Global Edible Offal Market Size, Share, And Industry Analysis Report By Source (Cattle, Goat, Pig, Sheep, Poultry, Horse, Others), By Application (Fresh, Processed), By Distribution Channel (Wholesale Stores, Food Service, Retail, Online Sales, Hypermarkets and Supermarkets, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181638

- Number of Pages: 317

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

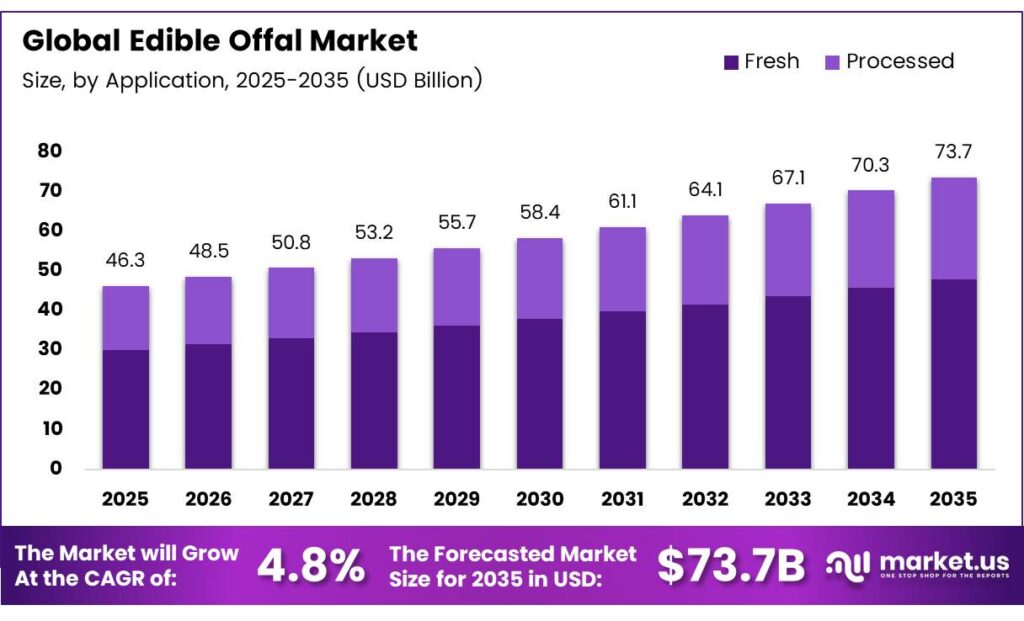

The Global Edible Offal Market size is expected to be worth around USD 73.7 billion by 2035 from USD 46.3 billion in 2025, growing at a CAGR of 4.8% during the forecast period 2026 to 2035.

Edible offal refers to the internal organs and other parts of livestock animals used for human food or animal feed. These include hearts, livers, kidneys, tongues, tripe, and other by-products from cattle, pigs, poultry, sheep, and goats. Offal delivers high nutritional value at relatively lower costs compared to prime cuts.

Global demand for organ meats continues to rise across both human food and premium pet food segments. Emerging markets in the Asia Pacific drive strong consumption, while Western markets increasingly embrace nose-to-tail eating philosophies. Moreover, industrial meat processors face stricter waste reduction targets, pushing offal utilization higher across global supply chains.

The United Kingdom imported $23,193,310 worth of frozen edible offal of sheep, goats, and horses in 2024, with a volume of 7,478,140 kg, reflecting sustained Western demand for specialty offal imports despite cultural hesitance in some consumer segments.

Australia’s beef offal exports reached a record 183,729 tonnes in 2024, a 17% increase year-over-year and 13% higher than the previous record set in 2014. This record export performance confirms growing international appetite for edible offal products across Asia, the Middle East, and North America.

Growth opportunities emerge across functional food development, pharmaceutical extraction, and premium pet nutrition. Bioactive compounds such as heparin, sourced from organ tissues, attract strong pharmaceutical interest. Consequently, processors and exporters now target higher-value applications beyond traditional food channels, creating diversified revenue streams for market participants.

Key Takeaways

- The Global Edible Offal Market is projected to reach USD 73.7 billion by 2035, growing at a CAGR of 4.8% from 2026 to 2035 was valued at USD 46.3 billion in 2025.

