Quick Navigation

Report Overview

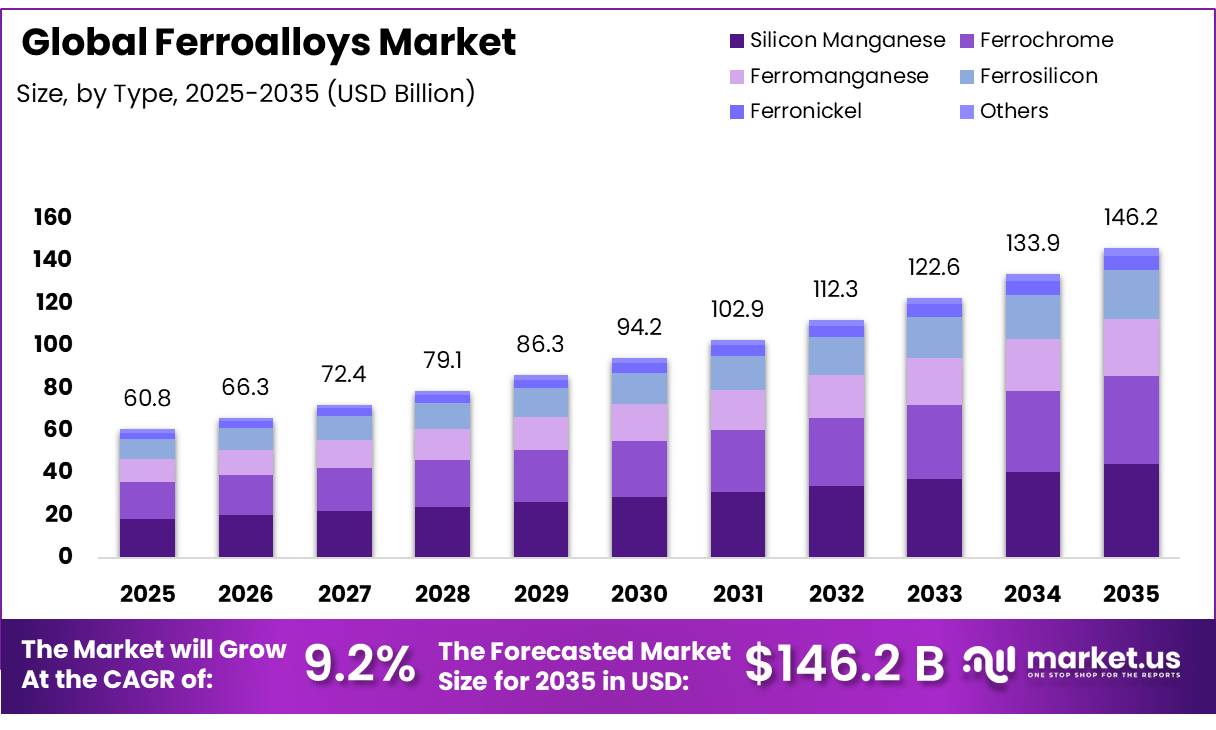

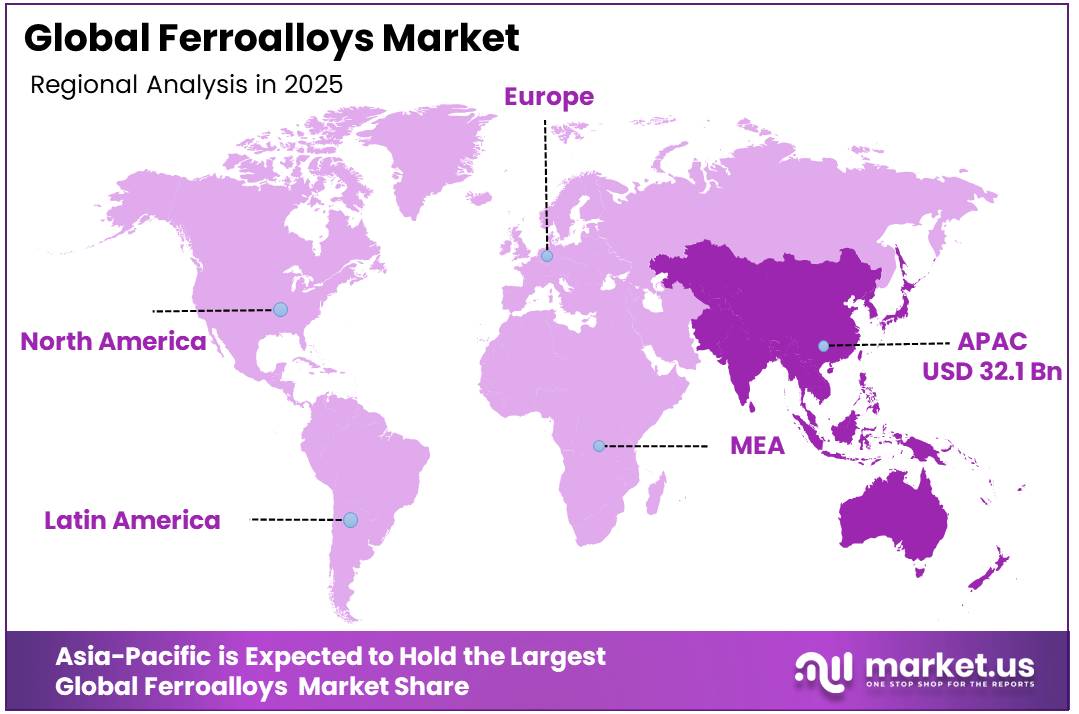

In 2025, the Global Ferroalloys Market was valued at US$60.8 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 9.2%, reaching about US$146.2 billion by 2035. In 2025, Asia Pacific led the market, achieving over 52.8% share with a revenue of US$ 32.1 Billion.

Key Takeaways

- The Global Ferroalloys Market was valued at US$60.8 billion in 2025.

- The global Ferroalloys Market is projected to grow at a CAGR of 9.2% and is estimated to reach US$146.2 billion by 2035.

- Silicon Manganese serves as the dominant product type within the global ferroalloys market, capturing a 30.5% segment share.

- Bulk Ferroalloys function as the dominant product category, overwhelmingly commanding 85.6% of the total market share.

- Deoxidizer operates as the leading market application, accounting for 34.7% of all ferroalloy utilization.

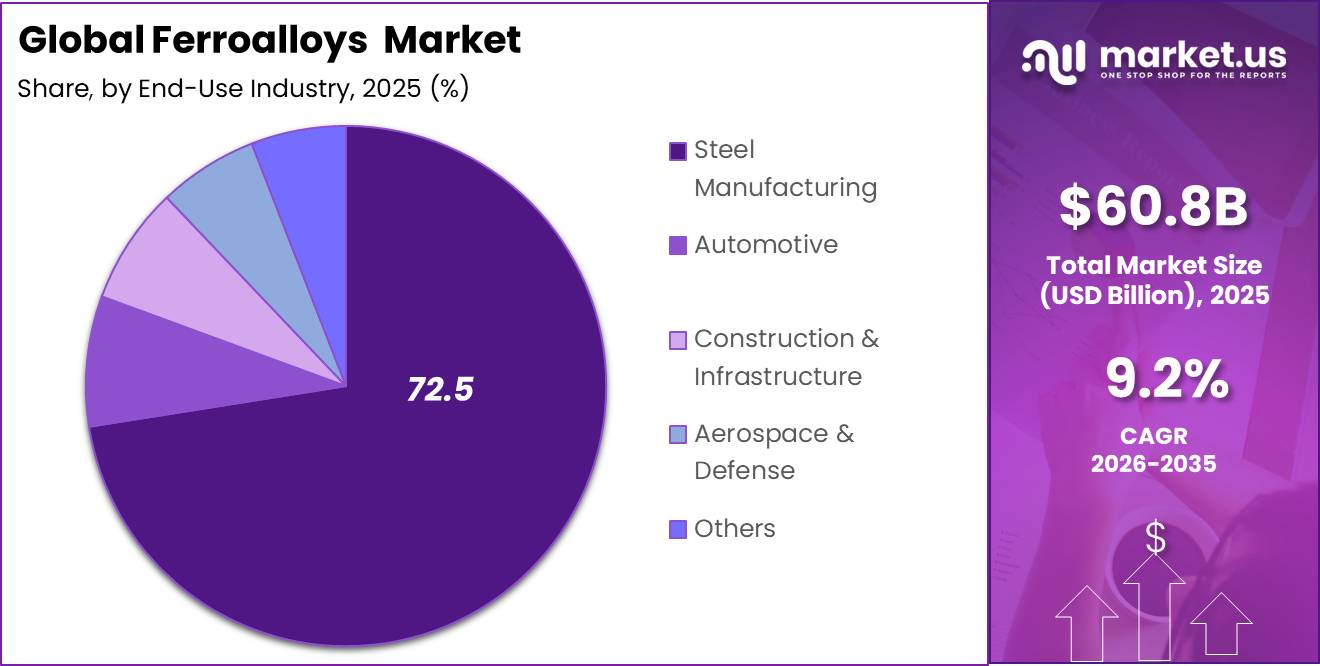

- Steel Manufacturing acts as the dominant end-use industry, standing as the primary growth driver with a massive 72.5% share.

- Asia Pacific emerges as the dominant geographic region, holding a 52.8% share of the global market

The global ferroalloys market is expanding due to ferroalloys’ relevance in reinforcing steel and automotive components. According to data from the United States Geological Survey (USGS), mineral-dependent manufacturing sectors contributed more than $4.09 trillion to the US GDP. The rapid development of infrastructure in emerging economies has been fueling this expansion. High fluctuation in electricity and energy prices presents a significant operational concern.

- According to the U.S. Geological Survey’s Mineral Commodity Summaries 2026, published on February 6, 2026, global chromite mine production was estimated at 51 million tonnes in 2025, representing a 3% increase from 2024. Global manganese ore production reached approximately 20 million tonnes of contained manganese in 2025, up from 18.7 million tonnes in 2024. The individual commodity reports are dated February 2026.

- According to the World Steel Association’s April 2026 Short-Range Outlook, global steel demand is nearing the end of its long-term structural adjustment cycle. Market demand rises by 0.3% to 1.724 billion tons, establishing a stable consumption foundation for bulk alloys. Decreasing contraction rates in China, along with steady industrial development in India, underpin this stabilization. This reversal safeguards the worldwide alloy smelting infrastructure against extreme demand fluctuations.

The production scope includes smelting methods such as submerged arc furnace and electric arc furnaces. Decarbonization of industries has emerged as the fastest-growing factor for demand. This means a quick move away from coal-dependent systems to more hydro-based manufacturing systems. The future forecast rests on the integration of artificial intelligence in the smelting processes. Smart AI programs optimize energy utilization to counteract price volatility. Intelligent automation leads to higher purity of chemical products without exposure to manganese fumes. Machine learning can estimate changes in raw material availability accurately.

Ferroalloys industries face dynamic changes in the sector, characterized by an ever-changing political environment and stringent regulations, including environmentally conscious measures. Protectionist policies, such as the EU CBAM, change conventional supply chain networks by targeting the carbon emissions of metal imports. In response to such trade barriers, producers are rapidly changing their metallurgy processes to include the use of green metallurgy by substituting metallurgical coal with renewable biocarbon as well as electric arc furnaces that use scrap steel. Precise segmentation in the market distinguishes the unique consumer profile of bulk alloys like silicomanganese and ferrosilicon compared to specialty noble alloys used in making stainless and electrical steels. Producers monitor benchmarking measures such as specific energy consumption (SEC).

Global Ferroalloys Market Segmentation

Type Analysis

Silicon Manganese leads with 30.5% due to its strong use in steelmaking.

In 2025, Silicon Manganese held a dominant market position, capturing more than a 30.5% share. By December 2025, its leadership remained supported by wide use in carbon steel and alloy steel production. Steelmakers rely on silicon manganese because it removes oxygen and improves strength, hardness, and surface quality. Its balanced alloying properties also help mills simplify production and control costs. Demand stayed firm across construction steel, automotive components, machinery, rail equipment, and infrastructure products. Reliable availability and established furnace technology further strengthened its position among major ferroalloy categories.

Ferrochrome emerged as the growing segment during December 2025. Its demand increased with wider stainless steel production and rising need for corrosion-resistant materials. Producers serving transport, energy, engineering, and processing industries benefited from this shift. Greater use of durable steel grades is expected to support continued ferrochrome consumption steadily worldwide.

Product Category Analysis

Bulk Ferroalloys lead with 85.60% due to their essential role in large-scale steel production.

In 2025, Bulk Ferroalloys held a dominant market position, capturing more than a 85.60% share. By December 2025, the segment remained central to steelmaking because products such as ferromanganese, silicomanganese, and ferrosilicon are used in large volumes for deoxidation, alloying, and strength improvement. Their broad availability, established production base, and suitability for carbon and low-alloy steels supported steady demand. Construction, automotive, machinery, rail, and infrastructure industries continued to depend on bulk ferroalloys for consistent steel quality and cost-efficient output.

Noble Ferroalloys emerged as the growing segment in December 2025. Demand increased as producers focused on specialty steels with better heat resistance, corrosion protection, hardness, and performance. Their use in aerospace, energy, defence, and advanced engineering applications supported wider adoption, especially where precise alloy composition and superior material properties were required across demanding and high-value manufacturing environments.

Application Analysis

Deoxidizer leads with 34.70% due to its essential role in producing clean, high-quality steel.

In 2025, Deoxidizer held a dominant market position, capturing more than a 34.70% share. By December 2025, the segment remained widely used because ferroalloys remove dissolved oxygen from molten steel and reduce defects during casting. Steel producers depend on deoxidizers to improve strength, surface finish, consistency, and overall product quality. Their regular use across carbon steel, stainless steel, construction steel, automotive components, machinery, and rail products supported stable demand. Established production methods and compatibility with large-scale steelmaking also strengthened the segment’s leading position.

Alloying Element Additive emerged as the growing segment in December 2025. Its use increased as manufacturers developed steel grades with better hardness, wear resistance, heat tolerance, and corrosion protection. Rising demand from energy, transport, defence, and advanced engineering applications encouraged greater consumption of ferroalloys as performance-enhancing additives in demanding and specialized manufacturing environments.

By End-Use Industry Analysis

Steel Manufacturing leads with 72.50% because ferroalloys remain essential for producing strong and reliable steel.

In 2025, Steel Manufacturing held a dominant market position, capturing more than a 72.50% share. By December 2025, the segment continued to lead because ferroalloys are widely used to improve steel strength, hardness, cleanliness, and resistance to wear and corrosion. Steel producers depend on manganese, silicon, chromium, and other alloying materials during melting and refining. Strong demand from construction, infrastructure, machinery, railways, energy equipment, and industrial fabrication supported regular ferroalloy consumption. Large production volumes, established supply chains, and the continuous need for consistent steel quality further strengthened the segment’s market position.

Automotive emerged as the growing segment in December 2025. Vehicle manufacturers increasingly used high-strength and specialty steels to reduce weight, improve safety, and extend component life. This trend supported rising ferroalloy use in body structures, engines, transmissions, suspension systems, and electric vehicle components globally.

Key Market Segments

By Type

- Silicon Manganese

- Ferrochrome

- Ferromanganese

- Ferrosilicon

- Ferronickel

- Others

By Product Category

- Bulk Ferroalloys

- Noble Ferroalloys

By Application

- Deoxidizer

- Alloying Element Additive

- Stainless Steel Production

- Desulfurizer

- Others

By End-Use Industry

- Steel Manufacturing

- Automotive

- Construction & Infrastructure

- Aerospace & Defense

- Others

Drivers

Restraints

Opportunity

Challenge

Geopolitical Impact Analysis

The Russia-Ukraine War and the Ferroalloys Market

The current conflict between Russia and Ukraine is a major disruptor, changing trade routes, pricing baselines, and supply vulnerabilities in the global ferroalloys market. Previously positioned as significant upstream exporters of vital bulk and specialty alloys, both states have seen their production and logistical networks severely changed by targeted military actions and international economic reprisal.

Localized frontline wars in Ukraine, as well as continuous energy infrastructure degradation, have directly harmed domestic smelting capacity. Massive processing operations, including big Ukrainian silicomanganese and ferromanganese factories, frequently drop to minimal capabilities or come to a complete halt as a result of severe localized electricity shortages and unsustainable power rates. Concurrently, damaged rail links and frontline transport bottlenecks have reduced regional export volumes to historic lows, interrupting supplies to important consumer countries such as Poland, Turkey, and Italy.

Russia’s export market is seeing unprecedented regulatory friction as broad global sanctions packages are fully implemented. While past carve-outs and transition quotas provided temporary protection for material exports, strict limitations on direct imports of Russian pig iron, direct reduced iron (DRI), and core ferroalloy variations into the European Union severely penalize uncertified supply lines. Furthermore, rigorous secondary restrictions penalize third-party producers processing Russian-origin metallurgical inputs, permanently weakening traditional Western supply chain dependence on Russian ferrosilicon and noble alloys.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Ferroalloys Market.

The Asia-Pacific region accounted for a leading 52.8% share in the global ferroalloys market. This clear dominance is driven directly by the massive concentration of primary crude steel manufacturing hubs, rapid urbanization, and extensive civil infrastructure developments across the territory. According to the World Population Review’s demographic and economic findings, Asia-Pacific is home to more than 60% of the world’s human population, with nations such as India and China leading the way in growing population concentration and megacity expansion. This dense human footprint establishes an indefinite structural mandate for commercial long goods, automobile sheets, and high-performance engineering alloys, tying regional smelting networks to large continuous-feed manufacturing regimes. For example, large-scale metallurgical complexes in mainland China and India utilize millions of tonnes of bulk ferromanganese, silicomanganese, and ferrosilicon each year to meet rising domestic infrastructure and real estate construction demands.

The region’s overwhelming supremacy is bolstered by its easy access to low-cost mineral riches and extremely advantageous government manufacturing projects. Upstream mining operations and massive localized submerged arc furnace installations across major regional corridors, such as China’s inner manufacturing provinces and India’s mineral-rich eastern belt, benefit from vertically integrated supply chains that protect refiners from external logistical shocks. Furthermore, the rapid expansion of industrial production programs in growing Southeast Asian nations produces a highly localized, insatiable need for heavy alloying elements. Because these developing economies are constantly expanding their automotive body manufacturing lines and cross-country railway networks, the broader Asia-Pacific regional market continues to expand at a faster rate than Western manufacturing corridors.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global ferroalloys market exhibits a highly consolidated, oligopolistic structure where the market is controlled by a small number of leading global players. Market concentration is particularly strong across bulk alloy divisions, where massive initial capital expenditures and significant energy access barriers prevent smaller competitors from entering the market. The top market leaders control significant portions of worldwide output by running tightly integrated operations that include everything from raw manganese and chromium ore mines to high-capacity submerged arc furnace plants. These large producers influence contract pricing, which is heavily shaped by ore costs and electricity prices, to protect their processing margins from external raw material disruptions. This oligopolistic behavior enables dominant businesses to carefully manage production capacity, secure long-term supply contracts with key global steel mills, and exert stronger market control via centralized distribution networks.

In contrast, the specialty noble ferroalloy segments of ferrovanadium, ferromolybdenum, and ferrotungsten exhibit more fragmented and competitive behavior, as do limited downstream processing corridors. In these technological niches, multiple medium-sized refiners and secondary recycling operators fight for market share using product purity, chemical precision, and tailored formulation criteria rather than sheer volume scale. In these regions, various independent local smelters use their closeness to regional steel mills and different localized power subsidies to compete with worldwide suppliers. This combination of a tightly consolidated bulk oligopoly at the base and highly localized, fragmented specialty channels at the tip results in a two-layered competitive environment in which players must constantly optimize their specific energy consumption (SEC) and supply chain logistics to maintain market share.

Market Key Players

- Glencore plc

- Eurasian Resources Group (ERG)

- Tsingshan Holding Group Co., Ltd.

- Samancor Chrome

- Erdos Group

- Jiangsu Delong Nickel Industry Co., Ltd.

- Nikopol Ferroalloy Plant

- Shandong Xinhai Technology Co., Ltd.

- OM Holdings Ltd.

- Sakura Ferroalloys Sdn. Bhd.

- Vale S.A.

- Tata Steel Limited

- ArcelorMittal S.A.

- China Minmetals Corporation

- OFZ, a.s.

- Ferro Alloys Corporation Limited (FACOR)

- Georgian American Alloys, Inc.

- Gulf Ferroalloys Company (SABAYEK)

- Outokumpu Oyj

- Sheng Yan Group

- Others

Key Development

- In May 2026, Vale advanced production agreements with the U.S. DOE, which published NEPA compliance reviews for Phase 1 of its industrial briquette facility using cold-agglomeration technology to supply low-carbon inputs for high-strength steel-making.

- In May 2026, Glencore signed a follow-on strategic collaboration and equity investment agreement with Chilean Cobalt Corp (C3), officially disclosed in U.S. SEC filings. The agreement strengthens Glencore’s strategic position in critical mineral supply chains.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$60.8 Bn |

| Forecast Revenue (2035) | US$146.2 Bn |

| CAGR (2026-2035) | 9.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Silicon Manganese, Ferrochrome, Ferromanganese, Ferrosilicon, Ferronickel, Others), By Product Category (Bulk Ferroalloys, Noble Ferroalloys), By Application (Deoxidizer, Alloying Element Additive, Stainless Steel Production, Desulfurizer, Others), By End-Use Industry (Steel Manufacturing, Automotive, Construction & Infrastructure, Aerospace & Defense, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Glencore plc, Eurasian Resources Group (ERG), Tsingshan Holding Group Co. Ltd., Samancor Chrome, Erdos Group, Jiangsu Delong Nickel Industry Co. Ltd., Nikopol Ferroalloy Plant, Shandong Xinhai Technology Co. Ltd., OM Holdings Ltd., Sakura Ferroalloys Sdn. Bhd., Vale S.A., Tata Steel Limited, ArcelorMittal S.A., China Minmetals Corporation, OFZ a.s., Ferro Alloys Corporation Limited (FACOR), Georgian American Alloys Inc., Gulf Ferroalloys Company (SABAYEK), Outokumpu Oyj, Sheng Yan Group, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |