Global Foundry Service Market Size, Share, Growth Analysis By Material (Ferrous Metals, Non-Ferrous Metals), By Process (Sand Casting, Investment Casting, Die Casting, Permanent Mold Casting, Centrifugal Casting, Others), By End-Use (Automotive, Aerospace and Defense, Electrical and Electronics, Machinery and Equipment, Construction, Energy and Power, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: Jul 2025

- Report ID: 152811

- Number of Pages: 342

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

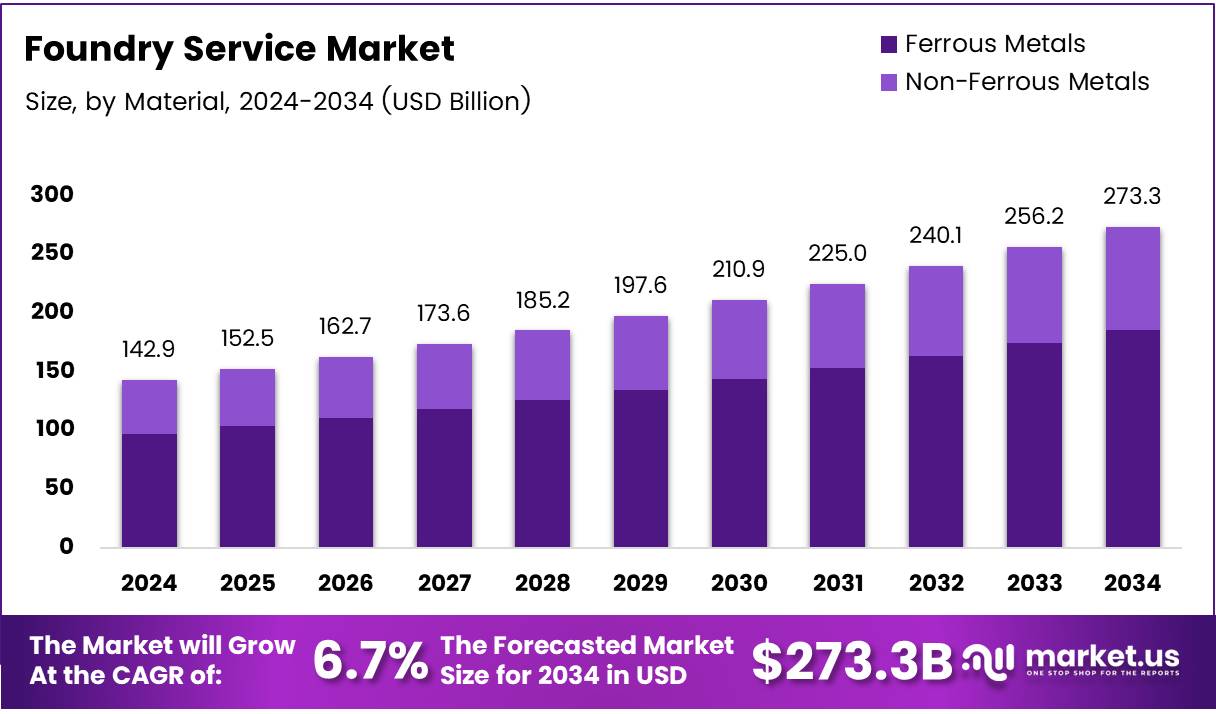

The Global Foundry Service Market size is expected to be worth around USD 273.3 Billion by 2034, from USD 142.9 Billion in 2024, growing at a CAGR of 6.7% during the forecast period from 2025 to 2034.

The foundry service market refers to the sector that provides casting and metal shaping services for various industries, including automotive, aerospace, and industrial equipment. It involves the creation of metal parts through molding and melting processes, offering significant support for manufacturing. These services are essential for producing high-precision components.

In recent years, the foundry service market has experienced notable growth, driven by increased demand from sectors like automotive and aerospace. This growth can be attributed to rising industrialization, along with advancements in technology that enable the production of complex metal parts. The market is expected to maintain a steady growth trajectory.

Opportunities abound for market players as the demand for sustainable and energy-efficient casting solutions rises. Many companies are focusing on developing innovative technologies, such as 3D printing and automated casting processes, to enhance product quality and reduce production time. These innovations are opening new revenue streams for industry participants.

Government investments and regulations have also played a pivotal role in shaping the foundry service market. Governments worldwide are prioritizing infrastructure and manufacturing industries, resulting in increased funding for foundries and related services. At the same time, regulations regarding environmental standards are pushing companies to adopt cleaner, more efficient casting techniques, further spurring innovation.

Moreover, regional developments in emerging markets such as Asia-Pacific and Latin America are presenting lucrative opportunities for market growth. These regions are seeing an uptick in demand for foundry services due to expanding industrial activities and urbanization. As a result, companies are increasingly focusing their efforts on these growing markets.

The rising trend of automation and digitalization within the foundry industry is transforming the market dynamics. Automation is not only improving operational efficiency but also reducing costs and human error. These technological advancements offer competitive advantages to firms that are quick to adapt, further enhancing market prospects.

Key Takeaways

- The Global Foundry Service Market is expected to reach USD 273.3 Billion by 2034, growing at a CAGR of 6.7% from 2025 to 2034.

- Ferrous Metals held a dominant market position with a 60.1% share in 2024.

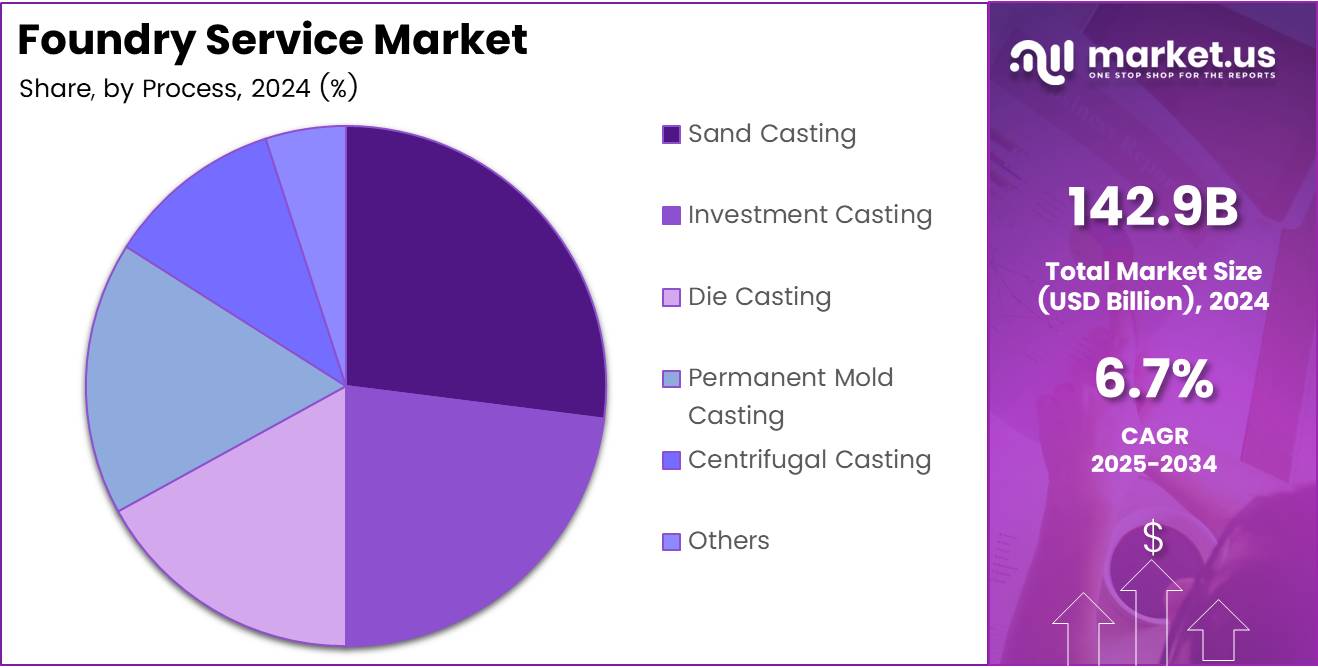

- Sand Casting held a dominant market position in the Foundry Service Market in 2024.

- The Automotive sector held a dominant position in the Foundry Service Market in 2024.

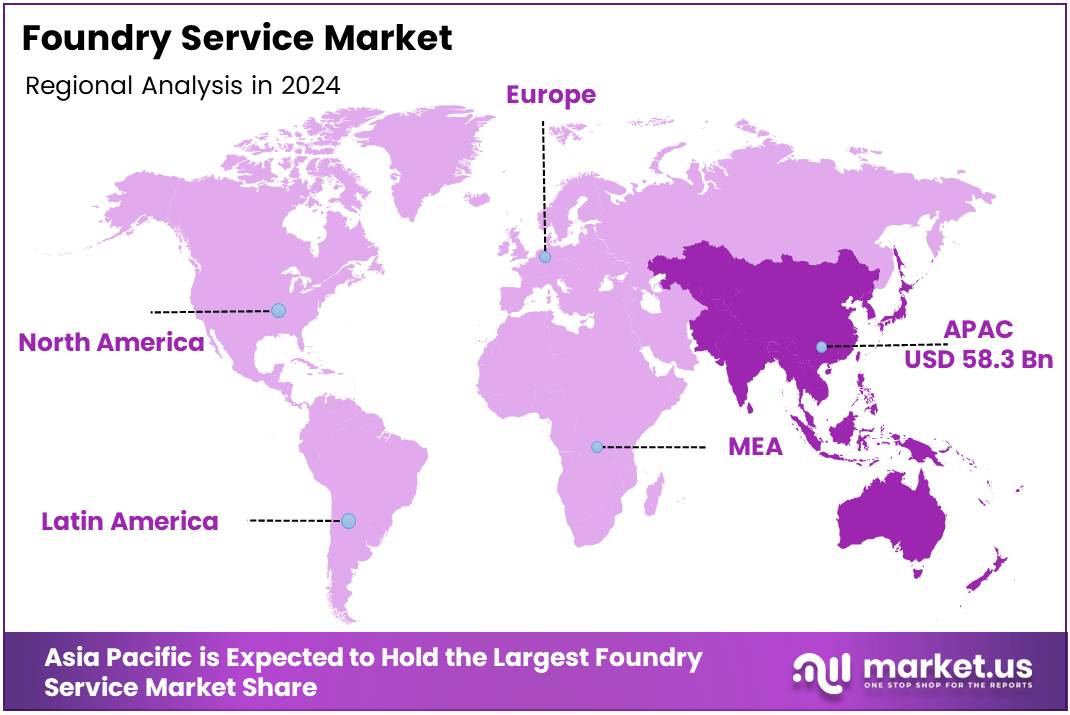

- Asia Pacific dominated the market with a 40.8% share, valued at USD 58.3 Billion in 2024.

Material Analysis

Ferrous Metals held a dominant market position with a 60.1% share in 2024.

Ferrous Metals segment is driven by the widespread use of ferrous metals in various industries due to their high strength, durability, and cost-effectiveness.

The demand for ferrous metals in the foundry service market is further supported by their essential role in automotive, construction, and machinery manufacturing. Ferrous materials are a preferred choice for creating complex parts and components, which explains their market dominance.

In contrast, non-ferrous metals hold a smaller portion of the market. These metals, including aluminum, copper, and zinc, are gaining traction for their lightweight properties and resistance to corrosion. However, they currently make up a significantly smaller share compared to ferrous metals, with demand increasing in applications requiring specialized performance.

Process Analysis

Sand Casting held a dominant market position in the Foundry Service Market in 2024.

Sand casting is a widely adopted process due to its versatility and low cost, making it ideal for producing a variety of metal parts across different industries. This process dominates the market as it can accommodate large, complex shapes and is suitable for both small and large-scale production.

Other casting methods such as investment casting, die casting, and centrifugal casting also contribute to the foundry service market, though none match the widespread use and cost-effectiveness of sand casting.

Investment casting, for instance, is known for its precision and ability to produce complex parts, but it holds a smaller share due to its higher cost. Despite this, its demand is growing in sectors requiring high-precision components.

End-Use Analysis

Automotive held a dominant market position in 2024 within the Foundry Service Market.

The automotive sector’s reliance on foundry services is driven by the increasing demand for high-quality, durable components used in vehicle manufacturing. These components require materials like ferrous metals, which are produced using casting processes such as sand casting and die casting. The automotive industry’s need for efficiency and performance ensures its dominance in the foundry services market.

Other sectors, such as aerospace and defense, electrical and electronics, and machinery and equipment, also contribute to the foundry service market. However, these industries tend to have a smaller share due to their more specialized requirements and the use of more expensive materials and processes.

The construction and energy sectors, while important, also hold smaller market shares compared to automotive, with their demand for foundry services driven by specific, large-scale projects.

Key Market Segments

By Material

- Ferrous Metals

- Non-Ferrous Metals

By Process

- Sand Casting

- Investment Casting

- Die Casting

- Permanent Mold Casting

- Centrifugal Casting

- Others

By End-Use

- Automotive

- Aerospace and Defense

- Electrical and Electronics

- Machinery and Equipment

- Construction

- Energy and Power

- Others

Drivers

Increasing Demand for Custom Metal Castings Drives Market Growth

The increasing demand for custom metal castings is a significant driver in the foundry service market. Industries require precision and tailored solutions, particularly in aerospace, automotive, and machinery sectors. Custom castings help meet the unique needs of these industries, enhancing product performance and quality.

Advancements in automation and technology in foundries have streamlined production processes. Automation reduces human error, increases productivity, and lowers labor costs, allowing foundries to meet higher demand more efficiently. These innovations ensure greater consistency and precision in casting.

The automotive and aerospace industries are major contributors to market growth. The constant need for advanced components in vehicles, machinery, and aircraft fuels demand for foundry services. New technologies in these industries also require customized metal solutions, providing opportunities for foundries to expand and innovate.

Sustainability and environmental compliance are now more important than ever. Foundries are focusing on reducing emissions and adopting eco-friendly practices. This shift ensures compliance with regulations, which in turn attracts environmentally conscious clients, providing a competitive edge in the market.

Restraints

Lack of Skilled Labor in the Foundry Sector Constraints Market Growth

A significant restraint in the foundry service market is the shortage of skilled labor. The technical nature of foundry operations requires experienced workers, but the industry is facing challenges in attracting and retaining qualified personnel. This labor gap hampers efficiency and increases operational costs.

Stringent environmental regulations are another constraint. As foundries face increasing pressure to comply with environmental standards, the cost of maintaining eco-friendly practices rises. These regulations, while necessary, create additional financial burdens for businesses that must invest in technology and processes to remain compliant.

Volatility in raw material prices also poses a challenge. The prices of metals and other materials fluctuate, affecting the overall cost structure for foundries. Such unpredictability can lead to price increases for customers and affect profit margins, making it harder for businesses to remain competitive.

Growth Factors

Expansion of 3D Printing and High-Performance Alloys Drives Foundry Service Market Growth

The rise of 3D printing in metal casting presents exciting growth opportunities. Foundries are incorporating 3D printing to create complex, customized components more efficiently. This technology enables precise metal casting, allowing industries to innovate and meet specific demands, thereby expanding the scope of foundry services.

High-performance alloys are in increasing demand due to their application in industries such as aerospace and automotive. These materials offer better strength, durability, and heat resistance, which is essential for specialized parts. Foundries are adapting by refining their processes to meet the growing need for these advanced alloys.

Smart foundries represent another area of growth. As automation and IoT technologies become more prevalent, investments in smart foundries are expected to rise. These advancements improve production efficiency, reduce downtime, and optimize resource use, providing long-term growth potential for the sector.

The integration of Artificial Intelligence (AI) and the Internet of Things (IoT) into foundry operations also offers significant opportunities. These technologies optimize processes, improve quality control, and enable predictive maintenance, allowing foundries to enhance their operations and reduce operational costs.

Emerging Trends

AI Integration and Green Practices Drive Foundry Service Market Trends

AI is increasingly being integrated into foundry operations for predictive maintenance. This technology helps identify potential equipment failures before they occur, minimizing downtime and optimizing machine performance. This trend is critical for maintaining productivity and reducing costs in the foundry industry.

Additive manufacturing, also known as 3D printing, is being adopted widely in foundries. This technology allows for the creation of complex geometries that are difficult to achieve with traditional methods. The use of additive manufacturing in metal casting improves production efficiency and offers more design flexibility for customers.

The shift toward green and eco-friendly foundry practices is gaining momentum. Foundries are adopting sustainable methods such as reducing emissions, using recycled materials, and minimizing waste. These practices not only help companies comply with environmental regulations but also appeal to environmentally conscious consumers.

Digital twins are becoming more common in foundry operations. This technology allows foundries to create digital replicas of their physical systems, providing valuable insights into performance. It helps optimize processes, reduce waste, and enhance overall efficiency, which is crucial for staying competitive in the evolving market.

Regional Analysis

Asia Pacific Dominates the Foundry Service Market with a Market Share of 40.8%, Valued at USD 58.3 Billion

In 2024, Asia Pacific held a dominant market share of 40.8%, valued at USD 58.3 billion, driven by robust industrial growth and increasing demand for automotive and aerospace components. The region’s growing manufacturing sector and advancements in foundry automation are expected to propel its market dominance further. The high demand for customized metal castings and the expansion of end-user industries like automotive and construction are expected to continue fueling growth in the coming years.

North America Foundry Service Market Trends

North America is a significant player in the foundry service market, driven by high demand from the automotive, aerospace, and energy industries. The region’s advanced manufacturing technologies and well-established supply chains contribute to its strong market presence. The rise of sustainability initiatives and the adoption of environmentally compliant processes are expected to support future growth, enhancing market potential.

Europe Foundry Service Market Insights

Europe has a strong foothold in the foundry service market, particularly due to its well-established automotive and machinery industries. The region is seeing a shift toward more sustainable and energy-efficient foundry processes. The push for innovation and advanced automation technologies in manufacturing is expected to drive the market forward, with notable demand from countries like Germany, Italy, and France.

Middle East and Africa Foundry Service Market Outlook

The Middle East and Africa (MEA) market is poised for growth, driven by expanding infrastructure projects and an increasing demand for energy and power-related components. The region is expected to see higher demand for ferrous and non-ferrous metals, especially in construction and energy sectors. Investments in automation and technology to enhance foundry processes are also likely to play a critical role in boosting market growth in MEA.

Latin America Foundry Service Market Trends

Latin America has been witnessing gradual growth in the foundry service market, with significant contributions from the automotive and machinery industries. The region’s increasing focus on industrialization and infrastructure development is anticipated to drive future demand. However, challenges like raw material price volatility and skilled labor shortages could hinder rapid market growth. The shift toward more sustainable practices is also expected to play a role in shaping the market dynamics in Latin America.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Foundry Service Company Insights

In 2024, Nemak continues to dominate the global foundry service market with a strong reputation for manufacturing high-quality aluminum castings. The company’s emphasis on innovation and technological advancements in its production processes positions it as a key player, particularly in the automotive industry.

Waupaca Foundry, Inc. is recognized for its expertise in producing iron castings. The company’s focus on operational efficiency and customer-driven solutions has made it a preferred supplier in various industries, including automotive, agriculture, and industrial equipment, contributing to its prominent market presence.

Hitachi Metals, Ltd. remains a significant player in the foundry service market, specializing in the production of high-performance castings for applications in energy, automotive, and industrial sectors. The company’s commitment to research and development enables it to deliver cutting-edge solutions, enhancing its competitive edge globally.

Bharat Forge Limited is well-positioned in the market with its diverse offerings of forged and cast components. The company leverages advanced manufacturing techniques and robust supply chains, playing a key role in sectors such as automotive, aerospace, and industrial machinery, further strengthening its market position.

Top Key Players in the Market

- Nemak

- Waupaca Foundry, Inc.

- Hitachi Metals, Ltd.

- Bharat Forge Limited

- Alcoa Corporation

- Thyssenkrupp AG

- General Motors Company

- Castings PLC

- Metal Technologies, Inc.

- AAM Casting

- Grede Holdings LLC

- CIE Automotive

- Precision Castparts Corp.

- Reliance Foundry Co. Ltd.

Recent Developments

- In April 2024, Magnus Metal secured US$74 million in Series B funding to advance its innovative Digital Casting™ technology, aimed at revolutionizing the metal part casting industry through enhanced precision and efficiency.

- In October 2024, AMPCO METAL acquired Schmelzmetall Group, strengthening its position in the market for copper alloy solutions and expanding its capabilities in high-performance casting products.

Report Scope

Report Features Description Market Value (2024) USD 142.9 Billion Forecast Revenue (2034) USD 273.3 Billion CAGR (2025-2034) 6.7% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Material (Ferrous Metals, Non-Ferrous Metals), By Process (Sand Casting, Investment Casting, Die Casting, Permanent Mold Casting, Centrifugal Casting, Others), By End-Use (Automotive, Aerospace and Defense, Electrical and Electronics, Machinery and Equipment, Construction, Energy and Power, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Nemak, Waupaca Foundry, Inc., Hitachi Metals, Ltd., Bharat Forge Limited, Alcoa Corporation, Thyssenkrupp AG, General Motors Company, Castings PLC, Metal Technologies, Inc., AAM Casting, Grede Holdings LLC, CIE Automotive, Precision Castparts Corp., Reliance Foundry Co. Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Nemak

- Waupaca Foundry, Inc.

- Hitachi Metals, Ltd.

- Bharat Forge Limited

- Alcoa Corporation

- Thyssenkrupp AG

- General Motors Company

- Castings PLC

- Metal Technologies, Inc.

- AAM Casting

- Grede Holdings LLC

- CIE Automotive

- Precision Castparts Corp.

- Reliance Foundry Co. Ltd.

Our Clients

- 152811

- Jul 2025