Quick Navigation

Report Overview

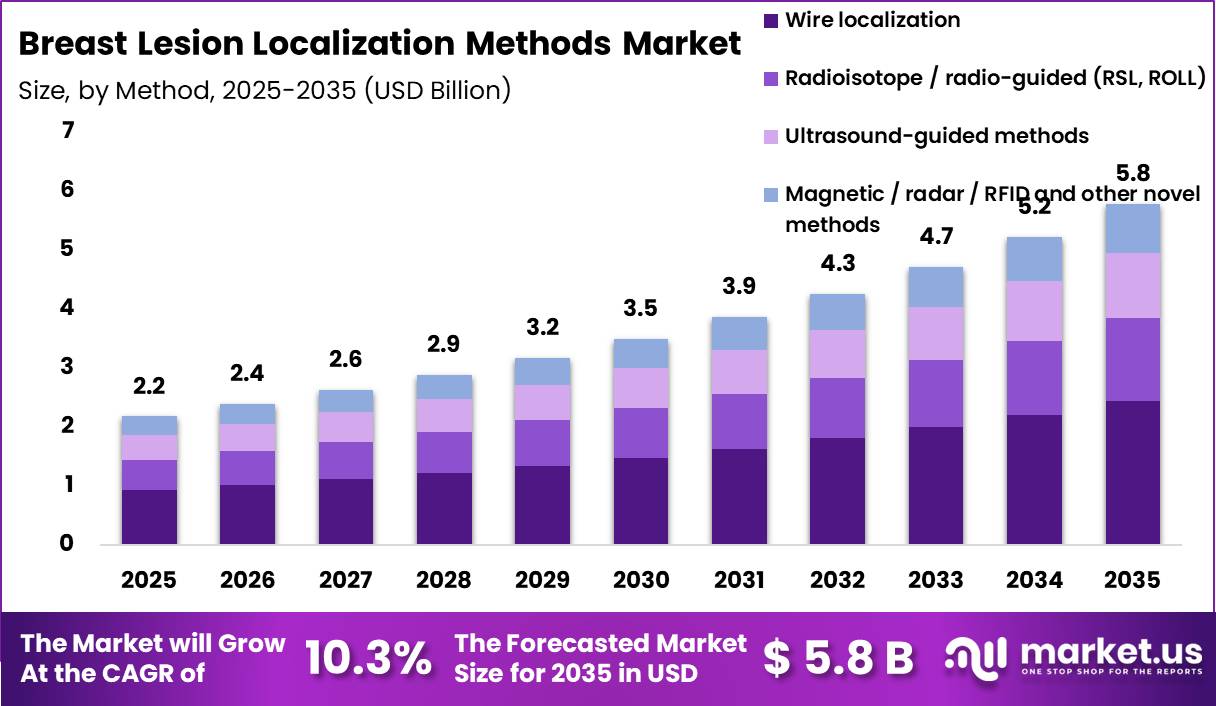

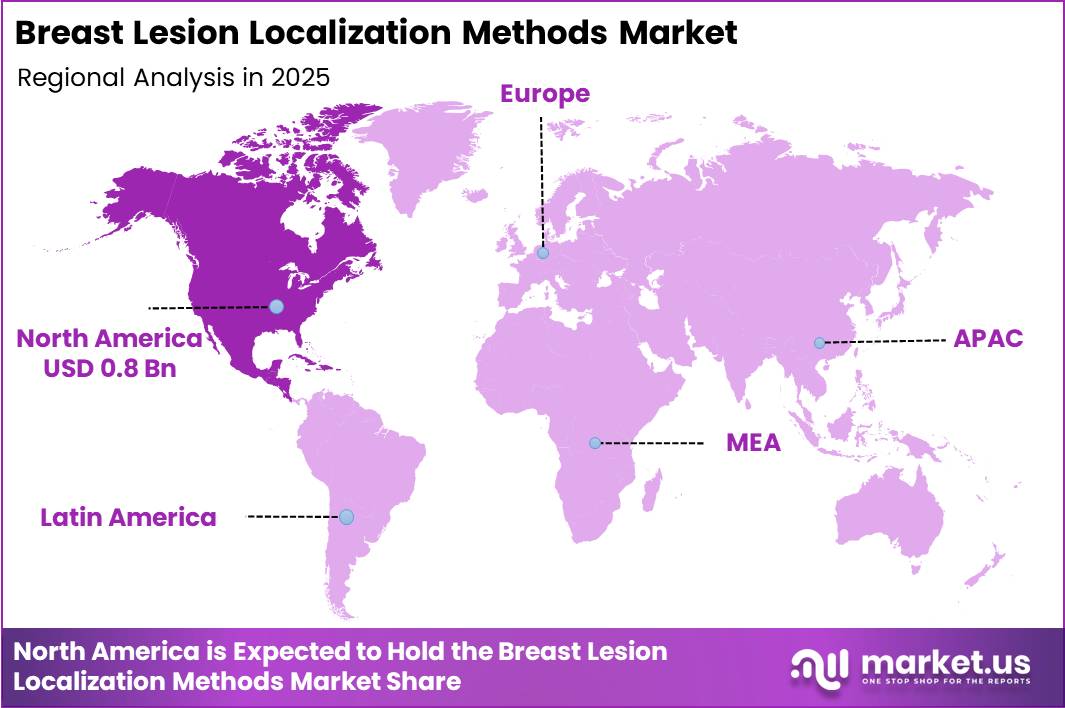

Global Breast Lesion Localization Methods Market size is expected to be worth around US$ 5.8 Billion by 2035 from US$ 2.2 Billion in 2025, growing at a CAGR of 10.3% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 35.8% share, holding USD 0.8 Billion in revenue.

The breast lesion localization methods market is shifting from conventional wire-based workflows toward more precise, imaging-integrated, and wire-free solutions. While wire localization still holds a significant position due to its widespread clinical familiarity and established hospital infrastructure, its limitations in scheduling flexibility, patient comfort, and workflow coordination are driving gradual displacement.

This transition is being shaped by growing adoption of radioactive seed, magnetic seed, RFID, and radar-based localization systems, supported by ultrasound, mammography, tomosynthesis, and MRI guidance for marker placement or direct lesion visualization.

Hospitals remain the central adoption hub, balancing legacy systems with newer technologies designed to support breast-conserving surgery, improve scheduling flexibility, and potentially reduce positive-margin or re-excision risk in selected clinical settings. As a result, competition is increasingly centered on procedural efficiency, interoperability with imaging systems, and clinical precision.

Demand growth is strongly supported by rising breast cancer incidence and the global shift toward early detection and breast-conserving surgical approaches. This has elevated the importance of accurate lesion localization as a critical factor in surgical success and post-operative outcomes. Healthcare providers are increasingly prioritizing solutions that integrate seamlessly into existing radiology and surgical workflows while improving intraoperative flexibility and accuracy.

Expansion of advanced imaging infrastructure in tertiary care settings is further enabling adoption of non-wire techniques, while manufacturers are focusing on systems that reduce procedural complexity and improve operating room efficiency. Collectively, these factors are repositioning lesion localization technologies as essential enablers of precision-driven breast cancer surgery.

Key Takeaways

- Market Size: Global Breast Lesion Localization Methods Market size is expected to be worth around US$ 5.8 Billion by 2035 from US$ 2.2 Billion in 2025.

- Market Share: The market is growing at a CAGR of 10.3% during the forecast period from 2026 to 2035.

- Method Analysis: Wire Localization dominated the market, constituting 42.3% of the total market share.

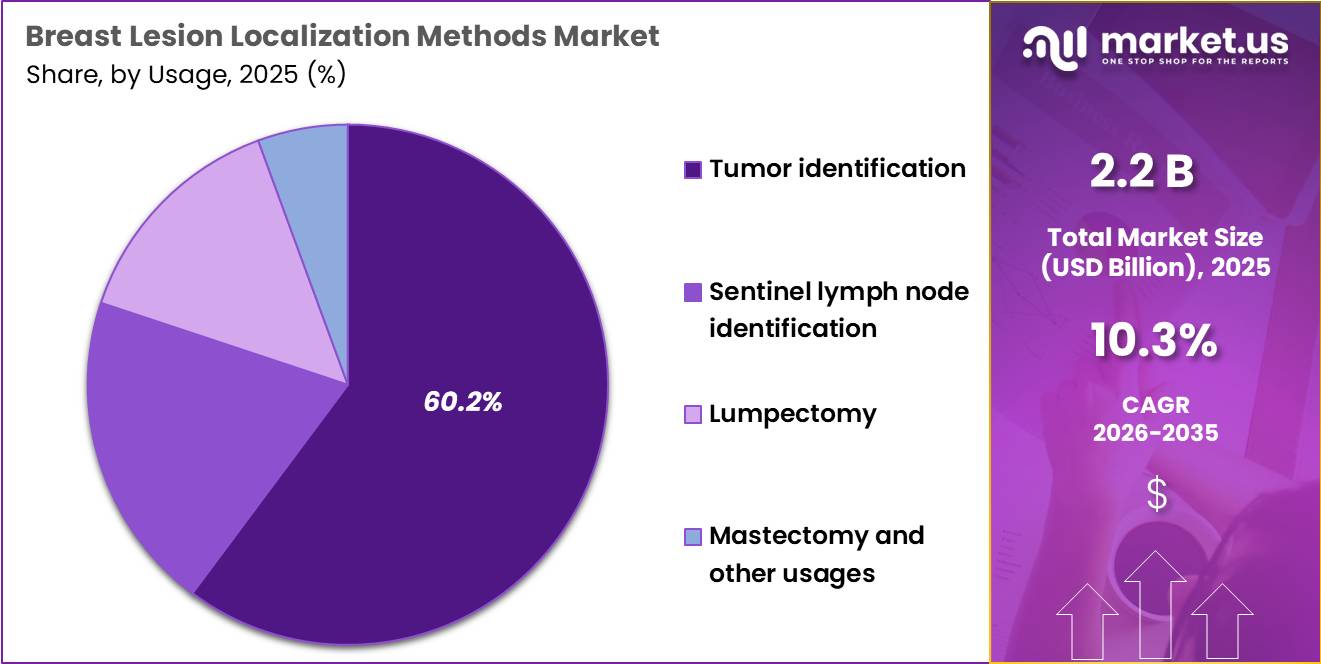

- Usage Analysis: Tumor Identification dominated the Breast Lesion Localization Methods Market, with a substantial market share of around 60.2%, driven by the primary clinical indication of marking non-palpable breast lesions for precise surgical excision in breast-conserving surgery programs.

- End Users Analysis: Hospitals dominated with a 55.7% market share.

- Regional Analysis: In 2025, North America was the most dominant region in the Breast Lesion Localization Methods market, accounting for 35.8% of total global revenue.

Method Analysis

Wire Localization Represents the Key Revenue-Generating Method Segment in the Global Breast Lesion Localization Methods Market.

Wire localization remains the dominant method in the global breast lesion localization methods market, accounting for 42.3% share, driven by its long-standing clinical adoption, procedural familiarity, and strong integration within established hospital workflows. Its continued leadership is primarily supported by cost efficiency, minimal infrastructure requirements, and consistent procedural outcomes, making it the preferred choice in high-volume surgical oncology environments.

Despite the gradual shift toward advanced alternatives, many healthcare systems continue to rely on wire-based techniques due to the high cost and training requirements associated with transitioning to newer localization technologies. This has ensured sustained dominance, particularly in hospitals where operational continuity and workflow predictability remain critical priorities.

At the same time, the market is witnessing a steady shift toward advanced localization approaches, particularly radioisotope/radio-guided and ultrasound-guided systems, which are increasingly adopted in modern oncology centers to improve surgical precision and reduce re-excision rates. These methods are gaining preference in settings focused on breast-conserving surgery outcomes and enhanced intraoperative flexibility.

- In October 2025, Merit Medical Systems, Inc. announced that its SCOUT® Radar Localization technology had been used in more than 750,000 patients worldwide, reflecting the gradual transition toward wire-free localization while conventional wire localization continues to remain the most widely used approach globally.

Meanwhile, emerging magnetic, radar, and RFID-based technologies are gradually gaining traction as next-generation alternatives, signaling a slow but clear structural shift in clinical practice toward more precise, minimally invasive localization systems.

Usage Analysis

Tumor Identification Represents the Leading Usage Segment in the Global Breast Lesion Localization Methods Market.

Tumor identification dominates the market with a 60.2% share, driven by the essential role of localization technologies in accurately identifying and targeting non-palpable breast lesions during diagnosis and surgery. Growing breast cancer screening rates and increasing adoption of breast-conserving procedures have strengthened demand for precise localization methods, as accurate tumor identification directly influences surgical margins, treatment outcomes, and re-excision rates.

The segment also benefits from the integration of localization technologies into standard diagnostic and surgical oncology workflows across hospitals and specialized breast care centers. The segment’s leadership is further supported by healthcare providers focus on improving procedural accuracy and operational efficiency.

- In September 2024, MOLLI Surgical Inc. expanded clinical adoption initiatives for its wire-free breast lesion localization technology, highlighting the industry’s emphasis on enhancing tumor targeting and surgical precision.

End-User Analysis

Hospitals Represent the Dominant End User Segment in the Global Breast Lesion Localization Methods Market

Hospitals account for the largest share of the breast lesion localization methods market, representing 55.7% of total demand. Their dominance is driven by the concentration of breast cancer diagnosis, imaging, localization procedures, and surgical interventions within hospital settings.

Hospitals possess the multidisciplinary infrastructure required for breast lesion localization, including radiology departments, surgical oncology teams, advanced imaging systems, and post-operative care capabilities. The growing volume of breast-conserving surgeries and complex oncology procedures further reinforces hospitals as the primary users of localization technologies.

The segment also benefits from greater investment capacity for adopting advanced localization systems and integrating them into existing surgical workflows. Hospitals are increasingly prioritizing technologies that improve procedural accuracy, reduce re-excision rates, and enhance patient outcomes.

- In March 2025, Hologic, Inc. published clinical findings demonstrating the high accuracy of its LOCalizer™ RFID system for preoperative breast lesion localization, supporting broader adoption of advanced localization technologies across hospital-based breast surgery programs.

While ambulatory surgical centers, diagnostic centers, and oncology clinics are gradually increasing utilization of localization technologies, hospitals remain the central hub for breast lesion management due to their comprehensive clinical capabilities and high procedural volumes.

Key Market Segments

By Method

- Wire Localization

- Radioisotope / Radio-guided (RSL, ROLL)

- Ultrasound-guided Methods

- Magnetic / Radar / RFID and Other Novel Methods

By Usage

- Tumor Identification

- Sentinel Lymph Node Identification

- Lumpectomy

- Mastectomy and Other Usages

By End User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Diagnostic Centers

- Oncology Clinics & Academic Institutes

Driver

Dense-breast notification and supplemental imaging lesion discovery

The U.S. MQSA dense-breast notification requirement became effective on September 10, 2024, and facilities must now include an overall breast-density assessment along with specific patient notification statements in mammography reporting.

This development is commercially relevant because dense-breast awareness tends to increase shared decision-making around supplemental imaging, and supplemental imaging has historically detected additional cancers that frequently present as non-palpable targets requiring localisation.

Prior evidence cites additional cancer detection with ultrasound at 4.4 per 1,000 exams and with MRI ranging from 3.5 to 28.6 per 1,000 following negative mammography, while tomosynthesis added 1.4 to 2.5 cancers per 1,000 compared with mammography alone.

As facilities respond with greater use of ultrasound, MRI, and contrast-enhanced workups for dense breast populations, the downstream procedure pool expands for lesion marking technologies, particularly wire-free platforms favoured in complex, imaging-led diagnostic pathways.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wire-free shift from same-day WGL to RFID/radar/magnetic workflows | +2.1% | North America core, Western Europe, Australia, Japan, tertiary APAC centers | Short term (≤ 2 years) |

| Dense-breast notification and supplemental imaging lesion discovery | +1.7% | U.S. core, Canada, EU screening markets, developed APAC | Short term (≤ 2 years) |

| Margin reduction and re-excision control in breast-conserving surgery | +1.4% | U.S., EU, UK, South Korea, urban China | Medium term (2-4 years) |

| Outpatient throughput and radiology-OR decoupling economics | +1.2% | U.S. HOPD/ASC, private EU hospitals, Gulf, private APAC | Short term (≤ 2 years) |

| Rising early-stage breast cancer load and screening access expansion | +1.8% | Global, with strongest incremental volumes in APAC, Latin America, MENA | Medium term (2-4 years) |

| Radiation-free compliance preference over seed-based methods | +0.9% | Community hospitals in U.S./EU, mid-tier APAC hospitals | Medium term (2-4 years) |

Challenge

Wire-Dependence Workflow Inertia as a Structural Adoption Barrier

Persistent reliance on wire-guided localization (WGL) creates workflow inertia in breast surgery, with many hospitals still using wires for 60–70% of non-palpable lesion localizations despite strong evidence supporting wire-free alternatives.

Ingrained day-of-surgery scheduling, tight radiology–surgery coordination, and legacy equipment extend pre-operative localization to 45–60 minutes per case and constrain daily throughput by 10–20% compared with wire-free approaches that allow placement days in advance.

Although wire-free systems have demonstrated lower re-excision and margin positivity rates, hospitals typically face a 24–36-month change-management period to update protocols, retrain staff, and rebalance OR blocks. This slow conversion dampens near-term adoption and trims achievable market CAGR by an estimated 1.2% points across North America and Western Europe.

To overcome this inertia, vendors and providers must invest in sustained clinical education, integrated radiology–surgery pathways, and redesigned patient flows that decouple localization from OR time. Target outcomes include a 15–20% reduction in day-of-surgery localization minutes and a 3–5 percentage-point improvement in margin outcomes within 2–4 years.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Wire-dependence workflow inertia | -1.2% | North America, Western Europe | Medium term (2–4 years) |

| Capital-intensive tech upgrades | -1.0% | North America core, APAC growth hubs | Long term (≥ 4 years) |

| Talent & training bottlenecks | -0.8% | EU regulatory hubs, APAC tertiary centers | Medium term (2–4 years) |

| Interdepartmental scheduling friction | -0.7% | North America, EU, urban APAC | Short term (≤ 2 years) |

| Data integration & traceability gaps | -0.9% | North America, EU, advanced APAC | Long term (≥ 4 years) |

| Reimbursement & value-evidence lag | -1.1% | North America, Europe | Medium term (2–4 years) |

Restraints

Fragmented Reimbursement and Coding Burden as an Adoption Brake

Fragmented reimbursement and complex coding materially slow adoption of advanced breast localization technologies, reducing market CAGR by an estimated 2.2% points over 2026 to 2030. Bundled payment rules, particularly policies from the Centers for Medicare & Medicaid Services that treat guidance and post procedure imaging as non separately payable, cut professional and facility revenue per case by roughly 8 to 12 percent.

This weakens the investment case for wire free or RFID based systems that add USD 150 to 400 in per case device cost without reliable incremental reimbursement.Payer heterogeneity compounds the issue. While screening mammography is broadly covered, reimbursement for adjunct imaging and localization devices is inconsistent across commercial plans, often shifting USD 500 to 1,200 per episode to patients in high deductible plans and dampening procedure volumes.

On the operational side, navigating multiple CPT codes and local coverage determinations increases billing complexity, raising administrative costs by 3 to 5 percent of departmental revenue and elevating denial rates on complex claims.

Collectively, these financial and coding frictions delay capital investment by 12 to 24 months, compress service line margins by up to 150 basis points, and divert spending toward more predictable modalities. The net effect is a meaningful deceleration of what would otherwise be double digit market growth.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented reimbursement & coding burden | -2.2% | North America core, selected EU | Medium term (2-4 years) |

| Capital intensity & OR workflow rigidity | -1.6% | North America core, EU, high-income APAC | Medium term (2-4 years) |

| Radioactive & regulatory compliance friction | -1.2% | North America core, EU, APAC corridors | Short–Medium term (≤ 4 years) |

| Skill gaps & training lag in advanced localization | -1.0% | EU, APAC emerging, LatAm | Medium–Long term (≥ 3 years) |

| Access disparity in LMIC screening infrastructure | -1.8% | Asia (LMIC), Africa, LatAm | Long term (≥ 4 years) |

Opportunity

Magnetic Seed and Tracer Expansion into Multi-Site Oncologic Localization

Magnetic markers and tracers cleared by the U.S. Food and Drug Administration for breast tumor and sentinel lymph-node localization remain under-utilized beyond breast lumpectomy, creating a significant adjacent opportunity.

Clinical data show magnetic systems perform comparably to radioisotope-based methods while eliminating radiation exposure and simplifying scheduling and handling, yet 15–25% of oncology cases across breast, melanoma, and select gastrointestinal indications still rely on radioisotopes. Rising cancer incidence in Asia and high mortality-to-incidence ratios in parts of Africa are straining nuclear medicine capacity, positioning magnetic localization as a scalable alternative.

Shifting 30–50% of eligible cases to radiation-free workflows could ease isotope supply constraints and facility dependence. Commercially, extending magnetic platforms into multi-tumor pathways supports platform pricing with modest premiums and lower per-case logistics costs. This expansion could add USD 200–350 million in annual revenues by 2035 and contribute roughly 1.8% points of CAGR upside versus a breast-only adoption scenario.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| AI-augmented imaging triage & localization platforms | +2.0% | EU, North America, high-SDI Asia | Medium term (2-4 years) |

| Magnetic seed & tracer expansion into multi-site oncologic localization | +1.8% | North America core, EU, APAC urban | Medium term (2-4 years) |

| Value-based, bundled breast care pathways with localization as a reimbursable node | +1.5% | North America, EU, select LATAM | Long term (≥ 4 years) |

| Outpatient, minimally invasive localization hubs in emerging Asia & Africa | +2.2% | APAC emerging, Africa, Middle East | Long term (≥ 4 years) |

| Integrated lymph-node and breast lesion localization systems | +1.3% | North America, EU, high-volume tertiary centers globally | Medium term (2-4 years) |

| Remote-guided localization and tele-mentoring networks | +1.0% | Global, with focus on APAC and LATAM secondary cities | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Supply Chain Localization and Regulatory Pressure.

Geopolitical factors are increasingly shaping the breast lesion localization methods market through tighter regulatory oversight and growing emphasis on healthcare self-reliance. Radioisotope-based and advanced imaging-guided localization systems face strict compliance requirements, particularly in regions strengthening medical device safety and radiation handling regulations. At the same time, government-led breast cancer screening initiatives and healthcare modernization programs are supporting steady adoption of localization technologies across both developed and emerging markets.

Supply chain localization and trade diversification are also influencing manufacturing and procurement strategies, as healthcare systems prioritize resilience and reduced dependence on single-region suppliers. This is encouraging manufacturers to expand regional production and strengthen distribution networks.

- In 2025, Cook Medical LLC expanded its operational footprint across key international markets to improve supply continuity for interventional products, reflecting the broader industry shift toward localized manufacturing and risk mitigation.

Regional Analysis

North America Held the Largest Share of the Global Breast Lesion Localization Methods Market.

North America dominates the global breast lesion localization methods market with a 35.8% share, driven by a highly advanced breast cancer screening ecosystem and early adoption of image-guided surgical technologies.

Strong integration between radiology and surgical oncology departments enables efficient execution of diagnostic localization and breast-conserving procedures, while high procedural volumes and robust reimbursement systems sustain strong demand across hospitals and cancer centers. Continuous investment in advanced imaging infrastructure further supports the shift toward more precise and workflow-efficient localization methods.

The region’s leadership is reinforced by rapid adoption of minimally invasive, precision-based surgical workflows focused on improving outcomes and reducing re-excision rates. Europe is steadily expanding, while Asia Pacific is growing rapidly due to rising cancer incidence and improving diagnostic infrastructure. Latin America and the Middle East & Africa are gradually increasing adoption as oncology care access and healthcare infrastructure continue to develop.

- In October 2025, Merit Medical Systems, Inc. announced that more than 1,100 healthcare facilities worldwide had adopted its SCOUT® Radar Localization platform, reflecting the strong uptake of advanced breast lesion localization technologies across North American breast care centers and reinforcing the region’s leadership in precision-guided breast surgery.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global breast lesion localization methods market is moderately consolidated, with the top tier dominated by a mix of large diversified medical device companies and specialized breast imaging and surgical technology firms. Leading players such as Hologic, Inc., Becton, Dickinson and Company (BD), Merit Medical Systems, Inc., Cook Medical LLC, and Endomagnetics Ltd collectively shape innovation direction, particularly in wire-free localization, RFID- and magnetic-based systems, and integrated surgical navigation workflows.

The market structure is characterized by strong hospital-driven procurement, where purchasing decisions are increasingly influenced by procedural accuracy, workflow efficiency, and compatibility with breast-conserving surgery protocols. Beneath this leading group, the market remains fragmented, with regional and niche players competing on cost efficiency, localized distribution, and procedural specialization.

Competitive advantage is increasingly shifting toward companies capable of delivering integrated, minimally invasive solutions that combine localization accuracy with improved intraoperative usability. Market leaders are focusing on expanding wire-free portfolios, strengthening clinical adoption programs, and deepening partnerships with hospitals and oncology centers to accelerate workflow integration. Differentiation is being driven less by standalone devices and more by ecosystem-based offerings that support end-to-end breast cancer surgical workflows.

Major Key Players

- Hologic, Inc.

- Becton, Dickinson and Company (BD)

- Leica Biosystems Nussloch GmbH

- Merit Medical Systems, Inc.

- Cook Medical LLC

- SOMATEX Medical Technologies GmbH (Hologic Inc.)

- Argon Medical Devices, Inc.

- MOLLI Surgical Inc.

- Cianna Medical (Hologic)

- Endomagnetics Ltd

- STERYLAB S.r.l.

- Theragenics Corporation

- MDL SRL

- Devicor Medical Products Inc.

- Ranfac Corporation

- Others

Key Development

- In March 2025, Hologic, Inc. (following its acquisition of Endomagnetics Ltd) systematically expanded the clinical adoption of the Magseed® magnetic seed localization technology across multiple hospital networks in North America and Europe, supporting a broader transition toward wire-free breast lesion localization workflows [INDEX].

- In June 2025, Hologic, Inc. advanced the integration of wire-free localization solutions within breast conservation programs, strengthening alignment between imaging systems and surgical navigation workflows to improve procedural efficiency.

- In January 2026, Becton, Dickinson and Company (BD) enhanced its interventional and biopsy portfolio with workflow-focused improvements aimed at improving precision in image-guided breast lesion detection and surgical planning.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 2.2 Billion |

| Forecast Revenue (2035) | US$ 5.8 Billion |

| CAGR (2026-2035) | 10.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Method (Wire Localization, Radioisotope / Radio-guided [RSL, ROLL], Ultrasound-guided Methods, Magnetic / Radar / RFID and Other Novel Methods), By Usage (Tumor Identification, Sentinel Lymph Node Identification, Lumpectomy, Mastectomy and Other Usages), By End User (Hospitals, Ambulatory Surgical Centers [ASCs], Diagnostic Centers, Oncology Clinics & Academic Institutes) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Hologic Inc., Becton Dickinson and Company (BD), Leica Biosystems Nussloch GmbH, Merit Medical Systems Inc., Cook Medical LLC, SOMATEX Medical Technologies GmbH (Hologic Inc.), Argon Medical Devices Inc., MOLLI Surgical Inc., Cianna Medical (Hologic), Endomagnetics Ltd, STERYLAB S.r.l., Theragenics Corporation, MDL SRL, Devicor Medical Products Inc., Ranfac Corporation, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |