Global Gamma Butyrolactone Market Size, Share, And Industry Analysis Report By Purity (Min 99.9 percent, Min 99.7 percent), By Application (Solvent, Batteries and Capacitors, Herbicides and Insecticides, Sedative and Anesthetic, Others), By End Use (Pharmaceutical, Electrical and Electronics, Agrochemical, Chemical, Other), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: February 2026

- Report ID: 178931

- Number of Pages: 329

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

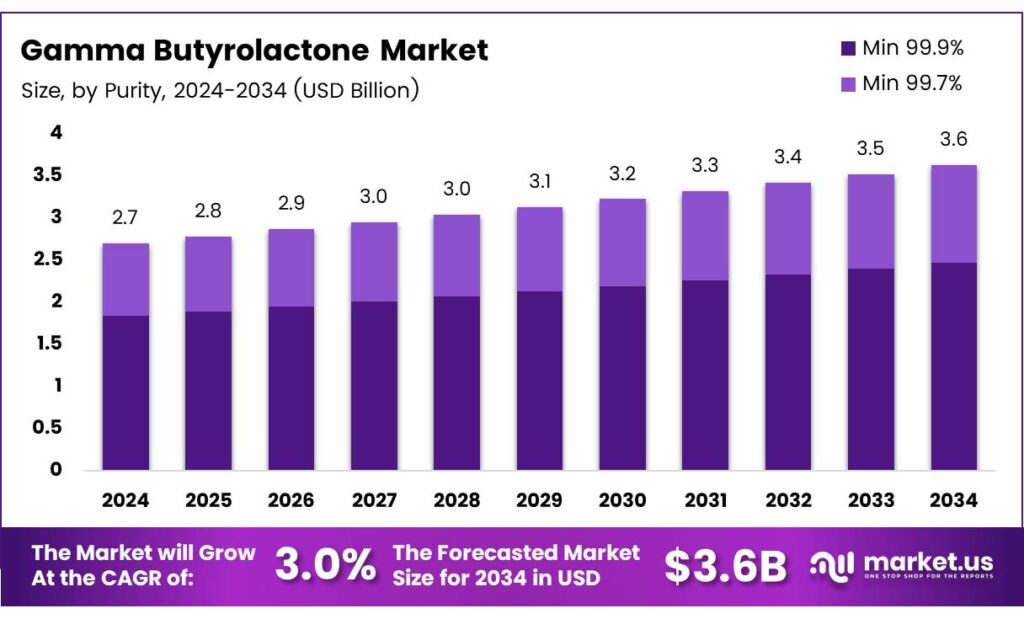

The Global Gamma Butyrolactone Market size is expected to be worth around USD 3.6 billion by 2034 from USD 2.7 billion in 2024, growing at a CAGR of 3.0% during the forecast period 2025 to 2034.

Gamma-butyrolactone (GBL) is a clear, water-soluble lactone chemical with broad industrial utility. Manufacturers widely use it as a high-performance solvent, a key battery electrolyte component, and a versatile intermediate in pharmaceutical synthesis. Its unique chemical properties make it one of the most sought-after specialty solvents in modern industrial chemistry.

GBL serves multiple downstream industries simultaneously. Pharmaceutical companies rely on it as a drug precursor solvent, while electronics manufacturers use it for circuit board cleaning. Additionally, agrochemical producers incorporate it into herbicide and pesticide formulations, and the energy sector adopts it in lithium-ion battery electrolytes.

- India’s gamma-butyrolactone import market recorded 691 total shipments from 13 exporting countries involving 133 suppliers and 84 buyers, illustrating a diversified and active global trade network. This breadth of trade activity reflects strong downstream demand across pharmaceuticals, solvents, and specialty chemicals in emerging Asian markets.

- International Diol Company maintains a dedicated GBL productive capacity of 5,000 metric tons per annum, operating alongside 76,500 mtpa of tetrahydrofuran and 50,000 mtpa of butanediol. This production scale highlights the growing role of Middle Eastern petrochemical groups in supplying global GBL demand.

Market growth draws support from rapid industrialization across the Asia-Pacific, rising electric vehicle production, and expanding pharmaceutical output. Consequently, demand for high-purity GBL grades continues to accelerate. Moreover, government policies promoting clean energy and sustainable chemistry further reinforce investment in GBL-related production capacities worldwide.

Key Takeaways

- The Global Gamma Butyrolactone Market was valued at USD 2.7 billion in 2024 and is projected to reach USD 3.6 billion by 2034, at a CAGR of 3.0% during the forecast period 2025–2034.

- The Min 99.9% segment held a dominant share of 67.2% in 2025.

- The Solvent segment led the market with a 39.5% share in 2025.

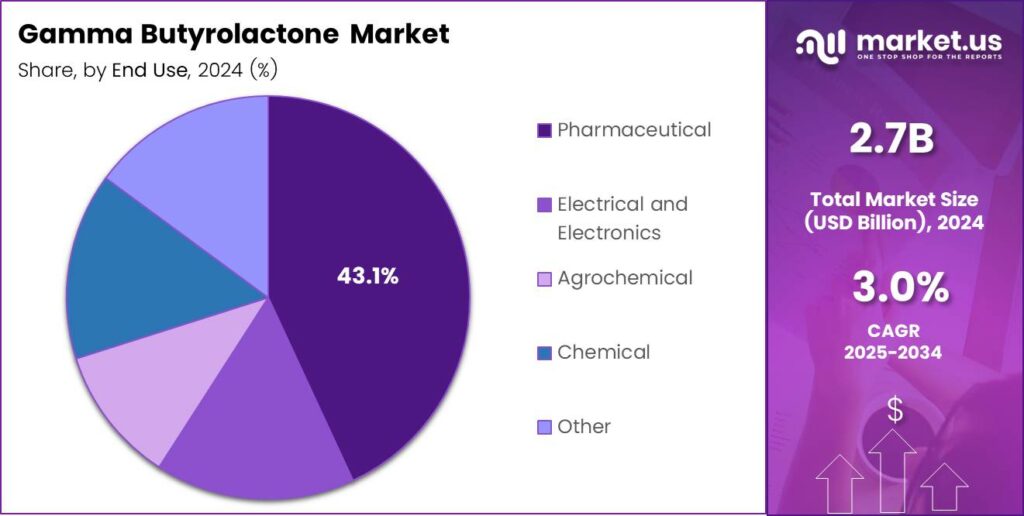

- The Pharmaceutical segment dominated with a 43.1% market share in 2025.

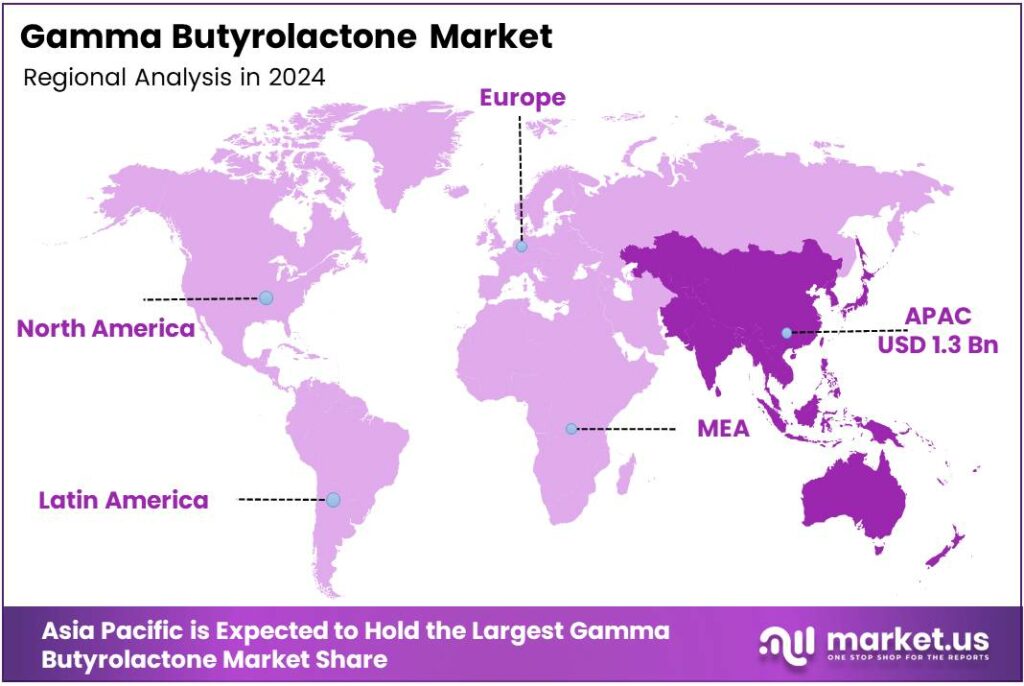

- Asia Pacific held the largest regional share at 47.9%, valued at approximately USD 1.3 billion in 2025.

By Purity Analysis

Min 99.9% dominates with 67.2% due to rising demand from electronics, battery, and pharmaceutical industries requiring ultra-high purity GBL.

In 2025, Min 99.9% held a dominant market position in the By Purity segment of the Gamma Butyrolactone Market, with a 67.2% share. Electronics manufacturers and battery producers demand this grade for precision applications where trace impurities can compromise performance. Moreover, pharmaceutical companies prioritize ultra-high purity GBL to meet strict drug safety and regulatory standards, reinforcing this segment’s leadership.

Min 99.7% represents the secondary purity tier, serving industrial users where slightly lower purity levels remain acceptable. Chemical manufacturers and agrochemical producers commonly adopt this grade for large-scale solvent and synthesis applications. Consequently, the Min 99.7% segment supports cost-sensitive end uses while maintaining adequate performance standards across mainstream industrial processes.

By Application Analysis

Solvent dominates with 39.5% due to GBL’s superior solvency power, miscibility, and low toxicity profile compared to many conventional industrial solvents.

In 2025, Solvent held a dominant market position in the By Application segment of the Gamma Butyrolactone Market, with a 39.5% share. Electronics and chemical industries rely on GBL as a high-boiling, water-miscible solvent for cleaning, stripping, and formulation. Additionally, its low vapor pressure and stable thermal properties make it a preferred choice for demanding industrial solvent applications.

Batteries and Capacitors represent a rapidly growing application segment, driven by the global electric vehicle boom and energy storage expansion. GBL serves as a key electrolyte component in lithium-ion cells, improving low-temperature performance and ionic conductivity. Therefore, battery manufacturers increasingly specify GBL-based formulations as cell energy density and safety requirements become more stringent.

Herbicides and Insecticides form a significant agrochemical application where GBL functions as a synthesis intermediate. Agrochemical producers incorporate it in the production of crop protection actives and plant growth regulators. Moreover, rising global food demand drives agrochemical output, consequently expanding GBL consumption in this segment across the Asia-Pacific and Latin American markets.

Sedative and Anesthetic applications cover GBL’s pharmaceutical use as a precursor to gamma-hydroxybutyrate-based compounds. Research institutions and licensed pharmaceutical manufacturers use controlled-grade GBL in drug development and clinical compound synthesis. However, regulatory restrictions on GBL as a controlled substance precursor require licensed procurement and audited supply chains for this application.

By End Use Analysis

Pharmaceutical dominates with 43.1% due to GBL’s indispensable role as a drug precursor solvent and active ingredient synthesis intermediate across global pharma operations.

In 2025, Pharmaceutical held a dominant market position in the By End Use segment of the Gamma Butyrolactone Market, with a 43.1% share. Drug manufacturers use GBL in the synthesis of active pharmaceutical ingredients, excipient formulations, and reaction solvent systems. Moreover, expanding generic drug production in India and China drives significant GBL procurement volumes across Asian pharmaceutical supply chains.

Electrical and Electronics end users consume GBL primarily for circuit board cleaning, semiconductor fabrication, and battery electrolyte manufacturing. Rising global electronics output, particularly in the Asia-Pacific region, sustains consistent demand. Additionally, advancements in electric vehicle batteries and energy storage systems create new high-purity GBL consumption volumes within this end-use category.

Agrochemical producers use GBL as an intermediate in herbicide, pesticide, and plant growth regulator synthesis. Growing food security concerns and expanding farmland management practices in emerging economies support this segment. Consequently, agrochemical companies increase GBL procurement in line with the rising production of crop protection formulations across South Asia and Southeast Asia.

Chemical industry users incorporate GBL in polymer production, resin formulations, and specialty chemical synthesis. The segment benefits from GBL’s versatile chemical reactivity and compatibility with a wide range of industrial processes. Therefore, large chemical manufacturers maintain consistent GBL sourcing as a core raw material across their product portfolios.

Key Market Segments

By Purity

- Min 99.9%

- Min 99.7%

By Application

- Solvent

- Batteries and Capacitors

- Herbicides and Insecticides

- Sedative and Anesthetic

- Others

By End Use

- Pharmaceutical

- Electrical and Electronics

- Agrochemical

- Chemical

- Other

Emerging Trends

High-Purity GBL and Green Chemistry Drive the Next Phase of Market Evolution

Industry players observe a strong shift toward high-purity GBL grades of ≥99.9% for advanced electronics and battery applications. Manufacturers serving semiconductor and EV battery customers now require ultra-refined solvent grades to meet product performance specifications. In 2025, Biosynth expanded its catalog of functionalized butyrolactone derivatives for research and lab use, reflecting growing scientific interest in high-purity GBL chemistry.

- Green chemistry initiatives increasingly position GBL as a safer alternative to conventional industrial solvents. Chemical companies integrate GBL into low-emission formulations targeting workplace safety and environmental compliance goals. The average GBL import price stood at $1.59 per unit, suggesting a cost-competitive positioning that supports broader adoption in eco-friendly formulations across regulated markets.

Industry consolidation and capacity expansions focused on sustainable manufacturing shape competitive dynamics. Producers invest in bio-based GBL production routes and strategic research collaborations to strengthen specialty product portfolios. Additionally, growing preference for GBL in clean-label agrochemical and food-grade functional formulations reflects a broader industry pivot toward traceable, low-impact chemical inputs.

Drivers

Pharmaceutical Demand, EV Growth, and Electronics Manufacturing Accelerate GBL Market Expansion

The pharmaceutical sector drives the largest share of GBL demand globally. Drug manufacturers use it extensively as a versatile precursor solvent and active ingredient synthesis intermediate. In 2025, Ashland announced a global price increase for its 1,4-butanediol intermediates range, including GBL, reflecting tight supply conditions driven by sustained pharmaceutical procurement volumes across key markets.

- The electric vehicle boom accelerates GBL adoption in lithium-ion battery electrolyte formulations. Battery producers specify GBL-based electrolytes for improved low-temperature ionic conductivity and cell performance. The United States received 103 GBL import shipments between May 2023 and April 2025, with India supplying 93% of that import volume by shipment count, demonstrating active cross-border trade flows driven by EV sector demand.

Surging electronics manufacturing further supports GBL consumption across circuit board cleaning and semiconductor fabrication segments. Manufacturers in Asia-Pacific increasingly adopt GBL for precision cleaning applications where solvent purity and low residue profiles are critical. Moreover, rising agrochemical production in emerging economies fuels additional GBL usage in herbicide and pesticide intermediate synthesis.

Restraints

Regulatory Controls and Raw Material Price Volatility Constrain GBL Market Growth

Stringent global regulatory controls present the most significant barrier to GBL market growth. Governments in the United States, the European Union, and several Asian jurisdictions classify GBL as a precursor to gamma-hydroxybutyrate (GHB), a controlled narcotic substance. Consequently, producers and distributors must maintain detailed import-export licensing, end-user verification, and transaction reporting to comply with international chemical control frameworks.

- Compliance obligations add substantial administrative costs and create market access barriers for smaller producers. Chemical companies without an established regulatory infrastructure struggle to enter or expand in controlled markets. According to BASF’s preliminary 2025 disclosure, full-year sales are expected at €59.7 billion, down from €61.4 billion in 2024, reflecting broader pricing pressure across the chemicals industry that also squeezes GBL value-chain margins.

Persistent volatility in 1,4-butanediol raw material prices compounds cost management challenges for GBL producers. Feedstock price swings reduce margin predictability and complicate long-term supply contract negotiations. Moreover, increasing environmental compliance costs related to emissions controls and waste treatment requirements further elevate production costs, discouraging capacity investments in markets with strict environmental enforcement.

Growth Factors

Asia-Pacific Industrialization, Bio-Based Innovation, and Cosmetics Adoption Fuel Long-Term GBL Growth

Asia-Pacific emerging markets offer the most significant untapped expansion potential for GBL producers. Rapid industrialization, pharmaceutical output growth, and rising electronics manufacturing across India, Vietnam, and Indonesia create new demand centers. India recorded 248 GBL import shipments between July 2024 and June 2025 from 20 Indian buyers and 15 suppliers, illustrating robust and growing commercial import activity.

- Development of bio-based and low-emission GBL production routes opens new market opportunities aligned with corporate sustainability mandates. Chemical companies invest in renewable feedstock research and green process engineering to reduce carbon footprints. Sipchem’s planned capacity expansions, including its blue ammonia project and ethylene vinyl acetate plant expansion by 70,000 tons, reflect upstream investments that support GBL’s intermediate supply chain growth.

Strategic research collaborations drive the development of high-purity specialty GBL derivatives with enhanced functional properties. Academic institutions and specialty chemical companies partner to explore novel GBL applications in advanced materials and drug delivery. Additionally, rising adoption in cosmetics and personal care markets for eco-friendly emulsifying and solvent applications adds a new and structurally growing demand channel.

Regional Analysis

Asia Pacific Dominates the Gamma Butyrolactone Market with a Market Share of 47.9%, Valued at USD 1.3 Billion

Asia Pacific commands a dominant 47.9% share of the global gamma-butyrolactone market, valued at approximately USD 1.3 billion. The region’s leadership reflects its massive pharmaceutical manufacturing base in India and China, expanding electronics and battery production across South Korea, Japan, and Southeast Asia, and rapidly growing agrochemical industries.

North America represents a mature and tightly regulated GBL market, led by the United States. Pharmaceutical research, specialty chemical manufacturing, and advanced battery production drive consistent demand. The US recorded 103 GBL import shipments between May 2023 and April 2025, indicating stable commercial procurement despite regulatory oversight requirements for controlled substance precursors.

Europe maintains a significant GBL market anchored by its pharmaceutical, specialty chemical, and advanced materials industries. Germany, France, and the Netherlands serve as primary consumption hubs. However, strict European Chemicals Agency (ECHA) regulations and GHB precursor controls add compliance complexity for producers and distributors operating across EU member states, moderating market expansion compared to Asia-Pacific growth rates.

Latin America presents a developing GBL market with growth driven by expanding agrochemical and pharmaceutical sectors in Brazil and Mexico. Rising crop protection chemical demand and growing generic drug manufacturing create incremental GBL procurement volumes. Additionally, improving regional chemical distribution infrastructure supports more reliable GBL supply access for downstream industrial users across the continent.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Ashland operates as a leading global specialty chemicals company with a strong position in solvent and intermediate chemical supply chains. The company serves pharmaceutical, electronics, and industrial markets through a diversified product portfolio that includes GBL and related lactone chemistry. In 2025, Ashland announced a global price increase for its 1,4-butanediol intermediates and solvents range, including GBL, reflecting its ability to exercise market pricing influence.

Balaji Amines is a major Indian specialty chemicals manufacturer with integrated production capabilities across amines, solvents, and related intermediates. The company serves both domestic pharmaceutical clients and international export markets from its manufacturing base in India. Its strategic positioning within India’s growing chemicals export infrastructure supports its role as a competitive GBL and specialty solvent supplier to global buyers.

Biosynth specializes in fine chemicals, research reagents, and specialty biochemicals for pharmaceutical and life sciences applications. The company maintains a broad catalog of butyrolactone derivatives and high-purity GBL variants for research and development use. In 2025, Biosynth expanded its range of functionalized butyrolactone derivatives, serving the growing demand from academic and industrial research laboratories worldwide.

CDH Fine Chemical provides laboratory-grade and industrial chemicals, including GBL and related specialty solvents, to research and manufacturing customers. The company serves a broad base of pharmaceutical, chemical, and institutional laboratory clients across Asian markets. Its focus on product quality, reliable supply, and technical support positions it as a trusted supplier within the fine chemical and reagent distribution segment.

Top Key Players in the Market

- Ashland

- Balaji Amines

- Biosynth

- CDH Fine Chemical

- Chang Chun Group

- Dairen Chemical Corporation

- Dongao Chemical

- Hefei TNJ Chemical Industry Co., Ltd.

- Mitsubishi Chemical Group

Recent Developments

- In 2025, Ashland announced a global price increase for its 1-4-Butanediol intermediates and solvents range. Gamma-butyrolactone (BLO) saw a minimum increase(or equivalent in euros), effective as stated in the release. This applies alongside increases for related products like N-methyl-pyrrolidone (NMP).

- In 2025, Biosynth (specialty/fine chemicals and research reagents supplier) offers various substituted or functionalized butyrolactone derivatives for research and lab use (e.g., α-Methylene-γ-butyrolactone, (S)-(+)-gamma-Hydroxymethyl-γ-butyrolactone, α-Hydroxy-γ-butyrolactone). These appear in their online catalog as high-purity research chemicals.

Report Scope

Report Features Description Market Value (2024) USD 2.7 Billion Forecast Revenue (2034) USD 3.6 Billion CAGR (2025-2034) 3.0% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Purity (Min 99.9%, Min 99.7%), By Application (Solvent, Batteries and Capacitors, Herbicides and Insecticides, Sedative and Anesthetic, Others), By End Use (Pharmaceutical, Electrical and Electronics, Agrochemical, Chemical, Other) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Ashland, Balaji Amines, Biosynth, CDH Fine Chemical, Chang Chun Group, Dairen Chemical Corporation, Dongao Chemical, Hefei TNJ Chemical Industry Co., Ltd., Mitsubishi Chemical Group Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Gamma Butyrolactone MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Gamma Butyrolactone MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Ashland

- Balaji Amines

- Biosynth

- CDH Fine Chemical

- Chang Chun Group

- Dairen Chemical Corporation

- Dongao Chemical

- Hefei TNJ Chemical Industry Co., Ltd.

- Mitsubishi Chemical Group

Our Clients

- 178931

- February 2026