Quick Navigation

Report Overview

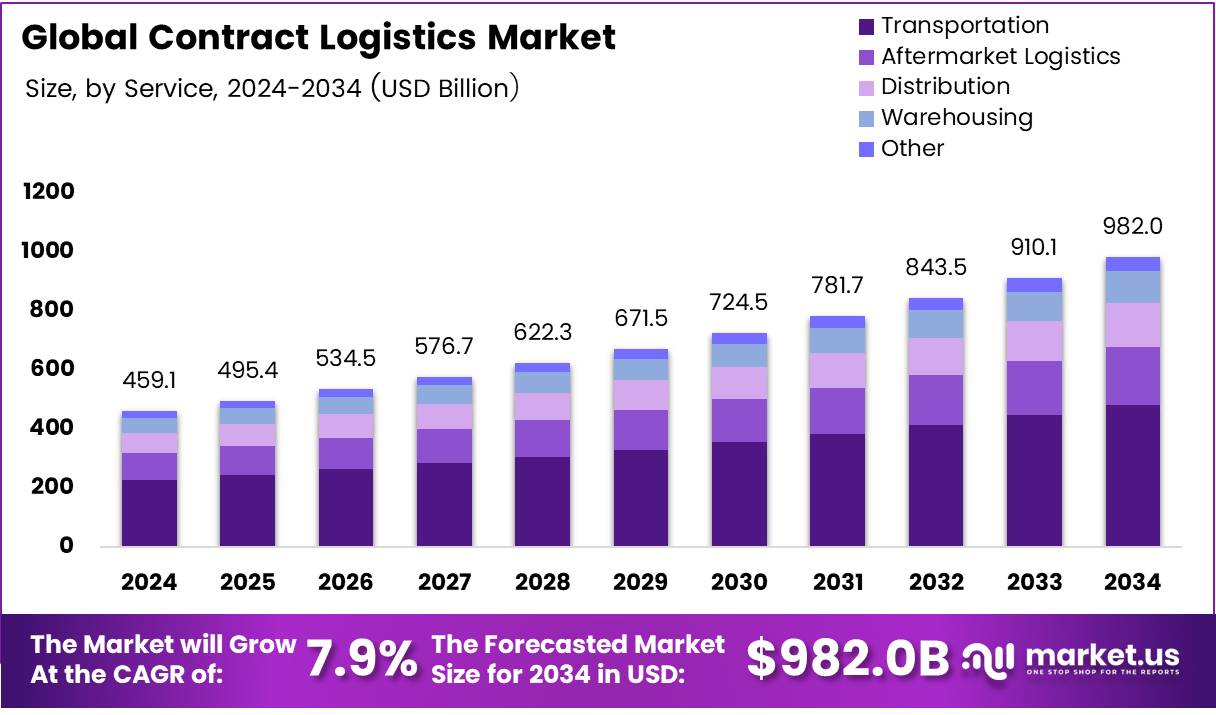

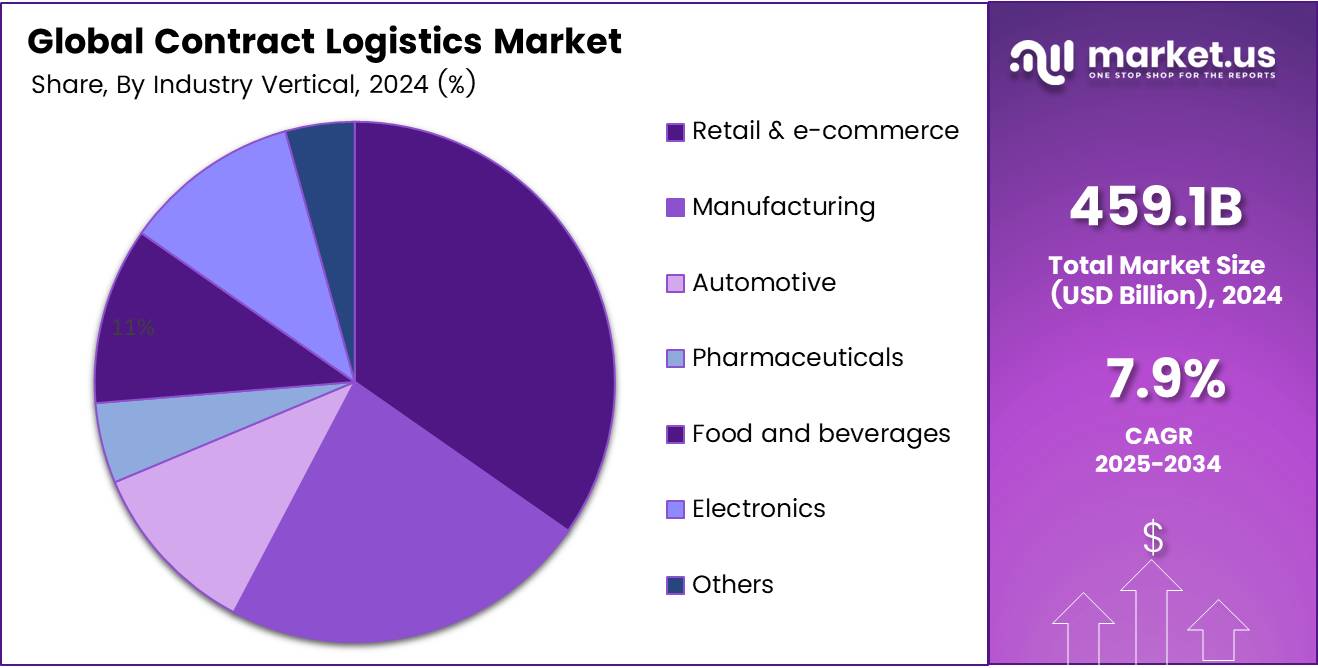

The Global Contract Logistics Market size is expected to be worth around USD 982.0 Billion by 2034, from USD 459.1 Billion in 2024, growing at a CAGR of 7.9% during the forecast period from 2025 to 2034.

The Contract Logistics Market is a dynamic segment within the broader logistics industry, focusing on outsourcing the logistics functions of businesses to specialized service providers. This includes services such as transportation, warehousing, inventory management, and value-added services tailored to meet the needs of businesses. As companies increasingly seek to optimize their supply chains, the demand for contract logistics services has surged, creating growth opportunities across the globe.

According to Adexin, in 2023, 43% of investments were directed into U.S. logistics startups, highlighting the country’s dominant role in driving innovation and growth within the logistics space. This strong investment influx demonstrates the market’s growth potential, particularly in regions with robust infrastructure and technology adoption. Additionally, 19% of investments were placed into Indian logistics startups, underscoring the growing importance of the Asia-Pacific region in the global contract logistics market.

The key drivers of growth in the contract logistics market include advancements in technology, increasing e-commerce demand, and a focus on supply chain optimization. Governments worldwide are increasingly investing in infrastructure, regulations, and digitalization to support logistics growth. For instance, many countries are offering incentives and subsidies to enhance logistics capabilities, streamline operations, and encourage sustainability within the sector.

Government regulations are also shaping the future of the contract logistics market. Regulatory bodies are focusing on improving transportation safety, reducing carbon emissions, and ensuring compliance with international trade agreements. These regulatory frameworks are particularly important for global logistics players looking to expand across multiple regions. As a result, logistics providers must remain agile to adapt to regulatory changes while meeting the evolving needs of their clients.

In terms of cost structure, according to Tech, 58% of logistics costs are driven by transportation, followed by 23% for warehousing, 11% for inventory carrying, and 8% for administrative costs. Understanding these cost dynamics allows businesses to focus on optimizing their operations in areas that can offer the greatest impact on cost efficiency.

Key Takeaways

- Global Contract Logistics Market is projected to reach USD 982.0 Billion by 2034, growing at a CAGR of 7.9% from 2025 to 2034.

- In 2024, the transportation segment dominated the market with a 34.7% share, fueled by e-commerce growth and global trade expansion.

- Outsourcing emerged as the leading model, accounting for 55.6% of the market share in 2024, driven by cost reduction and efficiency needs.

- Roadways transportation remained dominant in 2024 due to its flexibility, cost-effectiveness, and extensive infrastructure.

- The retail and e-commerce sector held a dominant position in 2024, boosted by a surge in online shopping and evolving consumer habits.

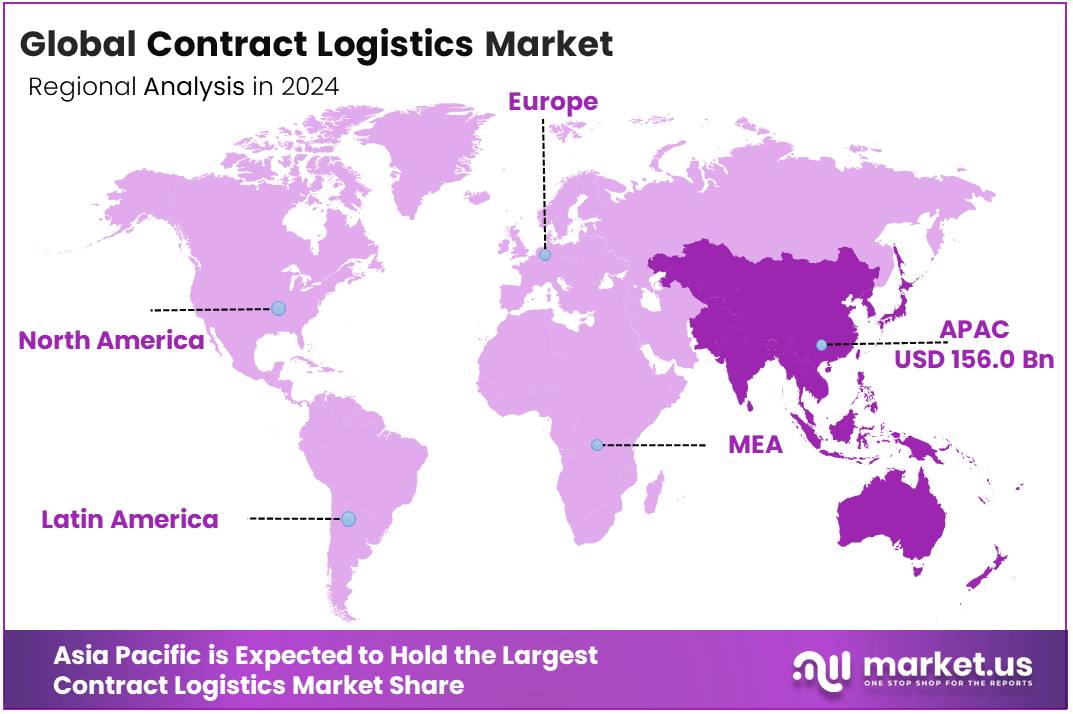

- Asia Pacific led the market with a 34.4% share (valued at USD 156.0 billion) in 2024, driven by strong manufacturing and e-commerce growth in China, India, and Southeast Asia.

Service Analysis

Transportation Dominates with 34.7% in Contract Logistics Market in 2024

In 2024, the transportation segment maintained its dominance in the contract logistics market with a significant share of 34.7%. This dominance is driven by the continuous growth of e-commerce, the need for efficient and cost-effective delivery solutions, and the increasing global trade activities. Transportation services include road, rail, air, and sea logistics, which are essential for moving goods across vast distances.

The aftermarket logistics segment also holds a considerable position in the market, primarily due to the increasing demand for spare parts and maintenance services across industries. As industries evolve, the need for efficient aftermarket logistics solutions to support product lifecycles remains critical.

Warehousing services are experiencing steady growth as well, fueled by the increasing demand for inventory management, storage, and fulfillment solutions. This is largely attributed to the rise of online shopping, which requires advanced warehousing systems.

