal purchasing power. At the center of the crisis was the Strait of Hormuz, which, according to the Modern War Institute at West Point and The Oregon Group, handles around 50% of global seaborne sulphur trade. When instability disrupted shipping through the strait, the effects spread rapidly because most sulfuric acid production depends on sulfur recovered as a byproduct of petroleum refining and natural gas processing.

Research from the U.S. Geological Survey Mineral Commodity Summaries and University College London shows that this process supplies the raw material required for an estimated 80–92% of sulfuric acid production facilities worldwide. The crisis deepened further as China and Russia imposed export quotas to shield domestic industries from global market shocks. These restrictions trapped large volumes of sulfur and sulfuric acid within national borders, tightening global supply even more.

Sovereign-level hoarding transformed sulfuric acid from a relatively overlooked industrial chemical into a strategically contested resource, creating an estimated $1.4 billion import burden on vulnerable agrarian regions in Western Europe and Latin America, based on USGS Mineral Commodity Summaries domestic value shipment data (2026).

Regional Analysis

Asia Pacific Held the Largest Share of the Global Sulfuric Acid Market

The global market for sulfuric acid in 2026 has a dominant presence in the Asia Pacific region, with the highest market share standing at 47.6%. The high market dominance in terms of regional shares reflects a huge industrial consumption of more than 65 million tons. The high consumption rates result from the huge agriculture and electronics manufacturing industries in China and India.

This market dominance will be altered significantly due to a major event in the 2026 market, whereby China has implemented chemical retention quotas to safeguard its internal agriculture chain from outside competition through merchant exportation. On the other hand, MEA emerges as the fastest-growing market segment.

Such fast development is being driven by enormous oil refineries and gas purification plants operating in countries such as Saudi Arabia that have decided to engage in forward integration very rapidly. Thanks to the adoption of modern technologies for transforming gases into acids, the plants can utilize raw emissions of hydrogen sulfide to generate profits in the form of a valuable product..

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Global sulfuric acid market dynamics include vertical integration, regional focus, and supply chain consolidation as players adapt to growing price volatility in the input markets and geopolitical threats. Major players prefer moving out of spot prices exposure into closed-loop strategies to create demand security while coping with volatile prices in the sulfur market that have recently touched the $7,050 per ton level.

Product purity, process automation, and long-term agreements with end users are becoming defining aspects in competitive positioning strategies. Firms are also working towards strengthening their logistics facilities to guarantee dependable supplies for sensitive uses, including electric vehicle production and energy storage solutions.

The Following Are Some of the Major Players in the Industry

- The Mosaic Company

- AkzoNobel N.V.

- BASF SE

- PVS Chemical Solution, Inc.

- Solvay SA

- Nutrien Ltd.

- INEOS Group Holdings S.A.

- Other Key Players

Key Development

- In April 2025, BASF SE launched a major capital investment in a high double-digit million-euro range to construct a brand-new, ultra-pure semiconductor-grade sulfuric acid facility at its Ludwigshafen site in Germany, targeting European microchip manufacturing demand.

- In May 2025, Ecovyst Inc. finalized a $41 million transaction to acquire the strategic virgin and regenerated sulfuric acid production assets of Cornerstone Chemical Company in Waggaman, Louisiana, expanding its global industrial supply footprint.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 18.0 Bn |

| Forecast Revenue (2035) | USD 29.1 Bn |

| CAGR (2026-2035) | 4.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2025 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Elemental Sulfur, Base Metal Smelters, Pyrite Ore, and Others), By Grade (Industrial Grade, Technical Grade, Battery Acid, Oleum / Fuming Sulfuric Acid, and Reagent Grade), By Application (Fertilizers, Chemical Manufacturing, Metal Processing & Metallurgy, Petroleum Refining, Automotive Batteries, and Others), By Distribution Channel (Direct Sales, Contract Supply, Industrial Distributors, and Spot Sales) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | The Mosaic Company, Akzo Nobel N.V., BASF SE, PVS Chemical Solutions, Inc., Solvay SA, Nutrien Ltd., INEOS Group Holdings S.A., Other key market players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |