Global Free Space Optics Backhaul Market Size, Share, Growth Analysis By Component (Transmitters, Receivers, Modulators, Demodulators, Others), By Application (Telecommunications, Military and Defense, Healthcare, Enterprise, Others), By Transmission Range (Short Range, Medium Range, Long Range), By Data Rate (Up to 10 Gbps, 10–40 Gbps, Above 40 Gbps), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 182637

- Number of Pages: 350

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Core Key Insights

- Network Analysis

- Future Predictions

- Market Outlook

- Key Market Segments

- Research-Based Segments

- By Component Analysis

- By Application Analysis

- By Transmission Range Analysis

- By Data Rate Analysis

- Regional Analysis

- US Market Size

- Driving Factors

- Restraint Factors

- Growth Opportunities

- Trending Factors

- Competitive Analysis

- Recent Developments

- Report Scope

Report Overview

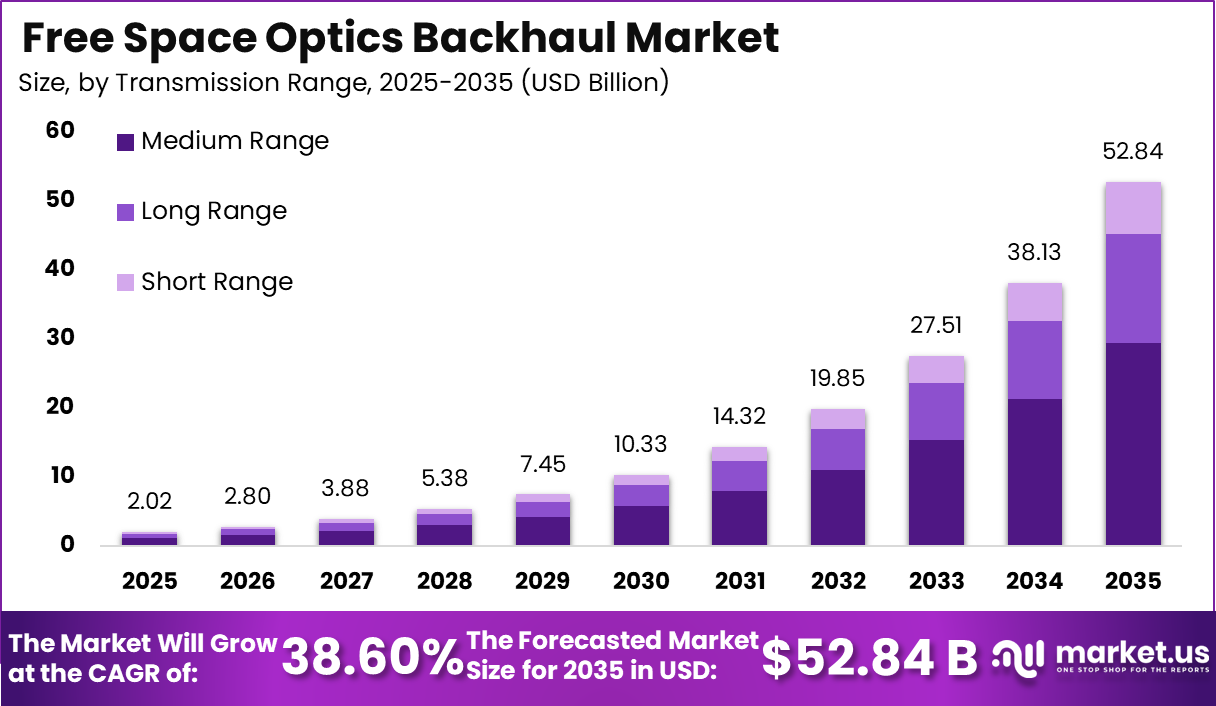

The Free Space Optics (FSO) Backhaul Market, the data indicates a strong growth trajectory driven by rising demand for high-capacity, wireless communication infrastructure. The market is valued at USD 2.02 billion in 2025 and is projected to reach USD 52.84 billion by 2035, reflecting a CAGR of 38.60%. This rapid expansion highlights the increasing need for fiber-like speeds without the complexity and cost of physical cable deployment, especially in urban and remote connectivity scenarios.

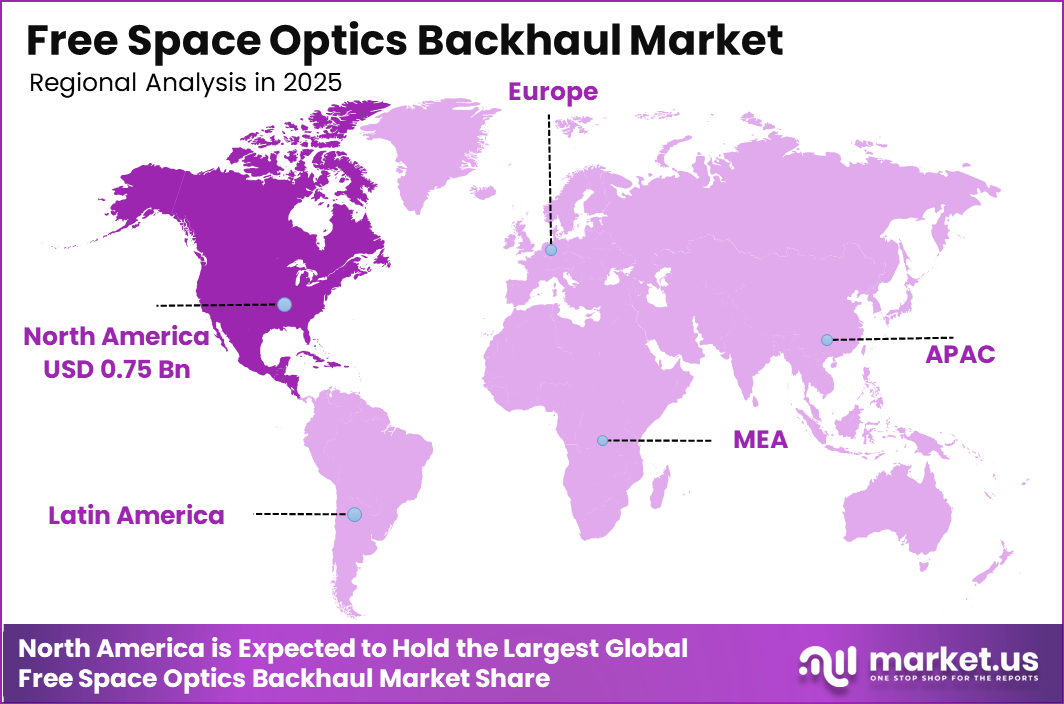

From a regional perspective, North America holds a dominant position with a 37.2% market share, accounting for USD 0.75 billion in 2025. This leadership is supported by advanced telecom infrastructure, early adoption of next-generation networking technologies, and strong investments in 5G backhaul solutions.

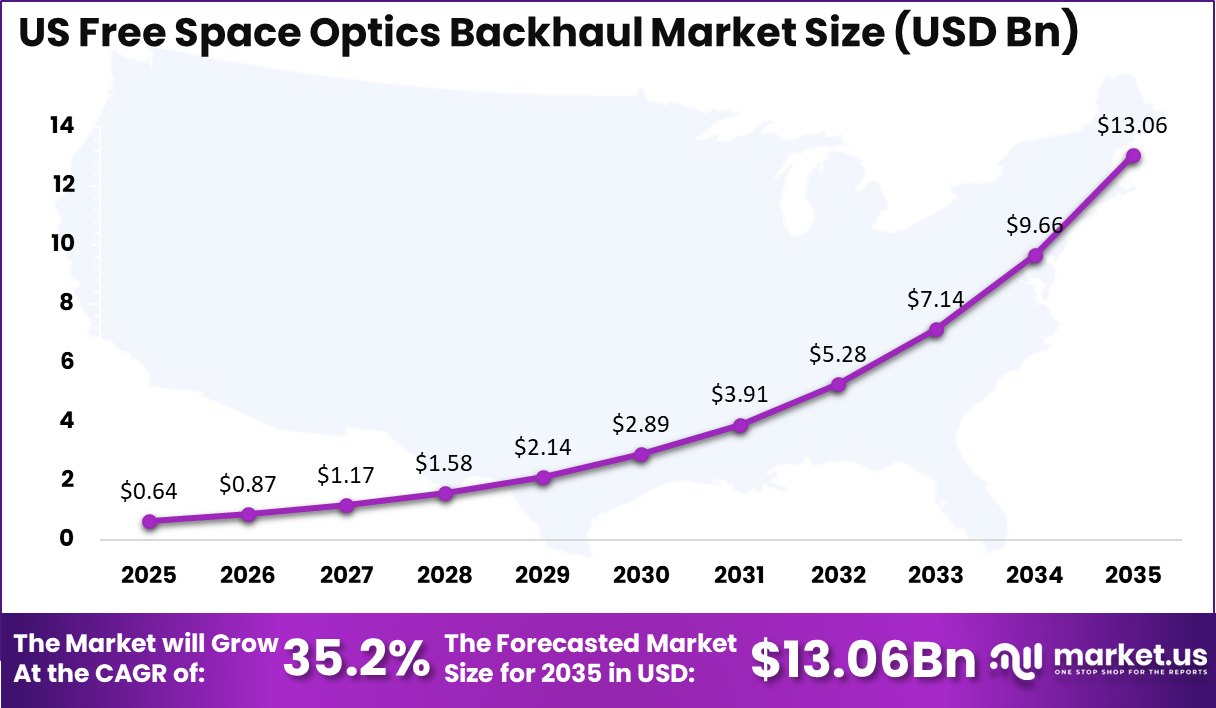

Within the region, the US market alone is valued at USD 0.64 billion in 2025 and is expected to reach USD 13.06 billion by 2035, growing at a CAGR of 35.2%. Overall, the data suggests that FSO backhaul solutions are becoming increasingly relevant for telecom operators and enterprises seeking scalable, high-speed, and cost-efficient alternatives to traditional fiber networks, particularly in areas where laying fiber is not feasible.

Free space optics backhaul adoption aligns closely with global data traffic and connectivity expansion trends. According to the International Telecommunication Union, over 5.4 billion people were using the internet by 2024, representing nearly 67% of the global population, which is increasing pressure on last-mile and backhaul networks. Mobile data traffic continues to surge, with Ericsson reporting global mobile data usage exceeding 130 exabytes per month in 2023, driven largely by video streaming and 5G services.

In urban environments, fiber deployment challenges remain significant. The Federal Communications Commission estimates that infrastructure deployment costs in dense areas can account for up to 70% of total network investment, encouraging alternatives such as wireless optical links.

Additionally, the GSMA highlights that over 60% of mobile operators are actively investing in non-fiber backhaul solutions to improve flexibility and reduce deployment timelines. These trends indicate a strong reliance on high-capacity wireless backhaul technologies like FSO to support increasing bandwidth demand, particularly in high-density cities and underserved regions.

Core Key Insights

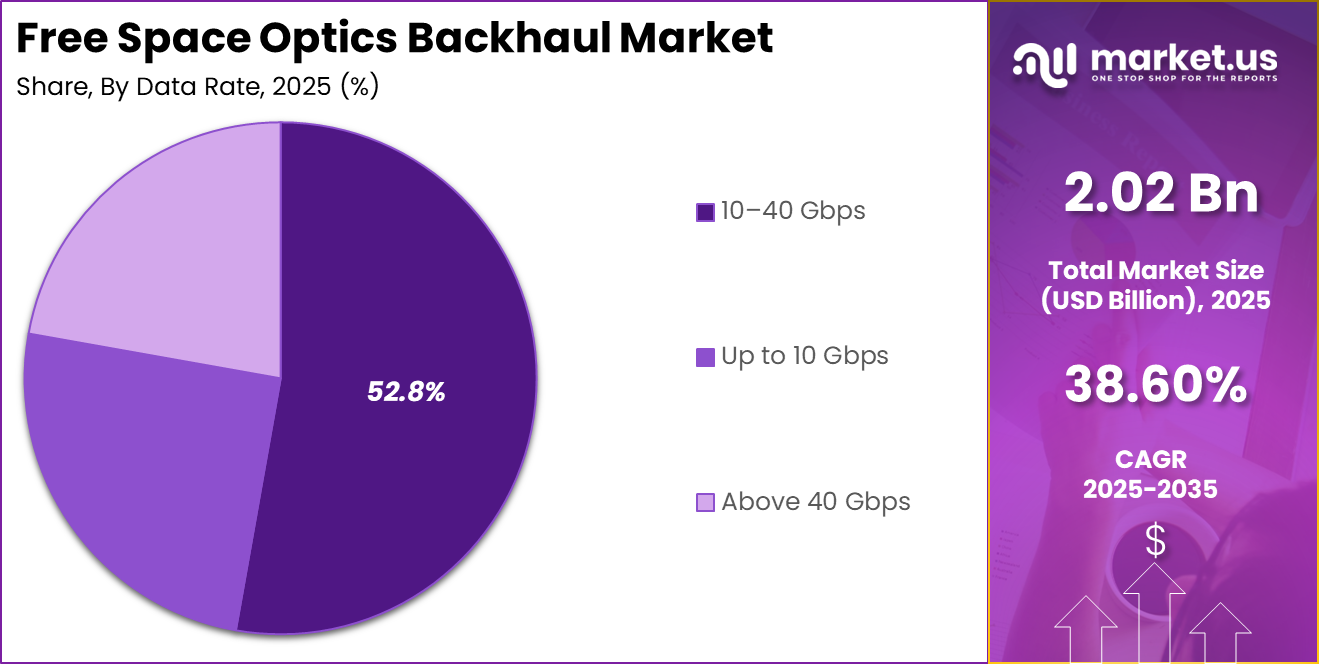

- The Free Space Optics Backhaul Market is valued at USD 2.02 billion in 2025 and is projected to reach USD 52.84 billion by 2035, reflecting a strong CAGR of 38.60%, indicating rapid adoption of high-speed wireless backhaul solutions.

- North America holds a leading position with 37.2% market share in 2025, accounting for USD 0.75 billion, supported by advanced telecom infrastructure and early 5G deployment strategies.

- The US market stands at USD 0.64 billion in 2025 and is expected to grow significantly to USD 13.06 billion by 2035, registering a CAGR of 35.2%, driven by rising data traffic and network densification.

- By component, transmitters dominate with 36.9% share, reflecting strong demand for efficient signal transmission technologies in optical wireless systems.

- By application, telecommunications leads with 40.4% share, highlighting the critical role of FSO in supporting high-capacity backhaul for mobile and broadband networks.

- By transmission range, medium range accounts for 55.7%, indicating its suitability for urban and metro network deployments.

- By data rate, the 10–40 Gbps segment leads with 52.8%, showing increasing preference for high-bandwidth communication to support growing digital consumption.

Network Analysis

The network analysis of the Free Space Optics (FSO) Backhaul Market shows a strong shift toward high-capacity, low-latency wireless infrastructure to support growing data demand. Telecom networks are becoming more dense with the expansion of small cells and 5G sites, which require efficient backhaul solutions. FSO technology fits well in this environment as it enables rapid deployment without the need for trenching or spectrum licensing.

In urban networks, FSO is increasingly used to bridge gaps between fiber nodes and base stations, especially where physical fiber installation is expensive or time-consuming. It supports point-to-point connectivity with high data throughput, making it suitable for enterprise campuses, smart city projects, and temporary network setups. The medium transmission range segment dominates because it balances performance and deployment flexibility in city environments.

From a performance perspective, FSO networks offer high bandwidth capacity, often comparable to fiber, but are influenced by environmental factors such as fog and heavy rain. To address this, hybrid network models combining FSO with RF links are being adopted to improve reliability. Overall, the network structure is evolving toward a mix of fiber, wireless, and optical solutions, where FSO plays a critical role in enhancing scalability and last-mile connectivity efficiency.

Future Predictions

The future outlook for the Free Space Optics Backhaul Market indicates strong expansion as telecom networks continue to evolve toward ultra-high-speed and low-latency communication. The growing rollout of 5G and the early development of 6G ecosystems are expected to increase the need for flexible and high-capacity backhaul solutions.

FSO technology is anticipated to play a key role in connecting dense small cell networks, especially in urban areas where fiber deployment remains complex and time-consuming. Advancements in optical communication technologies are projected to improve the reliability of FSO systems, particularly in challenging weather conditions.

Innovations such as adaptive optics, automatic beam alignment, and hybrid RF-FSO systems are expected to enhance performance and reduce signal disruption. These improvements are likely to expand the use of FSO beyond telecom into sectors such as defense, enterprise connectivity, and disaster recovery networks.

Additionally, the rising focus on smart cities and digital infrastructure development is expected to create new opportunities for FSO deployment. Governments and private players are anticipated to invest in scalable and cost-efficient connectivity solutions. As data consumption continues to grow globally, FSO backhaul is projected to become an essential component of next-generation network architectures.

Market Outlook

The Free Space Optics Backhaul Market outlook remains highly positive as demand for high-speed connectivity continues to rise across telecom and enterprise networks. The market is expected to witness sustained growth driven by increasing data consumption, expansion of 5G infrastructure, and the need for cost-efficient alternatives to fiber deployment.

FSO solutions are gaining attention due to their ability to deliver fiber-like speeds without the physical limitations of wired networks. From an industry perspective, telecom operators are expected to remain the primary adopters, using FSO to support network densification and improve last-mile connectivity.

Enterprises are also anticipated to increase adoption, particularly for campus networks, data center interconnects, and secure communication links. The medium transmission range segment is likely to remain dominant due to its suitability for urban deployments, where most connectivity gaps exist.

Regionally, developed markets are expected to maintain strong adoption due to advanced infrastructure, while emerging regions are projected to offer new growth opportunities as digital connectivity expands. Technological advancements aimed at improving reliability and performance are expected to further strengthen market confidence. Overall, the market outlook suggests that FSO backhaul will become a critical component in future network ecosystems, supporting scalable, high-capacity, and flexible communication networks.

Key Market Segments

The Free Space Optics Backhaul Market segmentation highlights clear dominance across key categories, reflecting strong alignment with current network infrastructure needs. By component, transmitters account for 36.9% share, as they play a critical role in converting electrical signals into optical signals for high-speed wireless transmission. Their demand is increasing with the expansion of data-intensive networks that require efficient and stable signal delivery.

By application, telecommunications leads with 40.4% share, driven by the rapid deployment of 5G networks and the need for reliable backhaul connectivity. Telecom operators are increasingly adopting FSO solutions to support network densification and to bridge connectivity gaps where fiber deployment is challenging.

In terms of transmission range, the medium range segment dominates with 55.7%, as it offers an optimal balance between performance and deployment flexibility. This range is widely used in urban and metro environments where distances are moderate and high data throughput is required.

By data rate, the 10–40 Gbps segment holds 52.8% share, indicating a strong preference for high-bandwidth communication systems. This segment supports growing data traffic demands from video streaming, cloud services, and enterprise applications, making it a key driver for market growth.

Research-Based Segments

By Component

- Transmitters

- Receivers

- Modulators

- Demodulators

- Others

By Application

- Telecommunications

- Military and Defense

- Healthcare

- Enterprise

- Others

By Transmission Range

- Short Range

- Medium Range

- Long Range

By Data Rate

- Up to 10 Gbps

- 10–40 Gbps

- Above 40 Gbps

By Component Analysis

36.9% share for transmitters highlights their leading role in the Free Space Optics Backhaul Market, as they form the core of optical signal generation and transmission. This dominance is driven by the increasing demand for high-capacity data transfer, where transmitters ensure efficient conversion of electrical signals into optical beams for wireless communication.

Their adoption is expected to rise further with expanding telecom infrastructure and the growing need for low-latency backhaul solutions. Transmitters are widely used in telecom and enterprise networks due to their ability to support high-speed data rates over line-of-sight communication.

Advancements in laser technologies and beam alignment systems are improving their performance, making them more reliable even in complex urban environments. Receivers play an equally important role by capturing optical signals and converting them back into electrical form, ensuring seamless data delivery.

Modulators and demodulators support signal processing by encoding and decoding data, which is essential for maintaining transmission accuracy and quality. The other segment includes supporting optical components that enhance system efficiency. Overall, the component landscape reflects a well-integrated system where transmitters remain central to performance and scalability.

By Application Analysis

40.4% share for telecommunications establishes it as the dominant application in the Free Space Optics Backhaul Market, supported by the rapid expansion of mobile networks and increasing demand for high-speed data connectivity. Telecom operators are actively deploying FSO solutions to support 4G and 5G backhaul, particularly in dense urban areas where fiber deployment is costly and time-consuming.

This segment is expected to maintain its lead as network densification and data traffic continue to rise. The military and defense segment is gaining importance due to the need for secure, line-of-sight communication systems that are difficult to intercept. FSO offers advantages such as low probability of detection and high data security, making it suitable for tactical communication and surveillance operations.

Healthcare applications are emerging steadily, where FSO is used for secure data transmission between hospitals and medical facilities, especially in scenarios requiring high bandwidth and low latency. Enterprise adoption is also increasing, driven by the need for reliable connectivity across campuses, data centers, and business locations.

The other segment includes niche applications such as disaster recovery and temporary network setups. Overall, telecommunications remains the primary driver due to its large-scale infrastructure requirements.

By Transmission Range Analysis

55.7% share for medium range highlights its dominance in the Free Space Optics Backhaul Market, as it offers an optimal balance between performance, cost, and deployment flexibility. This segment is widely adopted in urban and metro environments where communication distances typically range between a few hundred meters and several kilometers.

Medium-range solutions are expected to remain the preferred choice for telecom operators aiming to connect base stations and small cells efficiently without relying on extensive fiber infrastructure. Short-range systems are used in localized environments such as campus networks, enterprise buildings, and temporary setups where quick deployment and lower cost are key priorities.

These systems support high-speed communication over limited distances, making them suitable for indoor or closely spaced outdoor applications. Long-range transmission is gaining traction in specialized use cases such as rural connectivity, defense communication, and remote site linking.

However, its adoption remains relatively limited due to higher sensitivity to environmental conditions and the need for precise alignment over longer distances. Overall, the dominance of medium range reflects its strong applicability across mainstream telecom and enterprise deployments, where consistent performance and scalability are essential.

By Data Rate Analysis

52.8% share for the 10–40 Gbps segment establishes it as the leading data rate category in the Free Space Optics Backhaul Market, driven by the growing need for high-bandwidth communication across telecom and enterprise networks. This segment is widely adopted because it delivers a strong balance between performance and cost, making it suitable for 5G backhaul, metro connectivity, and data-intensive applications.

As digital consumption continues to rise, this range is expected to remain the preferred choice for scalable and efficient network deployment. The up to 10 Gbps segment is primarily used in smaller-scale deployments where bandwidth requirements are moderate, such as enterprise campuses and localized connectivity. It offers cost-effective solutions for businesses that do not require ultra-high data transfer speeds but still need reliable communication.

The above 40 Gbps segment is emerging as a high-performance category, particularly in advanced telecom infrastructure and data center interconnects. Its adoption is increasing with the growth of ultra-fast networks, although it requires higher investment and more precise system alignment. Overall, the dominance of the 10–40 Gbps segment reflects its strong alignment with current network capacity demands.

Regional Analysis

37.2% share held by North America highlights its leading position in the Free Space Optics Backhaul Market, with a regional value of USD 0.75 billion in 2025. This dominance is supported by strong telecom infrastructure, early adoption of advanced networking technologies, and continuous investments in high-speed connectivity solutions. The region is expected to maintain its leadership as demand for low-latency and high-capacity backhaul networks continues to grow.

The US plays a central role in regional growth, driven by rapid 5G deployment and increasing network densification across urban areas. Telecom operators are actively integrating FSO solutions to overcome challenges associated with fiber deployment, particularly in densely populated cities where installation costs and timelines remain high.

Canada is also contributing to market expansion through investments in digital infrastructure and efforts to improve connectivity in remote and underserved regions. The use of FSO technology in such areas is gaining traction due to its ability to deliver high-speed communication without extensive physical infrastructure.

Overall, North America’s strong technological base, high data consumption, and supportive regulatory environment are expected to drive continued adoption of FSO backhaul solutions across telecom, enterprise, and government applications.

US Market Size

The US Free Space Optics Backhaul Market is valued at USD 0.64 billion in 2025 and is projected to reach USD 13.06 billion by 2035, expanding at a CAGR of 35.2%. This strong growth reflects increasing demand for high-speed wireless backhaul solutions that can support rising data traffic and next-generation network infrastructure. The market is expected to benefit from continuous investments in advanced communication technologies and the expansion of digital services across industries.

The US telecom sector is a key driver, with rapid deployment of 5G networks and growing reliance on small cell architecture. FSO technology is increasingly adopted to provide high-capacity links between base stations, especially in urban areas where fiber installation is complex and costly. Enterprises are also contributing to market growth by adopting FSO for secure and high-speed connectivity across campuses and data centers.

In addition, government initiatives focused on improving broadband access and strengthening digital infrastructure are expected to support market expansion. The increasing use of cloud services, video streaming, and IoT applications is further driving demand for reliable backhaul solutions. Overall, the US market is projected to remain a major contributor to global growth, supported by strong technological advancement and infrastructure development.

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driving Factors

The Free Space Optics Backhaul Market is primarily driven by the rapid increase in global data traffic and the expansion of high-speed communication networks. Telecom operators are actively upgrading infrastructure to support 5G and dense network architectures, which require efficient backhaul solutions.

FSO technology is expected to gain traction due to its ability to deliver high bandwidth without the need for physical cables. Another key driver is the rising cost and complexity associated with fiber deployment, especially in urban environments. FSO provides a faster and more flexible alternative, enabling quick installation and scalability.

The growing adoption of cloud services, video streaming, and connected devices is also increasing the need for reliable data transmission. Additionally, enterprises are investing in secure and high-speed communication systems, further supporting market growth. These combined factors are projected to strengthen the adoption of FSO solutions across telecom and enterprise sectors.

Restraint Factors

Despite strong growth potential, the market faces certain limitations that may impact adoption. One of the key restraints is the sensitivity of FSO systems to environmental conditions such as fog, heavy rain, and dust, which can affect signal quality and reliability. This creates concerns for consistent performance, particularly in regions with challenging weather patterns.

Another constraint is the requirement for precise line-of-sight alignment between transmitter and receiver units, which can limit deployment flexibility in complex terrains or crowded urban settings. Initial setup costs for advanced FSO systems may also act as a barrier for small and medium enterprises.

In addition, limited awareness and technical expertise in some regions can slow down adoption. These challenges are expected to influence market growth, although ongoing technological improvements are anticipated to address some of these issues over time.

Growth Opportunities

The market presents significant opportunities driven by the increasing need for scalable and cost-efficient connectivity solutions. The expansion of 5G networks and future 6G development is expected to create strong demand for high-capacity backhaul systems, where FSO can play a critical role.

Emerging economies are projected to offer new growth avenues as they invest in digital infrastructure and seek alternatives to expensive fiber deployment. Smart city initiatives and the development of intelligent transportation systems are also expected to boost demand for FSO technology, as these applications require reliable and high-speed communication networks.

Additionally, hybrid solutions that combine FSO with radio frequency technologies are gaining attention, as they improve reliability and expand application scope. The growing use of FSO in defense, disaster recovery, and temporary network setups further enhances its potential. These factors are anticipated to open new revenue streams and accelerate market expansion.

Trending Factors

Several key trends are shaping the evolution of the Free Space Optics Backhaul Market. One notable trend is the integration of FSO with hybrid communication systems, combining optical and radio frequency technologies to ensure consistent performance under varying environmental conditions.

Another important trend is the advancement of adaptive optics and automatic alignment systems, which are improving the reliability and efficiency of FSO links. The increasing focus on smart cities and digital infrastructure is also driving the adoption of FSO solutions for urban connectivity.

Enterprises are showing growing interest in FSO for secure and high-speed data transfer across campuses and data centers. Additionally, there is a rising trend toward compact and energy-efficient FSO devices, which supports easier deployment and reduced operational costs. These trends are expected to enhance the overall value proposition of FSO technology and support its broader adoption across multiple industries.

Competitive Analysis

The competitive landscape of the Free Space Optics Backhaul Market is characterized by a mix of telecom equipment providers, optical communication specialists, and niche technology firms focusing on high-speed wireless solutions. The market remains moderately fragmented, with companies competing on performance, reliability, and deployment efficiency rather than pure pricing.

Technological capability, especially in maintaining stable links under environmental disturbances, plays a key differentiator. From a data perspective, the broader FSO communication market has shown strong momentum, with global valuations crossing USD 1.1 billion earlier and projected to exceed USD 16 billion within a decade, reflecting rapid technology adoption across telecom and enterprise sectors.

Earlier-stage adoption levels were relatively small, with the market below USD 200 million in 2020, indicating how quickly competition has intensified in recent years. Leading players are investing heavily in hybrid RF-FSO systems to address weather-related challenges, while also improving beam tracking and alignment technologies.

Strategic partnerships with telecom operators are common, as vendors aim to integrate FSO into 5G backhaul networks. Additionally, companies are focusing on compact, energy-efficient systems to meet enterprise demand. Overall, competition is expected to intensify as new entrants bring innovation and established firms expand their optical communication portfolios.

Top Key Players in the Market

- fSONA Networks

- LightPointe Communications

- CableFree (Wireless Excellence Limited)

- Plaintree Systems Inc.

- Mostcom Ltd.

- Wireless Excellence Ltd.

- Trimble Hungary Ltd.

- Laser Light Communications

- Anova Technologies

- AOptix Technologies Inc.

- Optelix

- HUBER+SUHNER AG

- IBSENtelecom Ltd.

- Sicoya GmbH

- Collinear Networks

- SkyFiber Inc.

- Redline Communications

- Aviat Networks

- BridgeWave Communications

- Cailabs

- Others

Recent Developments

- In 2024, global internet users exceeded 5.4 billion, highlighting the continued expansion of digital connectivity and creating significant demand for high-capacity backhaul solutions to support rising data traffic across networks.

- In 2023, global mobile data traffic crossed 130 exabytes per month, driven by video streaming and cloud-based services, increasing the need for efficient and scalable wireless backhaul technologies in dense network environments.

- In 2024, over 60% of mobile operators reported active investments in alternative backhaul technologies beyond fiber, reflecting a shift toward flexible and cost-efficient solutions to support rapid network deployment and expansion.

Report Scope

Report Features Description Market Value (2025) USD 2.02 Billion Forecast Revenue (2035) USD 52.84 Billion CAGR(2025-2035) 38.60% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends Segments Covered By Component (Transmitters, Receivers, Modulators, Demodulators, Others), By Application (Telecommunications, Military and Defense, Healthcare, Enterprise, Others), By Transmission Range (Short Range, Medium Range, Long Range), By Data Rate (Up to 10 Gbps, 10–40 Gbps, Above 40 Gbps) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape fSONA Networks, LightPointe Communications, CableFree (Wireless Excellence Limited), Plaintree Systems Inc., Mostcom Ltd., Wireless Excellence Ltd., Trimble Hungary Ltd., Laser Light Communications, Anova Technologies, AOptix Technologies Inc., Optelix, HUBER+SUHNER AG, IBSENtelecom Ltd., Sicoya GmbH, Collinear Networks, SkyFiber Inc., Redline Communications, Aviat Networks, BridgeWave Communications, Cailabs, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Free Space Optics Backhaul MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Free Space Optics Backhaul MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- fSONA Networks

- LightPointe Communications

- CableFree (Wireless Excellence Limited)

- Plaintree Systems Inc.

- Mostcom Ltd.

- Wireless Excellence Ltd.

- Trimble Hungary Ltd.

- Laser Light Communications

- Anova Technologies

- AOptix Technologies Inc.

- Optelix

- HUBER+SUHNER AG

- IBSENtelecom Ltd.

- Sicoya GmbH

- Collinear Networks

- SkyFiber Inc.

- Redline Communications

- Aviat Networks

- BridgeWave Communications

- Cailabs

- Others

Our Clients

- 182637

- Mar 2026