Quick Navigation

Market Overview

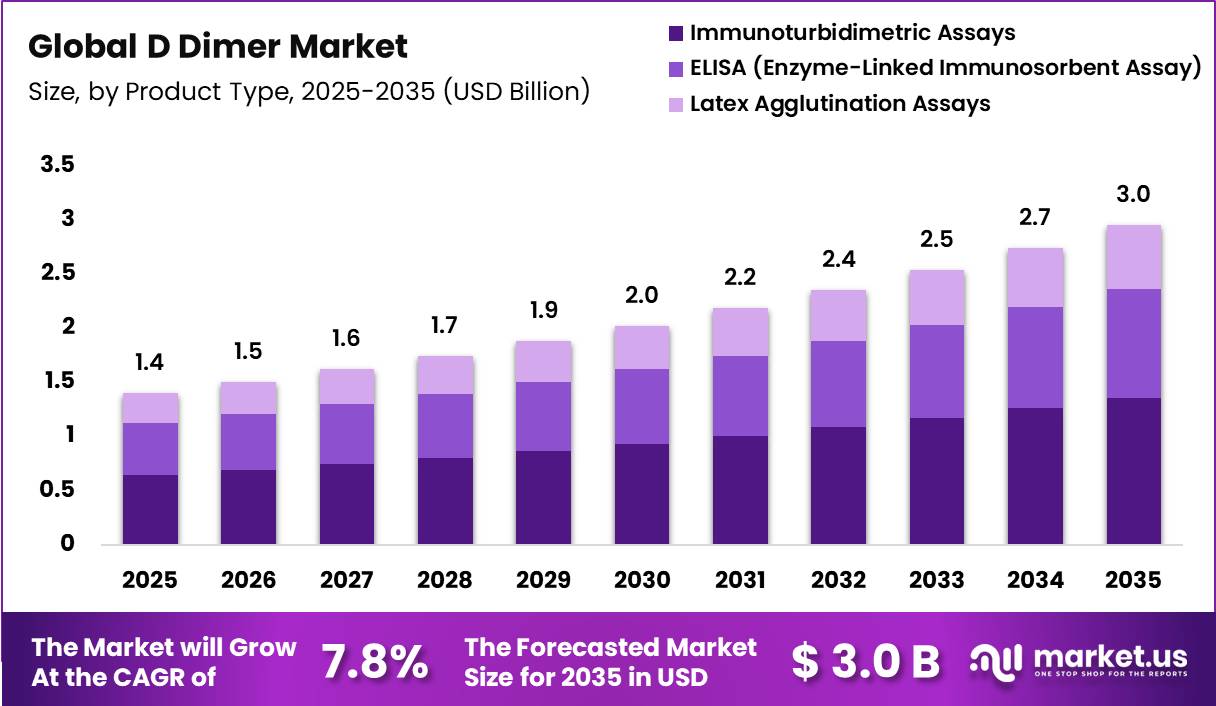

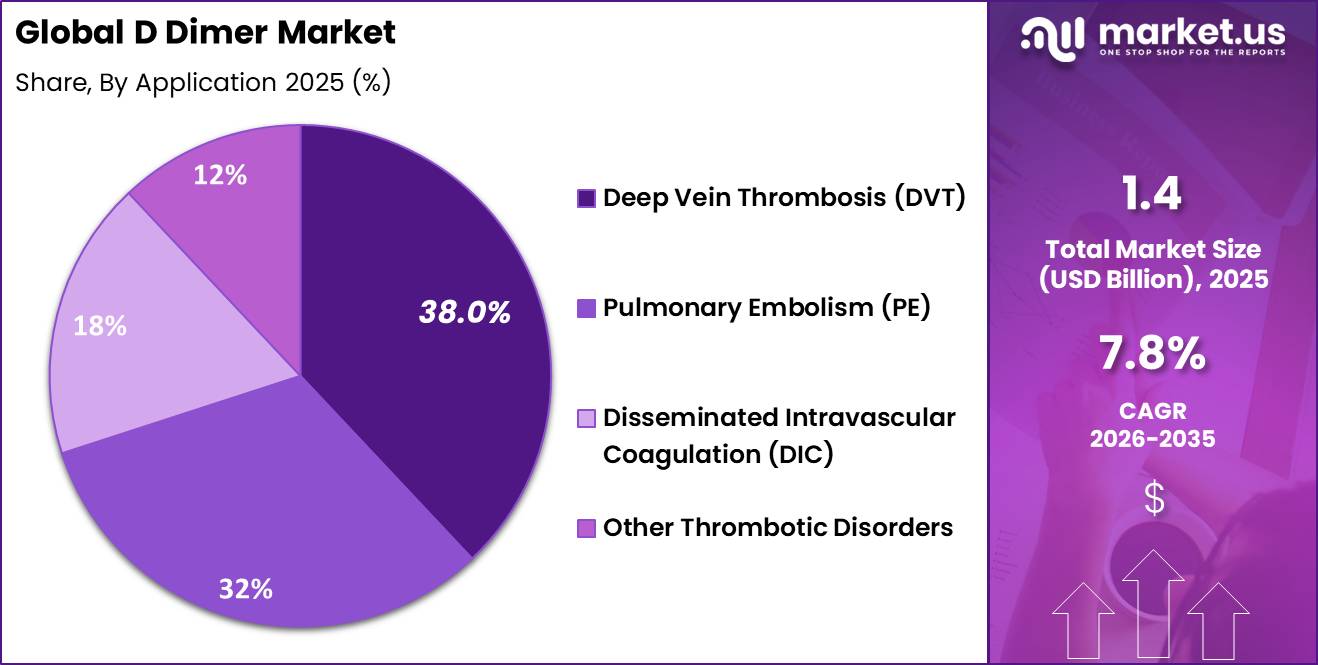

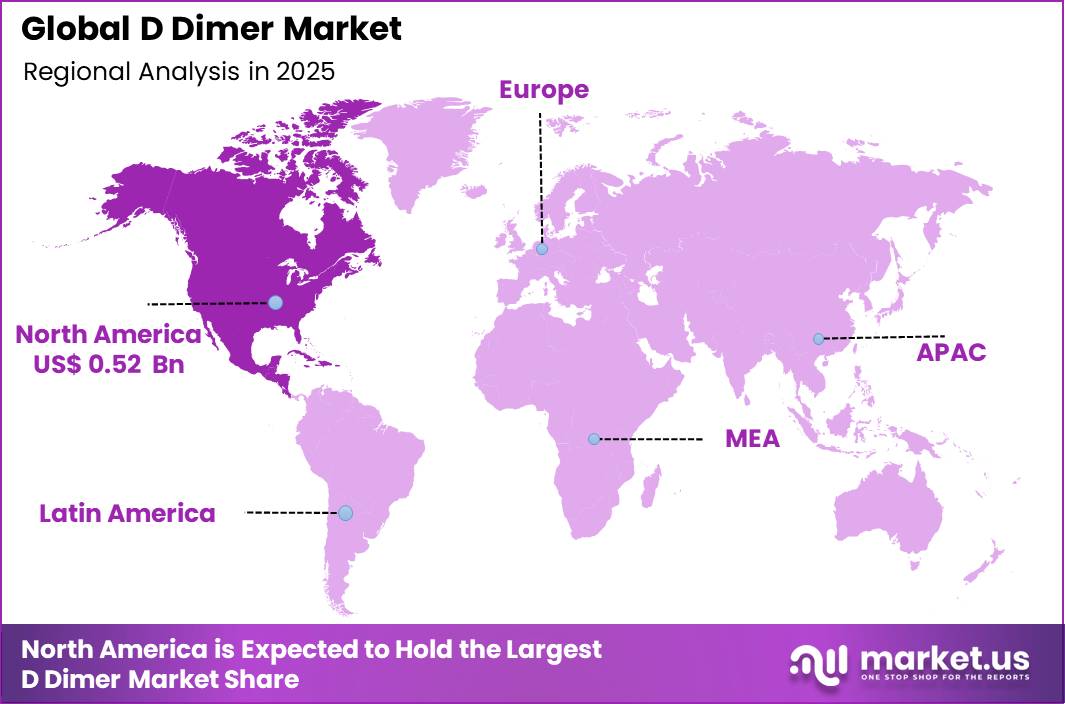

Global D Dimer Market size is expected to be worth around US$ 3.0 Billion by 2035 from US$ 1.4 Billion in 2025, growing at a CAGR of 7.8% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 37.00% share with a revenue of US$ 0.52 Billion.

The D-Dimer market is gaining importance worldwide as healthcare systems focus on the early detection and management of thrombotic disorders, including deep vein thrombosis (DVT), pulmonary embolism (PE), and disseminated intravascular coagulation (DIC). D-Dimer is a fibrin degradation product released when blood clots break down, making it a widely used biomarker in emergency medicine and clinical diagnostics.

According to the U.S. National Library of Medicine and MedlinePlus, D-Dimer testing is routinely used to help rule out potentially life-threatening blood clotting conditions and guide further diagnostic imaging when necessary. A standard negative result is generally below 500 ng/mL, providing a high negative predictive value in patients with suspected venous thromboembolism.

Market growth is being supported by the increasing burden of cardiovascular diseases, aging populations, rising hospitalization rates, and broader adoption of rapid diagnostic technologies. Healthcare providers are increasingly integrating high-sensitivity immunoassays and automated laboratory platforms to improve testing efficiency and turnaround times.

The expansion of emergency departments, critical care services, and diagnostic laboratories is further contributing to demand. In addition, growing awareness of thrombosis risk factors, including surgery, cancer, prolonged immobility, and infectious diseases, is encouraging wider use of D-Dimer screening. Continuous advancements in laboratory automation and point-of-care diagnostic solutions are expected to enhance accessibility and support the long-term development of the global D-Dimer market.

Key Takeaways

- Market Size: Global D Dimer Market size is expected to be worth around US$ 3.0 Billion by 2035 from US$ 1.4 Billion in 2025.

- Market Share: The market is growing at a CAGR of 7.8% during the forecast period from 2026 to 2035.

- Product Type: The D-Dimer market by product type is led by Immunoturbidimetric Assays, which accounted for 46.0% of the global market share in 2025.

- Application: Deep Vein Thrombosis (DVT) held the largest share of the D-Dimer market, accounting for 38.0% of total revenue in 2025.

- End User: Hospitals dominated the D-Dimer market with a 58.0% market share in 2025, making them the largest end-user segment globally.

- Technology Platform: The Automated Analyzers segment dominated the D-Dimer market, accounting for 61.0% of total market revenue in 2025.

- Sample Type: Plasma Samples held the largest share of the D-Dimer market, accounting for 72.0% of total market revenue in 2025.

- Distribution Channel: Direct Institutional Sales dominated the D-Dimer market with an impressive 83.0% share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 37.00% share with a revenue of US$ 0.52 Billion.

Product Type Analysis

The D-Dimer market by product type is led by Immunoturbidimetric Assays, which accounted for 46.0% of the global market share in 2025. This segment dominates due to its ability to deliver rapid and reliable results while supporting high-throughput testing environments.

Hospitals and diagnostic laboratories increasingly prefer immunoturbidimetric assays because they integrate seamlessly with automated analyzers, reduce manual workload, and enable faster clinical decision-making in emergency and critical care settings. The growing demand for efficient coagulation testing, coupled with the expansion of automated laboratory infrastructure, continues to strengthen the segment’s market leadership.