Distribution services, while slightly smaller in comparison, remain integral to supply chain operations, facilitating the movement of goods to various locations, including retail and distribution centers. Other services in the market continue to evolve, focusing on niche logistics requirements across different sectors.

Type Analysis

Outsourcing Leads with 55.6% in Contract Logistics Market in 2024

Outsourcing has become the dominant model in the contract logistics market, accounting for 55.6% of the market share in 2024. The appeal of outsourcing logistics operations to third-party providers is primarily driven by the need for businesses to reduce costs, improve efficiency, and focus on their core competencies. As a result, many companies are leveraging third-party logistics providers for warehousing, transportation, and distribution solutions.

In contrast, insourcing, though significant, holds a smaller portion of the market. It involves businesses managing logistics operations in-house, which offers greater control over supply chain activities but can be more resource-intensive. While some companies continue to favor insourcing for sensitive or specialized operations, the flexibility and scalability of outsourcing have made it the preferred choice for many businesses.

As the logistics landscape continues to evolve, the trend toward outsourcing is expected to remain strong, driven by technological advancements, globalization, and the growing complexity of supply chain management. Companies are increasingly outsourcing to leverage the expertise, technology, and global reach offered by third-party providers.

Transportation Mode Analysis

Roadways Holds the Largest Share in Transportation Mode in Contract Logistics Market in 2024

Roadways transportation continues to dominate the contract logistics market in 2024, thanks to its flexibility, cost-effectiveness, and vast infrastructure. The road transportation segment represents the bulk of logistics activities, with companies relying heavily on trucks and other vehicles to move goods both regionally and nationally. Road transport offers advantages in terms of accessibility and the ability to reach nearly all locations, including remote areas.

Waterways transportation holds a strong position, especially for the movement of bulk goods over long distances. However, its growth is often linked to global trade and port logistics. In contrast, airways are generally used for high-value, time-sensitive shipments, though they represent a smaller share due to the higher costs involved.

Railways, while effective for moving large quantities of goods over long distances, account for a smaller portion of the market. Rail transport is often more economical than road transport but is limited by infrastructure and geographical constraints. As businesses continue to optimize their supply chains, a mix of these transportation modes is employed to achieve the most cost-effective and efficient solutions.

Industry Vertical Analysis

Retail & E-Commerce Dominates with Strong Position in Contract Logistics Market in 2024

In 2024, the retail and e-commerce sector holds a dominant position in the contract logistics market, benefiting from a surge in online shopping and changing consumer behaviors. Retail & e-commerce logistics require efficient and scalable supply chains, driving the demand for advanced warehousing, order fulfillment, and last-mile delivery solutions. This vertical’s growth continues to be fueled by increasing consumer demand for faster delivery times and a wider variety of products.

The automotive sector also remains a key player in the logistics market, with a focus on managing the movement of parts and finished vehicles. As global supply chains for automotive manufacturing become more complex, logistics providers are increasingly relied upon to manage production schedules, inventory, and distribution efficiently.

The pharma and healthcare sectors are becoming increasingly important, with rising demand for temperature-sensitive products and regulated logistics services. Additionally, the high-tech and electronics industries require specialized logistics services for managing delicate and valuable items, while aerospace and defense logistics demand highly secure and precise operations. Each of these sectors presents unique challenges and opportunities for logistics providers to cater to specific needs.

Key Market Segments

By Service

- Transportation

- Aftermarket Logistics

- Distribution

- Warehousing

- Other

By Type

- Outsourcing

- Insourcing

By Transportation Mode

- Roadways

- Waterways

- Airways

- Railways

By Industry Vertical

- Retail & E-Commerce

- Automotive

- Pharma & Healthcare

- High-Tech & Electronics

- Industrial & Manufacturing

- Aerospace & Defense

- Other

Drivers

Expansion of E-commerce Drives the Need for Efficient Contract Logistics

The expansion of e-commerce has greatly influenced the growth of the contract logistics market. As online shopping continues to surge, businesses face a higher volume of orders that need to be processed, stored, and shipped quickly. This has created a need for efficient logistics solutions that can manage the growing demand.

E-commerce companies, in particular, require third-party logistics providers who can offer comprehensive services, from warehousing to last-mile delivery. Moreover, the pressure for faster delivery times and seamless customer experiences is pushing businesses to adopt more organized, reliable, and technologically advanced logistics solutions.

As a result, the demand for sophisticated contract logistics services has risen sharply. Logistics companies that can offer scalability and flexibility, along with innovative solutions to handle the complexities of e-commerce, will be well-positioned to capitalize on this growing demand, making e-commerce a major driver for the logistics industry’s growth.

Restraints

High Initial Investment and Complex Regulations Hamper Market Growth

One of the significant challenges facing the contract logistics market is the high initial investment required to establish or upgrade logistics networks. Logistics providers need significant capital to build the infrastructure necessary for operations, including warehouses, transportation fleets, and advanced IT systems.

For new entrants, these high startup costs can be a considerable barrier to entry. Additionally, the logistics market is hindered by complex and varying regulatory frameworks across different countries. Each region has its own customs, tax regulations, and compliance standards, making it difficult for logistics providers to manage operations smoothly across borders.

These regulatory challenges can result in delays, fines, and added operational costs, which may discourage some companies from expanding into new markets. As a result, the combination of high upfront investment and complex regulations can slow down the growth and expansion of contract logistics services in the global market.

Growth Factors

Green Logistics and Expanding Global Reach Offer Growth Potential

There are several growth opportunities in the contract logistics market, primarily driven by sustainability trends and expansion into emerging markets. One significant opportunity is the growing demand for green logistics solutions, where companies are striving to reduce their carbon footprints.

Consumers and businesses alike are becoming more environmentally conscious, prompting logistics providers to adopt eco-friendly practices, such as using electric vehicles, optimizing delivery routes, and employing sustainable packaging. This shift toward green logistics provides companies with an opportunity to stand out and attract customers who value sustainability. Additionally, developing regions like Asia, Africa, and Latin America offer significant untapped potential.

As these economies continue to grow, there is an increasing need for efficient logistics solutions to support rising consumer demand and expanding industries. These emerging markets provide a lucrative opportunity for logistics providers to expand their operations and cater to new customers, fueling growth in the contract logistics market.

Emerging Trends

Robotics, Predictive Analytics, and Real-time Tracking Drive Market Innovation

Innovation is a key driver in the contract logistics market, with technology playing a central role in enhancing operational efficiency. One of the most notable trends is the use of robotics and automation in warehouses, which allows logistics companies to streamline their processes. Automated systems improve accuracy, speed up picking and packing operations, and help manage large volumes of goods, leading to significant cost savings. Predictive analytics is also gaining momentum in the logistics industry.

Companies are increasingly using data-driven forecasting tools to predict demand, optimize inventory levels, and improve delivery routes. This helps businesses reduce waste, avoid stockouts, and offer faster delivery times. Furthermore, the growing demand for real-time tracking and visibility solutions is transforming customer expectations.

Consumers now want to track their shipments at every step of the delivery process, and logistics providers are investing in advanced tracking technologies to meet this demand. These trends in technology are enhancing service quality, efficiency, and customer satisfaction in the contract logistics market.

Regional Analysis

Asia Pacific Dominates Contract Logistics Market with 34.4% Share, Valued at USD 156.0 Billion

The Asia Pacific region leads the market with a commanding 34.4% share, amounting to USD 156.0 billion, driven by robust manufacturing sectors and expanding retail and e-commerce networks, particularly in China, India, and Southeast Asia. This region benefits from significant investments in logistics infrastructure and technology adoption, positioning it as a critical hub for international trade and supply chain operations.

Regional Mentions:

Europe maintains a strong position in the market, supported by advanced logistics and transportation networks, particularly in Germany, the UK, and France. The region focuses on sustainability and efficiency, integrating advanced technologies such as AI and IoT to enhance logistics operations.

North America follows closely, with a highly developed e-commerce sector fueling demand for sophisticated contract logistics services. The region’s emphasis on technological integration and innovation continues to drive market growth, particularly in the United States and Canada.

Middle East & Africa region is witnessing rapid growth in contract logistics, spurred by economic diversification efforts and the development of logistics hubs in the UAE, Saudi Arabia, and South Africa. This region is increasingly focusing on enhancing its logistics infrastructure to support trade with Asia and Europe.

Latin America shows promising growth potential, with Brazil and Mexico leading the way. The region is improving its logistics capabilities to overcome challenges related to transportation and regulatory frameworks, aiming to better integrate into the global market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global contract logistics market is undergoing dynamic transformation, led by the strategic efforts of major players like CEVA Logistics, United Parcel Service, Inc. (UPS), and Ryder System, Inc. CEVA Logistics is expanding aggressively across emerging markets, focusing on tailored sector-specific solutions to strengthen its market positioning.

UPS continues to leverage its extensive logistics expertise, enhancing operations with advanced warehouse automation and real-time tracking technologies. Meanwhile, Ryder System, Inc. is capitalizing on the growth of e-commerce by expanding its e-fulfillment and omnichannel supply chain capabilities, catering to the evolving demands of retail and consumer sectors.

Kuehne + Nagel International AG is driving forward with digital innovation, optimizing customer engagement through advanced logistics platforms and data-driven solutions. GXO Logistics, Inc. is building a strong reputation for delivering scalable and customized outsourced supply chain solutions, positioning itself as a key partner for complex logistics needs.

GEODIS SA is investing heavily in warehouse infrastructure and value-added services, supporting its global multimodal capabilities. Similarly, DB Schenker is focusing on integrating digital technologies to improve operational efficiency and create more resilient supply chains.

DSV A/S is enhancing its service offerings through strategic technology integration and a strong focus on flexible logistics solutions. Nippon Express Co., Ltd. is strengthening its cross-border logistics services, particularly within Asia, to capture rising trade flows in the region.

DHL Supply Chain continues to set industry benchmarks with its leadership in warehouse automation, green logistics initiatives, and strategic customer partnerships. These collective efforts are reshaping the global contract logistics landscape with innovation, efficiency, and customer-centric strategies at the forefront.

Top Key Players in the Market

- CEVA Logistics

- United Parcel Service, Inc.

- Ryder System, Inc.

- Kuehne + Nagel International AG

- GXO Logistics, Inc.

- GEODIS SA

- DB Schenker

- DSV A/S

- Nippon Express Co., Ltd.

- DHL Supply Chain

Recent Developments

- In January 2024, CEVA Logistics announced its plan to acquire Wincanton for $720 million, strengthening its footprint in the UK logistics market. The acquisition aims to boost CEVA’s supply chain capabilities across multiple sectors.

- In February 2024, DHL Supply Chain revealed a $200 million investment to expand its Life Sciences and Healthcare logistics operations. This move is designed to meet the rising demand for specialized healthcare logistics services.

- In August 2024, KSH INFRA committed Rs 450 crore towards the development of its first industrial and logistics park. This investment supports the company’s strategy to cater to India’s growing warehousing and logistics demands.

- In April 2025, DHL Group announced a €2 billion investment to enhance its global logistics infrastructure and technological capabilities. This significant funding underscores DHL’s focus on sustainability, digitalization, and network expansion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 459.1 Billion |

| Forecast Revenue (2034) | USD 982.0 Billion |

| CAGR (2025-2034) | 7.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service (Transportation, Aftermarket Logistics, Distribution, Warehousing, Other), By Type (Outsourcing, Insourcing), By Transportation Mode (Roadways, Waterways, Airways, Railways), By Industry Vertical (Retail & E-Commerce, Automotive, Pharma & Healthcare, High-Tech & Electronics, Industrial & Manufacturing, Aerospace & Defense, Other) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | CEVA Logistics, United Parcel Service, Inc., Ryder System, Inc., Kuehne + Nagel International AG, GXO Logistics, Inc., GEODIS SA, DB Schenker, DSV A/S, Nippon Express Co., Ltd., DHL Supply Chain |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |