Quick Navigation

Report Overview

Global Rainwater Harvesting Market is expected to be worth around USD 2.5 billion by 2034, up from USD 1.4 billion in 2024, and grow at a CAGR of 6.0% from 2025 to 2034. Increasing urbanization in North America is boosting rainwater harvesting adoption, strengthening its 43.20% market share.

Rainwater harvesting is the practice of collecting and storing rainwater for later use, reducing dependence on traditional water sources. It involves systems like rooftop catchments, surface runoff collection, and underground reservoirs to capture rainfall. This water can be used for irrigation, household needs, groundwater recharge, and even potable use with proper treatment. By implementing rainwater harvesting, communities can enhance water security, reduce utility costs, and support environmental sustainability by minimizing stormwater runoff and soil erosion.

The rainwater harvesting market refers to the industry that develops, installs, and maintains systems for collecting and utilizing rainwater. As water scarcity intensifies globally, governments, businesses, and homeowners are adopting these systems to ensure a sustainable water supply. The market includes components like storage tanks, filtration units, pumps, and smart monitoring systems. It is driven by rising environmental awareness, stricter water conservation regulations, and growing demand for alternative water sources in agriculture, industrial, and residential applications.

Urbanization and climate change are key drivers of the rainwater harvesting market, increasing the need for sustainable water solutions. With unpredictable rainfall patterns and depleting groundwater reserves, governments are promoting policies that incentivize water conservation. Additionally, advancements in storage and filtration technology make rainwater harvesting more efficient and accessible for both urban and rural areas.

The growing need for water conservation in drought-prone regions is pushing demand for rainwater harvesting systems. Industries facing water shortages are integrating these systems to maintain operations while reducing utility costs. Additionally, the rising cost of municipal water supplies encourages households and businesses to adopt rainwater collection as a cost-effective alternative.

Key Takeaways

- Global Rainwater Harvesting Market is expected to be worth around USD 2.5 billion by 2034, up from USD 1.4 billion in 2024, and grow at a CAGR of 6.0% from 2025 to 2034.

- Above-ground rainwater harvesting accounts for 69.30%, ensuring easy installation and maintenance efficiency.

- The dry system comprises 32.50%, offering cost-effective storage without continuous pipe water retention.

- Original equipment manufacturers dominate 65.70%, providing reliable components and advanced water harvesting solutions.

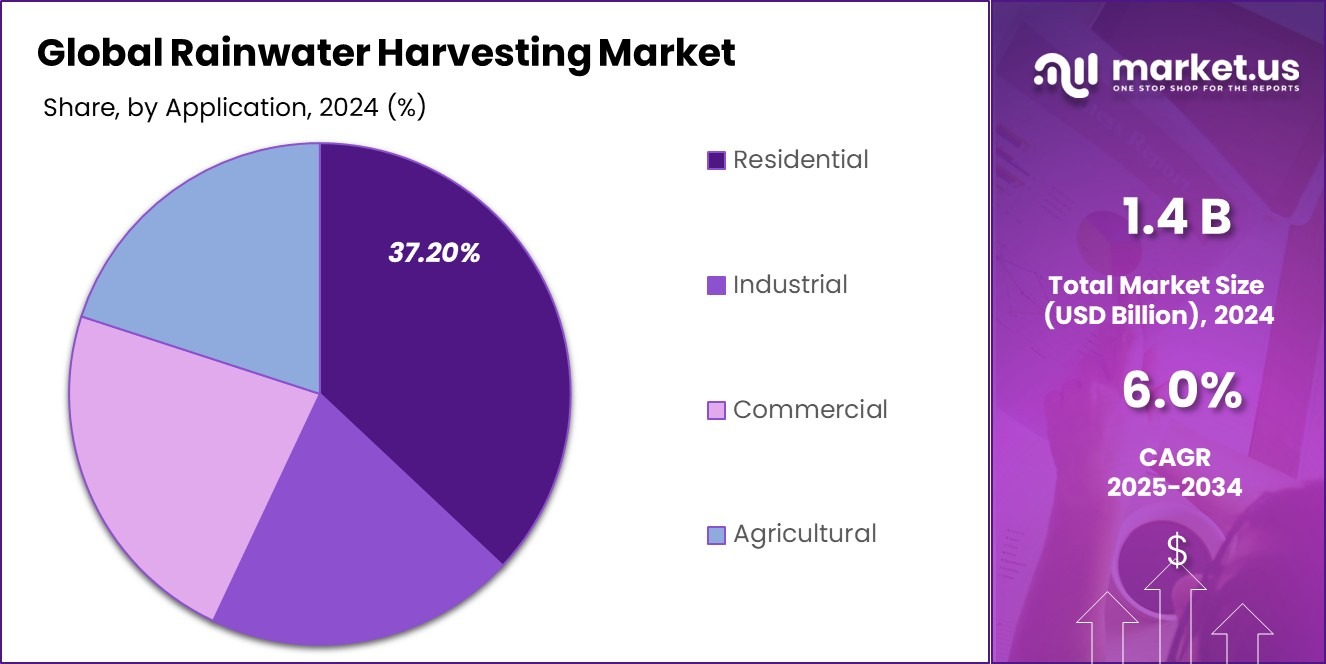

- Residential usage holds 37.20%, reflecting growing homeowner interest in sustainable water conservation methods.

- The North American rainwater harvesting market was valued at USD 0.6 billion, driven by water conservation initiatives.

By Harvesting System Analysis

In the Rainwater Harvesting Market, Above Ground Harvesting dominated with a 69.30% market share in 2024.

In 2024, Above Ground Harvesting held a dominant market position in the Harvesting System segment of the Rainwater Harvesting Market, with a 69.30% share. This growth is attributed to its ease of installation, lower initial costs, and suitability for residential, commercial, and agricultural applications.

Above-ground systems, including storage tanks and collection units, are widely adopted due to their accessibility and minimal maintenance requirements. Increasing government incentives for water conservation and rising awareness among homeowners and industries have further fueled the demand for these systems.

Urbanization and climate change have played a crucial role in driving the adoption of rainwater harvesting systems. With unpredictable rainfall patterns and declining groundwater levels, municipal bodies and businesses are integrating these systems to ensure water security. Additionally, industrial and commercial sectors are increasingly investing in above-ground solutions to meet regulatory compliance and reduce dependency on municipal water supplies.

Meanwhile, below-ground harvesting systems, though gaining traction, require higher capital investment and complex installation, limiting their adoption. However, advancements in filtration and monitoring technologies are expected to enhance system efficiency, opening new growth opportunities.

By Type Analysis

The Dry System held a 32.50% share in the Rainwater Harvesting Market, driven by affordability.

In 2024, Dry Systems held a dominant market position in the by-type segment of the Rainwater Harvesting Market, with a 32.50% share. This system’s widespread adoption is driven by its cost-effectiveness, minimal maintenance requirements, and suitability for residential and small-scale commercial applications.

The dry system is preferred due to its simple design, which allows rainwater to flow directly into storage tanks without the need for complex underground piping. This makes it an ideal choice for regions with moderate rainfall, where storage and utilization are efficiently managed.

The rising demand for water conservation in drought-prone regions has significantly contributed to the growth of dry systems. Households and businesses are increasingly opting for this system as it offers a practical solution for non-potable applications such as irrigation, toilet flushing, and landscaping. Additionally, government initiatives promoting rainwater harvesting have accelerated the installation of dry systems, particularly in suburban and rural areas.

Compared to wet systems, which require underground piping and higher installation costs, dry systems offer a lower barrier to entry for consumers. As urban water prices continue to rise and environmental awareness grows, the demand for efficient and affordable rainwater harvesting solutions like the dry system is expected to remain strong.

By Service Provider Analysis

Original Equipment Manufacturer led the Rainwater Harvesting Market, capturing a 65.70% share through innovation and reliability.

In 2024, Original Equipment Manufacturer (OEM) held a dominant market position in the By Service Provider segment of the Rainwater Harvesting Market, with a 65.70% share. The dominance of OEMs is driven by their ability to provide high-quality, customized solutions, advanced technological integration, and long-term reliability in rainwater harvesting systems. These manufacturers cater to residential, commercial, and industrial sectors by offering efficient storage tanks, filtration units, pumps, and monitoring devices designed for diverse water conservation needs.

The increasing adoption of smart rainwater harvesting systems, which integrate IoT-enabled monitoring and automated filtration, has further strengthened the role of OEMs. Their expertise in research and development, compliance with environmental regulations, and product innovation have positioned them as preferred providers in the market. Additionally, OEMs ensure consistent after-sales support, maintenance services, and warranties, making them a reliable choice for large-scale projects.

While third-party service providers and independent installers are gaining traction, OEMs maintain an edge due to their brand reputation, established distribution networks, and large-scale production capabilities. As demand for sustainable water management solutions rises, OEMs are expected to continue leading the market by expanding their product offerings and enhancing system efficiencies.

By Application Analysis

The Residential segment accounted for a 37.20% share of the Rainwater Harvesting Market in 2024.

In 2024, Residential held a dominant market position in the By Application segment of the Rainwater Harvesting Market, with a 37.20% share. The increasing adoption of rainwater harvesting systems in residential properties is driven by rising water costs, growing environmental awareness, and government incentives promoting sustainable water usage. Homeowners are investing in these systems to reduce dependency on municipal water supplies, especially in regions experiencing frequent droughts and water shortages.

The preference for above-ground and dry systems in residential applications has significantly contributed to this segment’s growth. These systems offer cost-effective installation, low maintenance, and immediate usability for irrigation, toilet flushing, and household cleaning. Additionally, government regulations and rebates for rainwater harvesting installations have encouraged widespread adoption in urban and suburban housing projects.

The demand for smart water management solutions in modern homes has also fueled the market, with homeowners opting for automated storage and filtration systems to optimize water usage. While commercial and industrial applications are expanding, the residential sector remains the key growth driver, supported by increasing awareness of self-sustaining water conservation solutions. As urbanization continues, the residential segment is expected to maintain its strong market presence.

Key Market Segments

By Harvesting System

- Above Ground Harvesting

- Under Ground Harvesting

By Type

- Rain Barrel System

- Dry System

- Wet System

- Green Roof System

- Others

By Service Provider

- Original Equipment Manufacturer

- Independent Supplier

By Application

- Residential

- Industrial

- Commercial

- Agricultural

Driving Factors

Water Scarcity and Rising Conservation Awareness

The increasing shortage of freshwater resources is the biggest driver of the rainwater harvesting market. Many regions worldwide face droughts, declining groundwater levels, and unpredictable rainfall patterns, making water conservation a critical necessity. Governments, industries, and households are actively seeking alternative water sources, and rainwater harvesting provides a sustainable and cost-effective solution.

Rising urbanization has also intensified the water demand, putting pressure on municipal supplies. As a result, authorities are implementing regulations and incentives to encourage rainwater collection systems.

Additionally, growing public awareness about water conservation has led to more residential and commercial users adopting these systems. With climate change worsening water shortages, the need for rainwater harvesting will continue to grow, shaping the market’s long-term expansion.

Restraining Factors

High Initial Costs and Installation Challenges

One of the biggest restraints in the rainwater harvesting market is the high upfront cost of installing these systems. While rainwater harvesting reduces long-term water expenses, the initial investment in tanks, filters, pumps, and piping can be expensive, especially for large-scale or underground systems. Many homeowners and businesses hesitate to adopt these systems due to the cost of materials and professional installation.

Additionally, space limitations in urban areas create installation challenges. Many buildings lack sufficient rooftop area or underground space for large storage tanks. Moreover, complex plumbing modifications may be needed to integrate these systems with existing water supply infrastructure.

Growth Opportunity

Smart Technologies Enhancing System Efficiency and Adoption

The integration of smart technologies presents a major growth opportunity in the rainwater harvesting market. Automated filtration, IoT-based monitoring, and AI-driven water usage optimization are making these systems more efficient and user-friendly. Smart sensors help track water levels, quality, and usage patterns, ensuring better management and reduced wastage.

Homeowners and businesses are more likely to invest in advanced, low-maintenance systems that provide real-time insights and remote control. Governments and environmental agencies are also promoting tech-enabled solutions to improve water conservation efforts. As digital transformation expands in the water sector, the demand for smart rainwater harvesting systems will grow.

Latest Trends

Integration of Rainwater Harvesting with Green Buildings

A key latest trend in the rainwater harvesting market is its integration with green buildings. As sustainability becomes a top priority, architects and developers are designing eco-friendly buildings with built-in rainwater collection systems. These structures use permeable surfaces, rooftop harvesting, and underground storage tanks to collect and reuse rainwater for irrigation, cooling, and sanitation.

Many governments and city planners are implementing building codes that require new constructions to include rainwater harvesting infrastructure. Additionally, businesses aiming for LEED (Leadership in Energy and Environmental Design) certification are investing in these systems to meet sustainability goals. With the push for carbon-neutral and energy-efficient buildings, integrating rainwater harvesting into urban development is expected to drive long-term market growth.

Regional Analysis

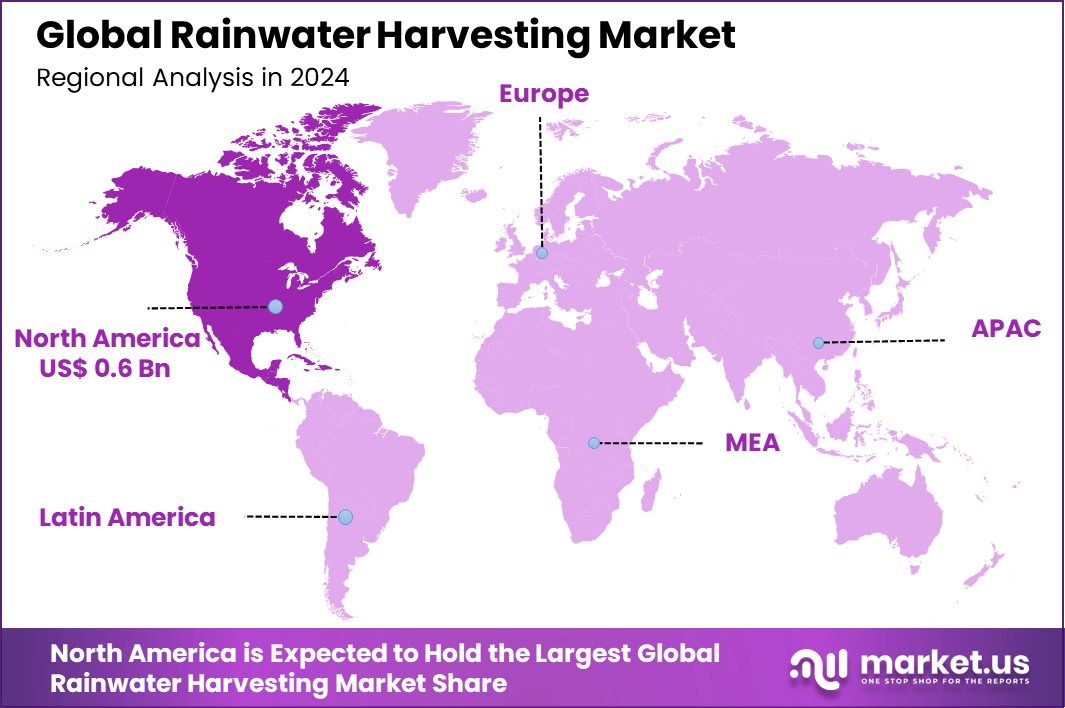

In North America, the Rainwater Harvesting Market held a 43.20% share, highlighting strong regional adoption trends.

In 2024, North America dominated the Rainwater Harvesting Market, holding a 43.20% share, with a market valuation of USD 0.6 billion. The region’s dominance is driven by strict water conservation policies, increasing urbanization, and rising adoption in residential and commercial buildings. The United States and Canada have implemented regulations promoting rainwater collection systems, further boosting market demand.

Europe follows closely, supported by environmental sustainability goals and government incentives promoting green infrastructure. Countries such as Germany, France, and the UK have witnessed significant adoption, particularly in commercial buildings and industrial applications.

The Asia Pacific region is experiencing strong growth, driven by water scarcity concerns, rapid urbanization, and increasing industrial demand. Countries like China and India are investing in rainwater harvesting systems as part of broader water conservation initiatives.

In the Middle East & Africa, limited freshwater resources and increasing reliance on alternative water sources are driving market expansion. Governments in GCC countries are implementing policies to encourage rainwater collection in urban areas.

Latin America is witnessing gradual growth, primarily in Brazil and Mexico, where rural and agricultural communities are adopting cost-effective water management solutions. As global demand for sustainable water solutions rises, regional market growth is expected to accelerate.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, key players in the global Rainwater Harvesting Market are focusing on technological advancements, regulatory compliance, and expanding regional presence to strengthen their market positions. Leading companies such as Kingspan Group, Watts Water Technologies, Inc., Graf Group, and WISY AG are leveraging product innovation and strategic partnerships to capitalize on the growing demand for sustainable water solutions.

Kingspan Group remains a dominant player, driven by its diverse product portfolio, including advanced water storage tanks and filtration systems. The company’s focus on eco-friendly and high-efficiency solutions aligns with the rising demand for sustainable infrastructure in residential and commercial projects.

Watts Water Technologies, Inc. is capitalizing on smart water management technologies, integrating IoT-based monitoring and automated control systems in rainwater harvesting solutions. With a strong presence in North America and Europe, the company is well-positioned to benefit from stringent water conservation regulations and the increasing adoption of green building standards.

Graf Group, with its focus on modular rainwater storage solutions, continues to expand in Europe and Asia Pacific. The company’s commitment to cost-effective and high-capacity systems makes it a preferred choice in urban and industrial applications.

WISY AG maintains a niche presence in high-quality rainwater filtration and pre-treatment solutions, essential for efficient system performance and water quality management. The company’s expertise in precision engineering ensures its strong positioning in premium residential and industrial segments.

Top Key Players in the Market

- Kingspan Group

- Watts Water Technologies, Inc.

- Graf Group

- WISY AG

- Innovative Water Solutions LLC

- D&D Ecotech Services

- Rain Harvesting Supplies, Inc.

- Water Field Technologies Pvt. Ltd

- Stormsaver

- Climate Inc

- DV Water Harvesters

- Heritage Tanks

- HITESH ENVIRO ENGINEERS PVT LTD

- Barr Plastics

- Caldwell Tanks

Recent Developments

- In 2024, D&D Ecotech Services continues to contribute significantly to the rainwater harvesting sector, focusing on sustainable water management solutions. D&D Ecotech provides advanced rainwater collection and conservation technologies that cater to both residential and commercial applications.

- In 2024, Water Field Technologies enhanced India’s water management with advanced, eco-friendly rainwater harvesting systems. These systems align with government sustainability policies and are aimed at conserving water effectively, supporting national water resource optimization goals.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.4 Billion |

| Forecast Revenue (2034) | USD 2.5 Billion |

| CAGR (2025-2034) | 6.0% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Harvesting System (Above Ground Harvesting, Under Ground Harvesting), By Type (Rain Barrel System, Dry System, Wet System, Green Roof System, Others), By Service Provider (Original Equipment Manufacturer, Independent Supplier), By Application (Residential, Industrial, Commercial, Agricultural) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Kingspan Group, Watts Water Technologies, Inc., Graf Group, WISY AG, Innovative Water Solutions LLC, D&D Ecotech Services, Rain Harvesting Supplies, Inc., Water Field Technologies Pvt. Ltd, Stormsaver, Climate Inc, DV Water Harvesters, Heritage Tanks, HITESH ENVIRO ENGINEERS PVT LTD, Barr Plastics, Caldwell Tanks |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |