Global Aviation Test Equipment Market Size, Share, Growth Analysis By System (Electrical, Hydraulic, Pneumatic, Others), By Aircraft Type (Manned, Unmanned), By End User (Defense/Military Sector, Commercial Sector, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181163

- Number of Pages: 215

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

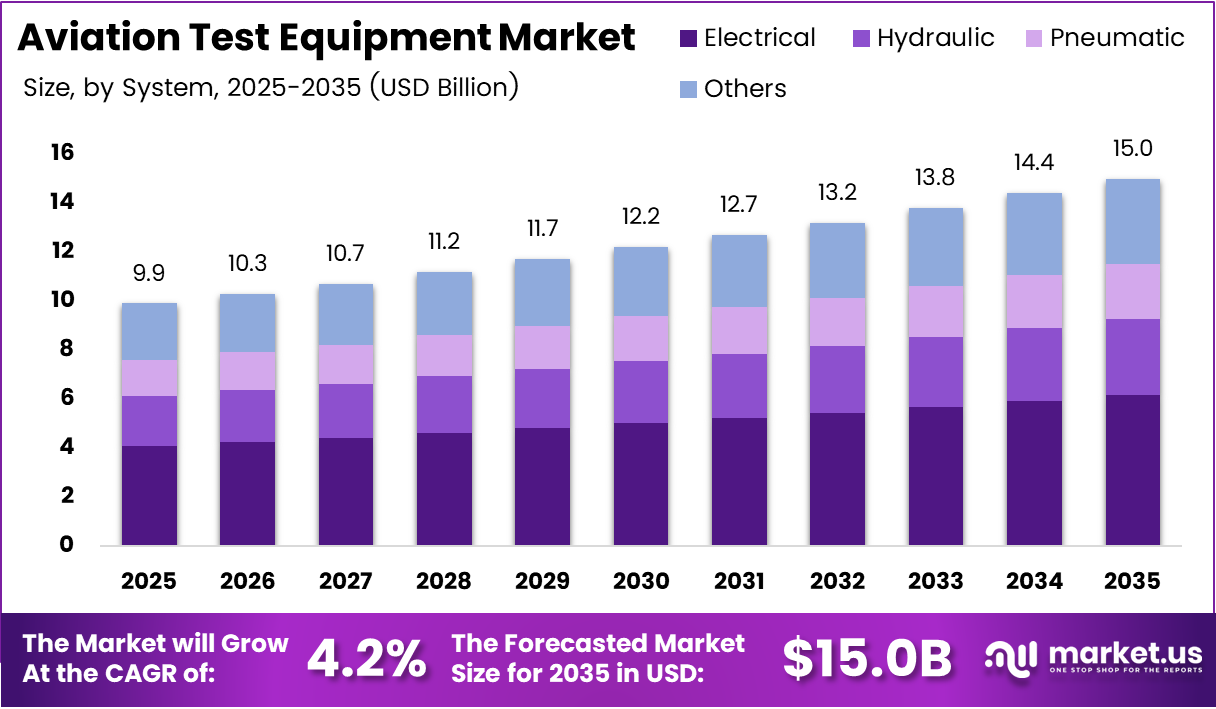

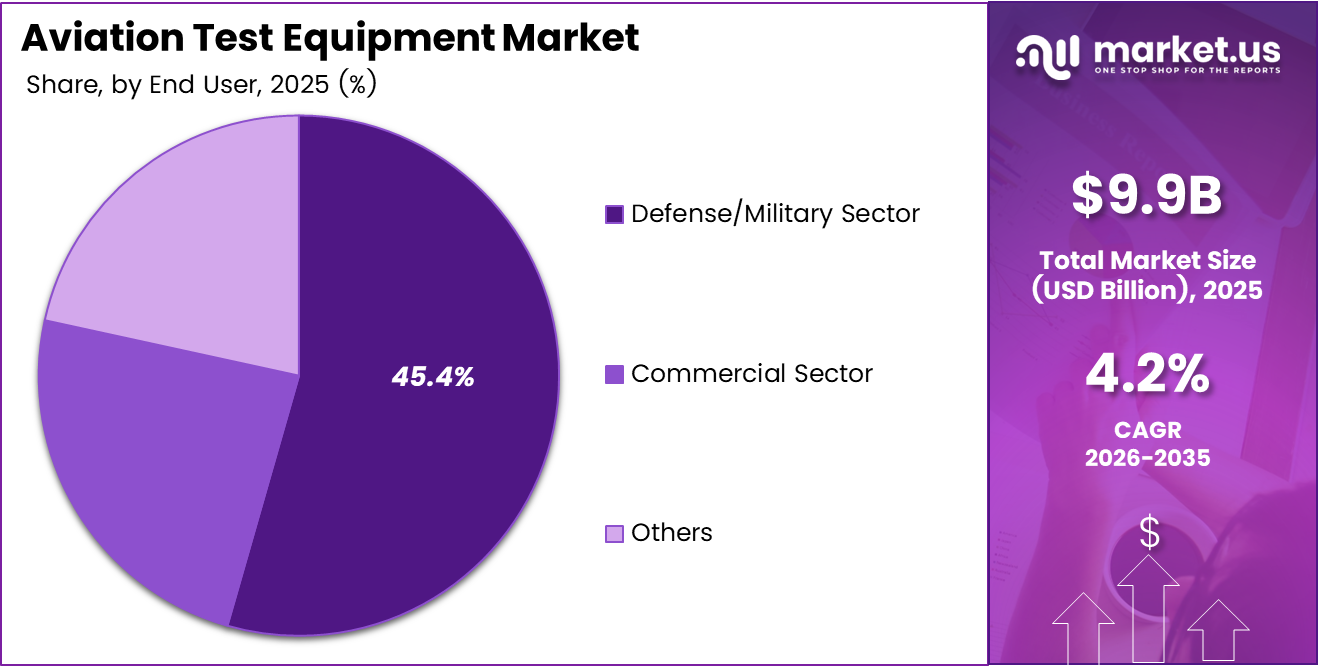

Global Aviation Test Equipment Market size is expected to be worth around USD 15.0 Billion by 2035 from USD 9.9 Billion in 2025, growing at a CAGR of 4.2% during the forecast period 2026 to 2035.

The aviation test equipment market covers diagnostic, calibration, and verification systems used to validate aircraft components, avionics, electrical networks, hydraulic assemblies, and pneumatic systems. These tools support both ground-based maintenance and in-flight readiness assessments across commercial, military, and unmanned aviation platforms.

Defense and commercial operators together drive procurement decisions in this market. Military fleets require precision-grade test systems to meet stringent airworthiness standards, while commercial operators need faster, more automated diagnostics to reduce turnaround times. This dual demand structure creates stable baseline revenue even through commercial aviation downturns.

Regulatory agencies including the FAA, EASA, and ICAO mandate recurring testing and certification intervals for aircraft systems. These requirements function as a built-in procurement cycle — operators cannot defer equipment upgrades without risking compliance violations. This regulatory floor gives test equipment suppliers predictable, recurring revenue streams independent of fleet growth.

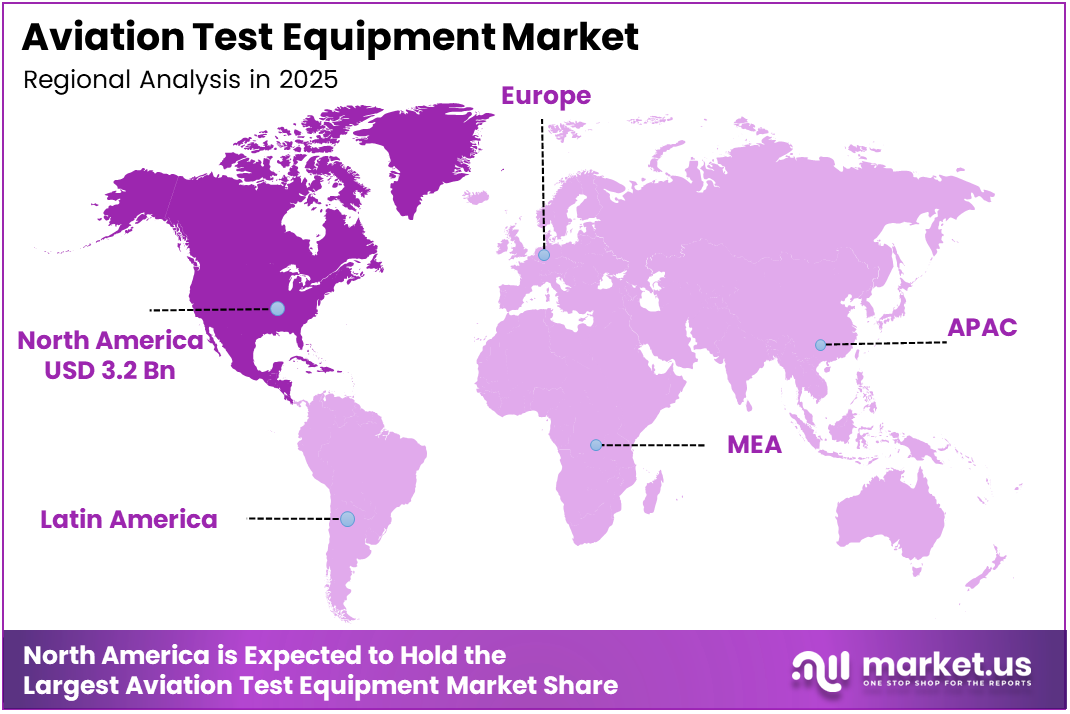

North America holds the largest regional share at 32.1%, valued at USD 3.2 Billion. This position reflects the concentration of military aviation programs, mature MRO infrastructure, and the presence of major aerospace OEMs. As these conditions replicate in Asia Pacific and the Middle East, geographic revenue diversification will accelerate.

In May 2024, TransDigm Group completed the acquisition of Raptor Scientific for approximately USD 655 million to expand capabilities in aerospace test and measurement technologies. This acquisition signals that strategic consolidation is underway — larger players are acquiring specialized test technology firms to deepen capabilities before competition intensifies.

According to Veryon’s 2025 Aviation Maintenance Benchmark Report, 72% of aviation maintenance professionals state that operational efficiency defines their maintenance strategies. This means test equipment buyers now evaluate procurement decisions on throughput and downtime reduction, not just technical compliance — shifting vendor competition toward speed and automation.

Additionally, the same report shows that 65% of aviation operators are actively exploring predictive maintenance integration. This broad adoption signal indicates that sensor-based and AI-enabled test systems are moving from pilot programs to standard procurement categories, compressing the window for early-mover advantage among specialized equipment vendors.

Key Takeaways

- The Global Aviation Test Equipment Market was valued at USD 9.9 Billion in 2025 and is forecast to reach USD 15.0 Billion by 2035.

- The market advances at a CAGR of 4.2% during the forecast period 2026 to 2035.

- By System, the Electrical segment leads with a 40.1% share, reflecting the dominance of avionics and electronic system testing across modern aircraft platforms.

- By Aircraft Type, the Manned segment holds a 70.1% share, supported by large commercial and military fleet maintenance requirements.

- By End User, the Defense/Military Sector accounts for 45.4% of market revenue, driven by mandatory airworthiness certification standards.

- North America dominates with a 32.1% market share, valued at USD 3.2 Billion, underpinned by mature MRO infrastructure and large defense budgets.

- Key players include Honeywell International Inc., Boeing, General Electric Co., 3M, Airbus, Rockwell Collins, Moog Inc., and Teradyne Inc., among others.

System Analysis

Electrical dominates with 40.1% due to rapid avionics proliferation across modern fleets.

In 2025, Electrical held a dominant market position in the By System segment of the Aviation Test Equipment Market, with a 40.1% share. Modern aircraft platforms integrate increasingly dense electronic architectures — from fly-by-wire controls to advanced communication suites — requiring continuous electrical system validation. This complexity compels operators to invest in specialized electrical test equipment as a non-negotiable maintenance asset.

Hydraulic testing serves as the structural backbone of flight control verification. Hydraulic systems govern critical functions including landing gear, braking, and flight surface actuation. Failures in these systems carry the highest safety consequences, which means hydraulic test equipment procurement follows strict replacement and calibration cycles mandated by airworthiness authorities, providing consistent demand regardless of fleet utilization levels.

Pneumatic test systems address pressurization, de-icing, and engine bleed air circuits. These systems are particularly relevant for wide-body commercial aircraft operating at high altitudes. Pneumatic testing requirements have become more complex as newer airframe designs reduce bleed-air dependency, pushing equipment manufacturers to develop dual-mode test platforms that handle both legacy and next-generation configurations.

Others in this segment includes fuel system testers, structural integrity monitors, and composite inspection tools. These niche categories serve specialized maintenance needs across both defense and commercial fleets. Though smaller in share, they carry higher margin potential because procurement is tied to specific airframe types rather than general fleet maintenance schedules.

Aircraft Type Analysis

Manned dominates with 70.1% due to large commercial and military fleet maintenance volumes.

In 2025, Manned aircraft held a dominant market position in the By Aircraft Type segment of the Aviation Test Equipment Market, with a 70.1% share. This dominance reflects the scale of active commercial and defense fleets requiring ongoing scheduled maintenance, certification renewals, and component-level testing. The volume of manned aircraft in service creates a continuous, high-frequency procurement cycle for test equipment suppliers.

Unmanned aircraft systems represent the highest-growth category within this segment. UAV proliferation across defense, logistics, and surveillance applications creates a new and distinct testing requirement set — one that existing manned-aircraft test platforms were not designed to serve. Vendors who develop UAV-specific diagnostic tools now position themselves ahead of a procurement wave that defense agencies and commercial drone operators have not yet fully addressed.

End User Analysis

Defense/Military Sector dominates with 45.4% due to stringent airworthiness mandates and sustained procurement budgets.

In 2025, the Defense/Military Sector held a dominant market position in the By End User segment of the Aviation Test Equipment Market, with a 45.4% share. Military operators maintain zero-tolerance safety standards and face mandatory testing intervals enforced by defense airworthiness authorities. These non-negotiable compliance requirements translate into recurring, budget-protected equipment procurement cycles that insulate this segment from broader economic volatility.

Commercial Sector buyers prioritize test equipment that reduces aircraft-on-ground time and minimizes maintenance labor costs. Airlines and MRO providers operate under tight margin constraints, which means procurement decisions increasingly favor automated and multi-function test platforms over single-purpose legacy systems. This buyer behavior is reshaping product development priorities among major equipment vendors.

Others in this segment includes general aviation operators, flight training institutions, and government research agencies. These buyers typically operate smaller fleets with less frequent testing intervals. However, they represent an underserved market for portable, lower-cost diagnostic tools — a segment that modular equipment vendors are beginning to address with entry-level product lines.

Key Market Segments

By System

- Electrical

- Hydraulic

- Pneumatic

- Others

By Aircraft Type

- Manned

- Unmanned

By End User

- Defense/Military Sector

- Commercial Sector

- Others

Drivers

Mandatory Safety Regulations and Fleet Expansion Push Sustained Procurement of High-Precision Aviation Test Systems

Aviation safety authorities — including the FAA, EASA, and ICAO — enforce mandatory testing and calibration intervals for all certified aircraft systems. These regulations function as a structural procurement floor: operators cannot delay equipment purchases without triggering compliance violations. This regulatory framework removes purchasing discretion and locks in recurring revenue for test equipment vendors across both defense and commercial end users.

Global aircraft fleet expansion compounds this regulatory demand. As airline operators and defense agencies add new platforms, the installed base requiring diagnostic coverage expands proportionally. Each new aircraft entering service creates a corresponding requirement for type-specific test equipment — electrical testers, hydraulic calibration rigs, and avionics validation platforms — which feeds directly into OEM and MRO procurement pipelines.

According to Reanin, 65% of aviation operators in 2025 rely on advanced diagnostic tools — including AI, IoT, and sensor-based systems — for safety and regulatory compliance. This figure confirms that test equipment adoption is no longer discretionary for most operators. In February 2024, VIAVI Solutions expanded its avionics and RF test portfolio to support validation of modern aircraft communication and navigation systems, illustrating how vendors are directly responding to this compliance-driven demand pattern.

Restraints

High Capital Costs and Complex Certification Processes Slow Test Equipment Adoption Among Smaller Operators

Advanced aviation test equipment carries significant upfront procurement costs. Specialized electrical, hydraulic, and avionics test platforms require substantial capital investment — a barrier that smaller MRO providers and regional operators cannot easily absorb. This cost structure concentrates purchasing power among large airlines, defense contractors, and major MRO networks, limiting market penetration into the long tail of smaller aviation maintenance organizations.

Certification and regulatory compliance processes add a second layer of friction. Test equipment used in airworthiness-critical applications must itself meet certification standards set by aviation authorities. Vendors must navigate lengthy approval timelines before new products can be deployed in certified maintenance environments. This slows product introduction cycles and delays adoption of newer diagnostic technologies even after they become commercially available.

According to Veryon’s 2025 Aviation Maintenance Benchmark Report, 78% of aviation professionals report managing complex regulatory compliance challenges in their maintenance operations. This figure signals that compliance burden is not a peripheral concern — it is the dominant operational pressure for most maintenance teams. For test equipment vendors, this creates both an adoption barrier and a product opportunity: solutions that simplify compliance documentation and reporting carry distinct commercial value.

Growth Factors

AI-Enabled Automation and Emerging Economy Infrastructure Expansion Open New Revenue Channels for Test Equipment Vendors

The shift toward automated and AI-enabled aircraft testing solutions creates measurable efficiency gains that justify capital replacement cycles. Maintenance facilities that deploy automated test platforms report faster diagnostic throughput and reduced technician dependency — a critical advantage given the certified technician shortage affecting 62% of maintenance teams. Automation does not just improve efficiency; it directly addresses a workforce constraint that operators cannot solve through hiring alone.

In June 2025, Curtiss-Wright introduced a new high-channel-count flight test data acquisition system designed to improve real-time aircraft performance monitoring. This product launch illustrates how vendors are responding to demand for higher-fidelity, real-time testing capabilities — particularly in flight test programs supporting next-generation electric and hybrid aircraft development where legacy test architectures are inadequate.

According to Reanin, approximately 55% of newly implemented aircraft test systems feature automated functions to boost efficiency and reduce turnaround times. This adoption rate confirms that automation is crossing from early adoption into mainstream procurement. Commercial aviation infrastructure build-out across Asia Pacific, the Middle East, and Latin America adds a geographic multiplier — each new MRO facility entering service represents a greenfield equipment procurement opportunity for vendors with established regional distribution.

Emerging Trends

Digital Twin Integration and Wireless Remote Monitoring Redefine Aircraft Testing From Reactive to Predictive

Digital twin technology allows aircraft operators to simulate system behavior and identify failure points before physical testing begins. This capability shifts maintenance from scheduled inspections to condition-based interventions — reducing unnecessary test cycles while improving fault detection accuracy. For test equipment vendors, digital twin integration signals a product evolution: hardware alone is no longer sufficient; embedded software and data connectivity become core value drivers.

Wireless and remote aircraft testing technologies remove the geographic constraints of traditional ground-based diagnostics. Field maintenance teams can now deploy portable sensor-based systems and transmit data to centralized analysis platforms in real time. According to Veryon’s 2025 Aviation Maintenance Benchmark Report, only 17% of aviation organizations have fully integrated AI into their operations — meaning the majority of operators remain in early or partial adoption stages, and the commercial window for vendors offering integrated AI-enabled test platforms remains open.

In March 2025, ATEQ Aviation launched the MyCloud digital platform enabling remote monitoring, fleet management, and data tracking for aviation test equipment. This product represents the convergence of hardware and software in test equipment — a structural shift where equipment value is increasingly measured by connectivity and data output, not just measurement precision. Early movers who build proprietary data ecosystems around their test platforms will establish switching-cost advantages that are difficult for competitors to replicate.

Regional Analysis

North America Dominates the Aviation Test Equipment Market with a Market Share of 32.1%, Valued at USD 3.2 Billion

North America holds a 32.1% share valued at USD 3.2 Billion, anchored by the world’s largest defense aviation budgets, a dense network of certified MRO facilities, and the headquarters concentration of major aerospace OEMs. These structural advantages compound over time: existing procurement relationships, type certifications, and installed equipment bases all create renewal cycles that sustain regional revenue leadership well beyond any single program cycle.

Europe Aviation Test Equipment Market Trends

Europe maintains a strong position supported by Airbus production programs, a mature commercial MRO sector, and EASA’s comprehensive airworthiness framework. Countries including Germany, France, and the UK operate large civil and military fleets requiring continuous test equipment investment. European defense modernization programs — particularly NATO-aligned fleet upgrades — are generating additional procurement demand for advanced avionics and systems testing platforms.

Asia Pacific Aviation Test Equipment Market Trends

Asia Pacific represents the fastest-expanding geography for aviation test equipment procurement. Commercial fleet growth in China, India, and Southeast Asia is creating new MRO infrastructure requirements, while defense modernization in India and South Korea drives military test equipment investment. In November 2024, Paras Defence and Space Technologies inaugurated a new optical systems testing and integration facility in Navi Mumbai, signaling India’s active investment in domestic aerospace testing infrastructure.

Middle East and Africa Aviation Test Equipment Market Trends

The Middle East benefits from sustained government investment in both military aviation and commercial hub expansion. Gulf Cooperation Council nations operate large defense fleets and continue expanding civil aviation capacity, both of which require testing infrastructure. Africa remains an early-stage market, but airport modernization programs and the introduction of new aircraft types are beginning to create structured procurement requirements for diagnostic equipment.

Latin America Aviation Test Equipment Market Trends

Latin America’s aviation test equipment market is driven by commercial fleet renewal in Brazil and Mexico, where established airlines are upgrading aging aircraft with modern avionics-equipped platforms. These newer aircraft require more sophisticated test systems than legacy fleets, creating an equipment replacement cycle. Regional MRO capacity expansion, particularly in Brazil’s established aerospace sector, is the primary near-term demand driver for test equipment vendors entering this geography.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Honeywell International Inc. positions itself as a vertically integrated aviation systems provider with deep test and validation capabilities across avionics, sensors, and propulsion electronics. Its advantage lies in owning both the system being tested and the test equipment used to validate it — a closed-loop positioning that creates natural cross-sell opportunities within its existing airline and defense customer base, reducing competitor access to those accounts.

Boeing approaches the aviation test equipment space from an OEM perspective, developing and deploying proprietary testing architectures tied to its commercial and military aircraft programs. This integration means Boeing’s test systems are often embedded in contractual maintenance agreements, locking in long-term service revenue. Its dual commercial and defense presence provides revenue diversification that pure-play test equipment manufacturers cannot match.

General Electric Co. leverages its engine manufacturing scale to drive test equipment adoption across the MRO operators that service GE-powered fleets globally. By aligning test equipment specifications with engine diagnostic requirements, GE creates a technical dependency that influences procurement decisions at airline maintenance centers worldwide. This OEM-to-MRO linkage gives GE a structural pull-through mechanism that independent test equipment vendors must work significantly harder to replicate.

3M competes in the aviation test equipment segment through specialized materials, sensing technologies, and surface inspection systems used in structural and component-level testing. Its differentiation rests on material science depth rather than avionics integration — a position that makes 3M a preferred supplier for composite inspection and non-destructive testing applications, particularly as next-generation aircraft increase their composite airframe content and require more sophisticated structural validation protocols.

Key Players

- Honeywell International Inc.

- Boeing

- General Electric Co.

- 3M

- Airbus

- Rockwell Collins

- Moog Inc.

- Teradyne Inc.

- SPHEREA Test & Services

- Rolls Royce Holdings Plc

- Other Key Players

Recent Developments

- March 2025 – Teledyne Technologies completed the acquisition of select aerospace and defense electronics businesses from Excelitas Technologies, expanding its advanced sensing and testing capabilities for aerospace and defense applications. This deal strengthens Teledyne’s position in precision test instrumentation for airborne and ground-based defense systems.

- July 2025 – Safran finalized the acquisition of Collins Aerospace’s flight control activities from RTX Corporation, strengthening its development and testing capabilities for next-generation aircraft flight control systems. This transaction directly expands Safran’s test infrastructure for advanced fly-by-wire and autonomous flight control validation programs.

- June 2025 – Curtiss-Wright introduced a new high-channel-count flight test data acquisition system designed to improve real-time aircraft performance monitoring and instrumentation capabilities. The system targets flight test programs for next-generation aircraft platforms including electric and hybrid aviation development projects.

- November 2024 – Paras Defence and Space Technologies inaugurated a new optical systems testing and integration facility in Navi Mumbai, strengthening domestic aerospace testing and validation infrastructure in India. This investment positions Paras Defence as a growing domestic supplier within India’s expanding aerospace MRO and defense manufacturing ecosystem.

Report Scope

Report Features Description Market Value (2025) USD 9.9 Billion Forecast Revenue (2035) USD 15.0 Billion CAGR (2026-2035) 4.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By System (Electrical, Hydraulic, Pneumatic, Others), By Aircraft Type (Manned, Unmanned), By End User (Defense/Military Sector, Commercial Sector, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Honeywell International Inc., Boeing, General Electric Co., 3M, Airbus, Rockwell Collins, Moog Inc., Teradyne Inc., SPHEREA Test & Services, Rolls Royce Holdings Plc, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Aviation Test Equipment MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Aviation Test Equipment MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Honeywell International Inc.

- Boeing

- General Electric Co.

- 3M

- Airbus

- Rockwell Collins

- Moog Inc.

- Teradyne Inc.

- SPHEREA Test & Services

- Rolls Royce Holdings Plc

- Other Key Players

Our Clients

- 181163

- Mar 2026