Meanwhile, ELISA (Enzyme-Linked Immunosorbent Assay) is emerging as a key growth segment owing to its superior sensitivity and analytical accuracy, particularly in specialized laboratories where confirmatory testing is required. Increasing focus on precision diagnostics and advanced laboratory capabilities is supporting its adoption across developed and emerging healthcare markets.

Reflecting this trend, Sysmex Corporation continues to expand its coagulation testing portfolio with solutions designed to enhance laboratory efficiency and diagnostic confidence. Latex Agglutination Assays maintain a stable presence in cost-sensitive and smaller laboratory settings, supporting broader access to D-Dimer testing.

Application Analysis

By application, Deep Vein Thrombosis (DVT) held the largest share of the D-Dimer market, accounting for 38.0% of total revenue in 2025. The segment’s dominance stems from the widespread use of D-Dimer testing as a frontline screening tool for suspected DVT cases.

Healthcare providers rely on these tests to rapidly exclude thrombotic conditions, reduce unnecessary imaging procedures, and accelerate treatment decisions. Rising prevalence of obesity, sedentary lifestyles, aging populations, and post-operative complications has further increased the number of patients undergoing DVT screening, reinforcing the segment’s leading position.

Pulmonary Embolism (PE) is expected to witness strong growth as awareness of life-threatening clotting disorders increases and healthcare systems emphasize rapid diagnosis in emergency settings. The growing use of D-Dimer testing in emergency departments and critical care units continues to support demand in this area.

As part of broader efforts to enhance diagnostic capabilities, QuidelOrtho Corporation has strengthened its portfolio of diagnostic solutions used in acute care and laboratory environments. Applications such as disseminated intravascular coagulation (DIC) and other thrombotic disorders continue to contribute to overall market expansion, supported by rising demand for coagulation monitoring.

End User Analysis

Hospitals dominated the D-Dimer market with a 58.0% market share in 2025, making them the largest end-user segment globally. Their leadership is driven by the high volume of coagulation testing performed in emergency departments, intensive care units, and inpatient settings.

Hospitals possess advanced laboratory infrastructure, automated diagnostic systems, and specialized clinical expertise, enabling rapid diagnosis and management of conditions such as deep vein thrombosis and pulmonary embolism. The increasing burden of cardiovascular diseases and thrombotic disorders continues to generate substantial testing demand, supporting the segment’s strong market position.

At the same time, Diagnostic Laboratories are experiencing significant growth as healthcare providers increasingly outsource specialized testing services to improve operational efficiency and reduce costs. Rising demand for high-throughput testing, standardized workflows, and accurate diagnostic results is driving expansion within this segment.

Supporting this trend, Randox Laboratories continues to strengthen its diagnostic testing capabilities for laboratory customers worldwide. Clinics and ambulatory care centers are also gradually increasing their use of D-Dimer testing as access to rapid diagnostic technologies improves and outpatient care services expand.

Technology Platform Analysis

The Automated Analyzers segment dominated the D-Dimer market, accounting for 61.0% of total market revenue in 2025. The segment’s leadership is primarily driven by the growing need for rapid, accurate, and high-volume diagnostic testing across hospitals and diagnostic laboratories. Automated analyzers significantly reduce manual intervention, improve workflow efficiency, and deliver consistent test results, making them the preferred platform for routine D-Dimer screening.

The increasing burden of thrombotic disorders, combined with rising patient volumes and pressure on laboratories to provide faster turnaround times, has accelerated the adoption of automated systems. In addition, healthcare facilities continue to invest in laboratory automation to enhance productivity, minimize human error, and support standardized testing procedures, further strengthening the segment’s market position.

Meanwhile, Manual Testing Kits continue to play an important role in smaller laboratories, community healthcare centers, and resource-constrained settings where access to advanced automation remains limited. These solutions are valued for their affordability, ease of implementation, and lower infrastructure requirements.

However, as healthcare systems increasingly prioritize efficiency and scalability, demand is gradually shifting toward automated platforms. Reflecting this industry trend, Beckman Coulter (Danaher) continues to expand its portfolio of automated diagnostic solutions designed to improve laboratory performance and support growing testing volumes. The ongoing modernization of laboratory infrastructure is expected to further reinforce the dominance of automated analyzers over the forecast period.

Sample Type Analysis

By sample type, Plasma Samples held the largest share of the D-Dimer market, accounting for 72.0% of total market revenue in 2025 because it provides high analytical accuracy, reliable fibrin degradation measurement, and compatibility with most commercially available assay platforms. Clinical laboratories and hospitals widely prefer plasma-based testing due to its established role in coagulation diagnostics and its ability to deliver consistent and reproducible results.

Furthermore, most regulatory-approved D-Dimer assays and laboratory protocols are validated using plasma specimens, making them the preferred choice for routine screening and diagnostic applications. The increasing emphasis on diagnostic precision and standardized testing practices continues to reinforce the segment’s dominant market position globally.

At the same time, Whole Blood Samples are gaining attention as healthcare providers seek faster and more convenient testing solutions, particularly in emergency care and point-of-care settings. Whole blood testing reduces sample preparation requirements and supports quicker clinical decision-making, making it attractive for decentralized healthcare environments.

Technological advancements are improving the accuracy and reliability of whole blood-based assays, creating new growth opportunities within the market. Supporting this evolution, HORIBA Medical continues to focus on innovative diagnostic technologies that enhance testing efficiency and broaden access to coagulation diagnostics. While plasma samples remain the benchmark for laboratory-based testing, increasing demand for rapid and decentralized diagnostics is expected to drive steady growth in whole blood testing applications.

Distribution Channel Analysis

Direct Institutional Sales dominated the D-Dimer market with an impressive 83.0% share in 2025. The segment leads because major hospitals, healthcare networks, and diagnostic laboratories typically procure analyzers, reagents, and consumables directly from manufacturers through long-term supply agreements.

Direct purchasing provides advantages such as reliable product availability, technical support, staff training, and favorable pricing structures. As laboratory networks continue to expand and invest in automated diagnostic systems, direct manufacturer-to-institution relationships remain the preferred procurement model across the healthcare sector.

However, Online Procurement is emerging as a rapidly growing distribution channel as healthcare organizations increasingly adopt digital purchasing platforms to improve supply chain management and streamline ordering processes. The shift toward digital procurement is helping laboratories enhance operational efficiency while gaining easier access to a wider range of diagnostic products.

In line with evolving distribution strategies, Sekisui Diagnostics has broadened market access for its diagnostic solutions through expanded channel partnerships and procurement networks. Traditional distributors continue to play a supportive role, particularly in regional and emerging markets where localized logistics and customer support remain important.

Key Market Segments

Product Type

- Immunoturbidimetric Assays

- ELISA (Enzyme-Linked Immunosorbent Assay)

- Latex Agglutination Assays

Application

- Deep Vein Thrombosis (DVT)

- Pulmonary Embolism (PE)

- Disseminated Intravascular Coagulation (DIC)

- Other Thrombotic Disorders

End User

- Hospitals

- Diagnostic Laboratories

- Clinics & Ambulatory Care

- Others (Research Institutes)

Technology Platform

- Automated Analyzers

- Manual Testing Kits

Sample Type

- Plasma Samples

- Whole Blood Samples

Distribution Channel

- Direct Institutional Sales

- Distributors

- Online Procurement

Opportunities

Oncology recurrence monitoring represents an emerging opportunity for D-dimer testing beyond its traditional role in acute thrombosis rule-out. Clinical guidelines already recognize cancer-associated thrombosis (CAT) as a distinct condition requiring tailored anticoagulation strategies for patients with cancer and pulmonary embolism.

Cancer patients often remain at elevated thrombotic risk throughout treatment and recovery, creating demand for long-term monitoring approaches. The opportunity lies in using serial D-dimer measurements to support recurrence-risk assessment, treatment follow-up, and anticoagulation-duration decisions in both solid-tumor and hematology patients. Compared with one-time acute diagnostic testing, longitudinal monitoring can increase testing frequency several-fold per patient over the course of care.

D-dimer may also become part of broader risk-stratification panels used by oncology networks and hospital systems. Standardized monitoring protocols could improve identification of patients at higher risk of recurrent thrombotic events. Adoption potential is strongest in North America, Europe, Japan, and South Korea, where cancer care pathways and thrombosis management programs are well established.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| ED algorithmic triage integration | +2.5% | North America core, EU, urban APAC | Short term (≤ 2 years) |

| Oncology recurrence monitoring | +2.0% | North America, EU, Japan, Korea | Medium term (2-4 years) |

| Point-of-care decentralization | +2.3% | India, SEA, LATAM, Middle East, rural West | Medium term (2-4 years) |

| Pregnancy-specific rule-out panels | +1.6% | EU, North America, GCC, advanced APAC | Short term (≤ 2 years) |

| Sepsis and DIC risk stratification | +1.8% | Global ICU hubs, tertiary hospitals | Medium term (2-4 years) |

| Integrated assay-software platforms | +1.7% | North America, EU, China, Japan | Long term (≥ 4 years) |

DriversSepsis coagulopathy monitoring is becoming an important growth area for D-dimer testing beyond its traditional use in venous thromboembolism (VTE) diagnosis. Clinical guidance recognizes D-dimer as a valuable marker of coagulation activation and fibrinolysis in patients with sepsis and septic shock.

D-dimer is also a key laboratory parameter used in the assessment of disseminated intravascular coagulation (DIC), a serious complication associated with severe infections. Unlike emergency-department rule-out testing, sepsis management often requires repeated D-dimer measurements over several days to track progression or worsening of coagulopathy.

This allows clinicians to monitor changes in coagulation status during critical-care treatment. The shift from one-time testing to serial monitoring increases demand for laboratory testing within intensive care units and tertiary-care hospitals. D-dimer is increasingly being incorporated into broader coagulation-monitoring panels used in critical-care settings. The opportunity is particularly relevant as hospitals expand sepsis management pathways and critical-care monitoring programs.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Age-adjusted rule-out adoption | +2.6% | North America core, EU, Japan, Korea | Short term (≤ 2 years) |

| Pregnancy-adapted PE pathways | +1.8% | North America, EU, GCC, advanced APAC | Medium term (2-4 years) |

| ED imaging-avoidance protocols | +2.1% | North America, EU, urban APAC | Short term (≤ 2 years) |

| Suspected DVT triage expansion | +1.7% | North America, EU, Australia | Medium term (2-4 years) |

| Sepsis coagulopathy monitoring | +1.5% | Global ICU hubs, tertiary hospitals | Medium term (2-4 years) |

| Algorithm-linked lab standardization | +1.4% | North America, EU, China, Japan | Long term (≥ 4 years) |

Challenges

Recurrent VTE evidence gaps remain a significant challenge for the D-dimer testing market because most clinical validation has focused on first-presentation venous thromboembolism (VTE) rule-out rather than recurrent events.

Clinical literature notes that there is currently no validated adjusted D-dimer threshold for patients with suspected recurrent VTE, whether they are receiving anticoagulant therapy or not. This limitation is important because recurrent-VTE patients often require complex and resource-intensive clinical management.

Without standardized thresholds, clinicians frequently rely on more conservative diagnostic strategies and additional imaging studies. The lack of recurrence-specific evidence reduces confidence in using D-dimer as a standalone decision-support tool in these cases.

As a result, adoption remains limited in vascular medicine and specialized thrombosis programs. Expanding the evidence base for recurrent VTE could improve diagnostic pathways and support broader utilization of D-dimer testing in high-risk patient populations.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Assay cut-off variability | -1.8% | North America, EU, Japan, global lab networks | Medium term (2-4 years) |

| Pregnancy interpretation complexity | -1.5% | North America, EU, GCC, advanced APAC | Medium term (2-4 years) |

| Low-specificity clinical noise | -1.4% | Global EDs, ICUs, oncology centers | Short term (≤ 2 years) |

| Algorithm implementation inconsistency | -1.3% | North America, EU, urban APAC | Medium term (2-4 years) |

| Recurrent VTE evidence gap | -1.1% | North America, EU, tertiary vascular hubs | Long term (≥ 4 years) |

| Serial-monitoring value ambiguity | -1.0% | Global ICU hubs, academic hospitals | Medium term (2-4 years) |

Restraints

Imaging-dependent care pathways remain a significant restraint for D-dimer testing because the assay is typically used as part of a broader diagnostic workflow rather than as a standalone diagnostic tool. Clinical guidance for pulmonary embolism (PE) evaluation combines clinical probability assessment, D-dimer testing, and definitive imaging modalities such as CTPA, ultrasound, or V/Q scanning.

D-dimer is primarily used to exclude disease in lower-risk patients, while positive or inconclusive results generally require follow-up imaging. This dependency limits the test’s ability to function as a final diagnostic endpoint in most clinical settings.

As a result, the value of D-dimer remains closely linked to the availability of imaging infrastructure and established diagnostic protocols. Resource-constrained healthcare facilities may face challenges in fully utilizing D-dimer-based pathways without access to advanced imaging technologies. The continued reliance on imaging also limits the test’s role in independent clinical decision-making and broader market expansion.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Assay standardization limits | -2.0% | North America, EU, Japan, global lab networks | Medium term (2-4 years) |

| Low positive predictive power | -1.8% | Global EDs, urgent care, hospital labs | Short term (≤ 2 years) |

| Recurrent VTE evidence gap | -1.5% | North America, EU, tertiary vascular centers | Long term (≥ 4 years) |

| Elderly false-positive inflation | -1.3% | North America, EU, Japan, aging markets | Medium term (2-4 years) |

| Unit and cutoff confusion | -1.1% | Global multisite lab systems | Short term (≤ 2 years) |

| Imaging-dependent care pathways | -1.0% | Global hospital systems | Medium term (2-4 years) |

Regional Analysis

North America dominated the Global D-dimer market.

North America dominated the Global D-dimer market in 2025, accounting for more than 37.0% of total revenue and generating approximately US$ 0.52 billion. The region’s leadership is primarily driven by its advanced healthcare infrastructure, widespread adoption of laboratory diagnostics, and high awareness of thrombotic disorders such as deep vein thrombosis (DVT), pulmonary embolism (PE), and disseminated intravascular coagulation (DIC).

The growing burden of cardiovascular diseases, cancer-related thrombosis, and an aging population has increased the demand for rapid and accurate coagulation testing across hospitals, diagnostic laboratories, and emergency care settings. In addition, favorable reimbursement frameworks and strong clinical guideline adoption support routine D-dimer testing in patient management and risk assessment.

The presence of major diagnostic manufacturers, extensive research activities, and continuous investments in healthcare technology further strengthen the region’s market position. Healthcare providers in the United States and Canada are increasingly utilizing high-sensitivity immunoassay platforms and automated laboratory systems that improve testing efficiency and diagnostic accuracy.

The growing use of D-dimer assays in emergency departments for ruling out venous thromboembolism and supporting clinical decision-making has also contributed significantly to market expansion. Furthermore, rising demand for point-of-care diagnostics and the integration of advanced laboratory automation solutions are expected to sustain North America’s dominance over the forecast period.

While North America remains the largest regional market, Asia-Pacific is emerging as the fastest-growing region due to expanding healthcare access, increasing diagnostic testing volumes, and ongoing healthcare infrastructure development across countries such as China and India.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

The global D-dimer market is moderately consolidated, with a group of established diagnostics companies competing through technological innovation, assay accuracy, automation capabilities, and laboratory workflow efficiency. Key participants including Roche Diagnostics, Siemens Healthineers, Abbott Laboratories, Thermo Fisher Scientific, Sysmex Corporation, and Beckman Coulter maintain strong market positions through extensive diagnostic portfolios and global distribution networks.

As healthcare providers increasingly emphasize rapid diagnosis of thrombotic disorders, pulmonary embolism, and deep vein thrombosis, manufacturers are focusing on improving assay sensitivity, turnaround times, and integration with automated laboratory systems. Competition is driven not only by product performance but also by the ability to support high-throughput testing environments and deliver standardized results across diverse healthcare settings.

Leading companies are investing heavily in research and development to enhance biomarker detection technologies and expand clinical applications of D-dimer testing. Strategic partnerships with hospitals, diagnostic laboratories, and healthcare networks enable broader adoption of integrated testing platforms.

Product innovation remains a core competitive strategy, with companies introducing advanced immunoassay solutions, automated analyzers, and digital connectivity features that streamline laboratory operations. Workflow integration has become increasingly important, allowing D-dimer assays to function seamlessly within broader coagulation and diagnostic testing ecosystems.

Additionally, ecosystem-based competition is strengthening as manufacturers combine instruments, reagents, software, and data management solutions into comprehensive diagnostic platforms. This approach helps improve operational efficiency, supports clinical decision-making, and creates long-term customer relationships while reinforcing competitive differentiation in the evolving D-dimer market.

Top Key Players

- Roche Diagnostics

- Siemens Healthineers

- Abbott Laboratories

- Thermo Fisher Scientific

- Sysmex Corporation

- Beckman Coulter (Danaher)

- bioMérieux

- QuidelOrtho Corporation

- Randox Laboratories

- HORIBA Medical

- F. Hoffmann-La Roche Ltd

- Mindray Medical International

- Trinity Biotech

- Sekisui Diagnostics

- Stago (Diagnostica Stago)

Recent Developments

- In June 2025, Sysmex Corporation received U.S. FDA clearance for the CN-6000 Automated Blood Coagulation Analyzer, including the INNOVANCE D-Dimer reagent. This was a major regulatory milestone that expanded Sysmex’s presence in the U.S. hemostasis testing market and strengthened its D-dimer testing portfolio.

- In January 2026, Sysmex America launched the CN-9000 Automated Hemostasis Solution in North America. The system was designed for high-volume laboratories and supports automated coagulation testing workflows, improving efficiency and throughput in D-dimer and other hemostasis assays.

- In March 2025, Beckman Coulter Diagnostics received FDA clearance for the DxC 500i Clinical Analyzer. The integrated clinical chemistry and immunoassay platform enhances laboratory workflow efficiency and expands Beckman Coulter’s capabilities in diagnostic testing environments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.4 Billion |

| Forecast Revenue (2035) | US$ 3.0 Billion |

| CAGR (2026-2035) | 7.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Immunoturbidimetric Assays, ELISA (Enzyme-Linked Immunosorbent Assay), Latex Agglutination Assays), By Application (Deep Vein Thrombosis (DVT), Pulmonary Embolism (PE), Disseminated Intravascular Coagulation (DIC), Other Thrombotic Disorders), By End User (Hospitals, Diagnostic Laboratories, Clinics & Ambulatory Care, Others (Research Institutes)), By Technology Platform (Automated Analyzers, Manual Testing Kits, Sample Type Plasma Samples, Whole Blood Samples), By Distribution Channel (Direct Institutional Sales, Distributors, Online Procurement) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Roche Diagnostics, Siemens Healthineers, Abbott Laboratories, Thermo Fisher Scientific, Sysmex Corporation, Beckman Coulter (Danaher), bioMérieux, QuidelOrtho Corporation, Randox Laboratories, HORIBA Medical, F. Hoffmann-La Roche Ltd, Mindray Medical International, Trinity Biotech, Sekisui Diagnostics, Stago (Diagnostica Stago) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |