Quick Navigation

Report Overview

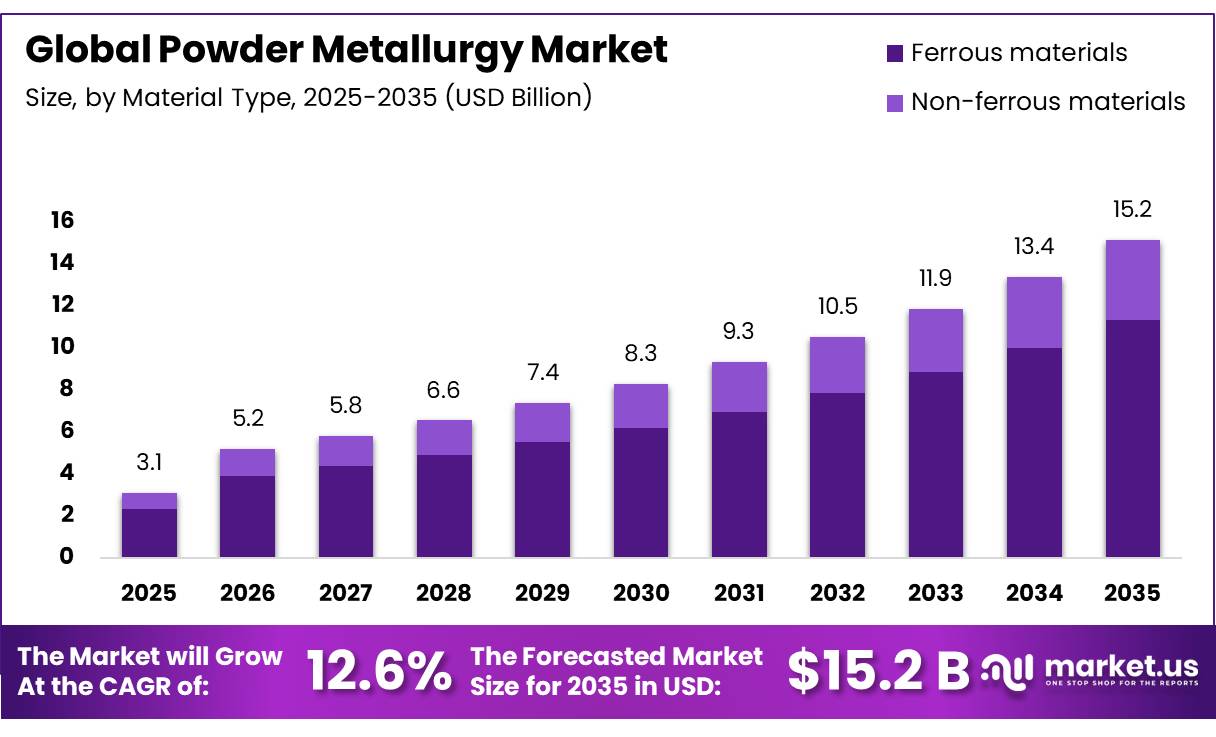

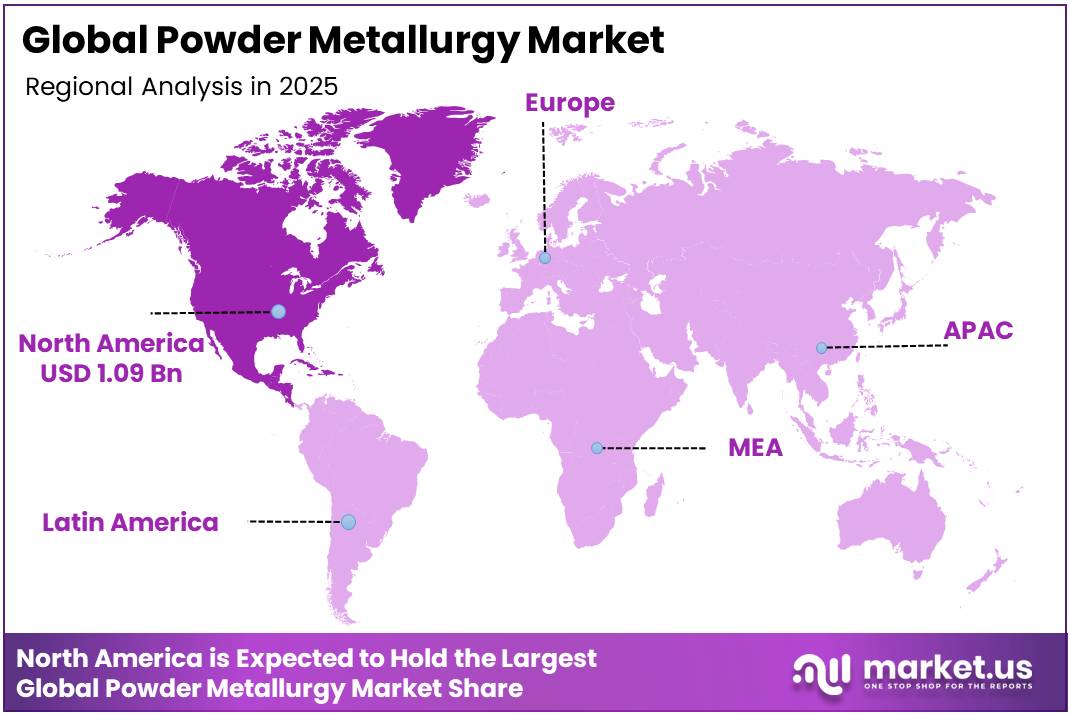

In 2025, the Global Powder Metallurgy Market was valued at US$3.1 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 12.6%, reaching about US$15.2 billion by 2035. North America held a dominant market position, capturing more than 35.2% share and generating USD 1.09 billion in revenue.

The powder metallurgy market is a core segment of the advanced manufacturing value chain, enabling the production of precision metal components through controlled compaction and sintering of metal powders a process that eliminates the material waste and geometric limitations associated with conventional machining and casting.

- According to the Metal Powder Industries Federation (MPIF, 2025), powder metallurgy typically converts more than 97% of the starting raw material into the finished component, significantly reducing scrap compared with machining-intensive production methods.

- According to the European Powder Metallurgy Association (EPMA, 2025), in a truck-transmission component comparison, the powder metallurgy route consumed only around 43% of the energy required by forging and machining. These material and energy efficiencies strengthen the process’s commercial importance in high-volume automotive and industrial component manufacturing.

Key Takeaways

- The global powder metallurgy market was valued at USD 3.1 billion in 2025.

- The market is projected to grow at a CAGR of 12.6% and is estimated to reach USD 15.2 billion by 2035.

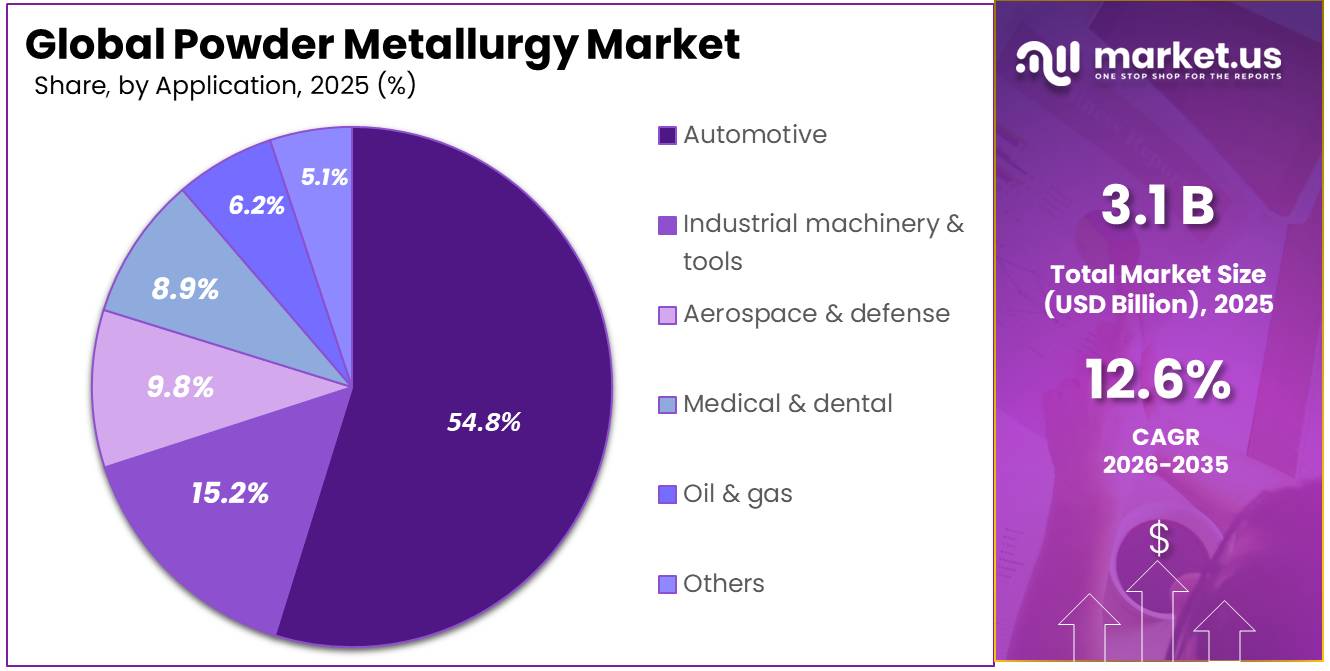

- On the basis of application, the automotive segment dominated the market, constituting 54.8% of the total market share.

- Based on the process, press and sinter dominated the powder metallurgy market, with a substantial market share of around 44.2%.

- Based on the material type, ferrous materials led the market, comprising 74.7% of the total market.

- In 2025, North America was the most dominant region in the powder metallurgy market, accounting for 35.2% of the total global consumption.

Demand is closely tied to the expansion of electric vehicle production, aerospace manufacturing, medical device development, and industrial machinery where the need for lightweight, high-strength, and complex-geometry components is growing with every passing year. Ferrous and non-ferrous metal powders form the primary material base, with process technologies including press and sinter, metal injection moulding, additive manufacturing, and hot isostatic pressing each serving distinct application requirements across the market’s broad end-use landscape.

- According to the Japan Powder Metallurgy Association, the average weight of sintered components used per vehicle reached 14.8 kilograms in the United States and 8.4 kilograms in Europe in 2024, demonstrating the significant role of powder metallurgy components in vehicle systems and precision mechanical assemblies.

Production and consumption are significantly concentrated in North America and Asia-Pacific, which together account for the majority of global powder metallurgy manufacturing capacity and end-use demand. North America leads in high-value aerospace, defence, and additive manufacturing applications, while Asia-Pacific driven primarily by China’s massive automotive and industrial manufacturing base commands the largest regional volume share and is growing at the fastest pace.

Japan and South Korea remain key technology leaders in precision metal injection moulding and advanced sintering technologies, while emerging manufacturing bases across India, Southeast Asia, and Eastern Europe are gradually expanding local powder metallurgy capabilities through industrial policy support and foreign investment.

- According to American Metal Powder Industries Federation approximately 70% of iron powder shipments in North America are consumed by the passenger vehicle segment, highlighting the deep structural integration of powder metallurgy within automotive manufacturing supply chains.

Application Analysis

Automotive Represents the Dominant Segment in the Market.

Automotive accounts for the largest share in the powder metallurgy market at 54.8% and honestly, that should surprise no one. Cars are built from thousands of precisely engineered metal components, and powder metallurgy is one of the most efficient and cost-effective ways to produce them at the volume and consistency that automotive manufacturing demands. Gears, bearings, bushings, connecting rods, valve seat inserts these are the kinds of components that powder metallurgy produces better, faster, and with less waste than almost any alternative process.

For instance: In May 2024, Amsted Automotive presented cutting-edge powder metallurgy innovations for next-generation powertrain development at the CTI Symposium showcasing advanced sintered gear and transmission components specifically engineered for electric vehicle drivetrains and directly reflecting how the automotive sector’s transition to EVs is driving real and significant product innovation investment across the powder metallurgy industry globally.

Process Analysis

Press & Sinter Represents the Dominant Segment in the Market.

Press and sinter leads the powder metallurgy process segment with 44.2% share and its dominance reflects a straightforward manufacturing reality. It is the most mature, most widely understood, and most cost-efficient powder metallurgy process available making it the default choice for high-volume production of standard components across automotive, industrial, and consumer product applications.

The process is reliable, scalable, and well-supported by a deep global ecosystem of equipment suppliers, tooling specialists, and process engineers who have been refining it for decades. For manufacturers producing millions of identical components at tight cost targets, press and sinter remains the most commercially sensible process choice in most standard applications.

- In February 2026, the European Powder Metallurgy Association reported that press and sinter accounted for approximately 85% of the metal powders supplied for powder metallurgy parts by tonnage in 2024, making it the largest conventional PM processing route.

Material Type Analysis

Ferrous Materials Represent the Dominant Segment in the Market.

Ferrous materials iron and steel-based powders dominate the powder metallurgy material segment with 74.7% share, and their dominance is built on a foundation of cost, availability, and proven performance across the widest range of applications. Iron and steel powders are significantly cheaper than non-ferrous alternatives, produced at enormous global scale, and compatible with the full range of powder metallurgy processes making them the natural default material choice for the vast majority of standard automotive, industrial, and machinery applications.

- In June 2026, the Metal Powder Industries Federation reported that estimated North American iron and steel powder shipments reached 268,880 metric tons in 2025, against total metal powder shipments of 327,379 metric tons. Based on these figures, iron and steel powders accounted for approximately 82.1% of total regional shipment volume. When separately reported stainless steel powder shipments are also included, ferrous powders represented approximately 83.6% of the total.

Non-ferrous materials including titanium, aluminium, copper, nickel, and cobalt-based powders account for the remaining share and represent the most technologically advanced and highest-value segment of the powder metallurgy materials market. Titanium is growing fastest, driven by its exceptional strength-to-weight ratio and biocompatibility properties that make it the material of choice for aerospace structural components and medical implants alike.

Key Market Segments

By Application

- Automotive

- Industrial machinery & tools

- Aerospace & defense

- Medical & dental

- Oil & gas

- Others

By Process

- Press & sinter

- Metal injection molding (MIM)

- Additive manufacturing

- Hot isostatic pressing (HIP)

By Material Type

- Ferrous materials

- Non‑ferrous materials

Driver Analysis

Auto production rebound and ICE-hybrid component intensity

Global motor vehicle production rose from 92.7 million units in 2024 to 96.4 million in 2025, up 3.9%, and Asia-Pacific production increased 7.6% to around 59.2 million vehicles, with China reaching 34.53 million units and India 6.49 million units in 2025. That matters because conventional and hybrid drivetrains still carry a high concentration of PM-intensive parts such as sprockets, connecting-rod caps, cam phasers, valve-train components, oil-pump gears, and transmission elements, so even a modest global production increase translates into meaningful tonnage utilization for ferrous powder and compaction lines.

The estimated +1.3 percentage-point CAGR support is strongest in the short term because PM producers can monetize installed press-and-sinter capacity quickly when OEM build schedules improve, especially in APAC and North America, while Europe contributes more selectively as its automotive base remains comparatively slower-growing.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV drivetrain scaling and lightweight PM parts demand | +1.6% | China core, EU, U.S., India, East Asia supply corridors | Medium term (2-4 years) |

| Auto production rebound and ICE-hybrid component intensity | +1.3% | APAC core, North America core, EU selective, MENA spill-over | Short term (≤ 2 years) |

| Industrial decarbonization and near-net-shape efficiency shift | +1.1% | U.S., EU, Japan, Korea, China industrial clusters | Medium term (2-4 years) |

| Critical raw materials security and regionalized powder supply | +0.9% | EU core, U.S., Canada, Australia, Japan | Medium term (2-4 years) |

| Sustainable product rules, recycled content, and circular manufacturing | +0.8% | EU core, U.K. alignment spill-over, export-oriented Asia | Long term (≥ 4 years) |

| Manufacturing resilience and medium-high-tech capacity expansion | +1.0% | APAC core, India, ASEAN, Mexico, Central Europe | Medium term (2-4 years) |

Restraint Analysis

Trade policy frictions on steel and metal powders

Trade policy frictions, notably tariff changes and anti-dumping measures on steel and related products, directly affect the economics of cross-border powder metallurgy supply chains because metal powder flows are nested within HS codes for steel, metal products, and specialty powders monitored by UN Comtrade and WTO/OECD trade policy reviews. For example, OECD documentation of 2024 steel trade developments indicates Mexico added 72 new tariff lines for steel products, while WTO filings show multiple economies, including India, reviewing retaliatory duties of up to 25–50% on certain steel and aluminum imports in response to tariff hikes from major trading partners, materially shifting landed costs for downstream products such as atomized powders.

This environment leads to elongated lead times, greater dependence on bonded warehouses, and higher trade finance costs, collectively reducing net export margins by 180–240 basis points and deferring cross-border capacity expansions and new customer qualifications by 1–2 years. Quantitatively, this trade friction is modeled to shave ~1.9 percentage points off the global powder metallurgy CAGR over 2026–2030, with export-dependent corridors in North America, the EU, and India particularly affected as they juggle tariff volatility, rules-of-origin compliance, and renegotiation of long-term supply contracts for automotive and aerospace powder components.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile ferrous raw material input costs | -2.3% | EU, North America core, APAC industrial hubs | Medium term (2-4 years) |

| Trade policy frictions on steel and metal powders | -1.9% | North America, EU, India export corridors | Medium term (2-4 years) |

| Automotive demand downcycle and platform shift | -1.7% | EU, Japan, North America, China OEM belt | Short to medium term (≤ 4 years) |

| Capital intensity and delayed capacity additions | -1.5% | APAC corridors, EU, emerging markets | Long term (≥ 4 years) |

| Environmental and occupational compliance tightening | -1.4% | EU, North America core, China coastal | Medium to long term (≥ 3 years) |

| Supply chain concentration in critical metal powders | -1.3% | APAC corridors, EU, North America | Medium term (2-4 years) |

Opportunity Analysis

PM-to-AM powder shift

This is an opportunity rather than a baseline driver because conventional press-and-sinter demand already underpins current market growth, whereas the future upside comes from powder metallurgy companies expanding into certified metal powders for additive manufacturing, parameter libraries, and print-ready material subscriptions that monetize the same atomization and particle-engineering base in higher-value formats.

A practical upside model is that if 12–18% of incumbent ferrous and specialty powder suppliers convert even 6–8% of revenue mix into AM-grade titanium, nickel, stainless, and cobalt-based powders by 2030, blended ASPs can rise about 2.0–3.5x versus standard PM powders, gross margins can expand by roughly 600–1,000 basis points, scrap-adjusted customer material efficiency can improve 10–20%, and recurring revenue from qualification support, reuse analytics, and digital material files can add 8–12% to annual account value, supporting an incremental market CAGR uplift of about 1.9 percentage points above baseline in the regions where standardization and certification infrastructure are already maturing

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| PM-to-AM powder shift | +1.9% | North America core, EU, Japan, India | Short term (≤ 2 years) |

| Circular powder recovery | +1.6% | EU core, North America, Japan | Medium term (2-4 years) |

| Defense & space localization | +1.4% | U.S., EU, Japan, India | Medium term (2-4 years) |

| Titanium/tungsten value-chain deepening | +1.2% | EU, U.S., Japan | Medium term (2-4 years) |

| Medtech custom implants | +1.1% | U.S., EU, advanced APAC | Short term (≤ 2 years) |

| India distributed PM scale-up | +1.8% | India, Southeast Asia, Middle East export hubs | Long term (≥ 4 years) |

Challenges Analysis

Alloy Feedstock Volatility

Powder metallurgy remains unusually exposed to alloy-input instability because atomized iron, copper, nickel, molybdenum, and specialty additions are purchased into a process window where chemistry drift of even 20-40 basis points can alter compressibility, sintering response, and final density, so raw material volatility transmits into both cost and throughput rather than only price lists; the World Bank reported rising manufacturing input-price pressure with the global manufacturing PMI input-price sub-index at 56.3 in January 2026, while commodity prices rose 8% month over month in January and metals prices stayed volatile, creating conditions in which powder producers often have to carry 45-75 days of safety stock, accept 3-6% higher working-capital lockup, and widen customer quotation validity bands from roughly 30 to 10-15 days to protect margins.

In practice, that pushes an estimated 80-140 basis point drag on achievable market growth by delaying bid conversion in automotive and industrial programs, raising scrap/reblend ratios by roughly 1-2 percentage points when incoming powder lots vary, and forcing OEM suppliers to redesign surcharge clauses, dual-source additive packages, and monthly rather than quarterly feedstock indexation to keep program economics stable.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Alloy Feedstock Volatility | -1.2% | North America core, EU regulatory hubs, APAC export bases | Medium term (2-4 years) |

| Critical Mineral Concentration | -1.0% | EU import-dependent clusters, U.S. specialty alloy chain, East Asia processing corridors | Long term (≥ 4 years) |

| Process Yield Variability | -0.8% | Global high-spec automotive, aerospace, medical components | Medium term (2-4 years) |

| Skilled Sintering Talent Gap | -0.7% | Germany, Japan, U.S. Midwest, Central Europe, China coastal clusters | Long term (≥ 4 years) |

| Energy-Intensity Cost Swings | -0.9% | Europe powder plants, Japan/Korea import-energy markets, India retrofit sites blogs. | Short term (≤ 2 years) |

| End-Market Planning Instability | -1.1% | Automotive-heavy NA/EU, industrial APAC, export-oriented EMDE suppliers | Medium term (2-4 years) |

Geopolitical Impact Analysis

Trade Tensions and Raw Material Supply Concentration Are Creating Real Pressure Across the Powder Metallurgy Supply Chain.

The powder metallurgy market is more exposed to geopolitical developments than its industrial positioning might suggest because the metal powders that form the foundation of everything this industry produces are sourced from a remarkably concentrated group of countries. China dominates global production of many critical metal powders including tungsten, rare earth magnetic powders, and speciality alloy powders and the export restrictions Beijing has progressively introduced on strategic materials since 2023 have created genuine supply availability concerns for powder metallurgy manufacturers operating outside China.

US tariff measures introduced in 2025 have added further cost pressure across the value chain forcing American manufacturers to urgently diversify sourcing toward higher-cost alternative suppliers in Europe, Japan, and domestic producers. High-purity metal powders including copper and nickel saw significant price volatility in early 2026 as geopolitical supply pressures and trade policy shifts combined to create simultaneous demand surges and supply constraints across global metal powder markets.

For instance, In February2026, Dauch Corporation acquired GKN Powder Metallurgy directly reflecting how geopolitical pressure to localise advanced manufacturing supply chains is fundamentally reshaping the competitive structure of the global powder metallurgy industry.

Regional Analysis

North America Leads the Global Powder Metallurgy Market.

In 2025, North America dominated the global powder metallurgy market, holding 35.2% of total global consumption a leadership position built on the region’s deeply integrated advanced manufacturing ecosystem, world-class aerospace and defence industries, and one of the most technically mature and demanding automotive sectors in the world.

The United States alone accounts for the overwhelming majority of North America’s market share, driven by its extraordinary concentration of tier-one automotive component manufacturers, defence-grade powder metallurgy producers, and additive manufacturing technology developers that collectively generate consistent and high-value demand for both standard and advanced powder metallurgy products.

Similarly, Canada contributes meaningfully through its aerospace and industrial manufacturing sectors, while Mexico’s rapidly expanding automotive assembly base is generating growing downstream demand for powder metallurgy components across its tier-one supplier network. Meanwhile, strong federal government investment in domestic advanced manufacturing capability including defence-related powder metallurgy applications and additive manufacturing infrastructure through programmes like the Manufacturing USA initiative is adding further structural support to the region’s market leadership.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global powder metallurgy market is dominated by a small group of large, well-resourced multinational manufacturers that have built their market positions over decades through deep process expertise, proprietary material technologies, long-established relationships with automotive and aerospace OEMs, and global manufacturing networks that give them the scale and geographic reach that smaller players simply cannot match.

These leading companies collectively hold the majority of commercially deployed powder metallurgy production capacity and registered material and process intellectual property advantages that are particularly powerful in an industry where customer qualification cycles are long, switching costs are high, and the technical barriers to producing consistently high-quality powder metallurgy components at automotive or aerospace grade are genuinely significant.

The Major Players in The Industry

- GKN Powder Metallurgy

- Höganäs AB

- Sandvik AB

- Carpenter Technology Corporation

- Miba AG

- Sumitomo Electric Industries, Ltd.

- Kennametal Inc.

- Fine Sinter Co., Ltd.

- PMG Holding GmbH

- Stackpole International

- Rio Tinto Metal Powders

- ATI Inc.

- C. Starck GmbH

- Advanced Technology & Materials Co., Ltd. (AT&M)

- ExOne / Desktop Metal

- Others

Key Development

- In February 2025, Carpenter Technology Corporation strengthened its position in the powder metallurgy and specialty-alloy market by announcing an investment of nearly US$400 million to expand its manufacturing site in Athens, Alabama. The project includes a new vacuum induction melting furnace, additional remelting equipment and finishing assets, which are expected to add around 9,000 tons of annual high-purity alloy capacity.

- In June 2025, GKN Powder Metallurgy introduced new Metallic Membrane cartridge filters for chemical, pharmaceutical and food-processing applications. These filters provide up to 30% higher productivity, are available in lengths of up to 72 inches, and offer filtration grades ranging from 3 micrometres to 1 micrometres.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.1 Bn |

| Forecast Revenue (2035) | USD 15.2 Bn |

| CAGR (2026-2035) | 12.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Application (Automotive, Industrial Machinery & Tools, Aerospace & Defense, Medical & Dental, Oil & Gas, and Others), By Process (Press & Sinter, Metal Injection Molding (MIM), Additive Manufacturing, and Hot Isostatic Pressing (HIP)), By Material Type (Ferrous Materials and Non-Ferrous Materials) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | GKN Powder Metallurgy, Höganäs AB, Sandvik AB, Carpenter Technology Corporation, Miba AG, Sumitomo Electric Industries Ltd., Kennametal Inc., Fine Sinter Co. Ltd., PMG Holding GmbH, Stackpole International, Rio Tinto Metal Powders, ATI Inc., H.C. Starck GmbH, Advanced Technology & Materials Co. Ltd. (AT&M), ExOne / Desktop Metal, and others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |