Quick Navigation

Report Overview

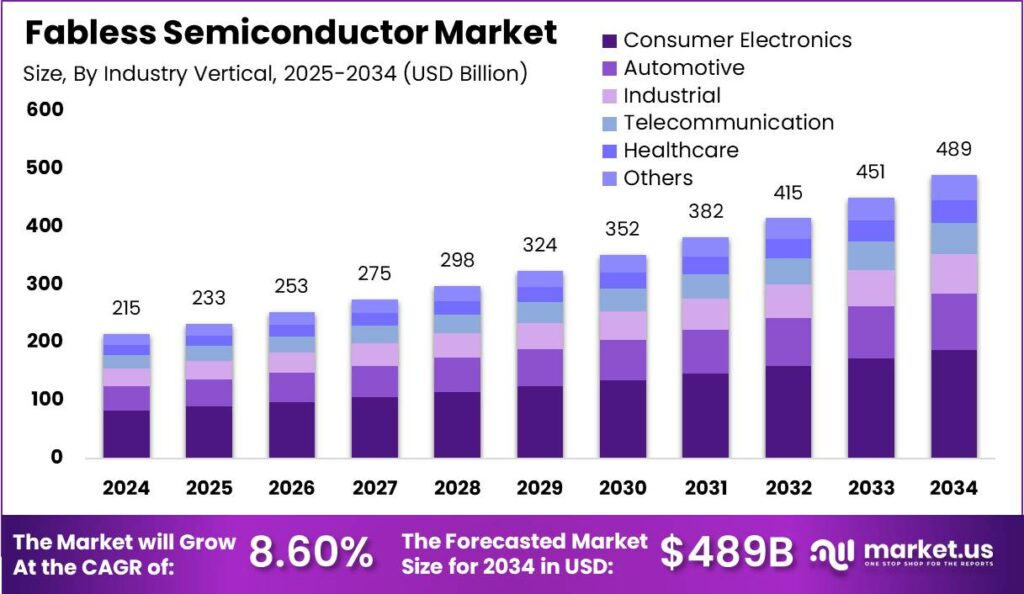

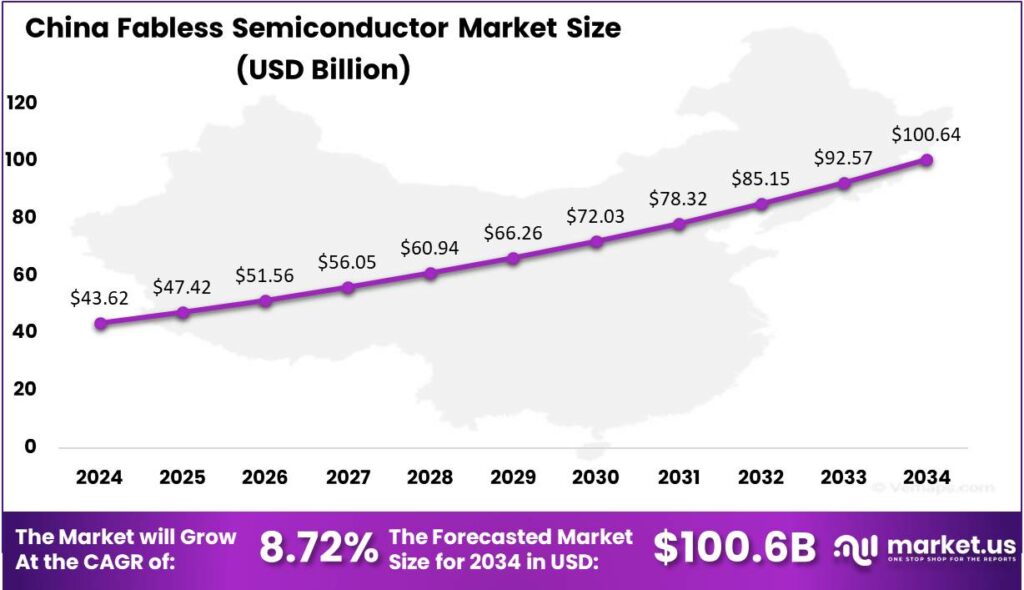

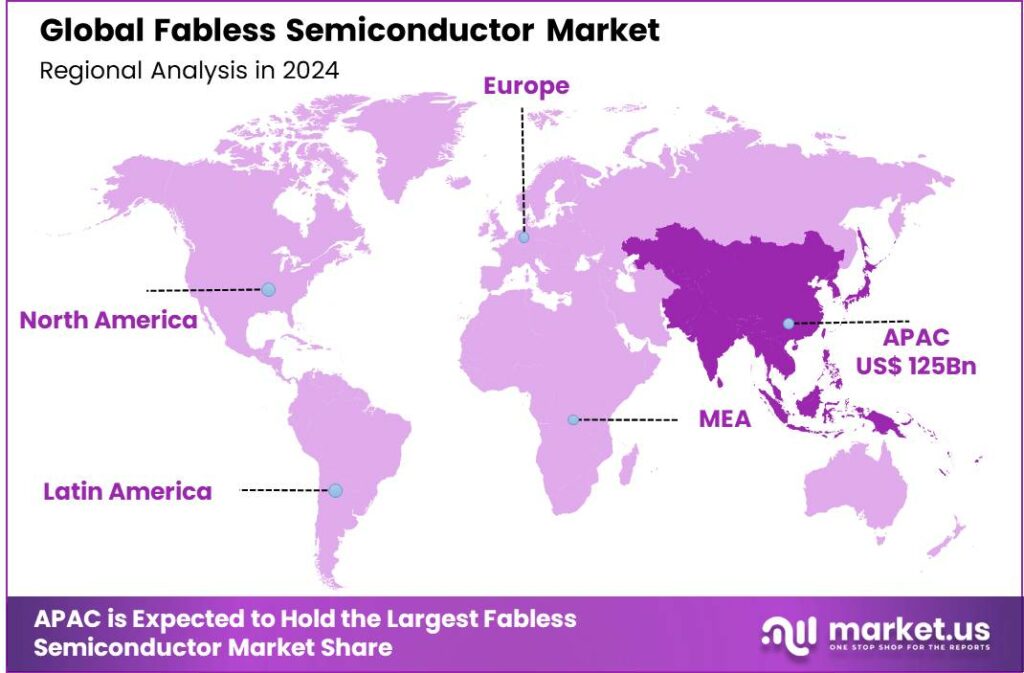

The Global Fabless Semiconductor Market size is expected to be worth around USD 489 Billion By 2034, from USD 214.5 Billion in 2024, growing at a CAGR of 8.60% during the forecast period from 2025 to 2034. In 2024, the Asia-Pacific region led the fabless semiconductor market, holding over 58.61% share and generating USD 125 billion in revenue. The China market was valued at USD 43.62 billion and is expected to grow at a CAGR of 8.72%.

A fabless semiconductor company specializes in the design and sale of hardware devices and semiconductor chips while outsourcing the fabrication (or ‘fab’) of these components to a specialized manufacturer known as a semiconductor foundry. This model enables fabless companies to focus on semiconductor design and development without the high costs of operating a fab.

The fabless semiconductor market involves companies that design and distribute chips and semiconductors but do not own or operate their own fabrication facilities. These companies leverage the manufacturing capabilities of third-party foundries, which allows them to be highly flexible and adaptive to changing market demands and technological advancements.

The primary driving factors for the fabless semiconductor market include the rising demand for advanced technology applications like artificial intelligence, Internet of Things (IoT), and 5G. These technologies require sophisticated semiconductor components that can handle high performance and low power consumption, which are effectively provided by fabless manufacturers.

The demand for fabless semiconductors is largely fueled by consumer electronics, with companies such as Apple and Samsung requiring advanced, energy-efficient chips for smartphones, tablets, and other devices. Additionally, the automotive sector’s rapid advancement in electric vehicles and ADAS systems also significantly contributes to the demand, requiring high-performance semiconductor solutions to support these technologies.

Adopting a fabless model offers several business benefits, including reduced capital expenditure as companies do not need to fund costly fab facilities. This allows them to allocate more resources towards research and development, enhancing innovation. The model also provides flexibility in scaling operations without the constraints of physical manufacturing capacity, enabling faster adaptation to market changes and technology advancements.

Key Takeaways

- The Global Fabless Semiconductor Market is projected to reach a value of USD 489 Billion by 2034, up from USD 214.5 Billion in 2024, growing at a CAGR of 8.60% during the forecast period from 2025 to 2034.

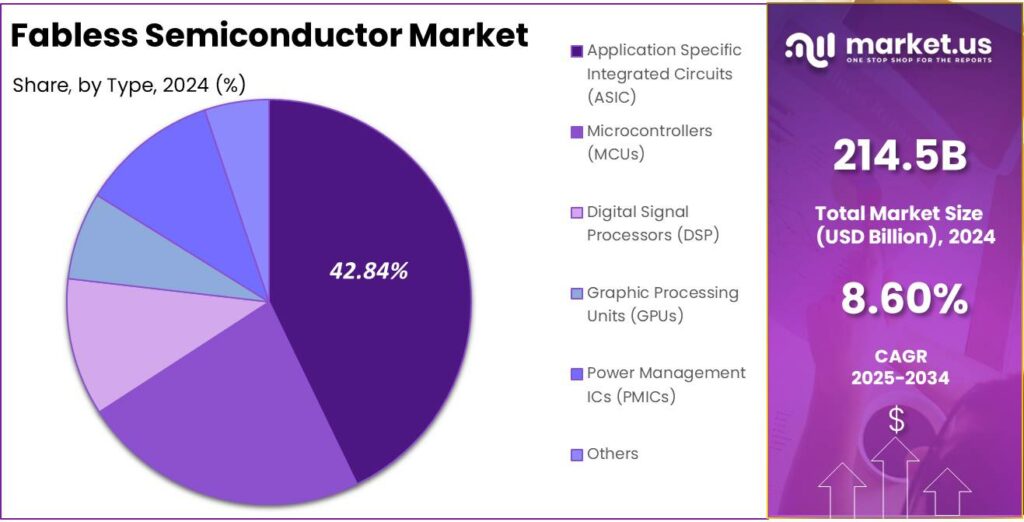

- In 2024, the Application Specific Integrated Circuits (ASIC) segment dominated the fabless semiconductor market, holding a market share of over 42.84%.

- The Consumer Electronics segment was the leading application in the fabless semiconductor market in 2024, capturing more than 38.3% of the market share.

- Asia-Pacific region led the fabless semiconductor market in 2024, with a significant share of over 58.61%, generating USD 125 billion in revenues.

- The fabless semiconductor market in China was valued at USD 43.62 billion in 2024, and it is expected to grow at a CAGR of 8.72%.

Analysts’ Viewpoint

From an investment perspective, the fabless semiconductor market presents substantial opportunities due to its robust growth and the critical role of semiconductors in modern technology. The market is expected to benefit significantly from advancements in technology and the increasing integration of semiconductors in various industries.

However, potential investors should be aware of the challenges related to global supply chain dependencies and the intense competition among leading market players. Strategic partnerships and innovations in semiconductor technology will likely be key factors influencing future market dynamics and investment opportunities

China Fabless Semiconductor Market

In 2024, the market for fabless semiconductors in China was valued at $43.62 billion. This market is projected to grow at a compound annual growth rate (CAGR) of 8.72%. The robust growth in the Chinese fabless semiconductor market can be attributed to several factors.

The rising demand for consumer electronics and expanding telecommunications infrastructure has fueled the need for advanced semiconductors. China’s reliance on high-performance integrated circuits for devices like smartphones and tablets drives this growth.

Moreover, government initiatives aimed at boosting domestic technological capabilities have fostered an environment conducive to the development of the semiconductor industry.Policies promoting innovation and R&D have helped local companies advance semiconductor technologies, boosting their global competitiveness.

Partnerships between Chinese firms and international tech providers have been key in sharing expertise, enhancing the design and production capabilities of Chinese fabless semiconductor companies. As these companies evolve, the market is set to maintain its growth, supported by both national and international backing.

In 2024, Asia-Pacific held a dominant market position in the fabless semiconductor market, capturing more than a 58.61% share with revenues amounting to USD 125 billion. This significant market share can be attributed to several key factors that underscore the region’s pivotal role in the global semiconductor industry.

Asia-Pacific leads the fabless semiconductor sector due to strong manufacturing capabilities and extensive supply chains in China, South Korea, and Taiwan. These nations, with advanced infrastructure and supportive policies, are key to semiconductor production and export. Investments in fabs and R&D have driven the region to the industry’s forefront.

The concentration of consumer electronics manufacturers in Asia-Pacific boosts the demand for fabless semiconductors. As global demand for mobile devices, PCs, and tech products grows, manufacturers in the region are increasingly relied upon for their ability to rapidly scale production and meet international market demands.

Strategic alliances between Asia-Pacific firms and global tech leaders have boosted innovation in semiconductor design and performance. These collaborations strengthen the regional ecosystem, ensuring continued growth and leadership in the fabless semiconductor market. Asia-Pacific is set to maintain its dominance through ongoing advancements and strong market demand.

Type Analysis

In 2024, the Application Specific Integrated Circuits (ASIC) segment held a dominant market position within the fabless semiconductor industry, capturing more than a 42.84% share. This leadership can be attributed to ASICs’ critical role in customized, high-performance computing tasks which are essential in sectors like telecommunications, data centers, and advanced automotive systems.

The rise of data-intensive technologies like 5G and machine learning has accelerated the growth of the ASIC segment. These technologies require fast, energy-efficient data processing, where ASICs thrive due to their custom design. As adoption increases, demand for ASICs continues to grow, solidifying their dominant position in the market.

The growing demand for secure hardware solutions amidst rising cybersecurity threats has also fueled the ASIC segment. ASICs can be customized with built-in security features, making them less vulnerable to attacks than generic hardware. This advantage makes them particularly valuable in sectors like finance and healthcare, where data security is critical.

The trend toward miniaturization boosts ASIC dominance, as their ability to integrate high functionality into small sizes aligns with the industry’s push for smaller, lighter, and more efficient devices. As industries innovate towards compact solutions, ASICs are set to maintain their lead in the fabless semiconductor market due to their efficiency and adaptability.

Industry Vertical Analysis

In 2024, the Consumer Electronics segment held a dominant market position in the fabless semiconductor market, capturing more than a 38.3% share. This leadership is attributed to several core factors that align with the global demand trends and technological advancements in the consumer electronics industry.

The continuous innovation in consumer devices like smartphones, tablets, laptops, and wearables has significantly boosted the demand for fabless semiconductors. These components are crucial for improving processing speeds, connectivity, and power efficiency. As consumer expectations for faster, more powerful devices grow, so does the need for advanced semiconductors to meet these demands.

The integration of IoT technology into consumer electronics has created new growth opportunities. Smart home devices, connected appliances, and advanced communication tools require sophisticated semiconductors for efficient operation. As the number of smart devices increases, so does the demand in the consumer electronics sector.

Additionally, the trend towards miniaturization of electronic devices necessitates the use of fabless semiconductors that can provide high functionality in smaller sizes. This trend not only applies to portable devices but also to the emerging technologies such as wearable health monitors and augmented reality systems, further expanding the scope of the consumer electronics segment.

Key Market Segments

By Type

- Microcontrollers (MCUs)

- Digital Signal Processors (DSP)

- Graphic Processing Units (GPUs)

- Application Specific Integrated Circuits (ASIC)

- Power Management ICs (PMICs)

- Others

By Industry Vertical

- Consumer Electronics

- Automotive

- Industrial

- Telecommunication

- Healthcare

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Rising Demand for Advanced Semiconductor Solutions

The fabless semiconductor industry is experiencing significant growth, driven by the escalating demand for advanced semiconductor solutions across various sectors. The proliferation of emerging technologies such as 5G, artificial intelligence (AI), the Internet of Things (IoT), and electric vehicles (EVs) has necessitated the development of sophisticated, high-performance chips.

These technologies require complex integrated circuits capable of delivering enhanced processing power, energy efficiency, and connectivity. Consequently, fabless companies, specializing in innovative chip design without owning fabrication facilities, are well-positioned to meet this demand. By focusing on research and development, these companies can rapidly adapt to technological advancements and deliver customized solutions, thereby fueling the industry’s expansion.

Restraint

Dependence on Third-Party Foundries

A significant restraint for fabless semiconductor companies is their reliance on third-party foundries for chip manufacturing. While this model allows companies to focus on design and innovation, it also exposes them to risks associated with external fabrication processes.

Potential issues include limited control over production schedules, quality assurance challenges, and supply chain vulnerabilities. Geopolitical tensions or natural disasters in key foundry regions can cause production delays, while the rising complexity of semiconductor designs requires tight collaboration between designers and manufacturers.

Misalignment can lead to inefficiencies and longer time-to-market. As demand for advanced chips grows, foundries may prioritize larger clients, putting smaller fabless firms at a disadvantage. This highlights the importance of strong partnerships and diversified manufacturing strategies to mitigate risks.

Opportunity

Expansion into Emerging Markets

The fabless semiconductor industry has a significant opportunity to expand into emerging markets, particularly in regions experiencing rapid technological adoption and industrialization. Countries in Asia, Africa, and Latin America are seeing growing demand for consumer electronics, automotive innovations, and smart infrastructure, all driving the need for advanced semiconductor solutions.

By tailoring products to meet the specific needs of these markets, fabless companies can tap into new revenue streams and establish a strong global presence. Moreover, collaborations with local firms and participation in government initiatives aimed at technological development can facilitate market entry and acceptance.

This strategic expansion not only diversifies business portfolios but also contributes to global technological advancement, positioning fabless companies as key players in the worldwide semiconductor landscape.

Challenge

Intellectual Property Protection

Protecting intellectual property (IP) presents a significant challenge for fabless semiconductor companies. The nature of the fabless model necessitates sharing sensitive design information with external foundries, increasing the risk of IP theft or unauthorized use.

In regions where IP enforcement is weak or regulations are lax, companies face heightened vulnerability to counterfeiting and infringement. Such breaches can lead to substantial financial losses and erosion of competitive advantage.

To mitigate these risks, fabless firms must implement stringent legal agreements, employ advanced encryption and security protocols, and conduct thorough due diligence when selecting manufacturing partners. Balancing collaboration with IP protection demands constant vigilance and strategic planning, highlighting the complexity of the global semiconductor industry.

Emerging Trends

The fabless semiconductor industry is undergoing major changes due to technological advancements and shifting market needs. A key trend is the growing integration of AI capabilities into chip designs. Fabless companies are creating application-specific integrated circuits (ASICs) for AI, improving processing efficiency for tasks like machine learning and data analytics.

A key development is the rise of advanced packaging techniques. With traditional scaling facing physical limits, fabless companies are turning to this approach to boost performance and functionality by stacking and interconnecting multiple chiplets, enhancing efficiency and reducing latency.

The proliferation of Internet of Things (IoT) devices has also influenced the fabless sector. There is a growing demand for low-power, high-performance chips to support the vast network of connected devices. Fabless companies are focusing on designing energy-efficient semiconductors to cater to this expanding market.

Business Benefits

The fabless semiconductor model offers key advantages, notably reducing capital expenditure. By outsourcing manufacturing to specialized foundries, companies save on the high costs of building and maintaining fabrication facilities, enabling better allocation of resources for research, development, and innovation.

This model also provides greater flexibility and scalability. Fabless companies can quickly adapt to market changes by collaborating with various foundries, enabling them to scale production up or down based on demand. This agility is particularly beneficial in the fast-paced technology sector, where rapid responses to market trends are crucial.

Focusing solely on design and development allows fabless firms to specialize and innovate without the distractions of manufacturing complexities. This specialization often leads to the creation of high-quality, cutting-edge products that meet specific market needs. Additionally, it fosters a competitive environment where companies strive to differentiate themselves through unique design capabilities.

Key Benefits

The fabless semiconductor model has gained significant traction in the tech industry, providing several advantages over traditional Integrated Device Manufacturers (IDMs)

- Lower Capital Expenditure: Fabless companies avoid the massive costs associated with building and maintaining fabrication plants (fabs). By outsourcing production to specialized foundries, they can allocate more funds to research and development, which drives innovation and enhances their competitive edge.

- Increased Flexibility and Agility: Without the burden of managing manufacturing facilities, fabless firms can quickly adapt to market changes. They can scale production up or down based on demand, allowing them to respond more effectively to emerging trends and opportunities.

- Focus on Innovation: The fabless model allows companies to concentrate on chip design and innovation rather than the complexities of manufacturing. This focus fosters a culture of creativity and collaboration, enabling fabless firms to develop cutting-edge technologies that meet evolving customer needs.

- Access to Advanced Manufacturing Technologies: By partnering with leading foundries like TSMC, fabless companies gain access to state-of-the-art manufacturing capabilities without the need for heavy investments. This partnership enables the production of high-quality chips using cutting-edge semiconductor technology.

- Higher Profit Margins: Fabless companies typically enjoy better gross margins compared to IDMs. The capital-light structure of the fabless model allows for leaner operations and healthier profit margins, as they do not incur the substantial overhead costs associated with owning fabs.

Key Player Analysis

The Fabless Semiconductor Market has become highly competitive, with several leading players shaping the semiconductor landscape.

Broadcom is a major player in the fabless semiconductor industry, renowned for its diverse portfolio of products, including chips used in networking, broadband, data centers, and wireless communications. The company has a solid reputation for delivering high-performance semiconductors that cater to various industries, from telecommunications to consumer electronics.

Qualcomm Inc. is a dominant force in the fabless semiconductor sector, particularly in the mobile and wireless technology markets. Known for its Snapdragon processors, Qualcomm designs chips that power smartphones, tablets, and other connected devices. Its leadership in 5G technology further cements its position in the industry.

Nvidia Corporation is best known for its graphics processing units (GPUs), which are used in gaming, artificial intelligence, data centers, and more. As a fabless company, Nvidia has become a leader in GPU technology, with its chips powering not only gaming consoles but also driving advancements in AI and deep learning.

Top Key Players in the Market

- Broadcom Inc.

- Qualcomm Inc.

- Nvidia Corporation

- Advanced Micro Devices Inc. (AMD)

- MediaTek Inc.

- Novatek Microelectronics Corp.

- UNISOC (Shanghai) Technologies Co., Ltd.

- XMOS

- LSI Corporation

- SMIC

- Marvell

- Realtek

- Other Major Players

Top Opportunities

The fabless semiconductor market presents several burgeoning opportunities that are shaping the landscape for industry players.

- Emerging Market Expansion: The increasing demand for consumer electronics in emerging markets, particularly in Asia-Pacific, is driving the need for more advanced semiconductor solutions. This region, led by countries like China, Taiwan, and South Korea, is expected to dominate the market due to its robust semiconductor manufacturing ecosystem.

- Automotive Sector Innovation: As the automotive industry continues to integrate more advanced electronic systems for electric vehicles and autonomous driving technologies, there is a growing need for specialized semiconductor components. The rise of electric vehicles and smart automotive technologies is pushing the demand for semiconductors in automotive applications, making it a key area of opportunity.

- Technological Advancements in AI and IoT: The market is witnessing significant growth driven by the advancements in artificial intelligence (AI) and the Internet of Things (IoT). Fabless companies are at the forefront of designing and developing chips that support these technologies, which are becoming increasingly prevalent across various consumer and industrial applications.

- High-Performance Computing and Data Centers: With the rapid expansion of data centers and the increasing reliance on cloud computing and big data analytics, there is a heightened demand for high-performance semiconductor chips. This sector offers substantial opportunities for fabless companies to innovate and provide solutions that meet the complex requirements of modern data centers.

- Healthcare Advancements: The healthcare sector is increasingly utilizing advanced technologies, including wearables and remote monitoring devices, which require sophisticated semiconductors to function effectively. The growth in medical technology and healthcare devices opens new avenues for fabless semiconductor companies to develop specialized chips that can meet the stringent requirements of this sector.

Recent Developments

- In May 2024, India’s first commercial high-performance system on chip (SoC), named Secure IoT, has been launched by Mindgrove Technologies. This fabless semiconductor startup, supported by Peak XV Partners, marks a significant milestone in the tech industry.

- In August 2024, VanEck is unveiling its latest thematic equity ETF, the VanEck Fabless Semiconductor ETF (SMHX), which focuses on fabless semiconductor companies. These firms design and develop chips while outsourcing their manufacturing, unlike integrated chip makers who handle both design and production in-house.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 214.5 Bn |

| Forecast Revenue (2034) | USD 489 Bn |

| CAGR (2025-2034) | 8.60% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Type (Microcontrollers (MCUs), Digital Signal Processors (DSP), Graphic Processing Units (GPUs), Application Specific Integrated Circuits (ASIC), Power Management ICs (PMICs), Others), By Industry Vertical (Consumer Electronics, Automotive, Industrial, Telecommunication, Healthcare, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Broadcom Inc., Qualcomm Inc., Nvidia Corporation, Advanced Micro Devices Inc. (AMD), MediaTek Inc., Novatek Microelectronics Corp., UNISOC (Shanghai) Technologies Co., Ltd., XMOS, LSI Corporation, SMIC, Marvell, Realtek, Other Major Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |