Global Dog Food Market Size, Share, And Industry Analysis Report By Type (Dry Food, Wet Food, Snacks/Treats), By Life Stage (Adult, Puppy, Senior), By Product Type (Dry Dog Food, Wet Dog Food, Raw Dog Food, Freeze-Dried Dog Food), By Ingredient Type (Meat-Based, Vegetarian, Grain-Free, Organic), By Distribution Channel (Supermarkets and Hypermarkets, Specialty Stores, Online), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182402

- Number of Pages: 255

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- By Type Analysis

- By Life Stage Analysis

- By Product Type Analysis

- By Ingredient Type Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Emerging Trends

- Drivers

- Restraints

- Growth Factors

- Regional Analysis

- Key Regions and Countries

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

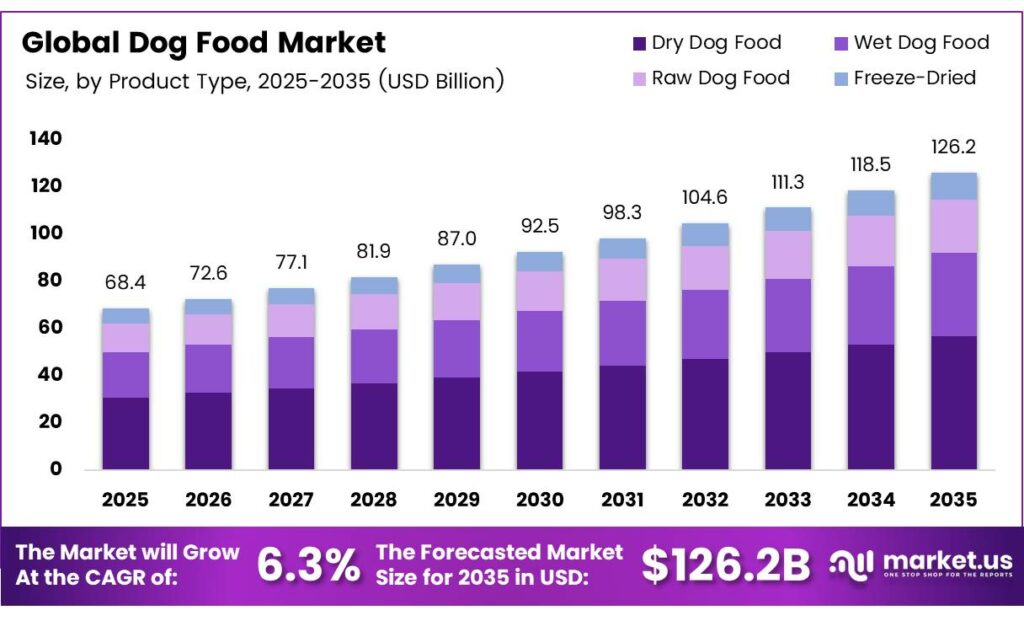

The Global Dog Food Market size is expected to be worth around USD 126.2 billion by 2035 from USD 68.4 billion in 2025, growing at a CAGR of 6.3% during the forecast period 2026 to 2035.

The dog food market covers all commercially manufactured food products for dogs, including dry kibble, wet food, raw diets, freeze-dried options, and functional treats. Manufacturers develop these products across life stages, such as puppy, adult, and senior, as well as breed-specific and condition-targeted formulations. Consequently, the market serves a wide range of consumer needs and preferences globally.

Pet humanization remains the strongest behavioral trend shaping this market. Dog owners increasingly treat their pets as family members, which drives demand for high-quality, nutritionally complete, and natural food options. Moreover, growing awareness of pet health conditions such as obesity, allergies, and joint problems pushes owners toward functional and ingredient-conscious diets.

Pet humanization remains the strongest behavioral trend shaping this market. Dog owners increasingly treat their pets as family members, which drives demand for high-quality, nutritionally complete, and natural food options. Moreover, growing awareness of pet health conditions such as obesity, allergies, and joint problems pushes owners toward functional and ingredient-conscious diets.The United States dog food market sales reached $40.9 billion in 2025, reflecting a 3.9% increase driven by premiumization and higher spending per pet. This trend confirms that North American dog owners consistently prioritize quality nutrition, making the region a critical growth engine for the global market.

The European Union and the Asia Pacific regions actively regulate dog food safety standards, labeling requirements, and ingredient sourcing. Regulatory frameworks such as AAFCO guidelines in the U.S. drive product quality compliance and support consumer confidence. Therefore, regulatory alignment creates a strong foundation for premium product expansion globally.

Key Takeaways

- The Global Dog Food Market is valued at USD 68.4 billion in 2025 and is projected to reach USD 126.2 billion by 2035 at a CAGR of 6.3% during the forecast period 2026 to 2035.

- Dry Food dominates with a 48.6% market share in 2025.

- Adult holds the leading position with a 67.3% share in 2025.

- Dry Dog Food leads with a 54.1% market share in 2025.

- Meat-Based formulations dominate with a 59.4% share in 2025.

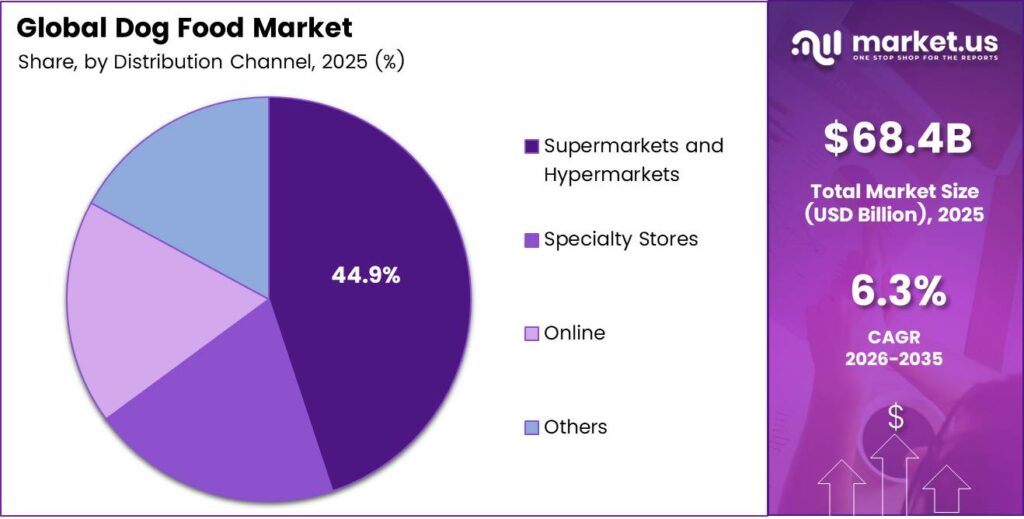

- Supermarkets and Hypermarkets hold the largest share at 44.9% in 2025.

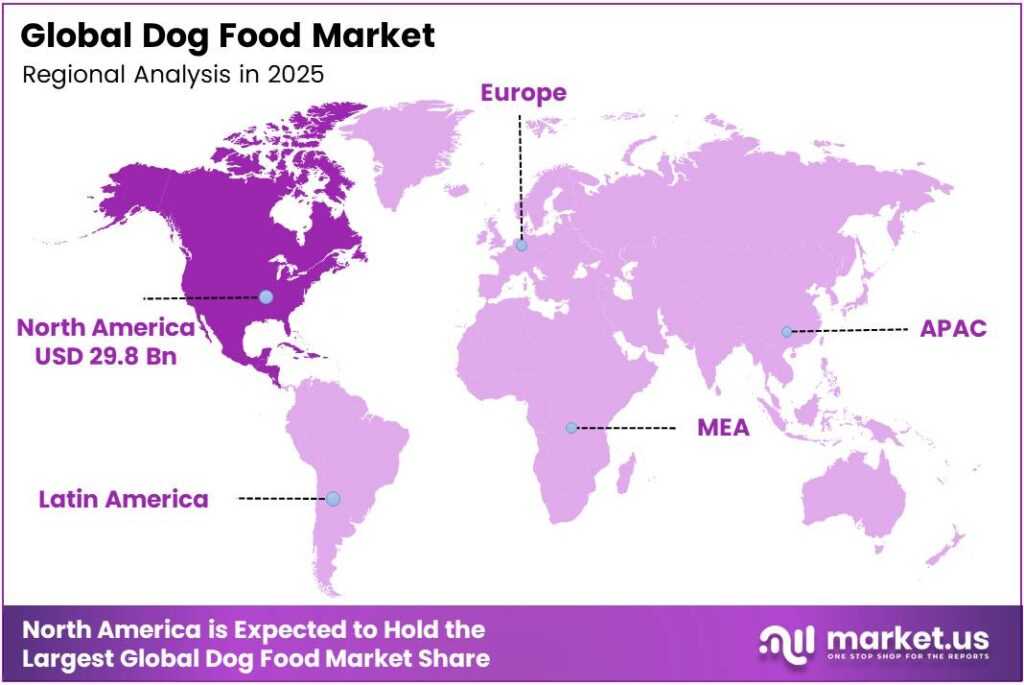

- North America dominates the regional market with a 43.7% share, valued at USD 29.8 billion in 2025.

By Type Analysis

Dry Food dominates with 48.6% due to affordability, long shelf life, and widespread retail availability.

In 2025, Dry Food held a dominant market position in the By Type segment of the Dog Food Market, with a 48.6% share. Dry kibble remains the preferred choice for most dog owners because it is cost-effective, easy to store, and nutritionally balanced. Moreover, its wide availability across supermarkets and online channels further supports its strong market leadership globally.

Wet Food holds a significant secondary position in the By Type segment. Dog owners increasingly use wet food as a palatability enhancer or a complete meal for senior and picky-eating dogs. Additionally, its higher moisture content appeals to health-focused owners who prioritize hydration and digestibility in their pets’ daily diet.

By Life Stage Analysis

Adult dominates with 67.3% due to the largest active dog population requiring consistent daily nutrition.

In 2025, Adult held a dominant market position in the By Life Stage segment of the Dog Food Market, with a 67.3% share. Adult dogs represent the largest demographic across all registered pet households globally. Therefore, manufacturers dedicate the majority of their formulation, production, and marketing investment toward adult maintenance diets across all ingredient and product formats.

Puppy formulations hold a strong secondary position in the By Life Stage segment. High-protein, calcium-rich, and DHA-enhanced puppy foods address critical early developmental needs. Moreover, growing puppy adoption rates globally, particularly in the Asia Pacific and Latin America, drive consistent demand for specialized starter nutrition products across both premium and value categories.

By Product Type Analysis

Dry Dog Food dominates with 54.1% due to its convenience, nutritional completeness, and broad consumer accessibility.

In 2025, Dry Dog Food held a dominant market position in the By Product Type segment of the Dog Food Market, with a 54.1% share. Dry formats offer extended shelf life, easy portion control, and broad price range accessibility, making them the everyday choice for most dog owners globally. Consequently, both mass-market and premium brands invest heavily in dry food product line expansions.

Wet Dog Food serves as a palatable and hydrating alternative within the By Product Type segment. Its high moisture content supports kidney health and suits dogs with dental issues or reduced appetite. Moreover, manufacturers increasingly develop grain-free and protein-rich wet formulas to attract health-conscious owners in the premium segment across North America and Europe.

By Ingredient Type Analysis

Meat-Based formulations dominate with 59.4% due to dogs’ natural protein requirements and strong owner preference for animal-sourced nutrition.

In 2025, Meat-Based held a dominant market position in the By Ingredient Type segment of the Dog Food Market, with a 59.4% share. Owners associate high animal protein content with biological appropriateness and superior nutritional quality for dogs. Therefore, chicken, beef, salmon, and lamb-based formulations consistently lead purchasing decisions across dry, wet, and raw product categories globally.

Vegetarian dog food options address a growing niche of ethically motivated owners who prefer plant-protein alternatives for their pets. Pea protein, lentil, and chickpea-based formulations provide complete amino acid profiles for dogs with animal protein sensitivities. Moreover, sustainability messaging around vegetarian diets increasingly attracts environmentally conscious consumers in Europe and North America.

By Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 44.9% due to mass accessibility, competitive pricing, and high daily foot traffic.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Dog Food Market, with a 44.9% share. These large-format retail outlets offer extensive product variety, promotional pricing, and immediate product availability. Therefore, everyday dog food purchases remain heavily concentrated in grocery and hypermarket channels across all major global markets.

Specialty Stores serve as the preferred destination for premium and veterinary-grade dog food products. Dedicated pet retail chains provide in-depth product knowledge, expert staff guidance, and exclusive brand access unavailable in mass retail formats. Moreover, growing consumer interest in tailored nutrition solutions drives consistent footfall toward specialty pet stores in urban markets.

Online channels represent the fastest-growing distribution pathway within the By Distribution Channel segment. E-commerce platforms and brand-direct subscription services enable price comparison, auto-delivery convenience, and access to a broader product assortment. Additionally, the post-pandemic normalization of online pet food purchasing continues to shift substantial volume away from brick-and-mortar retail globally.

Key Market Segments

By Type

- Dry Food

- Wet Food

- Snacks/Treats

By Life Stage

- Adult

- Puppy

- Senior

By Product Type

- Dry Dog Food

- Wet Dog Food

- Raw Dog Food

- Freeze-Dried Dog Food

By Ingredient Type

- Meat-Based

- Vegetarian

- Grain-Free

- Organic

By Distribution Channel

- Supermarkets and Hypermarkets

- Specialty Stores

- Online

- Others

Emerging Trends

Novel Proteins and Human-Grade Ingredients Transform Dog Food Formulations

Dog food manufacturers actively integrate novel proteins such as insect meal, venison, and bison into mainstream product lines. Moreover, transparent ingredient sourcing and eco-friendly packaging now serve as core purchase drivers, with blockchain traceability emerging as a competitive differentiator among premium and super-premium brands. Simmons Pet Food revenue reached $1.3 billion in 2024, driven by contract manufacturing of wet dog food for major global brands.

Functional Ingredients and Science-Backed Nutrition Drive Premium Segment Growth

Probiotics, omega-3 fatty acids, and antioxidants now appear consistently across premium dry and wet dog food lines. Grain-free and limited-ingredient recipes address rising pet allergy concerns among health-focused owners. Consequently, manufacturers pursue science-backed formulation strategies to differentiate their products and justify premium pricing within a rapidly evolving and increasingly competitive functional pet nutrition market.

Drivers

Rising Dog Ownership and Pet Humanization Fuel Demand for Premium Nutrition

Global dog ownership rates continue to rise, with pet humanization driving owners toward higher-quality and life-stage-specific nutrition solutions. Dog owners treat pets as family members, which directly elevates willingness to spend on premium formulations. Diamond Pet Foods revenue reached $1.5 billion in 2024, supported by private-label dog food manufacturing and contract production across North America, reflecting sustained industry-wide production growth.

E-Commerce Expansion and Health Awareness Accelerate Market Accessibility

Rapid growth in e-commerce platforms and subscription-based delivery models expands dog food accessibility beyond traditional retail boundaries. Heightened owner awareness of pet health conditions such as obesity and allergies accelerates the adoption of functional and breed-specific formulations. Moreover, growing preference for condition-targeted diets continuously drives product innovation, broadening the addressable consumer base across both developed and emerging markets.

Restraints

Raw Material Cost Volatility Erodes Manufacturer Margins and Pricing Stability

Persistent volatility in raw material costs for animal proteins and grains significantly pressures manufacturer profit margins. Fluctuating commodity prices for chicken, beef, and wheat create unpredictable input cost environments. Consequently, manufacturers struggle to maintain consistent retail pricing without absorbing margin losses, which limits their ability to invest in innovation and product development within an already competitive market landscape.

Premium Pricing Limits Penetration in Budget-Conscious and Emerging Markets

Elevated pricing of natural and specialized dog food products restricts market penetration in budget-sensitive regions. Consumers in emerging markets across Southeast Asia, Africa, and Latin America remain largely price-driven in their purchasing decisions. Therefore, premium and organic formulations face significant barriers to volume growth outside developed economies, limiting the near-term global scalability of high-value dog food product lines.

Growth Factors

Emerging Markets and Personalized Nutrition Platforms Unlock New Revenue Streams

Rising middle-class pet adoption in Asia and Latin America creates explosive growth potential for dog food manufacturers. Western-style pet spending patterns are rapidly taking hold across India, China, Brazil, and Mexico. General Mills’ pet food segment revenue reached $2.5 billion in FY2025, reflecting a 4% year-over-year increase driven by premium dog food brand growth, signaling strong consumer appetite for branded nutrition solutions.

Organic, Functional, and Custom Formulations Drive Innovation-Led Expansion

Surging demand for organic, vegan, and plant-based dog food lines aligns directly with sustainable and ethical consumer values. Personalized nutrition platforms offering custom formulations based on genetic profiling and individual health needs represent a high-value growth frontier. Additionally, functional treats and supplements targeting joint, digestive, and skin health expand the addressable product portfolio far beyond traditional meal replacement formats.

Regional Analysis

North America Dominates the Dog Food Market with a Market Share of 43.7%, Valued at USD 29.8 Billion

North America leads the global dog food market, commanding a 43.7% share valued at USD 29.8 billion in 2025. The region benefits from the highest dog ownership rates globally, a deeply entrenched pet humanization culture, and consumer willingness to spend on premium nutrition. The North American pet food market represents the largest regional market, driven by high dog ownership and premium food consumption.

Europe holds the second-largest share in the global dog food market, driven by strong regulatory standards and sophisticated consumer preferences. German, French, and British markets lead the adoption of grain-free, organic, and sustainable pet food lines. Additionally, EU regulatory frameworks around ingredient transparency and animal welfare labeling continue to elevate product quality benchmarks across the entire regional market.

Asia Pacific represents the fastest-growing regional market for dog food globally. Rising disposable incomes, rapid urbanization, and growing pet adoption rates in China, India, and South Korea drive substantial market expansion. Furthermore, Western-influenced pet ownership attitudes accelerate premiumization, and the proliferation of e-commerce platforms makes premium and imported dog food products increasingly accessible to urban consumers.

The Middle East and Africa region shows steady growth potential driven by rising urban pet ownership, particularly in GCC countries and South Africa. Premium and imported dog food brands gain traction among affluent urban households. However, limited domestic manufacturing capacity and price sensitivity in lower-income markets restrain broader regional penetration of premium and specialized dog food products.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Mars, Inc. operates one of the largest pet care businesses globally, with its dog food portfolio anchored by Pedigree and Royal Canin. Mars Petcare maintains extensive global distribution and continuously invests in science-based nutrition platforms that target specific breeds, life stages, and health conditions across all major markets.

The J.M. Smucker Company maintains a strong presence in the U.S. dog food market through established brands including Milk-Bone and Kibbles ‘n Bits. J.M. Smucker’s pet food leverages its broad retail distribution network and strong brand equity in the value and mid-premium dog food segments, consistently expanding its product range to meet evolving owner preferences for treats and complete nutrition solutions.

Nestlé Purina PetCare stands as a global leader in dog food innovation and distribution, with a portfolio spanning Purina Pro Plan, Dog Chow, and Beneful. Nestlé Purina PetCare is maintaining its position as the largest pet food company globally. The company drives growth through continuous product innovation in functional nutrition, life-stage specific formulations, and premium ingredient sourcing across North America and Europe.

Hill’s Pet Nutrition builds its market position on veterinarian-recommended therapeutic and preventive dog food solutions. Hill’s Pet Nutrition is driven by veterinary-prescribed dog food products and strong North American market penetration. The company’s science-backed formulation approach, combined with deep integration into veterinary care networks, creates strong brand loyalty and defensible premium pricing across clinical and retail distribution channels.

Top Key Players in the Market

- Mars, Inc.

- The J.M. Smucker Company

- Nestlé Purina PetCare

- Hill’s Pet Nutrition

- Drools Pet Food Pvt. Ltd.

- CANIN

- Nulo

- Agro Food Industries

Recent Developments

- In 2025, Mars announced that ORIJEN launched FRESHPREY, a new development elevating fresh pet food options (applicable to dog food lines). Mars Petcare partnered with Big Idea Ventures (and collaborators AAK, Bühler, Givaudan) to select three startups for the 2025 Next Generation Pet Food Program, aimed at sustainable innovation in pet food ingredients and processing (including pathways for dog food).

- In 2025, Smucker announced leadership changes, with Judd Freitag promoted to Senior Vice President and General Manager, Pet and Sweet Baked Snacks, overseeing the U.S. Retail Pet Foods segment alongside supply chain/manufacturing oversight enhancements.

Report Scope

Report Features Description Market Value (2025) USD 68.4 Billion Forecast Revenue (2035) USD 126.2 Billion CAGR (2026-2035) 6.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Dry Food, Wet Food, Snacks/Treats), By Life Stage (Adult, Puppy, Senior), By Product Type (Dry Dog Food, Wet Dog Food, Raw Dog Food, Freeze-Dried Dog Food), By Ingredient Type (Meat-Based, Vegetarian, Grain-Free, Organic), By Distribution Channel (Supermarkets and Hypermarkets, Specialty Stores, Online, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Mars, Inc., The J.M. Smucker Company, Nestlé Purina PetCare, Hill’s Pet Nutrition, Drools Pet Food Pvt. Ltd., CANIN, Nulo, Agro Food Industries Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Mars, Inc.

- The J.M. Smucker Company

- Nestlé Purina PetCare

- Hill's Pet Nutrition

- Drools Pet Food Pvt. Ltd.

- CANIN

- Nulo

- Agro Food Industries

Our Clients

- 182402

- March 2026