- Cattle dominate with a 41.7% share in 2025.

- The Fresh segment leads with a 67.9% share in 2025.

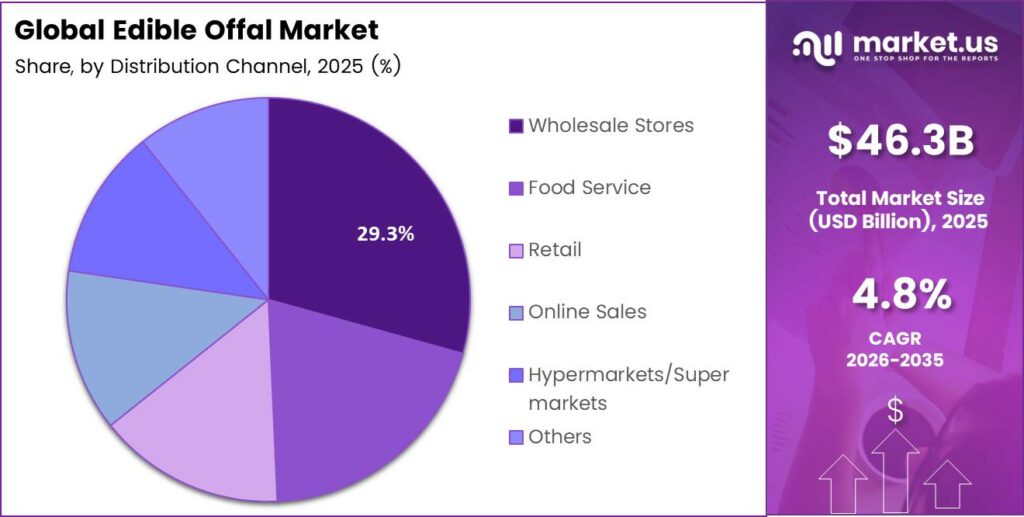

- Wholesale Stores hold the largest share at 29.3% in 2025.

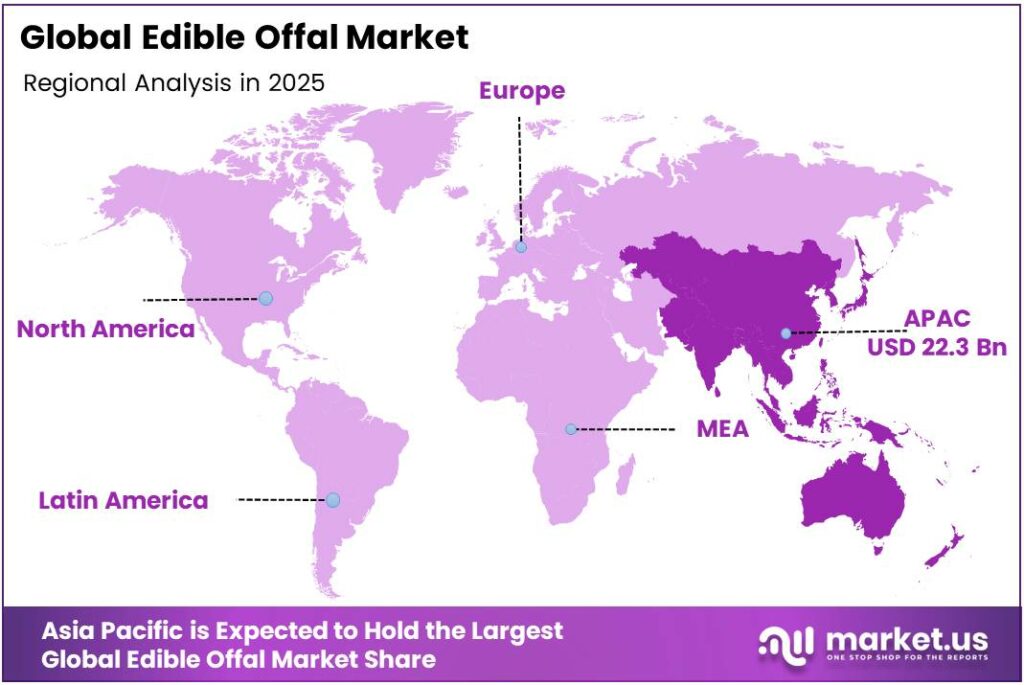

- Asia Pacific dominates the regional landscape with a 48.1% share, valued at USD 22.3 billion in 2025.

By Source Analysis

Cattle dominate with 41.7% due to high livestock volumes and widespread culinary demand globally.

In 2025, Cattle held a dominant market position in the By Source segment of the Edible Offal Market, with a 41.7% share. Cattle offal, including liver, kidney, tongue, and tripe, commands high demand across both food service and retail channels. Moreover, large-scale beef processing infrastructure supports consistent supply volumes globally.

Goat offal maintains strong demand across South Asia, the Middle East, and Sub-Saharan Africa, where traditional cuisines center on whole-animal preparation. Goat organ meats feature prominently in festival foods and everyday cooking. Additionally, expanding urban populations in these regions continue to sustain consistent commercial demand for goat-sourced offal products.

By Application Analysis

Fresh dominates with 67.9% due to strong consumer preference for unprocessed organ meats across global food markets.

In 2025, Fresh held a dominant market position in the By Application segment of the Edible Offal Market, with a 67.9% share. Fresh offal products reach consumers through food service outlets, traditional wet markets, and specialty butchers. Additionally, the fresh segment benefits from shorter supply chains in domestic and regional markets, ensuring product quality and consumer acceptance.

Processed offal encompasses canned and brine-preserved, frozen, sausage and bagged, and other value-added formats. Frozen offal has emerged as a key trade commodity, enabling long-distance international shipment. Moreover, sausage and bagged formats allow processors to combine offal with other ingredients, masking textural barriers that limit fresh consumption in markets with lower cultural familiarity.

By Distribution Channel Analysis

Wholesale Stores dominate with 29.3% due to high-volume purchasing by food processors and food service operators.

In 2025, Wholesale Stores held a dominant market position in the By Distribution Channel segment of the Edible Offal Market, with a 29.3% share. Wholesale buyers include large-scale food processors, restaurant chains, and institutional caterers who purchase in bulk. Moreover, wholesale distribution supports consistent pricing and reliable supply volumes for high-consumption markets.

Food Service channels represent a significant distribution avenue, driven by rising restaurant and catering demand for offal-inclusive menus. Retail outlets, including butchers and supermarkets, serve household consumers. Additionally, Online Sales platforms have gained momentum through specialty butcher subscriptions and curated offal box services. Hypermarkets and Supermarkets further serve mainstream shoppers seeking convenient packaged food options at accessible price points.

Key Market Segments

By Source

- Cattle

- Goat

- Pig

- Sheep

- Poultry

- Horse

- Others

By Application

- Fresh

- Human Food

- Animal/Pet Feed

- Others

- Processed

- Canned/Brine

- Frozen

- Sausage/Bagged

- Others

By Distribution Channel

- Wholesale Stores

- Food Service

- Retail

- Online Sales

- Hypermarkets/Supermarkets

- Others

Emerging Trends

Online Specialty Platforms and Social Media Drive Offal Discovery

Online specialty butcher platforms now offer curated offal subscription boxes, connecting niche consumers with premium organ meat products. Viral social media content featuring the preparation of the heart, tongue, and other lesser-known cuts builds awareness globally.

Moreover, celebrity chef campaigns actively demystify cooking techniques, drawing new consumer segments toward offal products. The United States exported $2.04 billion worth of edible offal, demonstrating strong commercial interest in global offal trade.

Keto and Carnivore Diet Movements Accelerate Organ Meat Consumption

Keto and carnivore diet communities increasingly center meal planning around nutrient-dense organ meats. Dedicated meal prep services now build entire product lines around liver, kidney, and heart-based blends. Consequently, these diet-driven consumer communities represent a fast-growing and commercially valuable segment for offal producers, processors, and online retailers worldwide.

Drivers

Nose-to-Tail Gastronomy and Premium Pet Food Drive Global Demand

Michelin-starred restaurants worldwide now feature nose-to-tail menus that spotlight organ meats as premium culinary ingredients. Meanwhile, the premium pet food segment rapidly expands its use of nutrient-dense organ meats in functional formulations. Tyson Foods reported total revenue of $53.31 billion for the full fiscal year ended September 2024, reflecting the scale of large meat processors that benefit from integrated offal utilization strategies.

Ancestral Diets and Waste Reduction Policies Strengthen Market Foundations

Mainstream health communities increasingly embrace ancestral and traditional diets that prioritize organ meat consumption for nutritional density. Additionally, industrial meat processors now face stringent government-mandated waste reduction targets across multiple jurisdictions. These regulatory pressures incentivize processors to develop higher-value applications for offal by-products rather than treating them as low-value residuals.

Restraints

Consumer Neophobia and Cultural Barriers Slow Western Market Growth

Entrenched consumer disgust and textural neophobia remain significant barriers to offal adoption across Western markets. Many consumers in North America and Northern Europe associate organ meats with unpleasant odors and unfamiliar textures. Consequently, mainstream retail channels struggle to position offal products attractively alongside conventional meat cuts without significant marketing investment.

Supply Chain Volatility Undermines Processor Confidence and Pricing Stability

Volatile raw material pricing and inconsistent supply chain performance for offal by-products challenge processor planning and margins. Danish Crown’s net profit for the 2024/25 financial year fell to DKK 788 million (approximately €105.5 million), a decline of more than 21%, partly reflecting cost and trade pressures that affect large integrated meat processors who handle significant offal volumes.

Growth Factors

Functional Food Innovation and Sports Nutrition Unlock New Revenue Streams

Processors now develop shelf-stable, flavor-masked offal-based functional snack foods that overcome traditional textural and sensory barriers. Strategic alliances with bodybuilding communities and elite athletic networks position organ meats as performance nutrition solutions. Indonesia imported 42,543 tonnes of Australian offal in 2024, accounting for 23% of total Australian offal exports, confirming strong institutional demand from large emerging markets.

Pharmaceutical Applications and Synthetic Biology Create Long-Term Value

Pharmaceutical manufacturers extract high-value bioactive compounds such as heparin directly from offal tissues, creating premium industrial demand beyond food channels. Moreover, cultivated and synthetic biology approaches to offal production attract ethical consumer segments who avoid conventional animal products. These emerging applications diversify market revenue and attract investment into offal-adjacent research and development pipelines globally.

Regional Analysis

Asia Pacific Dominates the Edible Offal Market with a Market Share of 48.1%, Valued at USD 22.3 Billion

Asia Pacific commands a 48.1% share of the global edible offal market, valued at USD 22.3 billion in 2025. The region’s culinary traditions across China, Vietnam, South Korea, Japan, and Southeast Asia deeply integrate organ meats into everyday cuisine. Moreover, large livestock processing industries in China and India generate substantial offal volumes that feed both domestic consumption and export markets.

North America sustains strong commercial demand for edible offal, driven by large-scale meat processing operations and growing interest in organ meats among health-focused consumer groups. The United States represents both a major exporter and importer of offal products. Additionally, the rise of carnivore and ancestral diet communities continues to expand domestic retail and online sales of organ meat products across the region.

Europe maintains a mature edible offal market underpinned by traditional culinary cultures in the United Kingdom, Spain, France, Germany, and Italy. Offal features prominently in sausage production, charcuterie, and traditional ethnic cuisines across the continent. However, shifting consumer preferences among younger demographics toward clean-label and plant-forward diets present moderate headwinds for conventional offal consumption in Western European markets.

The Middle East and Africa region demonstrates strong cultural and religious alignment with whole-animal consumption practices. Offal forms a central part of festive and everyday cooking across Gulf Cooperation Council countries, North Africa, and Sub-Saharan Africa. Saudi Arabia imported frozen edible offal of sheep, goats, and horses in 2024, confirming robust institutional and household demand across the Gulf region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ABP Food Group operates as one of Europe’s largest beef and lamb processing organizations, with deep expertise in whole-carcass utilization. The company sources livestock across Ireland and the United Kingdom and processes significant offal volumes for both domestic and international markets. ABP’s integrated processing model allows it to capture value across all carcass components, including high-demand offal categories such as liver, kidney, and tongue.

Allanasons Pvt. Ltd. stands as one of India’s leading exporters of halal-certified beef and buffalo offal products. The company serves large institutional buyers across the Middle East, Southeast Asia, and Africa. Allanasons combines vertically integrated processing with a strong logistics network, enabling reliable export volumes of frozen offal products. Additionally, the company’s halal certification opens access to premium markets with strict sourcing requirements.

Cargill Inc. participates in the edible offal market through its expansive global meat processing and protein supply chain operations. The company processes cattle, pigs, and poultry across multiple continents and distributes offal products through food service, industrial, and retail channels. Cargill’s research capabilities support product development in functional and value-added offal formats targeted at health-conscious and performance nutrition consumers.

Danish Crown Group ranks among Europe’s largest pork and beef processors, with offal handling integrated across its Danish, German, and UK operations. The company exports offal to markets in Asia, the Middle East, and the Americas. Reflecting the financial scale of its integrated meat processing activities, which encompass significant offal product streams alongside conventional cuts.

Top Key Players in the Market

- ABP Food Group

- Allanasons Pvt. Ltd.

- Alpha Field Products Co.

- Australian Agricultural Company (AACo)

- BRF S.A.

- Cargill Inc.

- Cenfood International Inc.

- Danish Crown Group

- Foyle Food Group

- Friboi

- Hormel Foods Corporation

- JBS Food Canada

- Kerry Group Plc.

- Marfrig Global Foods

- Minerva Foods

- NH Foods Ltd.

- Nippon Meat Packers Inc.

- Offal Cuisine

- Offal Delight

- Olymel L.P.

- Organic Meat Company

- Smithfield Foods Inc.

- Sure Good Foods Ltd.

- Tönnies Group

- Vion Food Group

- Yoma International

- Tyson Foods Inc.

Recent Developments

- In 2025, ABP Food Group is an Ireland/UK-based beef processor; developments relate to the broader meat sector, including potential by-products like edible offal. ABP Linden partnership showcase with Marks & Spencer on premium beef; workforce strike vote; and 338 jobs at risk from Dungannon retail packing cuts.

- In 2025, BRF S.A. CADE (Brazilian competition authority) cleared the BRF-Marfrig merger without restrictions, noting no major concerns in the fresh meat market. Ministry of Agriculture (Mapa) mission to the UAE highlighted BRF’s Abu Dhabi facility and export certification discussions.

Report Scope

Report Features Description Market Value (2025) USD 46.3 Billion Forecast Revenue (2035) USD 73.7 Billion CAGR (2026-2035) 4.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Cattle, Goat, Pig, Sheep, Poultry, Horse, Others), By Application (Fresh (Human Food, Animal/Pet Feed, Others), Processed (Canned/Brine, Frozen, Sausage/Bagged, Others)), By Distribution Channel (Wholesale Stores, Food Service, Retail, Online Sales, Hypermarkets/Supermarkets, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape ABP Food Group, Allanasons Pvt. Ltd., Alpha Field Products Co., Australian Agricultural Company (AACo), BRF S.A., Cargill Inc., Cenfood International Inc., Danish Crown Group, Foyle Food Group, Friboi, Hormel Foods Corporation, JBS Food Canada, Kerry Group Plc., Marfrig Global Foods, Minerva Foods, NH Foods Ltd., Nippon Meat Packers Inc., Offal Cuisine, Offal Delight, Olymel L.P., Organic Meat Company, Smithfield Foods Inc., Sure Good Foods Ltd., Tönnies Group, Vion Food Group, Yoma International, Tyson Foods Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- ABP Food Group

- Allanasons Pvt. Ltd.

- Alpha Field Products Co.

- Australian Agricultural Company (AACo)

- BRF S.A.

- Cargill Inc.

- Cenfood International Inc.

- Danish Crown Group

- Foyle Food Group

- Friboi

- Hormel Foods Corporation

- JBS Food Canada

- Kerry Group Plc.

- Marfrig Global Foods

- Minerva Foods

- NH Foods Ltd.

- Nippon Meat Packers Inc.

- Offal Cuisine

- Offal Delight

- Olymel L.P.

- Organic Meat Company

- Smithfield Foods Inc.

- Sure Good Foods Ltd.

- Tönnies Group

- Vion Food Group

- Yoma International

- Tyson Foods Inc.

Our Clients

- 181638

- March 2026