Quick Navigation

Report Overview

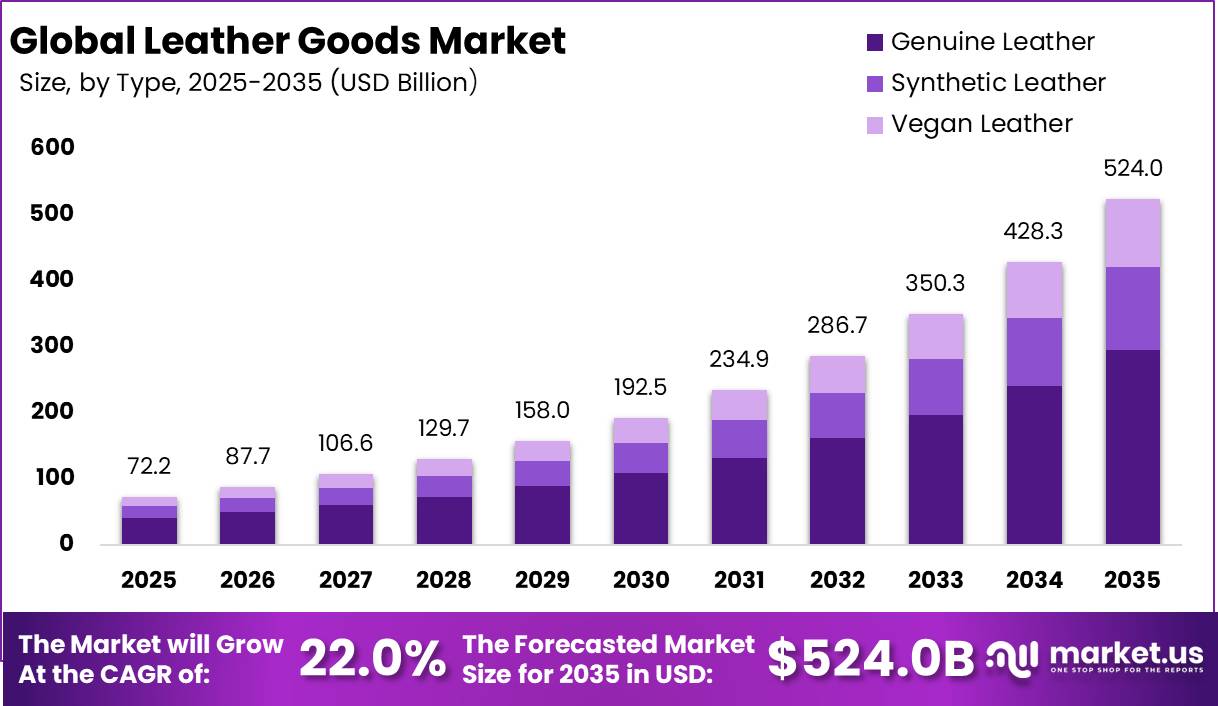

Global Leather Goods Market size is expected to be worth around USD 524.0 Billion by 2035 from USD 72.2 Billion in 2025, growing at a CAGR of 22.0% during the forecast period 2026 to 2035. This trajectory reflects a fundamental repositioning of leather goods from commodity fashion to high-value, brand-driven consumer assets across global markets.

The leather goods market spans personal accessories, apparel, home furnishings, automotive interiors, and pet products. It segments by material type across genuine, synthetic, and vegan leather and by product across handbags, small leather goods, apparel, home décor, and automotive accessories. This breadth means the market captures spending at every price tier, from mass retail to ultra-luxury.

Key Takeaways

- Global Leather Goods Market is valued at USD 72.2 Billion in 2025 and is forecast to reach USD 524 Billion by 2035.

- The market grows at a CAGR of 22.0% during the forecast period 2026 to 2035.

- Genuine Leather dominates the By Type segment with a 56.3% share in 2025.

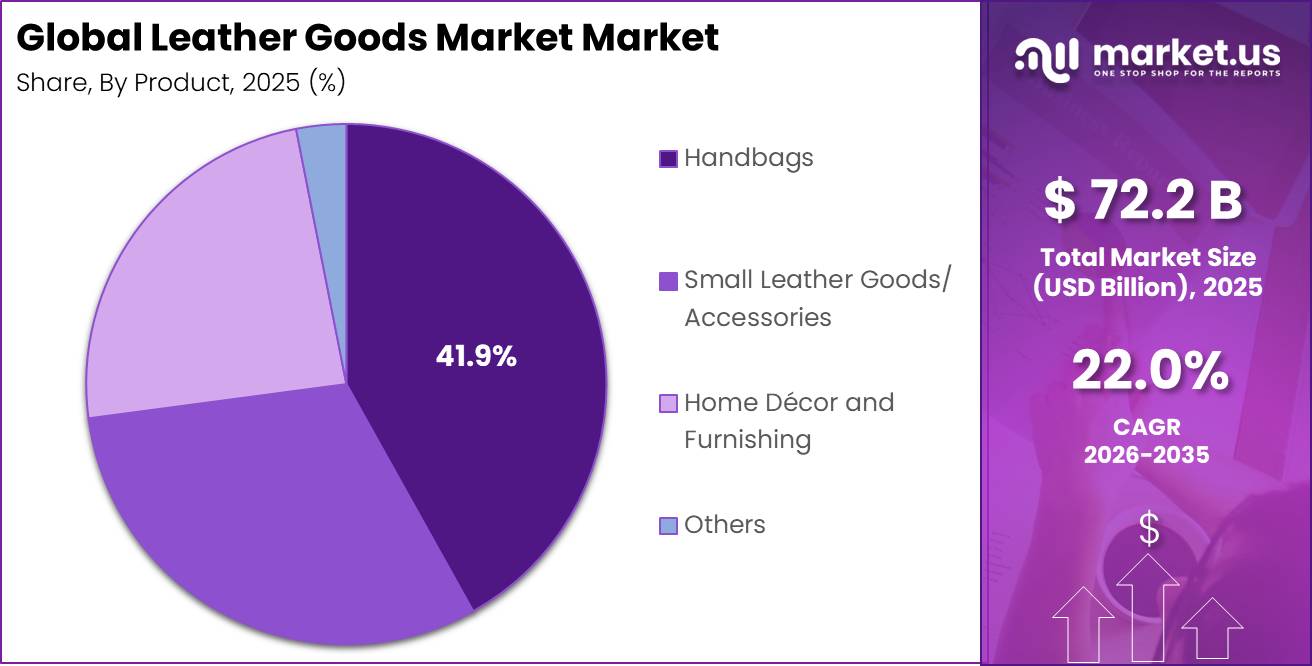

- Handbags dominate the By Product segment with a 41.9% share in 2025.

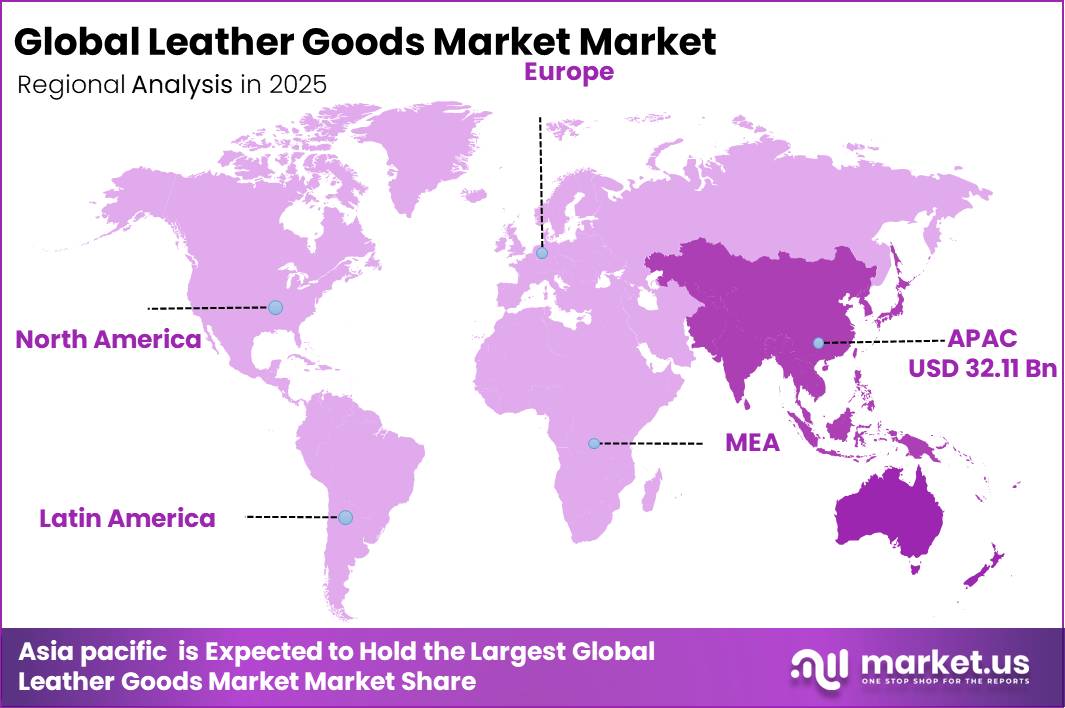

- Asia-Pacific is the leading region, holding a 44.5% market share valued at USD 32.83 Billion in 2025.

Governments across Asia-Pacific and the European Union are actively shaping leather goods supply chains through traceability mandates and tannery environmental compliance frameworks. The EU Deforestation Regulation and CITES enforcement are raising sourcing standards. This regulatory pressure is accelerating investment in certified leather supply chains, which creates compliance costs for smaller producers but builds long-term brand equity for compliant exporters.

According to PwC’s 2024 Voice of Consumer Survey, 80% of consumers are willing to pay more for sustainably produced or sourced goods. This is not marginal preference. It is mainstream buying behavior. Brands that certify and communicate sustainable sourcing are positioned to command higher price points and reduce churn among environmentally conscious buyers.

Data from PwC’s 2024 Voice of Consumer Survey shows consumers are willing to pay an average premium of 9.7% for products with sustainability-related attributes. This premium directly expands the addressable revenue pool for brands that invest in eco-tanning, traceable hides, and certified materials. Brands that delay this transition risk ceding price leadership to faster-moving competitors.

Type Analysis

Genuine Leather dominates with 56.3% due to durability perception and luxury brand preference.

In 2025, Genuine Leather held a dominant market position in the By Type segment of the Leather Goods Market, with a 56.3% share. Buyers across luxury and premium tiers consistently select genuine leather for its tactile quality, aging characteristics, and resale value retention. This structural preference creates a durable revenue base for manufacturers and brands anchored in full-grain and vegetable-tanned leather product lines.

Synthetic Leather serves a distinct buyer profile: cost-conscious consumers and performance-focused applications such as automotive seating and fashion accessories at accessible price points. As reported by PwC, 70% of consumers seek reviews before making a purchase decision, meaning synthetic leather products must consistently deliver on durability and value claims to retain repeat buyers in a review-driven discovery environment.

Vegan Leather occupies the fastest-shifting position in the material landscape. A 2024 academic study found that Generation Z exhibits stronger intentions to purchase sustainable clothing than previous young-adult cohorts. This behavioral pattern directly benefits vegan leather brands targeting Gen Z buyers in urban markets across North America and Europe, where ethical sourcing is an active purchase criterion rather than a secondary consideration.

Product Analysis

Handbags dominate with 41.9% due to brand power and consistent luxury consumer demand.

In 2025, Handbags held a dominant market position in the By Product segment of the Leather Goods Market, with a 41.9% share. LVMH’s Fashion and Leather Goods division reported an operating margin of 35% in 2025 despite industry-wide luxury demand pressure. This margin performance signals that premium handbag portfolios retain pricing power even during soft demand cycles, making them the most financially resilient product category in the market.

Small Leather Goods and Accessories anchor repeat purchasing behavior across mid-market and luxury consumers. Wallets, pouches, and watch straps generate higher transaction frequency than handbags and serve as entry points for aspirational consumers. PwC data confirms that 41% of consumers say a celebrity or influencer has influenced a purchase decision, and accessories are the category most commonly featured in influencer-led social content, amplifying their discovery and conversion rates.

In May 2026, Tapestry reported Coach handbag unit sales increasing by more than 20% and more than 2.4 million new customers acquired globally during the quarter. This result confirms that handbag-led brand strategies remain the most effective customer acquisition engine in the leather goods sector. Brands that prioritize handbag innovation and storytelling will build the broadest and most loyal consumer base over the forecast period.

Key Market Segments

By Type

- Genuine Leather

- Synthetic Leather

- Vegan Leather

By Product

- Handbags

- Tote Bag

- Clutch

- Satchel

- Others

- Small Leather Goods / Accessories

- Wallets

- Pouches

- Phone Covers/Cases

- Watch Straps

- Others

- Apparel

- Home Décor and Furnishing

- Pet Accessories

- Pet Collar and Leads

- Leather Pet Toys

- Automotive Accessories

- Seating Systems

- Others

Drivers

The leather goods market benefits from a rapid expansion of affluent consumers across emerging economies. In 2025, the global population of high-net-worth individuals exceeded 25 million, reflecting continued wealth accumulation worldwide. Wealth creation is particularly strong in Asia-Pacific and the Gulf region, where entrepreneurial activity and investment growth are converting aspirational buyers into active luxury consumers.

Influencer-led social commerce is reshaping brand discovery at scale. PwC’s 2024 Voice of Consumer Survey found that 67% of consumers use social media to discover new brands before making purchases. This behavioral shift reduces traditional media’s role in luxury brand awareness and places disproportionate power in the hands of social platforms, making DTC social commerce a mandatory channel investment for leather goods brands targeting under-40 buyers.

Social commerce conversion is accelerating beyond discovery. as per our research 46% of consumers purchased products directly through social media platforms in the survey period, compared with 21% in 2019. This more than doubling of social purchase rates creates a direct revenue channel that bypasses wholesale and reduces margin leakage for brands willing to invest in platform-native commerce infrastructure.

Research published in 2025 identified Generation Z as a major driver of sustainable apparel consumption. A survey involving 1,018 consumers confirmed that sustainability attitudes, social norms, and altruistic values significantly increase sustainable clothing purchase intentions. Leather goods brands that align product storytelling with Gen Z values will capture first-mover loyalty in the segment that will drive luxury spending over the next two decades.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income & HNWI Expansion in Emerging Markets | +2.1% | APAC (China, India, SE Asia), MEA | Short–medium term (≤3 years) |

| E-Commerce & DTC Channel Penetration | +1.6% | North America, APAC, EU digital-first cohorts | Short term (≤2 years) |

| Automotive Leather Upholstery Demand (EV-Led Premium Interiors) | +1.3% | APAC (China), North America, EU | Medium term (2–4 years) |

| Influencer-Led Social Commerce & Aspirational Brand Discovery | +1.1% | APAC (China, India, Korea), North America | Short term (≤2 years) |

| Sustainability-Driven Product Innovation (Chrome-Free & Eco-Tanning) | +1.0% | EU core, North America, urban APAC | Medium term (2–4 years) |

| Global Tourism Recovery & Destination-Retail Luxury Spending | +0.9% | EU (Paris, Milan), APAC (Japan, Dubai), North America | Short term (≤2 years) |

Restraints

The exotic leather goods segment faces mounting regulatory pressure from international wildlife trade frameworks. CITES is enforced by 184 signatory countries, requiring permits, species verification, origin documentation, and legal sourcing records for cross-border trade in protected animal products. Compliance requirements add approximately 2 to 8 weeks to shipment processing timelines, increasing operational risk for manufacturers and exporters across global trade routes.

The European Union enforces these rules across all member states and regulates trade involving more than 40,900 protected species. Documentation errors trigger shipment seizures, trade restrictions, or legal penalties. This compliance burden favors larger companies with dedicated regulatory teams and creates meaningful entry barriers for small and mid-sized brands seeking to compete in the exotic leather segment.

Figures from LVMH’s 2025 annual report show that Fashion and Leather Goods represented 39% of LVMH’s total Scope 1 and Scope 2 greenhouse-gas emissions footprint. This concentration places the segment under direct investor and regulatory scrutiny. Brands that fail to build credible emissions reduction roadmaps risk losing ESG-aligned institutional investor support and facing accelerated regulatory restrictions across their largest markets.

A 2025 research study identified Generation Z as a major driver of sustainable apparel consumption. This behavioral pattern reinforces commercial pressure on leather brands to reduce environmental impact. Brands that maintain high-emission production processes without credible transition plans face growing reputational risk among the consumer cohort that will represent the largest share of luxury spending through the 2030s.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China Luxury Demand Contraction & Structural Reset | -2.2% | APAC (China core); LVMH, Kering APAC P&L | Short–medium term (≤3 years) |

| Luxury Price Ceiling & Aspirational Consumer Retreat | -1.7% | North America, EU, APAC — aspirational tier | Short term (≤2 years) |

| CITES Exotic Skin Trade Restrictions | -1.1% | Global; EU, North America, APAC import markets | Long term (≥4 years) |

| Tannery Environmental Compliance & Closure Orders | -1.0% | India, China, Vietnam, Bangladesh tannery clusters | Medium term (2–4 years) |

| EU Animal Welfare Legislation Expansion | -0.8% | EU consumption market; LATAM, APAC supply origins | Medium–long term (3–5 years) |

| Currency Volatility & Export Margin Erosion | -0.7% | Italy, France, India, China export-dependent producers | Short term (≤2 years) |

Challenges

The leather goods industry faces a structural shortage of skilled artisans across its core manufacturing hubs in Italy, France, and Spain. The European Union is projected to lose approximately 1 million working-age individuals annually through 2050, intensifying labor availability challenges across all craft-dependent industries. In 2025, leather, footwear, and craft-related occupations were formally identified among Europe’s shortage professions, reflecting persistent recruitment difficulties.

More than one-third of manufacturing companies across Europe report challenges in filling skilled vacancies. Leather craftsmanship requires highly specialized techniques such as hand-stitching, edge-finishing, and exotic-skin preparation, with professional proficiency often requiring 5 to 10 years of training and apprenticeship. The retirement of experienced artisans accelerates the loss of tacit manufacturing knowledge that automation cannot easily replicate.

Efforts to recruit foreign workers and apprentices are helping address gaps but often require 18 to 24 months of onboarding, training, and skills alignment. This lag means labor shortages constrain production scalability in the near term even when investment is committed today. Brands that establish proprietary artisan training programs now will build a structural production advantage that competitors without such programs cannot quickly replicate.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Skilled Artisan & Craft Workforce Attrition | -1.4% | EU (Italy, France, Spain), APAC artisan corridors | Long term (≥ 4 years) |

| Counterfeit Proliferation & Brand Equity Erosion | -1.2% | Global; APAC sourcing, EU & NA consumption markets | Medium–long term (3–5+ years) |

| EUDR & Traceability Compliance Burden | -1.0% | EU core; LATAM, APAC supply origins | Short–medium term (≤3 years) |

| Tariff Volatility & Trade Route Disruption | -0.9% | North America, APAC export corridors, EU | Short–medium term (≤3 years) |

| Vegan & Bio-Leather Consumer Preference Shift | -0.8% | EU, North America, urban APAC (under-35 cohort) | Medium term (2–4 years) |

| Raw Hide Supply Concentration & Price Volatility | -0.7% | APAC tanneries, LATAM sourcing, EU processing hubs | Medium term (2–4 years) |

Opportunities

The circular luxury opportunity is reinforced by measurable shifts in consumer behavior and resale participation. In 2024, 58% of consumers reported purchasing secondhand apparel, up from 56% in 2023, demonstrating continued normalization of resale shopping. Among Gen Z and Millennials, nearly 70% reported buying or selling secondhand products during the year, making resale a key customer acquisition channel for premium brands.

Luxury handbags and leather accessories consistently rank among the highest-value categories in the secondary market due to strong value retention and consumer demand. Industry surveys indicate that more than 60% of luxury consumers consider a brand’s sustainability and circularity efforts when making purchase decisions. Authenticated resale programs attract younger first-time luxury buyers while extending customer lifetime engagement beyond the primary sale cycle.

The growing use of digital product passports and authentication technologies is improving trust, traceability, and participation in brand-owned resale ecosystems. This creates a scalable monetization opportunity beyond primary product sales. Brands that launch owned resale platforms in the short to medium term will control both the primary and secondary revenue stream from each product, compounding lifetime value per unit sold.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Bio-Based & Mycelium Leather Platform Entry | +1.8% | EU, North America, urban APAC | Medium term (2–4 years) |

| Owned Circular Economy & Resale Monetization | +1.5% | North America core, EU, APAC | Short–medium term (≤3 years) |

| Digital Product Passport (DPP) as a Monetization Layer | +1.2% | EU mandate-driven; North America, APAC follow-on | Short term (≤2 years) |

| Men’s Premium & Lifestyle Accessories — Untapped TAM | +2.0% | APAC (India, SE Asia), North America, MEA | Medium–long term (3–5 years) |

| B2B Corporate & Institutional Gifting Vertical | +1.3% | Global; India, GCC, North America core | Short term (≤2 years) |

| M&A Roll-Up of Artisanal & Regional Heritage Brands | +1.6% | Sub-Saharan Africa, LATAM, South & Southeast Asia | Long term (≥4 years) |

Regional Analysis

Asia-Pacific Dominates the Leather Goods Market with a Market Share of 44.5%, Valued at USD 32.83 Billion

Asia-Pacific commands 44.5% of the global leather goods market in 2025, driven by China’s dominant luxury consumption base, India’s expanding premium middle class, and South Korea’s influence on fashion-led accessories demand. Rising disposable incomes and urbanization across the region are converting aspirational consumers into active luxury buyers, concentrating the largest share of leather goods revenue outside Europe.

North America is the second-largest regional market, supported by strong DTC channel penetration, deep influencer-commerce infrastructure, and consumer willingness to pay premiums for authenticated luxury and sustainable products. The region’s concentration of high-net-worth individuals and mature retail ecosystems gives established leather goods brands a structurally stable revenue base, even as aspirational consumer spending softens during inflationary periods.

Europe retains strategic importance as the production and brand heritage center of the global leather goods industry. Italy, France, and Spain house the core manufacturing clusters for ultra-premium leather goods. Regulatory frameworks including EUDR and CITES enforcement are tightening sourcing standards, which disadvantages lower-compliance exporters and reinforces the pricing power of European heritage brands in domestic and export markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

LVMH‘s Fashion and Leather Goods division generated €37.8 Billion in revenue in 2025, holding the group’s largest business segment position. This scale gives LVMH unmatched negotiating power across tanneries, retail channels, and artisan networks. In May 2026, LVMH and WHP Global announced the acquisition of Marc Jacobs, extending their leather goods brand portfolio into a new consumer segment.

Ferragamo demonstrates category focus: leather goods and footwear accounted for 86% of the brand’s €976.5 Million in 2025 sales, with leather sourcing traceability confirmed for more than 80% of materials used. This concentration creates vulnerability to leather market disruptions but also positions Ferragamo as a credibility leader in sustainable and traceable luxury leather, a positioning that resonates with compliance-driven institutional buyers and sustainability-conscious consumers.

Key Players

- LVMH Moët Hennessy Louis Vuitton

- Ferragamo

- Tapestry Inc.

- Caleres Inc.

- Montblanc International

- Kering S.A.

- Capri Holdings

- Hermès International

- Prada Group

- Chanel

Recent Developments

- February 2025 – Caleres signed a definitive agreement to acquire Stuart Weitzman from Tapestry for $105 Million, strengthening its position in the premium footwear and leather accessories segment.

- August 2025 – Caleres completed the Stuart Weitzman acquisition for a net purchase price of approximately $108.7 Million, adding a globally recognized luxury leather footwear brand to its portfolio.

- May 2026 – Ferragamo confirmed traceability for more than 80% of the leather used in its products, significantly expanding its leather supply-chain transparency program.

- March 2026 – Montblanc released the second chapter of its Spring/Summer 2026 Leather Collection, adding the Rectangular Backpack and expanded business-travel leather products to its portfolio.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 72.1 Billion |

| Forecast Revenue (2035) | USD 524 Billion |

| CAGR (2026-2035) | 22.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Genuine Leather, Synthetic Leather, Vegan Leather); By Product (Handbags: Tote Bag, Clutch, Satchel, Others; Small Leather Goods/Accessories: Wallets, Pouches, Phone Covers/Cases, Watch Straps, Others; Apparel; Home Décor and Furnishing; Pet Accessories: Pet Collar and Leads, Leather Pet Toys; Automotive Accessories: Seating Systems, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | LVMH Moët Hennessy Louis Vuitton, Ferragamo, Tapestry Inc., Caleres Inc., Montblanc International, Kering S.A., Capri Holdings, Hermès International, Prada Group, Chanel |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |