Quick Navigation

Report Overview

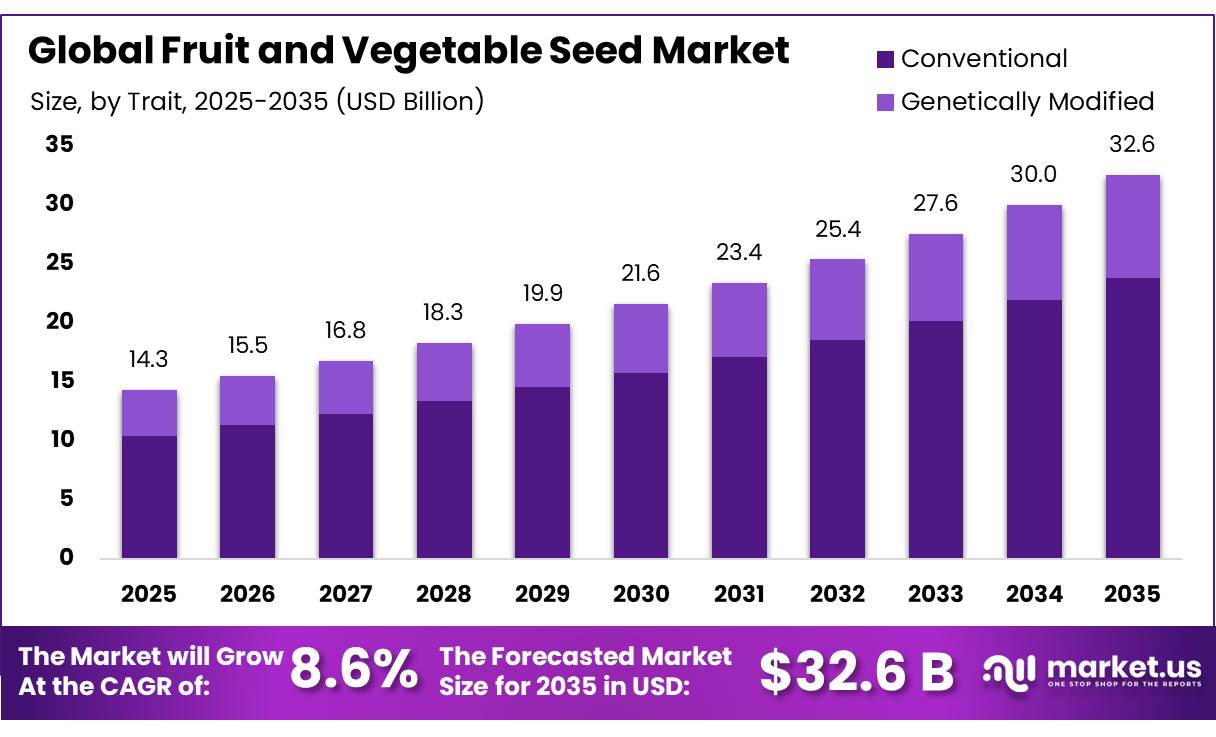

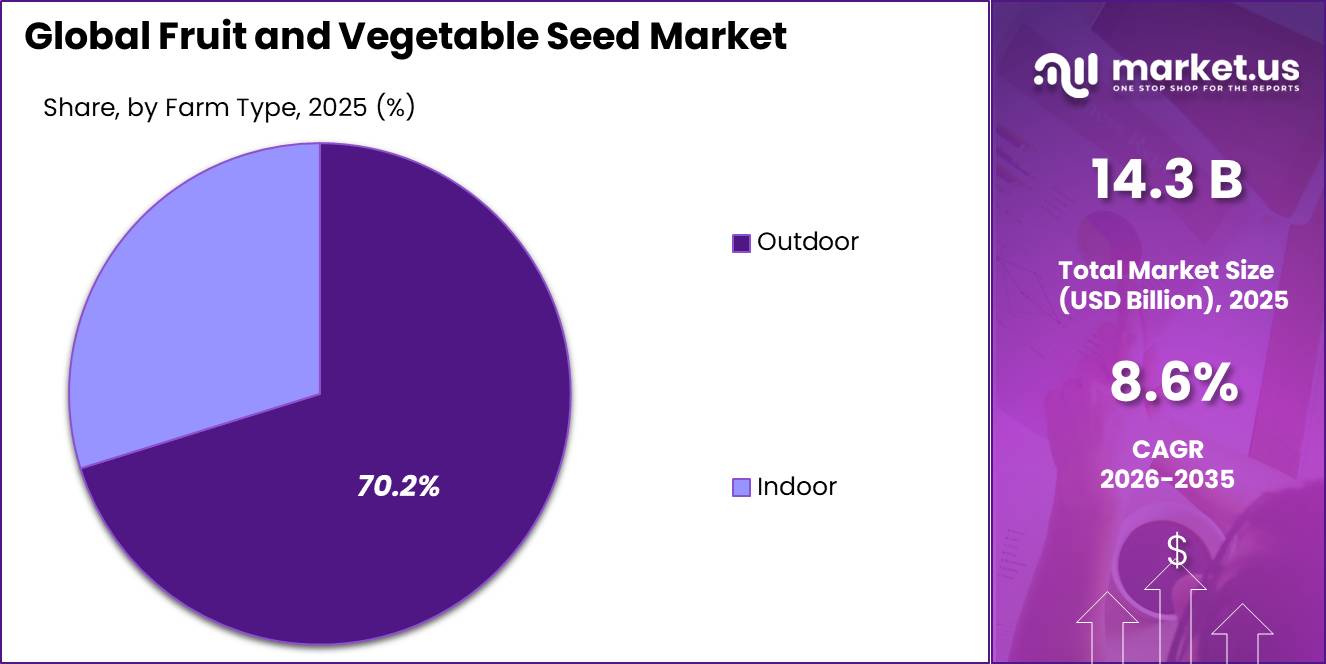

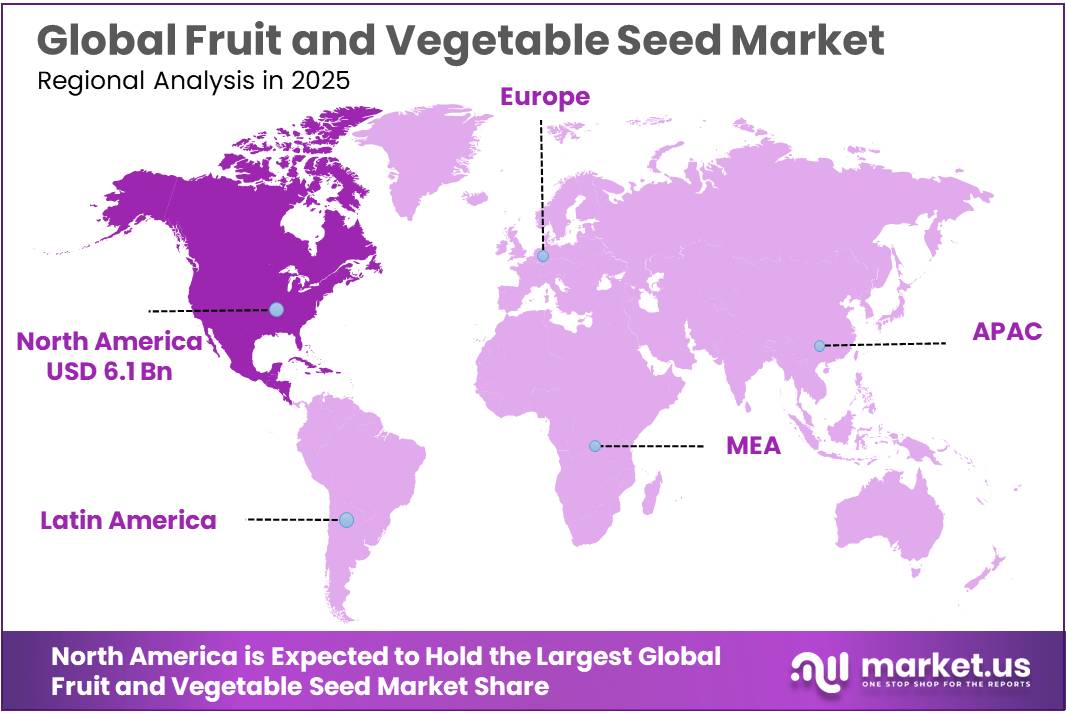

The Global Fruit and Vegetable Seed Market size is expected to be worth around USD 32.6 Billion by 2035, from USD 14.3 Billion in 2025, growing at a CAGR of 8.6% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 42.80% share, holding USD 6.1 Billion revenue.

The fruit and vegetable seed industry forms a critical base for global horticulture, as seed quality directly affects yield, crop uniformity, disease resistance, shelf life, and farm profitability. The sector serves growers producing tomatoes, peppers, onions, melons, cucumbers, carrots, leafy vegetables, and fruit crops for fresh and processed food channels. In 2024, the EU produced 63.8 million tonnes of vegetables and 40.8 million tonnes of fruits and nuts, while fresh fruit and vegetables accounted for 13.4% of total EU agricultural production, valued at EUR 72.2 billion.

Key Takeaways

- Fruit and Vegetable Seed Market size is expected to be worth around USD 32.6 Billion by 2035, from USD 14.3 Billion in 2025, growing at a CAGR of 8.6%.

- Solanaceae held a dominant market position, capturing more than a 37.30% share.

- Conventional held a dominant market position, capturing more than a 73.10% share.

- Inorganic held a dominant market position, capturing more than a 64.30% share.

- Outdoor held a dominant market position, capturing more than a 70.20% share.

- North America held a dominant position in the global Fruit and Vegetable Seed Market, accounting for 42.80% of the total market and reaching a value of approximately USD 6.1 Billion.

According to FAO, world fruit and vegetable production reached 2.1 billion tonnes in 2023, rising 1% from 2022. This large production base shows why improved hybrid and open-pollinated seeds are becoming more important for food security, nutrition supply, and climate-resilient farming. The OECD-FAO outlook also notes that meeting future food demand will require a 10% rise in food production and a 15% improvement in agricultural productivity by 2034, making improved seeds a key input for the fruit and vegetable value chain.

The industrial scenario is being shaped by higher demand for fresh produce, controlled-environment farming, export-quality vegetables, and seeds that can perform under heat, drought, pest pressure, and changing rainfall patterns. OECD-FAO’s 2025–2034 outlook highlights that agricultural growth will depend more on productivity improvement than land expansion, which supports demand for better seed genetics. In this environment, seed companies are investing in breeding, digital crop selection, seed treatment, and regional varieties suited to local soil and climate conditions.

Growth is driven by rising fresh produce demand, climate stress, disease pressure, labor shortages, and the need for higher farm output from limited land. The International Seed Federation noted that the global seed market is around USD 90 billion, while nearly 7 million tons of seeds are exported worldwide each year, showing how seed trade supports food security and crop diversity.

Government support is also helping the sector. In 2025, USDA announced USD 72.9 million under the Specialty Crop Block Grant Program to improve competitiveness of fruits, vegetables, tree nuts, dried fruits, and horticulture crops through research, marketing, education, and innovation. In Europe, vegetable output also grew from 58.8 million tonnes in 2023 to 62.2 million tonnes in 2024, showing stronger demand for dependable seed systems.

BASF SE also holds a strong position through its Nunhems vegetable seed brand. BASF Agricultural Solutions generated €9,587 million in sales in 2025, while its vegetable seed business offered more than 1,200 seed varieties across 20 vegetable crops. Nunhems focuses on crops such as tomatoes, onions, carrots, peppers, cucumbers, melons, and lettuce, with breeding programs designed for disease resistance, taste, shelf life, labor efficiency, and climate stress tolerance. Reuters also reported in 2025 that BASF’s agriculture arm was increasing its focus on seeds, with seed revenue targeted to rise from 22% of the unit’s sales to around 25%.

By Type Analysis

Manual Blowing Torch dominates with 42.5% due to its widespread availability and cost-effectiveness.

In 2025, Solanaceae held a dominant market position, capturing more than a 37.30% share in the global Fruit and Vegetable Seed Market. The segment maintained its leadership due to strong commercial demand for high-value vegetable crops such as tomato, pepper, eggplant, and other widely cultivated varieties. Solanaceae seeds continued to receive strong adoption from professional growers because of their high productivity, better disease resistance, and improved yield performance across controlled and open-field farming systems.

The segment’s growth was also supported by increasing consumption of fresh vegetables and the rising preference for premium-quality produce in developed and emerging agricultural economies. Seed producers continued to focus on introducing improved Solanaceae varieties with stronger germination rates, climate adaptability, and longer shelf life characteristics. These developments helped growers improve output quality while reducing crop losses.

By Trait Analysis

Conventional dominates with 73.10% due to its broad cultivation base and established seed adoption.

In 2025, Conventional held a dominant market position, capturing more than a 73.10% share in the global Fruit and Vegetable Seed Market. The segment maintained its leading position as growers continued to prefer conventional seeds because of their cost efficiency, wide availability, and long-standing acceptance across commercial and small-scale farming operations. Conventional seed varieties remained a practical choice for producers seeking reliable crop performance without the additional investment associated with advanced trait technologies.

The strong presence of this segment was also supported by established agricultural practices and existing seed distribution networks across major fruit and vegetable producing regions. Farmers continued to select conventional seeds for their stable output, ease of cultivation, and compatibility with different climatic and soil conditions. These factors supported consistent planting decisions across multiple crop cycles.

By Category Analysis

Inorganic dominates with 64.30% due to its strong commercial adoption and higher production consistency.

In 2025, Inorganic held a dominant market position, capturing more than a 64.30% share in the global Fruit and Vegetable Seed Market. The segment maintained its leading position as large-scale growers continued to rely on inorganic cultivation practices to achieve higher productivity, predictable crop output, and efficient farm management. The widespread use of conventional agricultural inputs and structured production systems supported stronger demand for seeds used in inorganic farming operations.

The dominance of this segment was also supported by the ability of inorganic cultivation methods to deliver stable harvest cycles and support year-round fruit and vegetable production. Commercial farming operations continued to prefer these practices due to their scalability and suitability for meeting rising global food demand. In addition, established agricultural infrastructure and broad availability of cultivation inputs encouraged continued seed usage under this category.

By Farm Type Analysis

Outdoor dominates with 70.20% due to its extensive cultivation area and strong dependence on open-field farming.

In 2025, Outdoor held a dominant market position, capturing more than a 70.20% share in the global Fruit and Vegetable Seed Market. The segment maintained its leadership because open-field cultivation continued to be the preferred farming method for large-scale fruit and vegetable production. Outdoor farming supported broader planting capacity, lower infrastructure requirements, and greater accessibility for growers across commercial and traditional agricultural operations.

The strong position of this segment was further supported by the large availability of agricultural land and the continued use of established cultivation practices. Farmers remained dependent on outdoor environments for growing a wide range of fruit and vegetable crops due to operational flexibility and efficient land utilization. The segment also benefited from seasonal planting cycles that supported consistent demand for seed products across multiple growing regions.

Key Market Segments

By Type

- Solanaceae

- Cucurbits

- Brassica

- Amaryllidaceous

- Citrus Family

- others

By Trait

- Conventional

- Genetically Modified

By Category

- Inorganic

- Organic

By Farm Type

- Outdoor

- Indoor

Market Dynamics

Driver Analysis - Rising Global Fresh Produce Consumption Drives Seed Demand

One of the major driving factors for the Fruit and Vegetable Seed Market is the continuous increase in global demand for fresh fruits and vegetables, supported by changing food consumption patterns, higher awareness of healthy diets, and the need for reliable agricultural output. As consumers increasingly include fresh produce in daily meals, growers are under pressure to improve productivity, crop quality, and supply consistency, which directly increases demand for high-performance fruit and vegetable seeds.

According to the Food and Agriculture Organization (FAO), global fruit and vegetable production reached approximately 2.1 billion tonnes in 2023, showing continued expansion compared with previous years. This growth reflects sustained demand across household, retail, and food service channels. Rising production volumes require a stable supply of quality seeds that can support better germination, improved resistance, and consistent harvest cycles.

Government and international food agencies are also supporting agricultural productivity and food security through long-term development programs. FAO’s agricultural statistics show that global primary crop production reached 9.9 billion tonnes in 2023, increasing by 3% compared with the previous year and rising by 27% since 2010. This ongoing growth highlights how agricultural systems are expanding to meet food requirements, creating stronger demand for improved seed availability across fruit and vegetable cultivation.

Restraint Analysis - Climate Variability And Crop Losses Limit Seed Adoption

One of the major restraining factors for the Fruit and Vegetable Seed Market is the increasing impact of climate variability and crop production losses. Fruit and vegetable cultivation depends heavily on stable weather conditions, soil quality, and predictable growing cycles. However, changing rainfall patterns, prolonged droughts, heat stress, floods, and rising pest pressure are creating uncertainty for growers. As production risks increase, farmers often delay investments in premium or improved seed varieties, which directly affects seed demand.

- According to the Food and Agriculture Organization (FAO), up to 40% of global crop production is lost every year because of plant pests and diseases. These losses create major financial pressure across agricultural systems and reduce confidence in investing in higher-value seed inputs for fruit and vegetable cultivation. FAO also estimates that crop losses linked to pests and diseases cost the global economy more than USD 220 billion annually.

Climate-related disruptions are creating additional pressure on agricultural output. FAO reported that climate change reduced average crop yields globally by more than 5% during 2000–2019. Rising temperatures, irregular precipitation, and frequent extreme weather events continue to affect crop establishment and productivity, making seed selection and planting decisions more difficult for producers.

Government and international organizations are responding through climate adaptation and sustainable agriculture programs. FAO continues supporting countries with resilient farming practices, improved crop management systems, and better agricultural planning to strengthen food security and reduce production risks. Despite these efforts, weather uncertainty remains a major challenge for seed suppliers and growers.

Opportunity Analysis - Expanding Protected Farming Creates Strong Seed Opportunities

One major growth opportunity for the Fruit and Vegetable Seed Market is the rapid expansion of protected farming and controlled-environment agriculture. Greenhouses, tunnel farming, and other protected cultivation systems are increasing across several agricultural economies as growers focus on improving productivity, reducing climate-related risks, and producing consistent crop quality. These farming methods require specialized fruit and vegetable seeds with stronger germination performance, disease resistance, and suitability for intensive cultivation systems.

Additional opportunity comes from the long-term outlook for food production. According to the OECD–FAO Agricultural Outlook 2024–2033, global agricultural output is expected to increase by around 10% by 2033, driven mainly by productivity improvements rather than expansion of farmland. This shift places greater importance on improved planting materials and seed technologies that can deliver better crop performance from existing agricultural land.

Government-backed initiatives are also encouraging adoption of sustainable and resilient agricultural practices. The Food and Agriculture Organization continues to promote climate-smart agriculture and resource-efficient cultivation models that support higher crop productivity and stronger food security outcomes. These developments create favorable conditions for fruit and vegetable seed producers to introduce specialized seed varieties aligned with changing production requirements.

Emerging Trend Analysis - Climate Resilient Seed Development Gains Industry Momentum

One of the major latest trends shaping the Fruit and Vegetable Seed Market is the growing development and adoption of climate-resilient seed varieties. Seed producers and agricultural organizations are increasingly focusing on developing seeds that can perform under changing weather conditions, including drought, temperature fluctuations, irregular rainfall, and rising pest pressure. This trend is becoming important as agricultural systems seek stable crop production while protecting food availability.

According to the Food and Agriculture Organization (FAO), approximately 733 million people faced hunger globally in 2023, increasing pressure on agricultural systems to improve crop productivity and resilience. At the same time, agriculture remains highly exposed to climate variability, encouraging investment in stronger and more adaptable seed genetics for fruits and vegetables. Improved seed varieties are helping growers maintain production efficiency and reduce crop failure risks under changing environmental conditions.

Government and international initiatives are also supporting this transition. FAO continues promoting climate-smart agriculture programs aimed at strengthening agricultural resilience, reducing production losses, and improving sustainable food production. These initiatives encourage innovation in seed development and wider use of improved planting materials.

Regional Insights

North America Dominates Fruit and Vegetable Seed Market with 42.80% Share

In 2025, North America held a dominant position in the global Fruit and Vegetable Seed Market, accounting for 42.80% of the total market and reaching a value of approximately USD 6.1 Billion. The region continued to lead due to its advanced agricultural infrastructure, strong commercial farming operations, and consistent adoption of improved seed varieties across fruit and vegetable cultivation. High awareness of crop quality, efficient production systems, and continued investment in agricultural productivity supported market expansion across the region.

The United States remained the key contributor to regional growth, supported by large-scale production of vegetables and fruits and extensive use of improved planting materials. Commercial growers continued focusing on high-yield seed varieties that support better crop quality, disease resistance, and improved harvest consistency. Rising consumer demand for fresh produce and year-round product availability also encouraged stronger seed usage across multiple crop categories.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE plays an important role in the Fruit and Vegetable Seed Market by combining seed development with agricultural solutions designed to improve crop productivity. The company continues expanding vegetable seed offerings through advanced breeding capabilities and sustainable farming support. In 2025, BASF maintained investment in agricultural innovation programs and expanded activities focused on seed quality and crop resilience. The company generated approximately EUR 65.3 billion in annual sales and continued supporting commercial fruit and vegetable cultivation through integrated agricultural technologies and seed development initiatives.

Bayer AG remains one of the major participants in the Fruit and Vegetable Seed Market through its broad seed portfolio and continuous investment in crop improvement. The company supports fruit and vegetable growers with breeding programs focused on yield enhancement, disease resistance, and climate adaptability. In 2025, Bayer continued strengthening seed innovation through digital agriculture integration and advanced breeding technologies. The company reported approximately EUR 46.6 billion in total sales in 2025 and continued allocating significant investment toward agricultural R&D activities, supporting long-term development across commercial fruit and vegetable seed operations.

Top Key Players Outlook

- Bayer AG (Germany)

- BASF SE (Germany)

- Sakata Seed Corporation (Japan)

- Syngenta Group (Switzerland)

- DLF (Denmark)

- Takii & Co Ltd (Japan)

- Longping Hitech (China)

- Enza Zaden (Netherlands)

- FMC Corporation (US)

- Vikima Seeds (Denmark)

- East-West Seeds (Thailand)

- RIJK ZWAAN ZAADTEELT EN ZAADHANDELBY (Netherlands)

- Bejo Zaden BV (Netherlands)

Recent Developments

In 2025, DLF strengthened its portfolio focus by forming United Beet Seeds with Groupe Florimond Desprez and transferring its Danespo seed potato shareholding, where GFD reached 98% ownership. This showed DLF’s strategy of focusing capital on core seed platforms, breeding, production, and international expansion rather than broad fruit and vegetable seed acquisitions.

In 2025, Syngenta Group strengthened its role in the Fruit and Vegetable Seed sector through its global vegetable seed business, which covers 30 crop species, more than 2,500 products, and serves growers in over 120 countries. The company reported USD 4.8 billion in seed sales in 2025, with vegetable seeds showing solid growth and a stable market environment. During the first 9 months of 2025, Syngenta Seeds recorded USD 3.3 billion in sales, while vegetable seed sales increased by 3%, showing steady demand from commercial growers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 14.3 Bn |

| Forecast Revenue (2035) | USD 32.6 Bn |

| CAGR (2026-2035) | 8.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Solanaceae, Cucurbits, Brassica, Amaryllidaceous, Citrus Family, others), By Trait (Conventional, Genetically Modified), By Category (Inorganic, Organic), By Farm Type (Outdoor, Indoor) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bayer AG (Germany), BASF SE (Germany), Sakata Seed Corporation (Japan), Syngenta Group (Switzerland), DLF (Denmark), Takii & Co Ltd (Japan), Longping Hitech (China), Enza Zaden (Netherlands), FMC Corporation (US), Vikima Seeds (Denmark), East-West Seeds (Thailand), RIJK ZWAAN ZAADTEELT EN ZAADHANDELBY (Netherlands), Bejo Zaden BV (Netherlands) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |