Quick Navigation

Report Overview

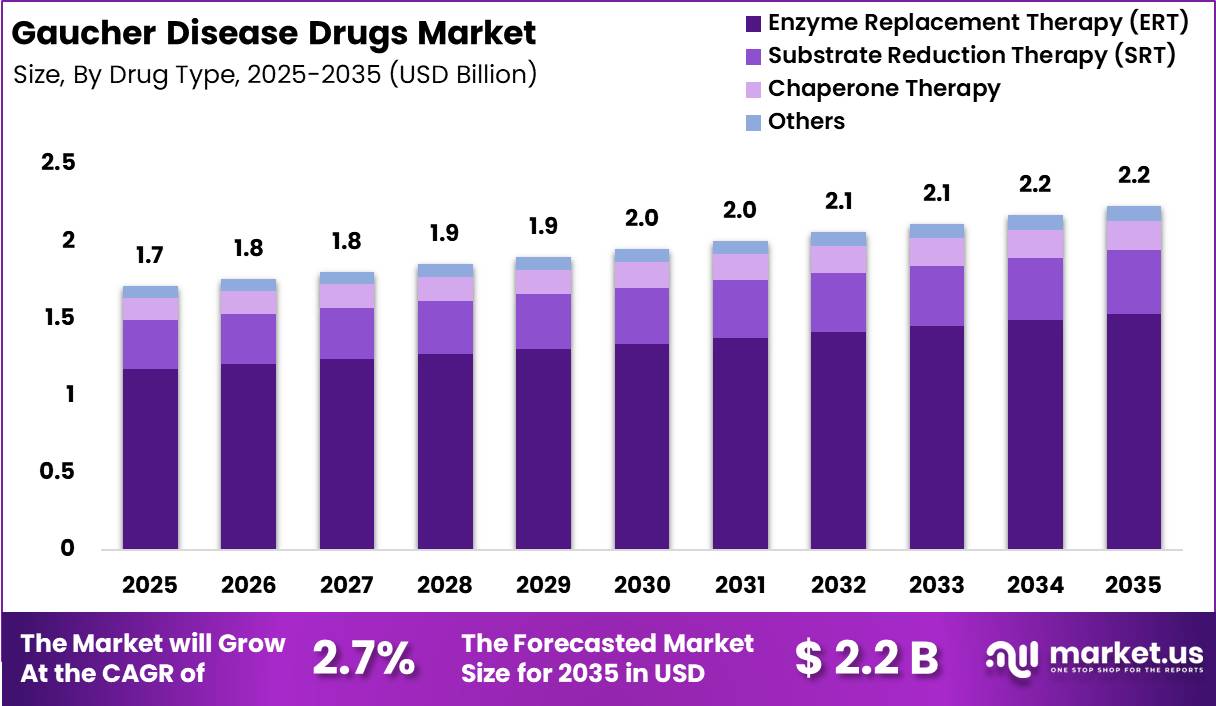

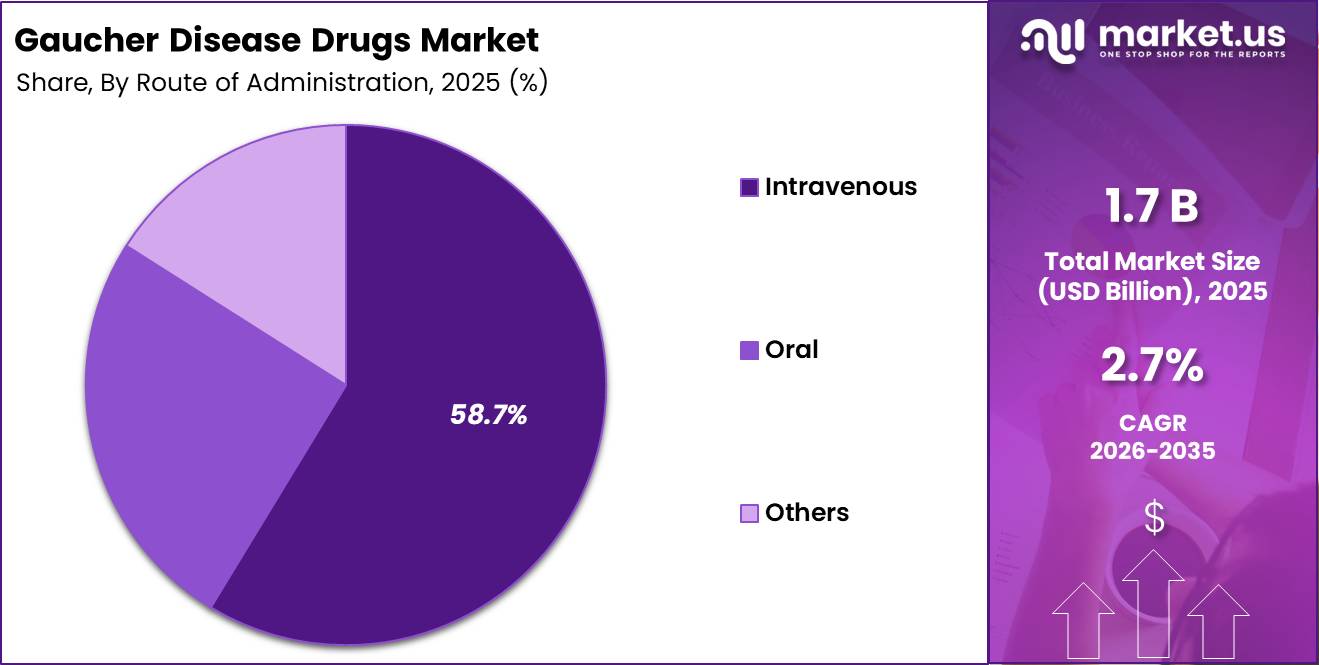

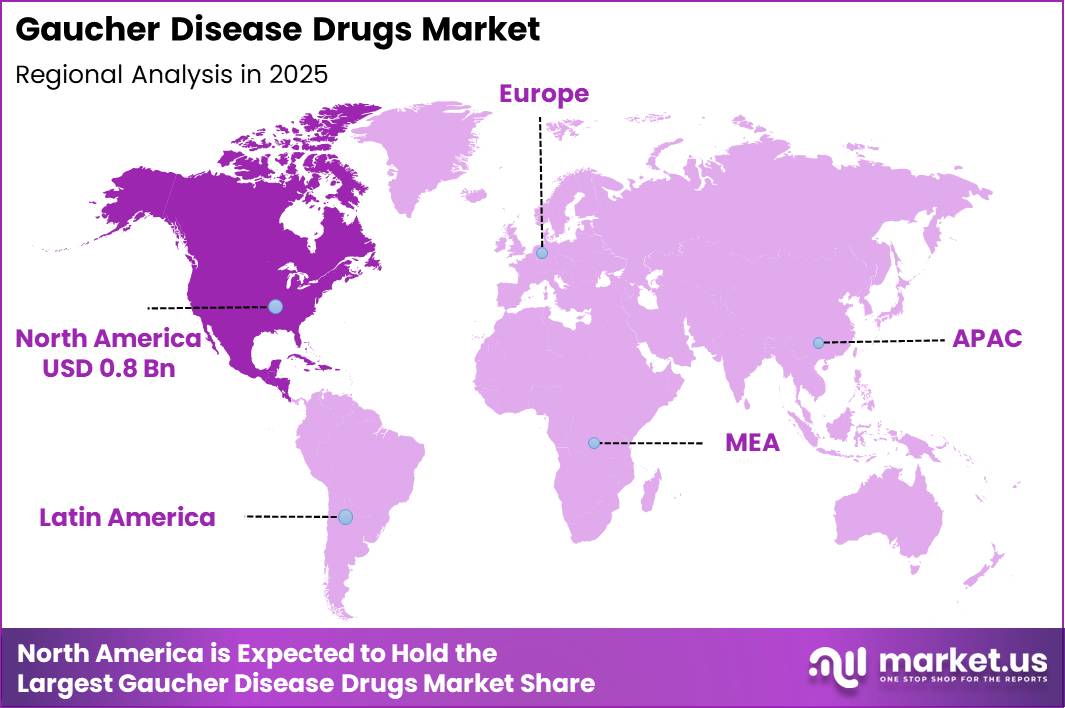

Global Gaucher Disease Drugs Market size is expected to be worth around US$ 2.2 Billion by 2035 from US$ 1.7 Billion in 2025, growing at a CAGR of 2.7% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 48.6% share with a revenue of US$ 0.8 Billion.

The Gaucher Disease Drugs Market represents a specialized segment of the rare disease therapeutics industry, focused on the treatment and long-term management of Gaucher disease (GD), a rare inherited lysosomal storage disorder caused by mutations in the GBA gene.

The condition results in a deficiency of the enzyme glucocerebrosidase, leading to the accumulation of glucocerebroside within macrophages and causing progressive damage to the spleen, liver, bone marrow, and skeletal system. According to a systematic review published by the U.S. National Library of Medicine, the global birth prevalence of Gaucher disease is estimated at approximately 1.5 cases per 100,000 live births, while the overall prevalence is around 0.9 cases per 100,000 population.

The market has evolved significantly over the past two decades with the introduction of disease-specific therapies designed to address the underlying enzymatic deficiency. Enzyme replacement therapies (ERTs), including imiglucerase, velaglucerase alfa, and taliglucerase alfa, remain the standard of care for many patients, while substrate reduction therapies (SRTs) such as eliglustat and miglustat provide alternative treatment options for eligible individuals. These therapies have improved disease management by reducing organ enlargement, improving hematological parameters, and enhancing patient quality of life.

Market growth is being supported by increasing awareness of rare genetic disorders, advances in genetic screening and diagnostic technologies, and expanding access to orphan drugs across developed and emerging healthcare systems. Government initiatives are also strengthening the treatment landscape for rare diseases.

For example, the Government of Canada launched its National Strategy for Drugs for Rare Diseases in 2023 with an investment of up to USD 1.5 billion over three years to improve access to effective therapies, enhance diagnostics, and support rare disease research and innovation.

Furthermore, ongoing research into next-generation enzyme therapies, gene therapies, and precision medicine approaches is expected to expand treatment possibilities for neuronopathic forms of Gaucher disease, addressing existing unmet clinical needs.

As healthcare systems continue to prioritize rare disease management and early diagnosis, the Gaucher Disease Drugs Market is anticipated to witness sustained growth, supported by technological advancements, favorable regulatory incentives for orphan drugs, and increasing investment in rare disease therapeutics worldwide.

Key Takeaways

- Market Size: Global Gaucher Disease Drugs Market size is expected to be worth around US$ 2.2 Billion by 2035 from US$ 1.7 Billion in 2025.

- Market Share: The market growing at a CAGR of 2.7% during the forecast period from 2026 to 2035.

- Drug Type Analysis: Enzyme Replacement Therapy (ERT) accounted for the largest market share of 68.5% in 2025.

- Route of Administration Analysis: The Intravenous segment dominated the market with a 58.7% share in 2025.

- End User Analysis: Hospitals held the leading market share of 58.5% in 2025, supported by their role as primary centers for diagnosis, treatment initiation, and administration of enzyme replacement therapies.

- Regional Analysis: In 2025, North America led the market, achieving over 48.6% share with a revenue of US$ 0.8 Billion.

Drug Type Analysis

The drug type segment of the Gaucher Disease Drugs Market is categorized into Enzyme Replacement Therapy (ERT), Substrate Reduction Therapy (SRT), Chaperone Therapy, and Others. Enzyme Replacement Therapy (ERT) accounted for the largest market share of 68.5% in 2025, owing to its established clinical efficacy, long-term safety profile, and widespread adoption as the standard treatment for Type 1 Gaucher disease.

ERT works by replacing the deficient glucocerebrosidase enzyme, thereby reducing the accumulation of glucocerebroside in affected organs. The strong presence of approved therapies, extensive physician familiarity, and favorable treatment outcomes continue to support segment dominance.

Substrate Reduction Therapy (SRT) represents the second-largest segment and is gaining traction due to its oral administration advantage and suitability for patients who are unable to receive enzyme replacement therapy. Increasing adoption of oral treatment alternatives and advancements in disease management are contributing to segment growth.

Chaperone Therapy is emerging as a promising treatment approach, particularly for patients with specific genetic mutations, as it helps stabilize defective enzymes and improve their function. The Others segment includes investigational therapies and supportive treatment options, which are expected to benefit from ongoing research and development activities focused on improving disease outcomes and patient convenience.

Route of Administration Analysis

Based on route of administration, the Gaucher Disease Drugs Market is segmented into Intravenous, Oral, and Others. The Intravenous segment dominated the market with a 58.7% share in 2025, primarily driven by the widespread use of enzyme replacement therapies, which are administered through intravenous infusion.

The established effectiveness of intravenous treatments in managing disease progression, reducing organ enlargement, and improving hematological parameters has contributed significantly to their strong market position. Additionally, healthcare providers continue to prefer intravenous therapies for severe and long-term disease management due to their proven clinical outcomes.

The Oral segment is witnessing notable growth as patients increasingly seek convenient treatment options that reduce hospital visits and improve treatment adherence. Oral therapies, particularly substrate reduction therapies, have expanded treatment accessibility and enhanced patient quality of life. The growing availability of advanced oral formulations and increasing acceptance among both patients and healthcare professionals are supporting segment expansion.

The Others segment includes alternative administration methods under development or used in specialized clinical settings. Ongoing innovations aimed at improving drug delivery efficiency, reducing treatment burden, and enhancing patient comfort are expected to create new opportunities across non-traditional administration routes during the forecast period.

End User Analysis

The Gaucher Disease Drugs Market, by end user, is segmented into Hospitals, Specialty Clinics, Homecare Settings, and Others. Hospitals held the leading market share of 58.5% in 2025, supported by their role as primary centers for diagnosis, treatment initiation, and administration of enzyme replacement therapies.

The availability of specialized healthcare professionals, advanced infusion facilities, comprehensive patient monitoring services, and multidisciplinary care teams has reinforced the dominance of hospitals in Gaucher disease management. Furthermore, the need for regular intravenous infusions and management of complex cases continues to drive patient preference toward hospital-based treatment settings.

Specialty Clinics represent a significant segment due to their focused expertise in rare genetic and metabolic disorders. These facilities provide personalized treatment plans, specialized monitoring, and improved access to disease-specific care, contributing to growing patient adoption. Homecare Settings are experiencing increasing demand as healthcare systems emphasize patient-centric care and cost-effective treatment delivery.

The expansion of home infusion services and improved patient support programs have enabled eligible patients to receive therapies in a more convenient environment. The Others segment includes research institutions, ambulatory care centers, and alternative healthcare facilities that contribute to disease management. Continuous improvements in treatment accessibility and healthcare infrastructure are expected to support growth across all end-user categories.

Key Market Segments

By Drug Type

- Enzyme Replacement Therapy (ERT)

- Substrate Reduction Therapy (SRT)

- Chaperone Therapy

- Others

By Route of Administration

- Intravenous

- Oral

- Others

By End User

- Hospitals

- Specialty Clinics

- Homecare Settings

- Others

Driving Factors

Increasing Diagnosis Rates and Expanding Treatment Adoption

The growth of the Gaucher Disease Drugs Market is being driven by increasing diagnosis rates and broader adoption of disease-specific therapies. Advancements in newborn screening programs, genetic testing technologies, and physician awareness have improved the identification of patients at earlier stages of disease progression. Earlier diagnosis enables timely therapeutic intervention, which contributes to better disease management and improved clinical outcomes.

The growing availability of specialized treatment centers and rare disease management programs has further increased patient access to approved therapies. In addition, expanding healthcare coverage for rare diseases across developed markets has supported higher treatment uptake. As more patients receive confirmed diagnoses and initiate long-term therapy, demand for Gaucher disease treatments continues to increase, supporting market expansion.

Trending Factors

Growing Preference for Oral Therapies and Personalized Treatment Approaches

A key trend shaping the market is the increasing preference for oral treatment options and personalized therapeutic strategies. Oral therapies offer greater convenience compared to intravenous treatment administration and can reduce the burden associated with frequent hospital or infusion-center visits. This shift is contributing to improved patient adherence and treatment satisfaction.

At the same time, advances in molecular diagnostics and genetic profiling are supporting more individualized treatment decisions. Healthcare providers are increasingly incorporating patient-specific genetic and metabolic information into therapy selection, reflecting the broader movement toward precision medicine in rare disease management. Continued research into targeted therapies and advanced treatment modalities is expected to further transform the treatment landscape.

Restraining Factors

High Cost of Long-Term Treatment and Limited Patient Pool

The market faces significant challenges due to the high cost associated with lifelong treatment and the relatively small patient population. Advanced biologic therapies require complex manufacturing processes and ongoing administration, resulting in substantial treatment expenses. These costs create financial pressures for healthcare systems and can limit treatment accessibility, particularly in low- and middle-income countries where reimbursement frameworks for rare diseases remain underdeveloped.

The rarity of Gaucher disease also restricts the commercial potential of new therapies, reducing economies of scale and increasing development costs for pharmaceutical manufacturers. Furthermore, delayed diagnosis resulting from non-specific symptoms can postpone treatment initiation and limit overall market penetration.

Opportunity

Advancements in Gene Therapy and Rare Disease Funding Initiatives

Significant opportunities are emerging from the advancement of gene therapy technologies and increasing governmental support for rare disease research. Growing investment in genetic engineering, cell-based therapies, and advanced drug development platforms is accelerating the development of disease-modifying and potentially curative treatment approaches.

In parallel, orphan drug incentives, research grants, and accelerated regulatory pathways are encouraging greater participation from biotechnology and pharmaceutical companies. Expansion of newborn screening programs, genetic counseling services, and rare disease awareness initiatives is also expected to improve early diagnosis rates and patient identification. These developments are creating favorable conditions for innovation and long-term market growth, particularly as next-generation therapies progress through clinical development and commercialization.

Regional Analysis

North America dominated the Gaucher Disease Drugs Market in 2025, accounting for more than 48.6% of the global market share and generating revenue of approximately US$ 0.8 billion. The region’s leadership can be attributed to its advanced healthcare infrastructure, strong presence of leading pharmaceutical companies, and widespread availability of innovative therapies for rare diseases.

Favorable reimbursement policies, high healthcare expenditure, and increasing awareness regarding early diagnosis and treatment of Gaucher disease have further supported market growth across the United States and Canada.

The United States represented the largest contributor within the region, driven by a well-established rare disease treatment ecosystem and significant investments in research and development. The availability of enzyme replacement therapies (ERTs) and substrate reduction therapies (SRTs), coupled with strong regulatory support for orphan drugs, has enhanced patient access to effective treatment options. In addition, the presence of specialized treatment centers and genetic screening programs has improved disease detection rates, contributing to sustained demand for Gaucher disease drugs.

Canada also contributed to regional growth through expanding healthcare coverage and increasing adoption of advanced biologic therapies. Furthermore, ongoing clinical research activities, collaborations between pharmaceutical companies and healthcare institutions, and the introduction of next-generation therapies are expected to strengthen North America’s position throughout the forecast period. The region is anticipated to maintain its market dominance due to continuous innovation and a supportive regulatory environment for rare disease treatments.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Gaucher Disease Drugs Market is characterized by the presence of several leading pharmaceutical companies focused on enzyme replacement therapies (ERTs) and substrate reduction therapies (SRTs). Key players include Sanofi, Takeda Pharmaceutical Company, and Johnson & Johnson through its rare disease portfolio. Sanofi maintains a strong market position with its established ERT products and extensive global distribution network.

Takeda continues to strengthen its presence through innovative treatment offerings and ongoing research initiatives. Market participants are increasingly investing in advanced therapies, including gene therapy and next-generation treatment approaches, to improve patient outcomes and expand their product portfolios.

Strategic collaborations, regulatory approvals, and geographic expansion remain key competitive strategies. The market is moderately consolidated, with high entry barriers due to complex drug development processes, stringent regulatory requirements, and the limited patient population associated with this rare genetic disorder.

Market Key Players

- Sanofi S.A.

- Takeda Pharmaceutical Company Limited

- Pfizer Inc.

- Johnson & Johnson (Janssen)

- Protalix BioTherapeutics, Inc.

- Amicus Therapeutics, Inc.

- Centogene N.V.

- Chiesi Farmaceutici S.p.A.

- BioMarin Pharmaceutical Inc.

- Shire plc (Takeda)

- Roche Holding AG

- Merck & Co., Inc.

- Novo Nordisk A/S

- Others

Recent Developments

- December 2025 – BioMarin Pharmaceutical Inc. announced a definitive agreement to acquire Amicus Therapeutics for approximately $4.8 billion. The transaction was designed to strengthen BioMarin’s rare disease portfolio and expand its presence in lysosomal storage disorders. Although Amicus is primarily focused on Fabry and Pompe diseases, the acquisition reflects increasing consolidation within the rare disease therapeutics landscape, which also includes Gaucher disease.

- October 2025 – Takeda Pharmaceutical Company Limited entered into a strategic partnership with Innovent Biologics. The collaboration, valued at up to $11.4 billion, was established to develop and commercialize innovative biologic assets. The agreement underscored Takeda’s broader strategy of enhancing its rare disease and specialty medicine pipeline through external innovation and global partnerships.

- Throughout 2025–2026 – Protalix BioTherapeutics continued expanding the commercial presence of ELELYSO® (taliglucerase alfa), a plant cell-expressed enzyme replacement therapy for Gaucher disease. The company maintained its focus on increasing treatment accessibility and strengthening its position in the global Gaucher disease market through ongoing commercialization initiatives and lifecycle management activities.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.7 Billion |

| Forecast Revenue (2035) | US$ 2.2 Billion |

| CAGR (2026-2035) | 2.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Type (Enzyme Replacement Therapy (ERT), Substrate Reduction Therapy (SRT), Chaperone Therapy, Others) By Route of Administration (Intravenous, Oral, Others) By End User (Hospitals, Specialty Clinics, Homecare Settings, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Sanofi S.A., Takeda Pharmaceutical Company Limited, Pfizer Inc., Johnson & Johnson (Janssen), Protalix BioTherapeutics, Inc., Amicus Therapeutics, Inc., Centogene N.V., Chiesi Farmaceutici S.p.A., BioMarin Pharmaceutical Inc., Shire plc (Takeda), Roche Holding AG, Merck & Co., Inc., Novo Nordisk A/S, Others, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |