Global Fly Ash Market Size, Share, Report Analysis By Product Type (Class F and Class C), By Applications (Cement and Concrete, Bricks and Blocks, Road Construction, Soil Stabilization, Mining, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Aug 2025

- Report ID: 156663

- Number of Pages: 249

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overviews

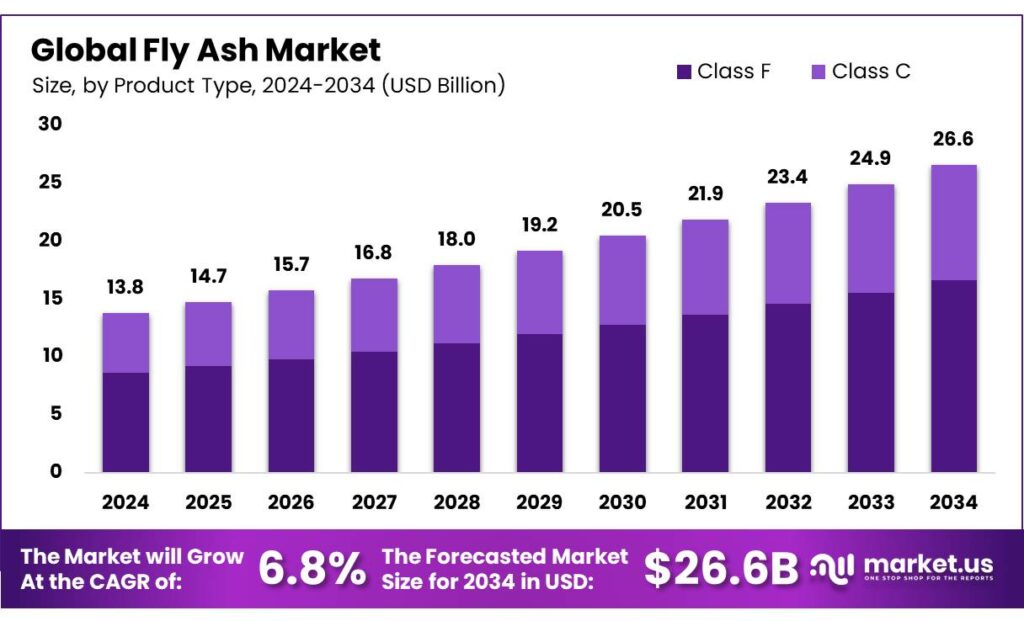

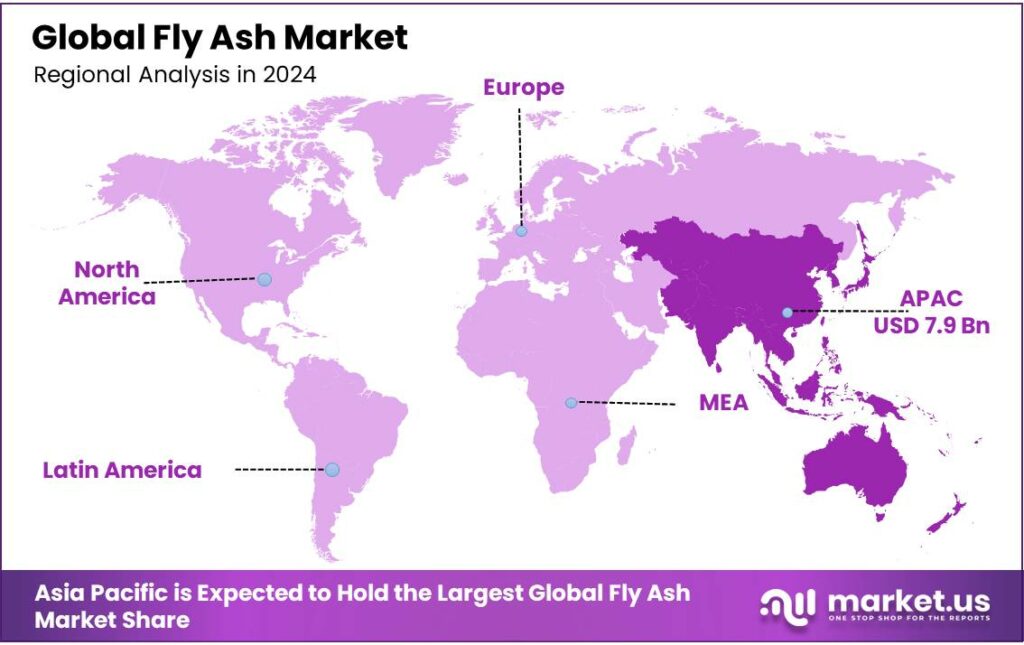

The Global Fly Ash Market size is expected to be worth around USD 26.6 Billion by 2034, from USD 13.8 Billion in 2024, growing at a CAGR of 6.8% during the forecast period from 2025 to 2034. In 2024, Asia Pacific held a dominant market position, capturing more than a 57.4% share, holding USD 7.9 Billion revenue.

Fly ash is a fine, powdery byproduct of burning coal in power plants composed of silica, alumina, iron oxide, and other trace elements. Fly ash is widely used in concrete as a partial replacement for portland cement, improving its strength, durability, and workability. Additionally, it is used in asphalt, soil stabilization, and other construction applications. The major driver of the fly ash market is the construction industry, particularly cement and concrete. The most used type of fly ash is the class F.

There is a global shift towards sustainable practices, including construction. Fly ash is highly hazardous if leaked into water bodies. There are several government initiatives that encourage the productive applications of fly ash. These government initiatives create opportunities in the market. However, as the demand for renewable energy sources increases and countries try to phase out of the coal market, there is a deficient supply of fly ash in the market.

- According to the International Energy Agency (IEA), global coal demand hit a record high of nearly 9 billion tons in 2024, fueled by increased electricity generation from coal, particularly in China and India.

Key Takeaways

- The global fly ash market was valued at USD 13.8 billion in 2024.

- The global fly ash market is projected to grow at a CAGR of 6.8% and is estimated to reach USD 26.6 billion by 2034.

- Based on product types, fly ash that belongs to class F dominated the market in 2024, comprising about 58.2% share of the total global market.

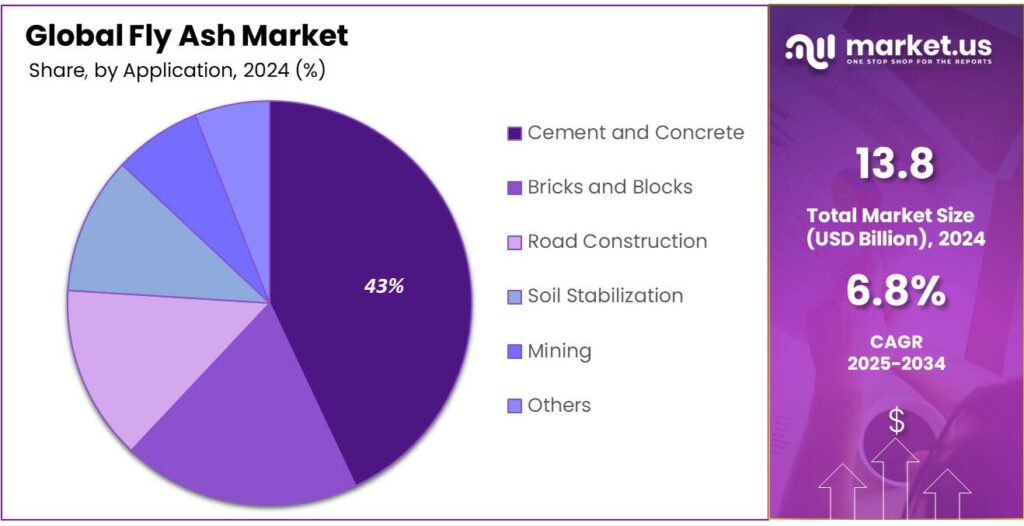

- Among the applications of fly ash, the cement and concrete manufacturing industry dominated the market in 2024, accounting for around 43.1% of the market share.

- Asia Pacific was the largest market for fly ash in 2024 due to its rapidly expanding construction and infrastructure industry.

Product Type Analysis

Fly Ash that Belongs to Class F Dominated the Market Due to Its Chemical Properties.

On the basis of product type, the fly ash market is segmented into class F and class C. Class F of fly ash dominated the market in 2024 with a market share of 58.2%. Class F fly ash often dominates usage over Class C due to its favorable chemical and durability characteristics. Containing low calcium, typically less than 10%, and rich in silica, alumina, and iron oxide, Class F exhibits strong pozzolanic activity, forming cementitious compounds when activated with lime or cementitious binders.

This composition grants it excellent resistance to sulfate corrosion and alkali–silica reaction, making it suitable for concrete in harsh environments. Although Class C contains higher calcium oxide, over 20-30%, and can self-cement, providing early strength gain, its higher alkalis and sulfate content can be less favorable in aggressive environments. Additionally, the self-hardening nature of Class C may limit mix flexibility and require stricter control in long-term durability-sensitive projects.

Application Analysis

In 2024, the Cement and Concrete Industry Dominated the Fly Ash Market.

In 2024, the cement and concrete industry emerged as the largest end-use sector for fly ash, accounting for nearly 43.1% of the product’s global consumption, outperforming sectors such as cement and concrete, bricks and blocks, road construction, soil stabilization, and mining. The dominance is attributed to the role of fly ash as a supplementary cementitious material, known for improving workability, reducing heat of hydration, and enhancing durability by refining pore structure and resisting chemical attacks.

Such features of fly ash make this sector especially reliant on it for producing blended cements and high-performance concrete, particularly in large-scale projects like roller-compacted concrete dams, where fly ash helps mitigate thermal cracking and optimize structural integrity. By contrast, other applications, such as bricks and blocks, road embankments, soil stabilization, and mining, collectively occupy smaller shares of utilization. The bricks and blocks benefit from fly ash’s pozzolanic properties, and uses in soil stabilization and mining are valuable for land reclamation and environmental restoration.

Key Market Segments

By Product Type

- Class F

- Class C

By Application

- Cement and Concrete

- Bricks and Blocks

- Road Construction

- Soil Stabilization

- Mining

- Others

Drivers

Demand for Fly Ash for the Construction Industry Drives the Market.

The construction sector serves as the principal lifeline of the fly ash market, owing to its proven enhancement of concrete properties and versatile applications. Worldwide, more than 95% of all fly ash consumption is tied directly to construction uses such as cement replacement, bricks, soil stabilization, and road embankments. In concrete production, fly ash frequently replaces up to 30% of Portland cement by mass, improving durability, reducing permeability, and lowering water demand, while in mass concrete settings like dams and pavements, these replacement levels can reach 70%.

For instance, India’s Ghatghar dam project in Maharashtra, where processed fly ash achieved 70% substitution in roller-compacted concrete, significantly reduced thermal cracking risks. Fly ash bricks, made from a mix of fly ash, sand, and cement, are up to 20% cheaper than traditional clay bricks, while also saving energy and reducing mercury emissions. Furthermore, blending fly ash with fine aggregates can enhance workability and compressive strength, creating opportunities for more sustainable non-structural construction applications.

Restraints

Shift Towards Renewable Energy Sources Might Hamper the Growth of the Fly Ash Market.

The global shift toward renewable energy sources might threaten the fly ash market by reducing its supply. Fly ash is a byproduct of burning coal for energy; however, as the world moves away from fossil fuels, the supply of this essential ingredient for concrete production is dwindling. For instance, many EU countries have committed to phasing out coal power by 2030, aligning with the EU’s climate targets. In April 2025, Finland’s last coal-fired power and heat plant was shut down.

The phasing out of coal-fired power plants signifies that less fly ash is being produced. The shrinking supply, combined with steady demand from the construction industry, has led to increased prices for fly ash. This price volatility makes it less economically viable for some projects. With a decreasing number of coal plants producing fly ash, the consistency and quality of the remaining supply can be unreliable. This variability is a challenge for construction processes that rely on standardized materials.

Opportunity

Government Initiatives Create Opportunities in the Fly Ash Market.

Governments in many countries are proactively catalyzing the fly ash market through a spectrum of regulatory mandates and supportive policies. For instance, in India, under the amendments of the Environment Protection Act, the government has steadily tightened norms, which require coal- and lignite-based thermal power plants (TPPs) to achieve 100% fly ash utilization, with penalties of INR1,000 per ton for non-compliance. Additionally, fly ash is to be made available free or at a nominal cost to end-users.

Initiatives such as the Ash Track portal bolster transparency by open-sourcing fly ash availability and contact details of power plants. Similarly, several companies try to communicate with the government to subsidize the activities in the industry.

For instance, in April 2025, Ashtech India, with the support of other leading cement companies, power plants, and various industry stakeholders, appealed to the government, resulting in a 40% discount for the transportation of fly ash/bed ash via railways, officially recognized by the Ministry of Railways.

Trends

Shift Towards Sustainable Construction Practices.

The rising embrace of sustainable construction is transforming the fly ash market into a key enabler of greener building practices. For instance, in the U.S., big commercial projects, such as the LBC-certified (Living Building Challenge) Bullitt Center, showcase fly ash in high-performance concrete and earn green‑building credits.

Similarly, in India, NTPC’s pioneering eco‑house in Bilaspur, composed of approximately 80% fly ash blocks, reduces carbon emissions by around 75% compared to conventional homes and features modular, interlocking components that eliminate the need for sand, cement, or steel. Globally, cities are adopting circular economy principles, highlighting vast potential for waste‑repurposing in construction.

However, out of nearly 100 million tons of fly ash generated annually, only about 30% is currently reused. Moreover, eco‑conscious builders value fly‑ash bricks for their 20% lower production cost, enhanced strength, and energy‑saving ambient‐curing methods.

Geopolitical Impact Analysis

Geopolitical Tensions Leading to Supply Chain Disruptions in the Fly Ash Market.

Geopolitical tensions have increasingly rippled through the global fly ash market, disrupting supply chains and stirring regional price divergence. According to IEA, the rebound from lows during the pandemic, underpinned by high gas prices in the aftermath of Russia’s full-scale invasion of Ukraine, has resulted in record global coal production, consumption, trade, and coal-fired power generation in recent years. Due to this, there is a steady production of fly ash.

However, due to geopolitical instability in key maritime routes such as the Red Sea, there were delays in key markets of North America, leading to price hikes. Similarly, Southeast Asia saw falling prices due to destocking amid weak demand, compounded by logistical snarls intensified by regional shipping bottlenecks. Similarly, the European markets often bridge supply shortfalls through imports from regions such as South Africa. Geopolitical disruptions, such as contested sea lanes and shifting regulatory frameworks, are compelling companies to restructure their supply chains and diversify them.

Regional Analysis

Asia Pacific is the Major Consumer in the Global Fly Ash Market in 2024.

Asia Pacific held the major share of the global fly ash market, led by China and India, valued at around US$ 7.92 billion. The Asia‑Pacific region emerged as the major global fly ash market, commanding an estimated 57.4% of total revenue share. This dominance stems from a robust coal-based energy infrastructure and fast‑paced urbanization, notably across China, India, Indonesia, and Vietnam, where large volumes of fly ash are generated and channeled into cement, concrete, bricks, and road projects.

- According to the International Energy Agency (IEA), the most significant increase in demand in 2024 is in India, up 70 metric tons, and China, up 56 metric tons, together with others like Indonesia and Vietnam.

China, the world’s largest coal consumer, accounted for over 56%, 4.8 billion metric tons of coal, of global demand in 2023. As the region produces most fly ash, to avoid its accumulation in the dump fills many government initiatives in these countries focus on the management of fly ash.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

There are several global key players in the fly ash market, such as Boral Limited, Charah Solutions, CEMEX S.A.B., LafargeHolcim, Ashtech, Separation Technologies, Cement Australia Holdings, Salt River Materials Group, and Ash Grove Cement Company. As the fly ash market is very niche, many players put efforts into strategic activities, such as product development, mergers, partnerships, and investments. For instance, in January 2022, leading cement supplier Ash Grove Cement, a CRH Company (formerly Suwannee American Cement in Florida), unveiled its state-of-the-art ship unloader with its shipment of FDOT-approved fly ash to its Port Manatee deep water import terminal.

Charah Solutions provides comprehensive fly ash management, from recycling and marketing to beneficiation technologies that improve fly ash quality for concrete and cement manufacturing. This approach reduces the need for landfill disposal, conserves natural resources, and offers environmental benefits for power plants and concrete producers.

CEMEX, a global building materials company, incorporates fly ash into its blended cements and Vertua low-carbon concrete products as a supplementary cementitious material (SCM) to improve concrete performance and reduce embodied carbon, thereby supporting sustainability goals and green building certifications. Ash Grove Cement Company utilizes fly ash, a byproduct of coal-burning power plants, to enhance their cement products and promote sustainable practices in the construction industry.

The major players in the industry

- Boral Ltd.

- Charah Solutions

- CEMEX S.A.B de C.V.

- Lafarge Holcim Ltd.

- Ashtech (India) Pvt. Ltd.

- Separation Technologies LLC

- Cement Australia Holdings Pty Ltd.

- Salt River Materials Group

- Ash Grove Cement Company

- Dirk Group

- Other Key Players

Key Developments

- In March 2024, Holcim North America, a leader in sustainable building materials, announced the introduction of ECO-Ash, beneficiated ash within its Lafarge Western Canada operations. It stands as a high-quality, specification-grade Type F fly ash reclaimed from landfills and transformed into a valuable resource for enhancing cement and concrete construction applications.

- In September 2023, Cardinal Operating Company, a leader in the coal electricity market, collaborated with Separation Technologies, producer of premier cement and building materials by Titan, to market fly ash produced by the plant. The deal gives Separation Technologies exclusive rights to the recycling of Cardinal’s fly ash and eliminates the need for keeping the fly ash in a landfill.

Report Scope

Report Features Description Market Value (2024) USD 13.8 Bn Forecast Revenue (2034) USD 26.6 Bn CAGR (2025-2034) 6.8% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Class F, Class C), By Applications (Cement and Concrete, Bricks and Blocks, Road Construction, Soil Stabilization, Mining, Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape Boral Limited, Charah Solutions, CEMEX S.A.B de C.V., LafargeHolcim Ltd., Ashtech (India) Pvt. Ltd., Separation Technologies LLC, Cement Australia Holdings Pty Ltd., Salt River Materials Group, Ash Grove Cement Company, Dirk Group, Other Key Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Boral Ltd.

- Charah Solutions

- CEMEX S.A.B de C.V.

- Lafarge Holcim Ltd.

- Ashtech (India) Pvt. Ltd.

- Separation Technologies LLC

- Cement Australia Holdings Pty Ltd.

- Salt River Materials Group

- Ash Grove Cement Company

- Dirk Group

- Other Key Players

Our Clients

- 156663

- Aug 2025