Quick Navigation

Report Overview

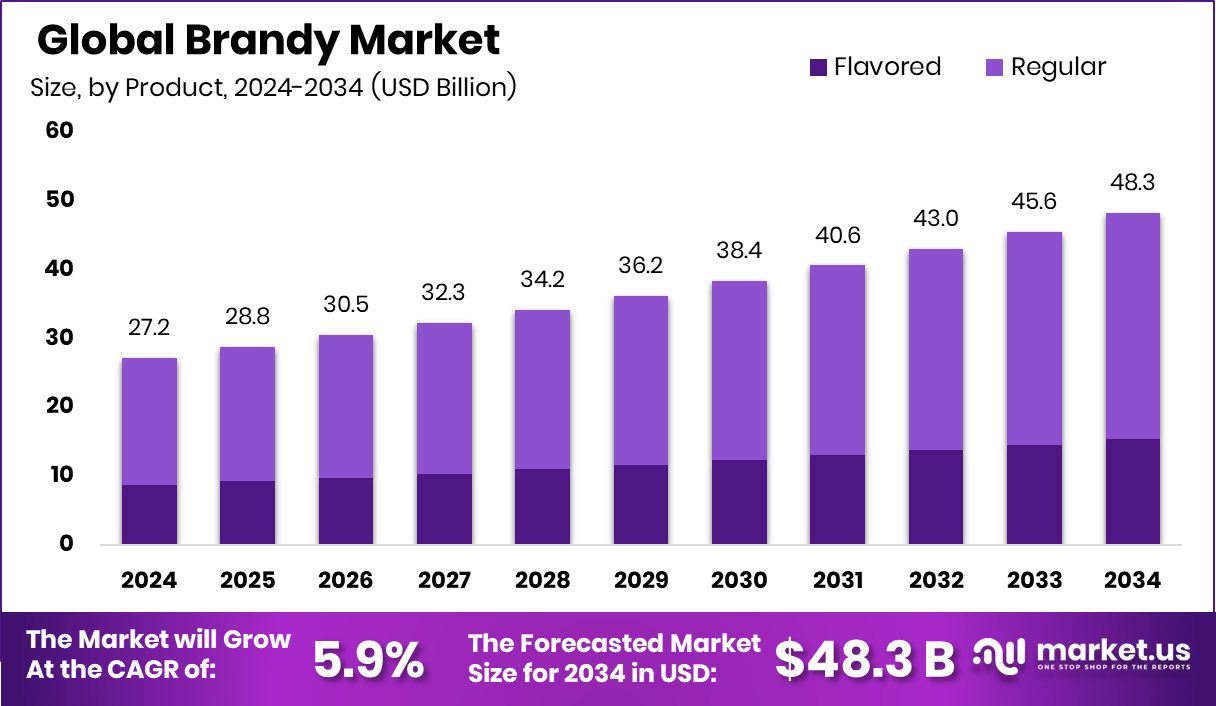

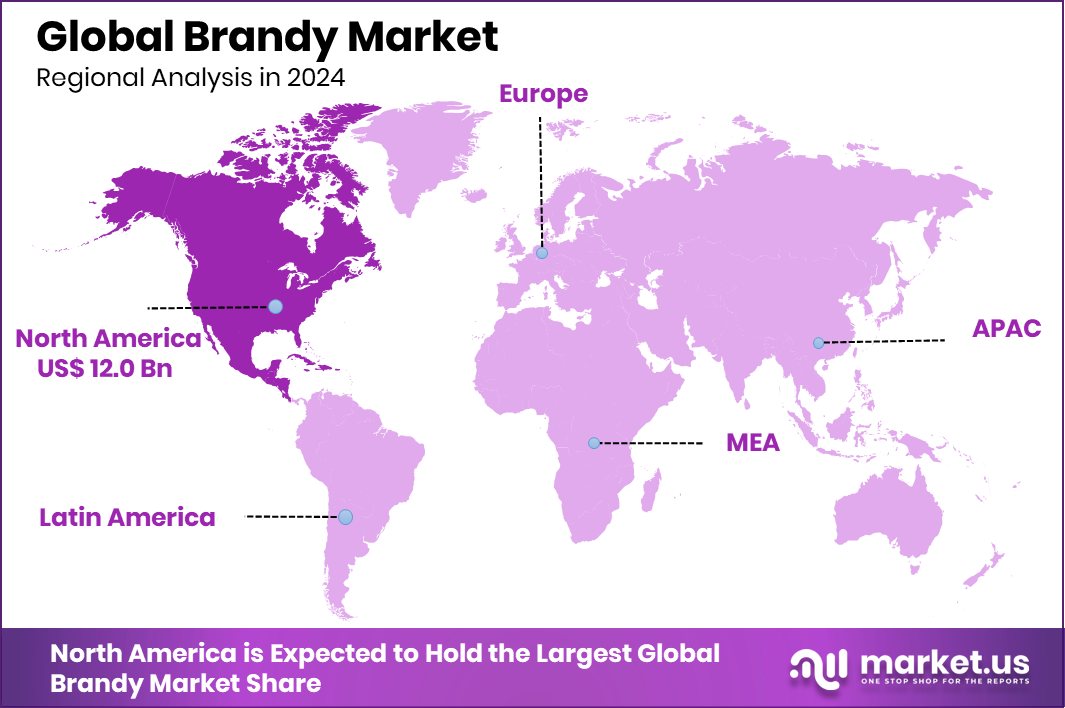

Global Brandy Market is expected to be worth around USD 48.3 billion by 2034, up from USD 27.2 billion in 2024, and grow at a CAGR of 5.9% from 2025 to 2034. Brandy sales in North America reached 44.3% market share, totaling USD 12.0 Bn.

Brandy is a distilled alcoholic beverage made by fermenting and distilling wine or other fruit juices. It typically contains 35% to 60% alcohol by volume and is aged in wooden casks to develop its rich flavor and smooth texture. Traditionally consumed as a sipping spirit, brandy is also used in cooking and various cocktail recipes. The name “brandy” comes from the Dutch word brandewijn, meaning “burnt wine,” referring to the heat used during the distillation process.

The brandy market has grown steadily in recent years due to increasing consumer interest in premium and craft spirits. As more people seek unique tasting experiences and high-quality aged liquors, brandy is gaining popularity beyond traditional demographics. Lifestyle shifts and the influence of Western drinking habits in emerging economies are also helping to broaden the consumer base for brandy. According to an industry report, Boutique Spirit Brands, a liquor startup, secures ₹80 crore in fresh funding.

Rising demand for fruit-based and flavored brandies, especially among younger consumers, is boosting global consumption. These variants appeal to those looking for sweeter and more approachable alternatives to classic spirits. In addition, brandy’s association with celebratory and festive occasions makes it a preferred choice during holidays and special events, further driving sales volumes seasonally. According to an industry report, A British brandy producer raises £2 million to support global expansion plans.

An emerging opportunity in the market lies in the expansion of online alcohol retailing. As digital platforms grow and laws evolve to support online alcohol sales, more consumers are opting for the convenience of ordering brandy through e-commerce. This shift has opened new channels for brand visibility and direct-to-consumer marketing, especially in regions with limited access to brick-and-mortar liquor outlets. According to an industry report, Coinbase Ventures participates in Moralis’ $40 million funding round.

Key Takeaways

- The global brandy market is expected to be worth around USD 48.3 billion by 2034, up from USD 27.2 billion in 2024, and grow at a CAGR of 5.9% from 2025 to 2034.

- In 2024, Regular brandy dominated the Brandy Market by product, accounting for 72.3% share.

- Cognac led the Brandy Market by product type in 2024, capturing a 38.4% market share.

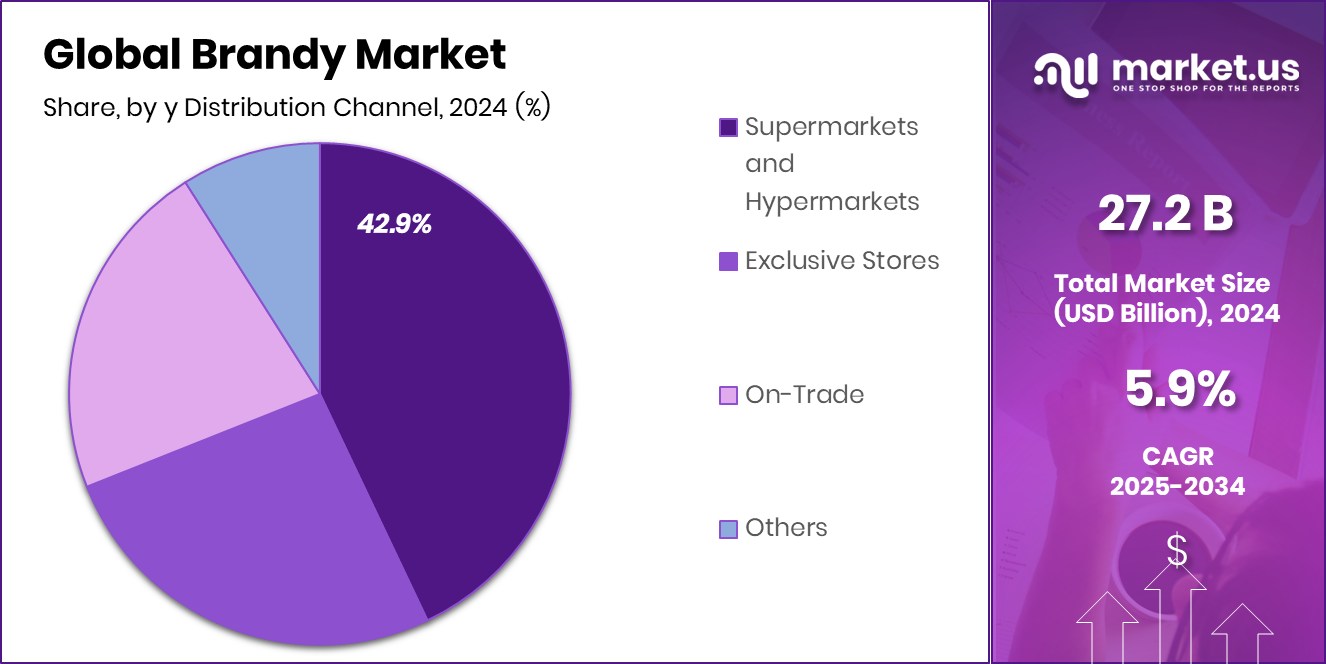

- Supermarkets and Hypermarkets held a 42.9% share in the Brandy Market’s distribution channel segment during 2024.

- Strong cultural demand and premium consumption boosted North America’s brandy market to USD 12.0 Bn.

By Product Analysis

In 2024, Regular brandy dominated with a 72.3% market share globally.

In 2024, Regular held a dominant market position in the By Product segment of the Brandy Market, with a 72.3% share. This dominance reflects the strong consumer preference for traditional brandy offerings, which continue to lead in both volume and value sales across key markets. Regular brandy maintains its appeal due to its familiarity, consistent flavor profile, and widespread availability in retail channels.

It is particularly favored in markets where brandy consumption is deeply rooted in cultural and social traditions, contributing to its consistent demand throughout the year. Additionally, its competitive pricing compared to more specialized or premium variants supports broader accessibility among diverse consumer income groups. The large share also indicates continued consumption in both household and foodservice sectors, where regular brandy is used not just as a beverage but also in culinary applications.

With established brand loyalty and widespread recognition, regular brandy remains a staple in liquor cabinets and bars, reinforcing its leadership in the segment. This performance is further bolstered by steady on-trade and off-trade sales, particularly in regions where brandy has longstanding popularity.

By Product Type Analysis

Cognac held the top spot in product type, accounting for 38.4% share.

In 2024, Cognac held a dominant market position in the By Product segment of the Brandy Market, with a 38.4% share. This strong performance highlights the continued global demand for premium and region-specific brandy offerings. Cognac, a high-quality variety produced under strict regulations in the Cognac region of France, remains a symbol of luxury and craftsmanship.

Its dominance is largely driven by consumers seeking refined taste profiles, age-specific classifications, and heritage-driven branding. The appeal of Cognac extends across both mature and emerging markets, where rising disposable incomes and a shift toward premium spirits are influencing purchasing behavior. The segment benefits from consistent demand in gifting occasions, celebratory events, and premium hospitality services, further boosting its share.

Additionally, the historical prestige and perceived exclusivity associated with Cognac elevate its status in both on-trade and off-trade channels. The 38.4% share indicates strong global distribution and recognition, particularly among brand-conscious consumers who value authenticity and aging credentials.

By Distribution Channel Analysis

Supermarkets and hypermarkets led distribution channels with a 42.9% share in sales.

In 2024, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Brandy Market, with a 42.9% share. This significant share is attributed to the widespread presence of these retail formats and their ability to offer a broad range of brandy products under one roof. Consumers prefer purchasing brandy from supermarkets and hypermarkets due to the convenience of one-stop shopping, competitive pricing, and the ability to physically compare products.

These retail outlets also invest in promotional displays, in-store tastings, and seasonal offers, which enhance customer engagement and boost sales volumes. The 42.9% share reflects the effectiveness of these strategies in influencing purchase decisions, especially in urban and semi-urban markets. Supermarkets and hypermarkets also ensure reliable stock availability and accessibility to both mass-market and premium brand variants, appealing to a wide consumer demographic.

Their strong supply chain networks further support consistent product distribution and shelf presence, maintaining brand visibility throughout the year. The dominant share confirms the continued reliance of consumers on organized retail formats for alcoholic beverage purchases, reinforcing the critical role supermarkets and hypermarkets play in the brandy market’s overall distribution ecosystem.

Key Market Segments

By Product

- Flavored

- Regular

By Product Type

- Grape Brandy

- Cognac

- Armagnac

- Fruit Brandy

- Others

By Distribution Channel

- Supermarkets and Hypermarkets

- Exclusive Stores

- On-Trade

- Others

Driving Factors

Rising Demand for Premium and Aged Brandy

One of the main driving factors for the brandy market is the growing demand for premium and aged brandy among consumers. People are now more interested in quality over quantity, and they prefer rich, well-aged spirits that offer a smoother taste and better experience. This shift is especially visible in urban areas where consumers are willing to pay more for high-end alcoholic beverages.

Aged brandy varieties, such as those labeled VSOP or XO, are becoming more popular because of their craftsmanship and unique flavors. As consumers become more educated about spirits, they are developing a deeper appreciation for brandy, helping to boost sales of premium products across both retail stores and restaurants.

Restraining Factors

High Taxes and Strict Alcohol Sale Regulations

One major factor that limits the growth of the brandy market is the high taxes and strict rules placed on alcohol sales. Many countries impose heavy excise duties on alcoholic beverages, making brandy more expensive for consumers. In addition, some regions have limited sales hours, restrictions on advertising, or age-verification policies that make it harder to market and distribute alcoholic products.

These regulations affect both small and large sellers, reducing their ability to reach new customers or expand into certain areas. For new brands, especially, the high cost of compliance and licensing can be a major barrier. These legal and financial hurdles often discourage new investments and can slow down the overall growth of the brandy market.

Growth Opportunity

Growing Popularity of Brandy in Cocktails Globally

A big growth opportunity for the brandy market is the rising use of brandy in cocktails. Many bartenders and mixologists are now adding brandy to modern and classic cocktail recipes, giving the drink a fresh image among younger consumers. This trend is especially strong in urban bars and lounges, where people are looking for new taste experiences.

Brandy-based cocktails like sidecars and brandy sours are gaining popularity because they offer smooth flavors and pair well with other ingredients. As brandy moves beyond traditional sipping and enters trendy drinking scenes, it opens new markets and appeals to a broader audience.

Latest Trends

Craft Brandy Gaining Attention Among Young Drinkers

A major trend in the brandy market is the growing interest in craft and small-batch brandy, especially among younger drinkers. These consumers are curious about where and how their drinks are made, and they value unique flavors and local ingredients. Craft brandy makers often focus on quality, using fresh fruits and traditional distilling methods that create a more personal drinking experience.

This trend is similar to what happened in the beer and gin markets, where small producers became very popular. As more people look for authentic and handmade spirits, craft brandy is becoming a trendy and premium choice. This shift is also helping revive interest in brandy among a generation that once favored other types of alcohol.

Regional Analysis

North America led the Brandy Market in 2024 with a 44.3% share, USD 12.0 Bn.

In 2024, North America emerged as the leading region in the global Brandy Market, accounting for 44.3% of the total market share with a valuation of USD 12.0 billion. This dominance is supported by strong consumer demand for both regular and premium brandy products across the United States and Canada. The region’s mature beverage industry, coupled with rising interest in craft and aged spirits, has contributed to consistent growth in brandy sales.

In Europe, brandy consumption continues to be stable, driven by traditional preferences and the presence of brandy-producing countries. Asia Pacific is witnessing a gradual rise in demand, particularly in urban centers where changing lifestyles and premiumization trends are influencing alcohol choices. The Middle East & Africa region maintains moderate brandy consumption, limited by regulatory and cultural factors, but niche markets continue to show potential.

Latin America, with its developing beverage sector, shows steady sales growth, particularly in areas with strong Western influence and increasing disposable incomes. Overall, while emerging regions show growing interest, North America remains the key revenue contributor in the global brandy landscape due to its broad consumer base, retail availability, and premium segment expansion.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Courvoisier Cognac continued to reinforce its position in the global brandy market through its heritage-driven approach and premium product offerings. Known for its craftsmanship and French origin, Courvoisier focused on expanding its appeal among both traditional connoisseurs and younger consumers by promoting limited-edition releases and strengthening its brand storytelling across key global markets.

Diageo Plc, a major player in the alcoholic beverages sector, leveraged its broad distribution network and marketing expertise to strengthen its brandy portfolio. In 2024, Diageo emphasized innovation and product visibility, with brandy positioned strategically within its premium spirits category. The company also capitalized on brand collaborations and digital platforms to reach wider audiences, especially in North America and parts of Asia.

E. & J. Gallo Winery, with its strong presence in the United States, maintained leadership in the regular brandy segment. The company’s strength lies in mass-market accessibility, competitive pricing, and consistent product availability through supermarkets and retail chains. In 2024, E. & J. Gallo focused on expanding regional distribution and promotional campaigns to enhance brand loyalty.

Top Key Players in the Market

- Courvoisier Cognac

- Diageo Plc

- E. & J. Gallo Winery

- Emperador

- F. Korbel & Bros.

- Martell

- Speciality Brands Ltd.

- Rémy Cointreau

- Thomas HINE & Co.(EDV SAS)

- Yantai Changyu Pioneer Wine Company Limited

- Hennessy

- Rémy Martin

- Courvoisier

- Torres

- E&J Gallo

- Christian Brothers

- St-Rémy

- Germain-Robin

- Vecchia Romagna

Recent Developments

- In May 2025, Emperador’s affiliate Andresons Group bought ₱337 million worth of Emperador shares (25 million new shares), bringing its stake to 0.79%, aiming to support Emperador’s expansion in brandy and whisky.

- In November 2024, Hennessy announced a new bottle set for the 2025 Chinese New Year (Year of the Snake), designed by Shuting Qiu. It includes VSOP, XO, and Paradis editions in vibrant snake-brocade styles

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 27.2 Billion |

| Forecast Revenue (2034) | USD 48.3 Billion |

| CAGR (2025-2034) | 5.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Flavored, Regular), By Product Type (Grape Brandy, Cognac, Armagnac, Fruit Brandy, Others), By Distribution Channel (Supermarkets and Hypermarkets, Exclusive Stores, On-Trade, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Courvoisier Cognac, Diageo Plc, E. & J. Gallo Winery, Emperador, F. Korbel & Bros., Martell, Speciality Brands Ltd., Rémy Cointreau, Thomas HINE & Co.(EDV SAS), Yantai Changyu Pioneer Wine Company Limited, Hennessy, Rémy Martin, Courvoisier, Torres, E&J Gallo, Christian Brothers, St-Rémy, Germain-Robin, Vecchia Romagna |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |