Global Force Sensor Market Size, Share, Growth Analysis By Measurement Type (Both, Tension Force, Compression Force), By Sensing Technology (Strain Gauge, Load Cell, Force Sensitive Resistors, Others), By Operation (Digital, Analog), By End Use Industry (Automotive, Locomotive, Manufacturing, Mining, Aerospace and Defense, Construction, Healthcare, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181442

- Number of Pages: 215

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

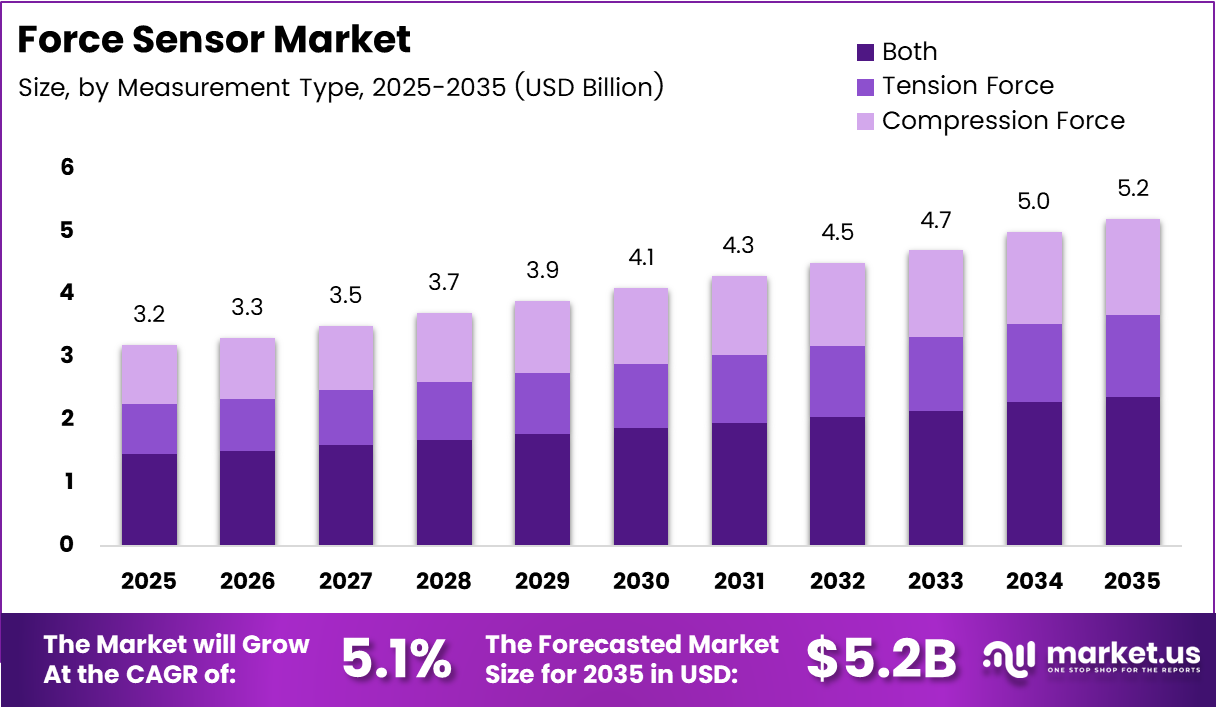

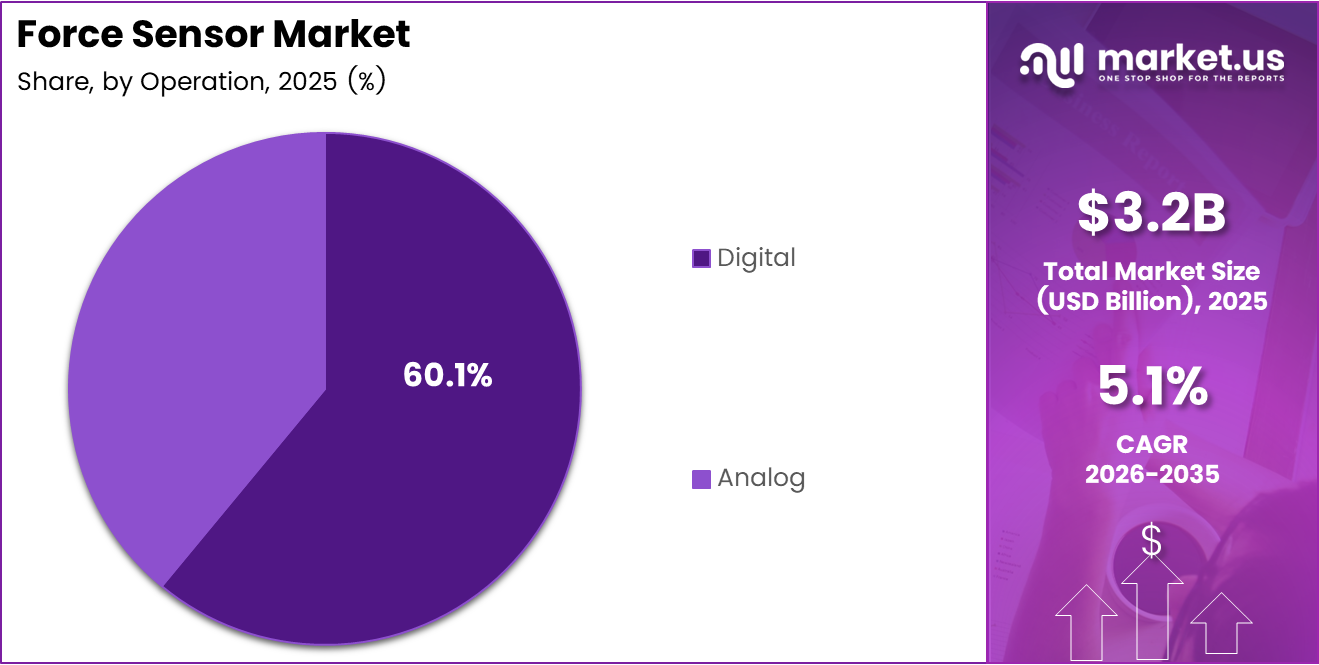

Global Force Sensor Market size is expected to be worth around USD 5.2 Billion by 2035 from USD 3.2 Billion in 2025, growing at a CAGR of 5.1% during the forecast period 2026 to 2035.

The force sensor market covers devices that measure tension, compression, and multi-axis mechanical loads across industrial, medical, and consumer applications. These sensors convert applied force into measurable electrical signals. Their adoption spans precision manufacturing lines, surgical robotics, automotive crash testing, and wearable health devices.

Digital operation formats now capture 60.1% of the market, reflecting a structural shift toward data-integrated production environments. Buyers no longer purchase standalone sensors — they procure measurement nodes that feed directly into analytics platforms. This shift raises switching costs and creates long-term vendor lock-in opportunities for early market leaders.

Automotive end-users hold 25.2% share, the largest of any vertical, driven by mandatory safety testing protocols and the rollout of advanced driver assistance systems. As electrification and autonomy reshape vehicle architecture, force measurement requirements per vehicle are increasing — not shrinking. This signals sustained volume demand from OEMs and Tier-1 suppliers through the forecast period.

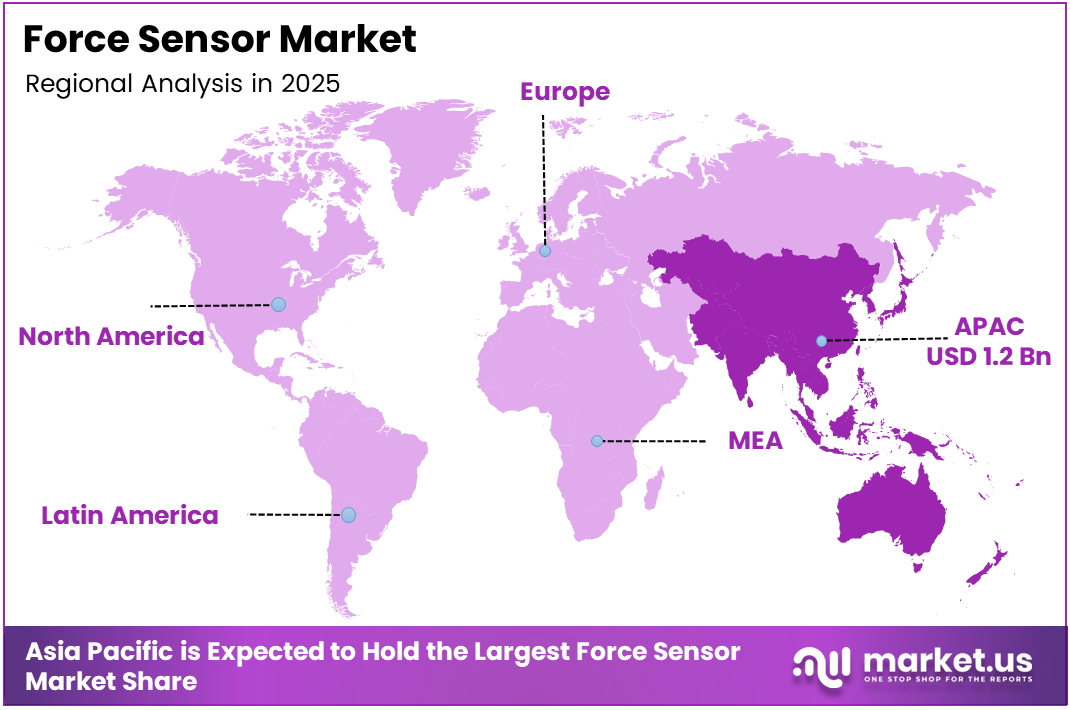

Asia Pacific leads with 40.1% share, valued at USD 1.2 Billion. The region’s dominance reflects the concentration of electronics manufacturing and collaborative robotics deployment in China, Japan, and South Korea. Investment in smart factory infrastructure across these markets continues to generate consistent sensor procurement cycles.

Strain gauge technology holds 35.4% of the sensing technology segment, confirming its position as the default choice for industrial buyers who prioritize proven accuracy over emerging alternatives. However, load cell and MEMS-based formats are closing the gap as miniaturization requirements from medical and electronics sectors intensify.

According to SRI Sensor, the M38XX series low-capacity high-accuracy 6-axis force/torque sensors achieve accuracy within 0.2% of full scale. This level of precision matters because it enables force sensors to replace legacy mechanical testing systems in aerospace and medical device validation — a market migration that carries significantly higher average selling prices.

According to a study published in Science Direct, the graphene MEMS force sensor achieves a resolution of 0.1 pN with maximum force sensitivity of 0.156 pN. At this sensitivity level, sensors can detect forces at the cellular scale — opening demand in next-generation biomedical diagnostics and nano-manufacturing quality control, markets that current sensor formats cannot address.

Key Takeaways

- The global force sensor market is valued at USD 3.2 Billion in 2025 and is forecast to reach USD 5.2 Billion by 2035, at a CAGR of 5.1%.

- By Measurement Type, the Both (Tension and Compression) segment dominates with a 45.6% share.

- By Sensing Technology, Strain Gauge leads with 35.4% share, followed by Load Cell, Force Sensitive Resistors, and Others.

- By Operation, Digital holds the dominant position with 60.1% share.

- By End Use Industry, Automotive leads with 25.2%, followed by Locomotive, Manufacturing, Mining, Aerospace and Defense, Construction, Healthcare, and Others.

- Asia Pacific dominates the regional landscape with 40.1% share, valued at USD 1.2 Billion.

Measurement Type Analysis

Both (Tension and Compression) dominates with 45.6% due to versatility across multi-application industrial environments.

In 2025, Both (Tension and Compression) held a dominant market position in the By Measurement Type segment of the Force Sensor Market, with a 45.6% share. Buyers across manufacturing, robotics, and aerospace prefer dual-mode sensors because they eliminate the need for separate instruments. This consolidation reduces procurement cost and simplifies system integration, making combined-mode devices the default specification in industrial purchasing decisions.

Tension Force sensors serve applications where pull or stretch loads must be isolated from compressive interference. Cable tension monitoring, material tensile testing, and structural wire load measurement drive this segment. Buyers in civil infrastructure and marine engineering specifically require pure tension measurement to avoid signal contamination from vibration or compressive side-loads during long-duration monitoring cycles.

Compression Force sensors address applications requiring downward or inward force measurement in confined spaces. Press-fit assembly lines, injection molding presses, and bearing load monitoring are primary use cases. The segment appeals to manufacturers where direct contact with a surface under load is the only viable measurement geometry, making compression-specific designs essential rather than optional.

Sensing Technology Analysis

Strain Gauge dominates with 35.4% due to proven accuracy and established industrial supply chains.

In 2025, Strain Gauge held a dominant market position in the By Sensing Technology segment of the Force Sensor Market, with a 35.4% share. Procurement teams in heavy industry and automotive testing default to strain gauge technology because its long performance history reduces qualification risk. Additionally, the global supplier base for strain gauge components is mature, keeping lead times short and prices competitive relative to newer sensor formats.

Load Cell technology serves as the primary force measurement format in legal-for-trade weighing, process control, and materials testing. Its dominance in regulated industries stems from traceable calibration standards accepted by metrology authorities worldwide. Buyers in food processing, pharmaceutical batch control, and logistics rely on load cells because compliance certification requirements effectively limit substitution by alternative technologies.

Force Sensitive Resistors offer a cost-effective solution for low-force detection in consumer electronics, wearables, and human-machine interface devices. Their thin-film form factor enables integration into keyboards, touchscreens, and pressure-sensitive surfaces where spatial constraints prevent conventional sensor installation. However, FSR accuracy limitations restrict their use to applications where relative force detection matters more than calibrated absolute measurement.

Others in this segment include piezoelectric, capacitive, and MEMS-based technologies. These formats are gaining share in high-frequency dynamic force measurement applications such as impact testing, vibration analysis, and nano-scale biomedical sensing. While their combined share remains smaller today, MEMS formats in particular are positioned to capture significant volume as miniaturization demands from next-generation electronics intensify through the forecast period.

Operation Analysis

Digital dominates with 60.1% due to direct compatibility with automated data acquisition systems.

In 2025, Digital held a dominant market position in the By Operation segment of the Force Sensor Market, with a 60.1% share. Factory automation systems and Industry 4.0 architectures require sensor outputs that integrate directly with PLCs, IoT gateways, and cloud analytics platforms. Digital sensors eliminate analog-to-digital conversion errors and support standardized communication protocols, making them the natural choice for engineers designing connected measurement infrastructure.

Analog operation retains relevance in applications where simplicity, low latency, and minimal processing overhead are priorities. High-speed dynamic testing, basic load monitoring in legacy equipment, and cost-constrained embedded systems continue to specify analog sensors. Consequently, analog formats remain commercially viable in price-sensitive markets and retrofit scenarios where digital infrastructure upgrades are not justified by the application requirements.

End Use Industry Analysis

Automotive dominates with 25.2% due to mandatory safety testing and ADAS integration requirements.

In 2025, Automotive held a dominant market position in the By End Use Industry segment of the Force Sensor Market, with a 25.2% share. Crash safety standards and ADAS validation protocols require force sensors at multiple points in vehicle design and manufacturing. As electric vehicle platforms introduce new powertrain architectures and battery structural requirements, force measurement specifications per vehicle are expanding — sustaining automotive as the highest-volume end-user through the forecast period.

Locomotive applications rely on force sensors for wheel-rail interaction measurement, braking force monitoring, and track load analysis. Rail operators and rolling stock manufacturers use force data to extend maintenance intervals and detect structural fatigue before failure occurs. Regulatory requirements for safety-critical load monitoring on passenger rail systems create a stable baseline demand that is largely immune to economic cycles.

Manufacturing integrates force sensors into assembly line robots, press monitoring systems, and quality control torque verification. Collaborative robot deployments in electronics and precision parts assembly are among the fastest-growing use cases within this vertical. As manufacturers add more sensor nodes per production line to satisfy traceability and zero-defect mandates, manufacturing’s share of total force sensor procurement is increasing.

Mining deploys force sensors in hoist rope tension monitoring, conveyor belt load measurement, and underground structural support systems. Harsh operating environments — dust, moisture, extreme temperature — create strong demand for ruggedized sensor designs. Mining operators prioritize sensors with overload tolerance and extended calibration intervals to minimize maintenance downtime in locations where sensor access is operationally costly.

Aerospace and Defense applications include structural load monitoring on aircraft frames, landing gear force measurement, and thrust vector testing for propulsion systems. Aerospace buyers apply the most rigorous qualification standards of any vertical, requiring sensors with documented traceability, environmental testing certifications, and long-term availability commitments from suppliers. These requirements limit supplier participation but protect incumbent vendors from competitive displacement.

Construction uses force sensors in pile load testing, structural health monitoring of bridges and high-rise buildings, and crane load management systems. Post-tensioned concrete structures require embedded force sensors to monitor cable tension over the operational life of the structure — a use case that generates recurring calibration and replacement revenue for sensor suppliers beyond initial installation.

Healthcare applies force sensors in surgical robotics for tactile feedback, rehabilitation equipment for resistance measurement, and prosthetic limb control systems. The miniaturization demands of minimally invasive surgical tools and the sensitivity requirements of prosthetics are driving procurement toward high-accuracy MEMS-based and multi-axis force sensor formats. Bota Systems, for example, launched the SensONE T5 in March 2024 specifically targeting collaborative robots used in precision medical and research applications, illustrating the growing overlap between robotics and healthcare sensor requirements.

Others include consumer electronics, agricultural equipment, and research instrumentation. Consumer electronics represents the highest-volume but lowest-average-price application within this grouping, with force sensing integrated into touchscreen pressure detection and wearable biometric monitoring. Agricultural equipment is an emerging use case where force sensors on planting equipment and harvesting machinery enable precision yield optimization by measuring soil resistance and crop load in real time.

Key Market Segments

By Measurement Type

- Both (Tension and Compression)

- Tension Force

- Compression Force

By Sensing Technology

- Strain Gauge

- Load Cell

- Force Sensitive Resistors

- Others

By Operation

- Digital

- Analog

By End Use Industry

- Automotive

- Locomotive

- Manufacturing

- Mining

- Aerospace and Defense

- Construction

- Healthcare

- Others

Drivers

Industrial Automation, Robotics, and Safety System Mandates Accelerate Force Sensor Procurement Across Verticals

Collaborative robots on precision assembly lines require force feedback to distinguish safe contact from dangerous collision. This technical necessity — not optional enhancement — makes force sensors a mandatory component in every cobot deployment. As manufacturing facilities add robotic workcells to meet output targets, sensor procurement volumes scale directly with robot unit installations.

Automotive safety regulations require force measurement at multiple stages of vehicle design validation, crash testing, and ADAS component verification. Each new vehicle platform qualification cycle generates a defined sensor procurement requirement that suppliers can plan against. According to Electronics Weekly, the MCS10-002-6C six-axis force sensor achieves an accuracy class up to 0.1, meeting the precision threshold required for ADAS and safety-critical automotive test environments — a specification that narrows the qualified supplier pool and strengthens pricing power for compliant vendors.

Additionally, Bota Systems introduced the SensONE T80 in October 2024, a force-torque sensor optimized for larger collaborative robots with ISO-standard flanges. This product directly targets the heavy-payload automation segment where sensor specifications are driven by safety certification requirements rather than cost alone. Consequently, regulatory and safety mandates across automotive, robotics, and industrial automation are compressing the choice-set for procurement teams toward higher-specification sensors.

Restraints

High Manufacturing Costs and Environmental Performance Limitations Constrain Force Sensor Penetration in Price-Sensitive and Harsh-Condition Markets

Force sensor manufacturing requires precision material processing, multi-step calibration, and controlled environmental assembly — cost structures that translate directly into unit prices that price-sensitive buyers in construction, agriculture, and light manufacturing find difficult to justify. The result is a bifurcated market where high-specification sensors sell into premium applications while lower-cost alternatives with inferior accuracy fill the volume tier.

Complex calibration requirements add operational cost beyond the purchase price. Industrial users must factor in periodic recalibration cycles, certified calibration equipment, and trained technicians — total cost of ownership calculations that often delay or prevent adoption in small and mid-sized manufacturing operations. This friction particularly slows penetration in emerging market manufacturing hubs where metrology infrastructure is less developed.

Performance degradation in extreme environments — high temperatures, humidity, vibration, and corrosive atmospheres — limits force sensor deployment in mining, offshore oil and gas, and heavy industrial applications. Sensors operating outside their rated environmental range produce drift errors that undermine the accuracy justification for purchasing them. Until ruggedized sensor designs achieve cost parity with standard-grade devices, harsh-environment markets will remain underpenetrated relative to their potential procurement volumes.

Growth Factors

Smart Factory Deployment, Medical Device Innovation, and MEMS Miniaturization Open New Revenue Streams for Force Sensor Suppliers

Industry 4.0 factories require continuous force monitoring at every critical assembly and transfer point to enable predictive maintenance and zero-defect quality systems. Each production line retrofit for smart factory compliance adds multiple sensor nodes where none previously existed. This greenfield installation opportunity — concentrated in Asia Pacific and Western Europe — represents incremental revenue beyond the replacement cycle that currently dominates procurement volumes.

Prosthetics and rehabilitation devices are incorporating multi-axis force sensing to enable natural limb movement feedback and adaptive resistance control. Interface Inc. released the ICPW Wireless Stainless Steel Compression Load Cell in May 2024, a product designed for portable force measurement scenarios that includes medical rehabilitation and wearable monitoring among its target applications. According to Science Direct, the mechanoluminescence-based impact force sensor achieves a measurement error below 2.5% over its calibrated range at an approximate manufacturing cost of RMB 3,000 — a cost point that makes portable medical force sensing commercially viable in clinical and home rehabilitation settings for the first time.

MEMS-based force sensors enable integration into devices where conventional sensors are physically impossible to install — surgical instrument handles, implantable monitoring devices, and compact consumer wearables. Aerospace structural load monitoring also represents an underserved segment where lightweight embedded MEMS sensors can replace heavier conventional instrumentation without sacrificing measurement accuracy. These applications collectively point toward a market expansion that is supply-constrained rather than demand-constrained.

Emerging Trends

MEMS Miniaturization and AI-IoT Integration Redefine Force Sensor Functionality from Measurement Instrument to Intelligent Node

MEMS-based force sensor development is shifting from laboratory prototypes toward commercial deployment in portable electronics, embedded robotics, and biomedical devices. According to SRI Sensor, the M37XX and M47XX series 6-axis force/torque sensors achieve non-linearity and hysteresis of 0.5% — a performance level now being targeted in next-generation MEMS formats at significantly smaller physical dimensions. Achieving this accuracy in miniaturized form factors will unlock sensor deployment in devices where size and weight constraints previously excluded force measurement entirely.

Integration of force sensors with AI analytics platforms transforms their role from passive data collectors to active process optimization inputs. Real-time force data fed into machine learning models enables predictive maintenance alerts, automatic assembly line adjustments, and robotic path correction without human intervention. This capability shift means buyers are no longer just purchasing measurement accuracy — they are purchasing decision-making infrastructure, which fundamentally raises the value proposition and justifies higher per-unit spending.

Multi-axis force sensors and flexible printed force sensor formats are converging on the same end market: advanced robotics and smart surface interfaces. Flexible sensors on electronic skin and smart surfaces can detect spatial force distribution across large areas, enabling applications in social robotics, interactive displays, and structural health monitoring of curved surfaces. These formats represent a structural departure from single-point measurement paradigms and signal where next-generation sensor design investment is concentrating.

Regional Analysis

Asia Pacific Dominates the Force Sensor Market with a Market Share of 40.1%, Valued at USD 1.2 Billion

Asia Pacific holds 40.1% of the global force sensor market, valued at USD 1.2 Billion. This position reflects the region’s concentration of electronics manufacturing, automotive production, and collaborative robot deployments, particularly in China, Japan, and South Korea. Government-backed smart factory programs in these countries sustain consistent procurement volumes that other regions cannot match on scale.

North America Force Sensor Market Trends

North America commands a substantial share driven by mature aerospace and defense procurement infrastructure, established automotive safety testing mandates, and a high density of collaborative robot installations in advanced manufacturing facilities. The region’s regulatory environment for medical device force sensing — particularly in surgical robotics — creates a premium market segment where accuracy and certification requirements favor established sensor suppliers with documented compliance histories.

Europe Force Sensor Market Trends

Europe’s force sensor demand concentrates in Germany, France, and the UK, where precision engineering industries, automotive OEMs, and industrial automation integrators operate at global scale. EU machinery safety directives and CE certification requirements for automated equipment mandate force sensing at key interaction points between humans and machines. This regulatory framework creates a non-discretionary procurement baseline that sustains demand independent of broader industrial investment cycles.

Latin America Force Sensor Market Trends

Latin America’s force sensor market is driven primarily by Brazil and Mexico, where automotive assembly plants and mining operations generate the most consistent demand. Both countries host Tier-1 automotive supplier facilities that follow global OEM sensor specification standards, creating a procurement pipeline connected to international design cycles rather than domestic market conditions alone. Infrastructure gaps in calibration and technical support continue to limit adoption in smaller industrial operations.

Middle East and Africa Force Sensor Market Trends

The Middle East and Africa market draws primary demand from oil and gas structural monitoring, construction load testing, and mining operations across South Africa and GCC countries. Harsh operating environments in these sectors require ruggedized sensor designs with extended environmental tolerances. Investment in infrastructure megaprojects across Saudi Arabia and the UAE is generating new structural health monitoring requirements that favor suppliers with proven performance in extreme-temperature outdoor deployments.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Alps Alpine Co., Ltd positions itself at the intersection of miniaturized sensing and consumer electronics integration. The company’s established supply relationships with major electronics OEMs give it a structural distribution advantage that pure-play sensor manufacturers cannot replicate at comparable cost. Its ability to embed force sensing into multi-function components — rather than selling standalone devices — creates stickier customer relationships and reduces displacement risk from commodity sensor providers.

Flintec concentrates its competitive positioning on precision load cell design for legal-for-trade and industrial process applications. The company’s investment in traceable calibration capabilities and compliance with international weighing standards differentiates it in regulated markets where procurement teams face audit risk if they substitute non-certified alternatives. This compliance moat makes Flintec difficult to displace in food processing, pharmaceutical, and trade weighing segments where regulatory approval is a prerequisite to installation.

FUTEK Advanced Sensor Technology, Inc builds its market position around high-accuracy multi-axis force and torque sensing for aerospace, medical robotics, and precision test applications. Its product catalog depth — spanning miniature sensors for surgical instruments to large-capacity load cells for structural testing — allows FUTEK to serve buyers across multiple verticals from a single supplier relationship. This breadth reduces procurement complexity for multi-site industrial customers who prefer consolidating their sensor spend.

Honeywell International Inc leverages its global brand, diversified sensing portfolio, and established distribution network to serve force sensor buyers who prioritize supply chain reliability over lowest unit price. In September 2024, TE Connectivity acquired Sense Eletrônica Ltda, a move that signals consolidation pressure on mid-tier sensor suppliers — a dynamic that reinforces Honeywell’s advantage as a financially stable, multi-geography supplier capable of sustaining long-term product availability commitments that smaller competitors cannot credibly offer.

Key players

- Alps Alpine Co., Ltd

- Flintec

- FUTEK Advanced Sensor Technology, Inc

- Honeywell International Inc

- Hottinger Brüel & Kjær

- Interlink Electronics, Inc

- PPS UK Limited

- Qorvo, Inc

- Sensata Technologies, Inc

- Tangio Printed Electronics

- Tekscan, Inc.

- Flintec Inc.

- HITEC Sensor Developments Inc.

- Kistler Group

- TE Connectivity

- Other Key Players

Recent Developments

- March 2024 — Bota Systems launched the SensONE T5, a high-sensitivity six-axis force-torque sensor targeting collaborative robots with small payloads. The product addresses the precision sensing gap in lightweight cobot applications used in electronics assembly and medical research environments.

- April 2024 — Bota Systems unveiled the PixONE force-torque sensor series, featuring an ultra-lightweight through-hole design for enhanced robot integration. The series reduces mechanical interference in the robot wrist, improving accuracy in applications where sensor mass directly affects end-effector positioning precision.

- January 2025 — Bota Systems partnered with Kinova Robotics to integrate SensONE force-torque sensors with the Kinova Gen3 robotic manipulator. The collaboration targets advanced AI testing and research applications, where real-time force feedback is essential for developing adaptive manipulation algorithms in unstructured environments.

Report Scope

Report Features Description Market Value (2025) USD 3.2 Billion Forecast Revenue (2035) USD 5.2 Billion CAGR (2026-2035) 5.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Measurement Type (Both, Tension Force, Compression Force), By Sensing Technology (Strain Gauge, Load Cell, Force Sensitive Resistors, Others), By Operation (Digital, Analog), By End Use Industry (Automotive, Locomotive, Manufacturing, Mining, Aerospace and Defense, Construction, Healthcare, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Alps Alpine Co., Ltd, Flintec, FUTEK Advanced Sensor Technology, Inc, Honeywell International Inc, Hottinger Brüel & Kjær, Interlink Electronics, Inc, PPS UK Limited, Qorvo, Inc, Sensata Technologies, Inc, Tangio Printed Electronics, Tekscan, Inc., Flintec Inc., HITEC Sensor Developments Inc., Kistler Group, TE Connectivity, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Alps Alpine Co., Ltd

- Flintec

- FUTEK Advanced Sensor Technology, Inc

- Honeywell International Inc

- Hottinger Brüel & Kjær

- Interlink Electronics, Inc

- PPS UK Limited

- Qorvo, Inc

- Sensata Technologies, Inc

- Tangio Printed Electronics

- Tekscan, Inc.

- Flintec Inc.

- HITEC Sensor Developments Inc.

- Kistler Group

- TE Connectivity

- Other Key Players

Our Clients

- 181442

- Mar 2026