Global Ethylene Amines Market Size, Share, And Industry Analysis Report By Type (Ethylenediamine (EDA), Diethylenetriamine (DETA), Triethylenetetramine (TETA), Piperazine (PIP), Others), By Application (Epoxy Curing Agents, Fuel Additives, Corrosion Inhibitors, Polyamide Resins, Surfactants, Rubber Chemicals, Others), By End-Use (Automotive, Personal Care and Cosmetics, Pulp and Paper, Aerospace and Defense, Adhesives, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 179912

- Number of Pages: 398

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

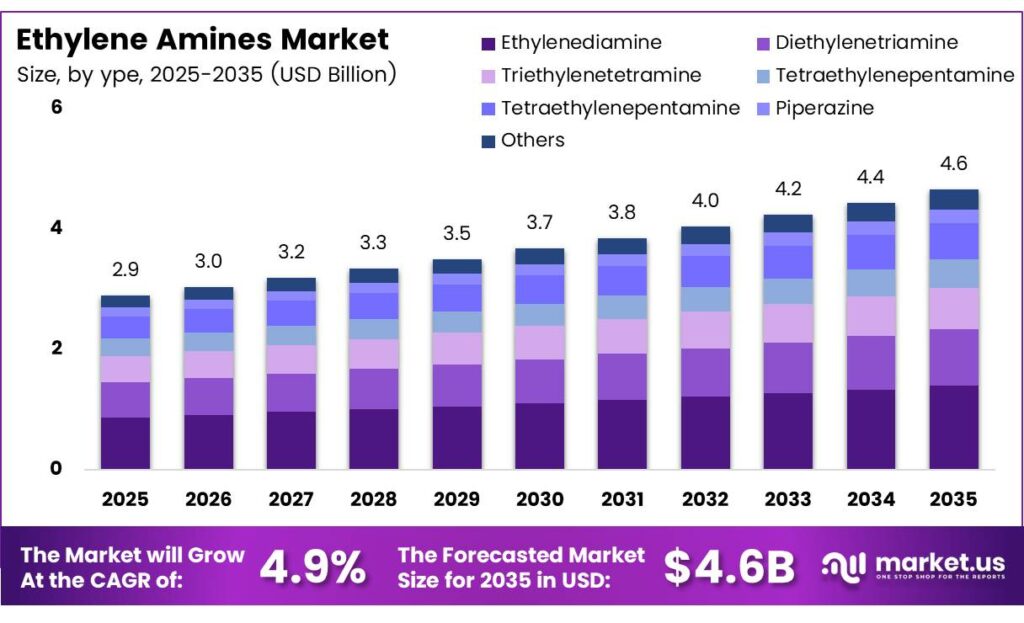

The Global Ethylene Amines Market size is expected to be worth around USD 4.6 billion by 2035 from USD 2.9 billion in 2025, growing at a CAGR of 4.9% during the forecast period 2026 to 2035.

Ethylene amines are a group of chemical compounds derived from ethylene dichloride or monoethanolamine. These compounds include ethylenediamine, diethylenetriamine, triethylenetetramine, and higher analogs. Industries use them widely as building blocks in resins, coatings, agrochemicals, and pharmaceuticals.

The market serves a broad range of end-use sectors. Manufacturers supply ethylene amines to automotive, aerospace, oil and gas, and personal care industries. Moreover, their role as curing agents for epoxy systems and as fuel additive components makes them essential to both industrial and consumer product formulations.

- Global exports of ethylenediamine and its salts reached a value of $907.7 million and a shipped quantity of 289.4 million kilograms, providing a clear measure of international trade flows. This volume signals robust and sustained industrial demand across key importing regions.

Government initiatives supporting green chemistry and low-emission manufacturing are reshaping the market. Regulatory bodies in the EU and North America push producers toward sustainable production pathways. Consequently, bio-based ethylene amines and biomass-balanced variants are gaining commercial traction across Europe and North America.

- The United States plays a significant role in global supply. The US exported $78.7 million of ethylenediamine and its salts, capturing an 8.67% share of global export value. This reflects the strength of North America’s chemical intermediates production base and its integration into global value chains.

Investment in carbon capture technologies is also driving demand for amine-blend solvents. Energy companies and industrial players adopt amine-based systems for CO2 scrubbing at scale. Additionally, wind energy blade manufacturers rely on epoxy curing agents derived from ethylene amines, linking the market’s growth directly to renewable energy expansion.

Key Takeaways

- The Global Ethylene Amines Market is valued at USD 2.9 billion in 2025 and is projected to reach USD 4.6 billion by 2035, at a CAGR of 4.9% during the forecast period 2026 to 2035.

- Ethylenediamine (EDA) dominates the market with a 29.4% share in 2025.

- Epoxy Curing Agents hold the leading position with a 22.6% share.

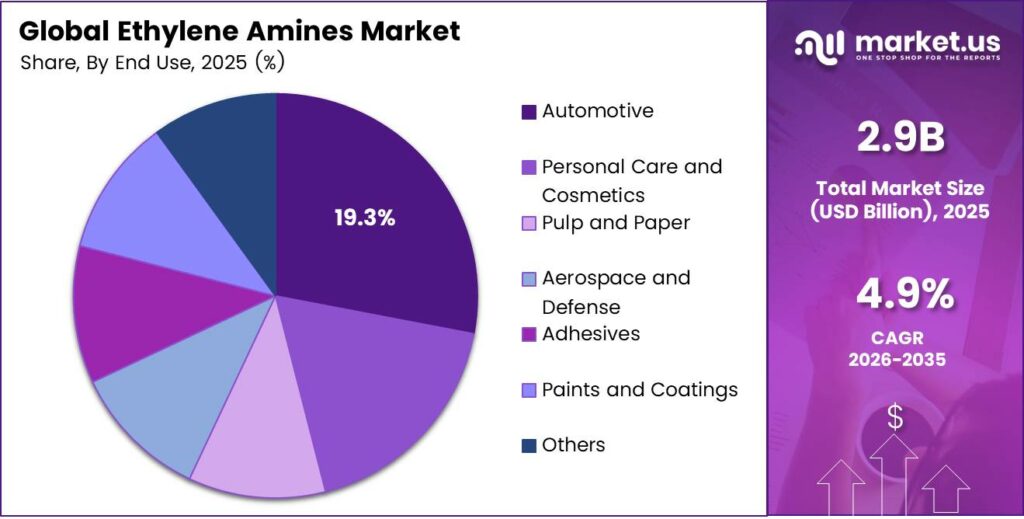

- The Automotive segment leads with a 19.3% market share.

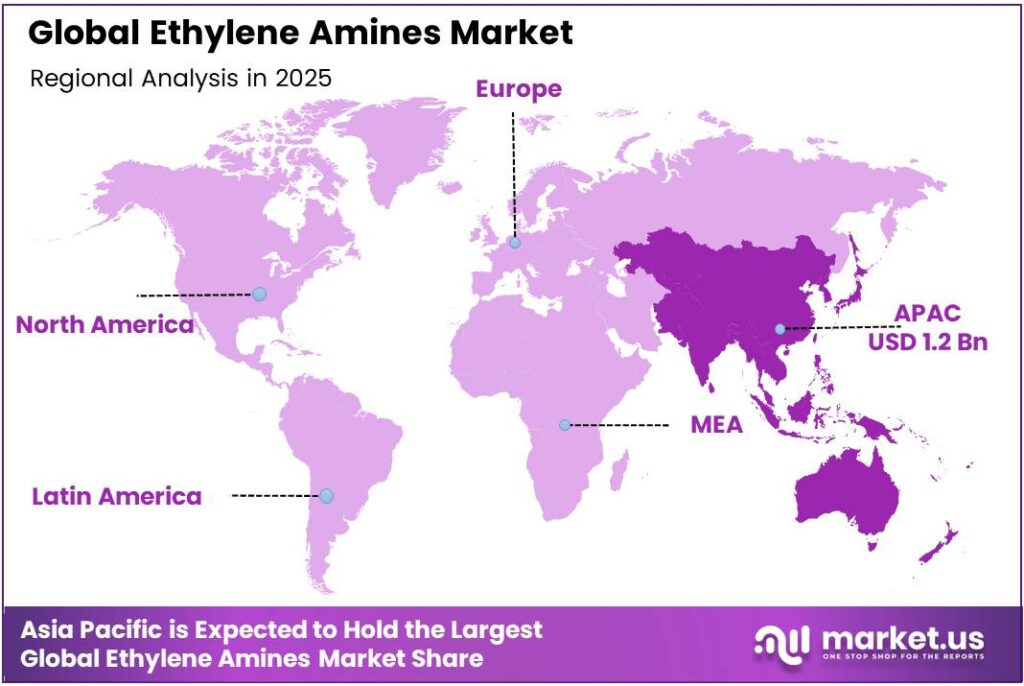

- Asia Pacific dominates the regional landscape with a 41.9% share, valued at USD 1.2 billion.

By Type Analysis

Ethylenediamine (EDA) dominates with 29.4% due to its broad application across epoxy curing, agrochemicals, and chelating agent production.

In 2025, Ethylenediamine (EDA) held a dominant market position in the By Type segment of the Ethylene Amines Market, with a 29.4% share. EDA serves as the primary building block for downstream amines and finds extensive use in epoxy hardeners and lube oil additives. Its versatility drives consistent demand across multiple end-use industries globally.

Diethylenetriamine (DETA) holds a notable share in the type segment. Manufacturers use DETA in fuel additive formulations and as a curing agent for epoxy systems. Additionally, it plays a role in paper wet-strength resin production. However, its demand remains more concentrated than EDA across end-use industries.

Triethylenetetramine (TETA) serves specialized applications in the ethylene amines market. Producers supply TETA primarily for epoxy curing in aerospace and marine coatings. Moreover, it finds use in rubber chemical formulations. Consequently, its demand correlates closely with construction and industrial maintenance activity globally.

Tetraethylenepentamine (TEPA) occupies a niche but growing position in the type segment. Industries apply TEPA in oil and gas demulsifier formulations and fuel additive packages. Its complex molecular structure offers specific performance properties that standard amines cannot replicate in high-demand industrial environments.

Heavy Polyamide (HPA) and Piperazine (PIP) round out the type segment with distinct application profiles. HPA supports adhesive and coating formulations, while PIP serves pharmaceutical and chemical intermediate uses. Both sub-segments contribute to diversified demand that strengthens the overall ethylene amines market.

By Application Analysis

Epoxy Curing Agents dominate with 22.6% due to high consumption in wind energy, aerospace, and construction sectors.

In 2025, Epoxy Curing Agents held a dominant market position in the By Application segment of the Ethylene Amines Market, with a 22.6% share. Wind energy blade manufacturers, automotive OEMs, and construction material producers all rely heavily on amine-based curing agents. This widespread adoption across high-growth industries sustains the segment’s leading position.

Fuel Additives represent the second major application for ethylene amines. Refiners and lubricant manufacturers incorporate amines into fuel packages to enhance combustion efficiency and engine protection. Moreover, stricter emission norms globally push fuel additive producers to optimize amine chemistry for cleaner performance standards.

Corrosion Inhibitors and Polyamide Resins together form a significant application cluster. Oil and gas operators and pipeline companies consume amine-based corrosion inhibitors to protect infrastructure. Additionally, polyamide resin producers use ethylene amines as key raw materials for engineering plastics and coatings applications.

Surfactants and Chelating Agents serve important roles in personal care, detergents, and industrial cleaning. Formulators use amine-derived surfactants for emulsification and foaming properties. Consequently, growth in home care and industrial cleaning product demand supports steady consumption of ethylene amines in this application segment.

Bleach Activators, Ion Exchange Resins, Fungicides, and Rubber Chemicals collectively address specialized industrial and agricultural needs. Agrochemical producers and water treatment companies consume ethylene amines for these targeted applications. The diversity of uses reduces market concentration risk and supports long-term demand stability.

By End-Use Analysis

Automotive dominates with 19.3% due to high consumption of fuel additives, coatings, and adhesive formulations.

In 2025, Automotive held a dominant market position in the By End-Use segment of the Ethylene Amines Market, with a 19.3% share. Vehicle manufacturers consume ethylene amines in fuel additive packages, corrosion inhibitors, and structural adhesives. Moreover, the transition to electric vehicles introduces new applications in battery component formulations and thermal management systems.

Personal Care and Cosmetics represent a fast-growing end-use sector for ethylene amines. Formulators rely on amine-based surfactants and conditioning agents for hair care and skin care products. Additionally, the premiumization trend in personal care markets globally drives demand for high-performance amine-derived ingredients.

Pulp and Paper and Aerospace and Defence segments serve distinct but important roles in total ethylene amines consumption. Pulp mills use wet-strength resins derived from amines, while aerospace manufacturers depend on high-performance epoxy curing agents. Consequently, both sectors generate stable, long-term demand for specific amine grades.

Adhesives and coatings together form a significant industrial end-use cluster. Construction activity and automotive refinishing drive consumption of amine-cured adhesive and coating systems. Furthermore, the growing waterborne coatings market expands the use of amine hardeners as environmentally preferred alternatives to solvent-based systems.

Agro Chemicals, Pharmaceutical and Healthcare, and Oil and Gas complete the end-use landscape. Agrochemical producers use ethylene amines in herbicide and fungicide synthesis. Pharmaceutical companies consume amine intermediates for active ingredient manufacturing. Oil and gas operators apply amines in refinery and pipeline operations globally.

Key Market Segments

By Type

- Ethylenediamine (EDA)

- Diethylenetriamine (DETA)

- Triethylenetetramine (TETA)

- Tetraethylenepentamine (TEPA)

- Heavy Polyamide (HPA)

- Piperazine (PIP)

- Others

By Application

- Epoxy Curing Agents

- Fuel Additives

- Corrosion Inhibitors

- Polyamide Resins

- Surfactants, Chelating Agents

- Bleach Activators

- Ion Exchange Resins

- Fungicides

- Rubber Chemicals

- Others

By End-Use

- Automotive

- Personal Care and Cosmetics

- Pulp and Paper

- Aerospace and Defense

- Adhesives

- Paints and Coatings

- Agro Chemicals

- Pharmaceutical and Healthcare

- Oil and Gas

- Others

Emerging Trends

Low-Carbon Production and Capacity Shifts Reshape the Global Ethylene Amines Landscape

Producers across the ethylene amines industry are shifting toward low-carbon and biomass-balanced production pathways. Chemical companies in Europe and North America invest in greener feedstocks to meet sustainability targets. Consequently, this transition is redefining supply structures and competitive positioning across major producing regions.

- Capacity rationalization characterizes Europe, while new investments accelerate in Asia. Companies in China and Saudi Arabia commission large-scale plants to capture growing regional demand. A major Chinese petrochemical complex reported a capacity to produce 1,600,000 metric tons per year of amines, including ethyleneamines, illustrating the scale of new Asian supply entering global markets.

Regulatory shifts further accelerate the adoption of sustainable and low-emission chemical processes. Governments in the EU and Asia mandate tighter environmental standards for chemical producers. Additionally, the integration of ethylene amines into eco-friendly formulations for coatings, detergents, and water treatment aligns with broader industry decarbonization goals.

Drivers

Booming Epoxy Resin Demand and Carbon Capture Adoption Drive Ethylene Amines Market Growth

Wind energy expansion directly fuels demand for ethylene amines as epoxy curing agents. Blade manufacturers require high-performance amine hardeners to produce structurally sound, lightweight composite materials. Moreover, global renewable energy investment continues to accelerate, creating sustained long-term consumption of amine-cured epoxy systems at an industrial scale.

- Carbon capture projects adopt amine-blend solvents to absorb CO2 from industrial emissions. Energy companies and power generators increasingly deploy these systems to meet regulatory carbon reduction targets. According to WITS trade data, Belgium exported $104.4 million worth of ethylenediamine and its salts, reflecting strong European production capacity serving both domestic and export amine demand.

Agrochemical and waterborne coatings sectors expand their use of ethylene amines as functional intermediates. Formulators increasingly adopt amine-derived surfactants for herbicide and fungicide formulations. Additionally, the growing automotive lubricant and fuel additive market in Asia and the Middle East drives rising consumption of higher-grade ethylene amine products across downstream industries.

Restraints

Volatile Raw Material Prices and Stringent Regulations Limit Ethylene Amines Market Profitability

Volatile raw material prices present a persistent challenge for ethylene amines producers. Ethylene dichloride and monoethanolamine feedstock costs fluctuate with crude oil and natural gas price movements. BASF Group reported sales of €59,657 million in 2025 versus €68,902 million in 2023, a two-year contraction reflecting the impact of input cost pressures and softer pricing on major amine producers.

Stringent environmental regulations increase operational complexity for chemical manufacturers. Producers must invest in emissions control systems, waste treatment infrastructure, and compliance reporting. Moreover, European chemical regulations under REACH impose additional testing and documentation requirements on ethylene amine producers, raising the cost burden for smaller and mid-sized market participants.

New market entrants face high capital barriers linked to plant construction and environmental permitting. However, established producers also face pressure to retrofit existing facilities to meet evolving standards. Consequently, these combined cost and regulatory factors compress margins across the ethylene amines value chain and slow the pace of new capacity additions in regulated markets.

Growth Factors

Bio-Based Applications and Electric Vehicle Integration Accelerate Ethylene Amines Market Expansion

Bio-based surfactants and chelating agents represent a high-growth application frontier for ethylene amines. Consumer goods and industrial cleaning product companies seek plant-derived amine alternatives to replace petrochemical-based ingredients.

Electric vehicle battery systems create new demand for specialty amine chemistries. Manufacturers integrate amine-based compounds in battery electrolyte formulations, thermal management systems, and adhesive materials. Consequently, the rapid global EV adoption curve opens a structurally new end-use channel for ethylene amine producers that did not exist in prior market cycles.

Water treatment and lubricant additive demand across the Asia Pacific drives volume growth for ethylene amines. Governments in India, China, and Southeast Asia invest in industrial water treatment infrastructure. Moreover, pharmaceutical and personal care formulation growth in these emerging markets further expands the consumption base for amine intermediates across multiple high-value application segments.

Regional Analysis

Asia Pacific Dominates the Ethylene Amines Market with a Market Share of 41.9%, Valued at USD 1.2 Billion

Asia Pacific leads the global ethylene amines market with a 41.9% share, valued at USD 1.2 billion in 2025. China, India, Japan, and South Korea anchor regional consumption through strong demand from the automotive, agrochemical, and coatings industries. Moreover, Nouryon Chemicals India Private Limited reported for the financial year ending March 2025, reflecting robust specialty amine sales in the Indian subcontinent.

North America maintains a strong position in the global ethylene amines trade and consumption. The United States supports demand through its wind energy, oil and gas, and advanced coatings industries. Furthermore, North American producers continue to invest in higher-value amine grades to serve specialty chemical end markets and sustain export competitiveness.

Europe holds a significant share in global ethylene amines production and trade. The European Union exported ethylenediamine and its salts. However, capacity rationalization and energy cost pressures continue to reshape the European competitive landscape.

Latin America represents an emerging growth region for ethylene amines consumption. Brazil and Mexico drive demand through expanding agrochemical, automotive, and personal care sectors. Additionally, infrastructure investment and rising industrial output across the region create incremental demand for corrosion inhibitors, fuel additives, and epoxy curing systems derived from ethylene amines.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Akzo Nobel N.V. operates as a global specialty chemicals and coatings company with a significant presence in amine-derived product lines. The company leverages its integrated chemicals platform to serve epoxy curing, surfactant, and corrosion inhibitor markets. Its strong distribution network and R&D investment position it as a leading supplier of amine-based specialty inputs across European and global industrial markets.

BASF S.E. stands as one of the world’s largest chemical producers with a comprehensive ethylene amines portfolio. The company supplies EDA, DETA, TETA, and higher polyamines to automotive, oil and gas, and coatings industries. Dow’s Industrial Intermediates & Infrastructure segment, while BASF continues to expand its amines capacity through strategic facility investments in Europe.

Dow maintains a major position in ethylene amines through its Industrial Solutions business within the Industrial Intermediates & Infrastructure segment. The company supplies amine intermediates for fuel additives, corrosion inhibitors, and epoxy curing applications. Dow’s global manufacturing footprint and customer partnerships with automotive and energy sector clients reinforce its competitive strength across the ethylene amines value chain.

Delamine BV, a dedicated ethyleneamines producer based in Delfzijl, Netherlands, focuses exclusively on the production and supply of EDA-based amines. Delamine’s Delfzijl facility operates with a nameplate capacity, positioning it as one of Europe’s key dedicated ethyleneamines production sites. Its specialization and scale support reliable regional and export supply.

Top Key Players in the Market

- Akzo Nobel N.V.

- Alkyl Amines Chemicals Ltd.

- Arabian Amines Company

- Arkema

- BALAJI SPECIALITY CHEMICALS LIMITED

- BASF S.E

- Delamine BV

- Diamines and Chemicals Ltd.

- Dow

- Eastman Chemical Company

- Evonik Industries

Recent Developments

- In 2025, Alkyl Amines reported modest top-line growth amid significant volume increases in aliphatic amines and derivatives, though offset by price drops. Raw material costs also declined, leading to mixed margin impacts. The company anticipates further growth, with ongoing price pressures but positive volume trends in the chemical sector.

- In 2025, Akzo Nobel’s specialty chemicals business, rebranded as Nouryon since 2018, has focused on sustainable advancements in ethylene amines. Nouryon obtained ISCC PLUS certification for the production of green ethylene oxide, ethanolamines, and ethylene amines at its facilities in Stenungsund, Sweden, and Ningbo, China.

Report Scope

Report Features Description Market Value (2025) USD 2.9 Billion Forecast Revenue (2035) USD 4.6 Billion CAGR (2026-2035) 4.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Ethylenediamine (EDA), Diethylenetriamine (DETA), Triethylenetetramine (TETA), Tetraethylenepentamine (TEPA), Heavy Polyamide (HPA), Piperazine (PIP), Others), By Application (Epoxy Curing Agents, Fuel Additives, Corrosion Inhibitors, Polyamide Resins, Surfactants, Chelating Agents, Bleach Activators, Ion Exchange Resins, Fungicides, Rubber Chemicals, Others), By End-Use (Automotive, Personal Care and Cosmetics, Pulp and Paper, Aerospace and Defense, Adhesives, Paints and Coatings, Agro Chemicals, Pharmaceutical and Healthcare, Oil and Gas, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Akzo Nobel N.V., Alkyl Amines Chemicals Ltd., Arabian Amines Company, Arkema, BALAJI SPECIALITY CHEMICALS LIMITED, BASF S.E, Delamine BV, Diamines and Chemicals Ltd., Dow, Eastman Chemical Company, Evonik Industries Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Akzo Nobel N.V.

- Alkyl Amines Chemicals Ltd.

- Arabian Amines Company

- Arkema

- BALAJI SPECIALITY CHEMICALS LIMITED

- BASF S.E

- Delamine BV

- Diamines and Chemicals Ltd.

- Dow

- Eastman Chemical Company

- Evonik Industries

Our Clients

- 179912

- March 2026