Quick Navigation

Report Overview

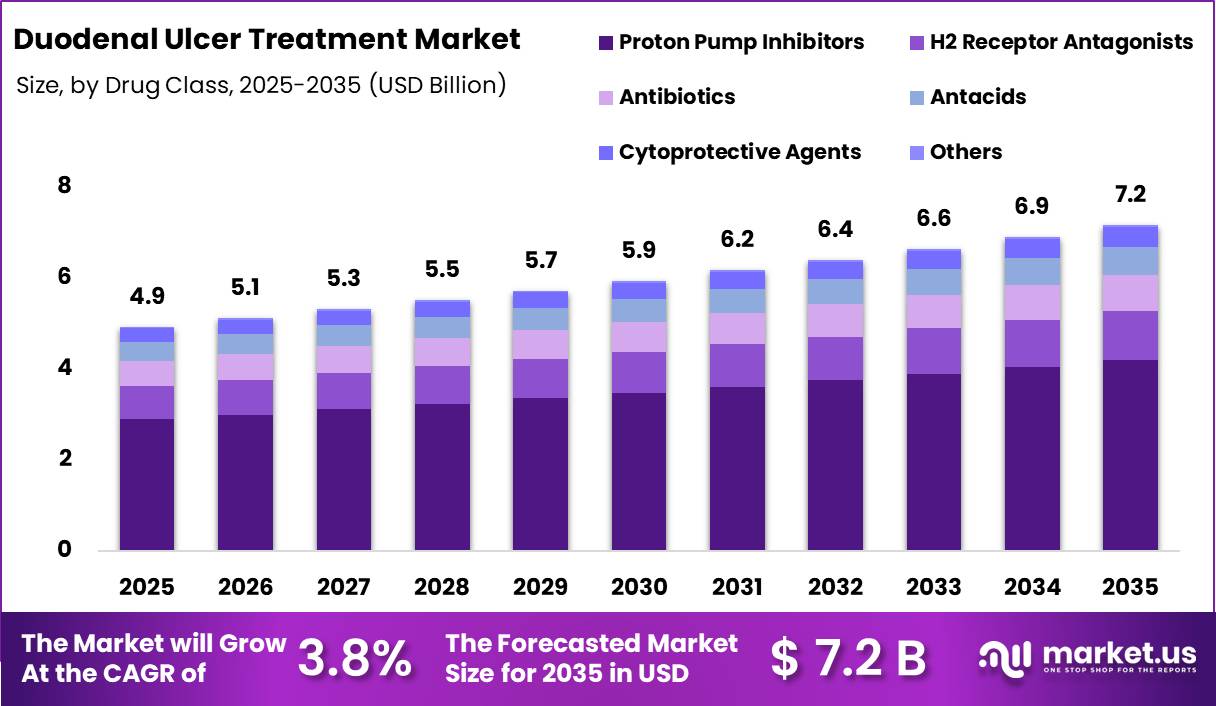

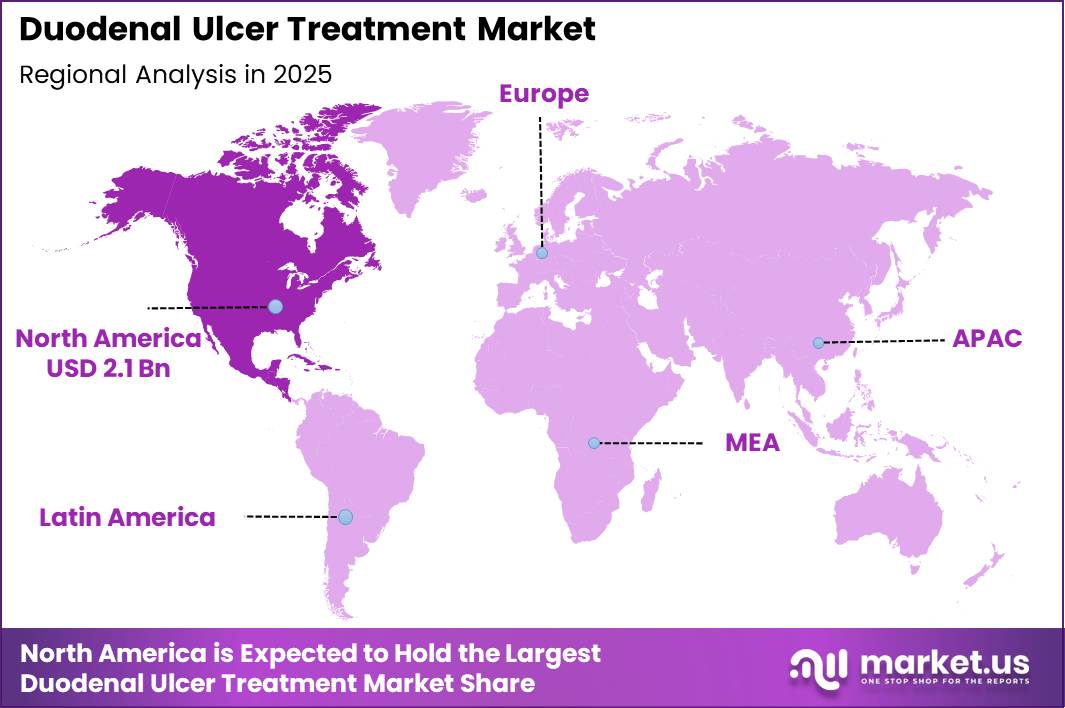

Global Duodenal Ulcer Treatment Market size is expected to be worth around US$ 7.2 Billion by 2035 from US$ 4.9 Billion in 2025, growing at a CAGR of 3.8% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 2.1 Billion.

The duodenal ulcer treatment market is driven by the continued global burden of peptic ulcer disease (PUD), increasing awareness of gastrointestinal disorders, and the widespread adoption of effective pharmacological therapies. Duodenal ulcers are open sores that develop in the lining of the duodenum, the first part of the small intestine, and represent one of the most common forms of peptic ulcer disease.

According to the U.S. National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), approximately 1% to 6% of the U.S. population is affected by peptic ulcers, with duodenal ulcers accounting for a significant proportion of cases.

The treatment landscape is primarily centered on addressing the underlying causes of the disease, particularly Helicobacter pylori (H. pylori) infection and prolonged use of nonsteroidal anti-inflammatory drugs (NSAIDs). The International Agency for Research on Cancer (IARC), a specialized agency of the World Health Organization (WHO), reports that approximately 95% of duodenal ulcers are associated with H. pylori infection, highlighting the importance of eradication therapies in disease management.

Current treatment approaches include proton pump inhibitors (PPIs), H2-receptor antagonists, antibiotics, and mucosal protective agents. The U.S. National Institutes of Health (NIH) recommends combination therapy consisting of two or more antibiotics alongside a proton pump inhibitor for H. pylori-positive patients to promote ulcer healing and prevent recurrence.

The increasing prevalence of gastrointestinal disorders among aging populations, growing NSAID consumption, and improved diagnostic capabilities such as endoscopy and non-invasive H. pylori testing continue to support demand for duodenal ulcer therapeutics.

Furthermore, advances in antimicrobial regimens aimed at overcoming antibiotic resistance are contributing to treatment optimization. According to clinical evidence reviewed by IARC, eradication therapy significantly reduces ulcer recurrence, with recurrence rates falling from approximately 64.4% to 12.9% in treated patients compared with untreated populations.

Overall, the duodenal ulcer treatment market remains an important segment of the gastrointestinal therapeutics industry, supported by ongoing clinical research, established treatment guidelines, and the persistent need for effective ulcer management and recurrence prevention.

Key Takeaways

- Market Size: Global Duodenal Ulcer Treatment Market size is expected to be worth around US$ 7.2 Billion by 2035 from US$ 4.9 Billion in 2025.

- Market Share: The market growing at a CAGR of 3.8% during the forecast period from 2026 to 2035.

- Drug Class Analysis: Proton Pump Inhibitors dominated the market, accounting for 58.6% of the total market share in 2025.

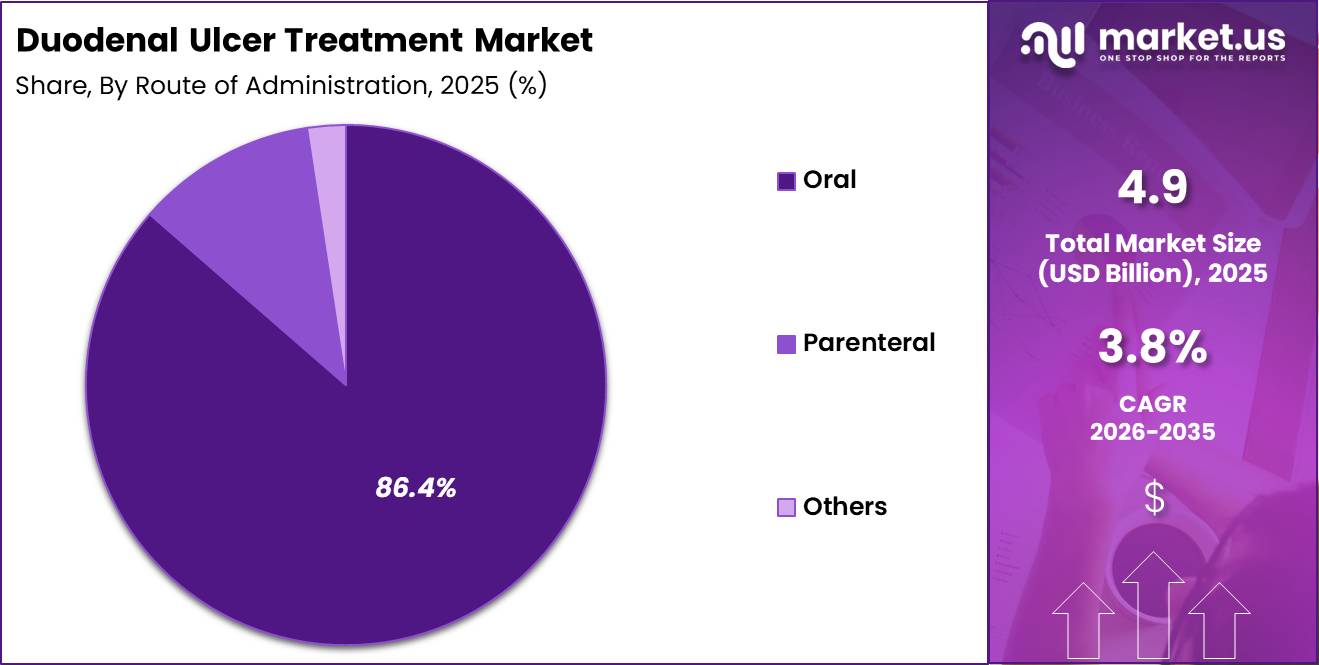

- Route of Administration Analysis: The Oral segment dominated the market with an 86.4% share in 2025.

- End User Analysis: Hospitals emerged as the leading segment, capturing 52.6% of the market share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 2.1 Billion.

Drug Class Analysis

The drug class segment of the Duodenal Ulcer Treatment Market is categorized into Proton Pump Inhibitors (PPIs), H2 Receptor Antagonists, Antibiotics, Antacids, Cytoprotective Agents, and Others. Proton Pump Inhibitors dominated the market, accounting for 58.6% of the total market share in 2025.

The strong position of PPIs is attributed to their superior efficacy in suppressing gastric acid secretion, promoting rapid ulcer healing, and reducing recurrence rates. Widely prescribed drugs such as omeprazole, pantoprazole, esomeprazole, and lansoprazole remain the preferred first-line therapies for duodenal ulcer management, particularly in patients with acid-related gastrointestinal disorders.

H2 Receptor Antagonists represent a significant segment due to their effectiveness in reducing stomach acid production and their use in patients who may not tolerate PPIs. Antibiotics hold an important share of the market owing to their critical role in the eradication of Helicobacter pylori infections, a major cause of duodenal ulcers.

Antacids continue to be utilized for immediate symptomatic relief, while Cytoprotective Agents support mucosal healing and protection. The Others segment includes combination therapies and emerging treatment options designed to enhance therapeutic outcomes and improve patient compliance.

Route of Administration Analysis

Based on route of administration, the Duodenal Ulcer Treatment Market is segmented into Oral, Parenteral, and Others. The Oral segment dominated the market with an 86.4% share in 2025. This dominance is primarily driven by the widespread availability of oral formulations, ease of administration, improved patient adherence, and cost-effectiveness.

Most commonly prescribed medications for duodenal ulcers, including proton pump inhibitors, H2 receptor antagonists, antibiotics, and antacids, are available in oral dosage forms, making them the preferred choice for both acute and long-term treatment. Oral therapies also enable convenient outpatient management, reducing the need for hospital-based interventions.

The Parenteral segment accounts for a smaller but important portion of the market. Injectable formulations are mainly utilized in hospitalized patients, severe ulcer cases, emergency settings, or situations where oral administration is not feasible. Intravenous proton pump inhibitors are frequently administered to manage complications and provide rapid acid suppression.

The Others segment includes alternative administration routes that are used in specific clinical circumstances. Continued advancements in drug formulation technologies and the growing preference for patient-friendly treatment options are expected to further strengthen the adoption of oral therapies across global healthcare systems.

End User Analysis

Based on end users, the Duodenal Ulcer Treatment Market is segmented into Hospitals, Specialty Clinics, Ambulatory Surgical Centers, and Others. Hospitals emerged as the leading segment, capturing 52.6% of the market share in 2025. The dominance of hospitals can be attributed to their comprehensive treatment capabilities, availability of advanced diagnostic technologies, and capacity to manage complex ulcer cases and associated complications.

Hospitals serve as primary treatment centers for patients requiring endoscopic evaluation, inpatient care, surgical intervention, or intensive monitoring, thereby generating substantial demand for duodenal ulcer therapeutics.

Specialty Clinics constitute a notable segment due to the increasing preference for specialized gastroenterology services. These facilities offer targeted diagnosis, personalized treatment plans, and follow-up care for patients with chronic gastrointestinal disorders, contributing to market growth.

Ambulatory Surgical Centers are gaining traction as healthcare systems increasingly adopt cost-effective and minimally invasive treatment approaches. These centers provide efficient outpatient procedures with shorter recovery times and reduced healthcare expenditures. The Others segment includes community healthcare centers, retail clinics, and home healthcare settings.

Rising awareness regarding gastrointestinal health, improved access to specialized care, and expanding healthcare infrastructure are expected to support growth across all end-user segments during the forecast period.

Key Market Segments

By Drug Class

- Proton Pump Inhibitors

- H2 Receptor Antagonists

- Antibiotics

- Antacids

- Cytoprotective Agents

- Others

By Route of Administration

- Oral

- Parenteral

- Others

By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Others

Market Dynamics

Driver – Growing NSAID Utilization and Increasing Gastrointestinal Disease Burden

The duodenal ulcer treatment market is primarily driven by the increasing use of nonsteroidal anti-inflammatory drugs (NSAIDs) and the rising burden of gastrointestinal disorders globally. The growing prevalence of chronic pain conditions, osteoarthritis, rheumatoid arthritis, and musculoskeletal disorders has contributed to sustained NSAID consumption, which remains a significant risk factor for duodenal ulcer development.

In addition, aging populations are more susceptible to ulcer-related complications due to long-term medication use and multiple comorbidities. Rising healthcare awareness, greater access to gastroenterology services, and increasing physician focus on ulcer prevention and management continue to support demand for effective therapeutic interventions across both developed and emerging healthcare markets.

Trend – Increasing Adoption of Resistance-Guided Treatment Approaches

A key trend shaping the duodenal ulcer treatment market is the growing adoption of resistance-guided treatment strategies aimed at improving eradication success rates and reducing treatment failures. Healthcare providers are increasingly incorporating follow-up testing and evidence-based treatment protocols to optimize clinical outcomes.

Advances in diagnostic technologies have improved the ability to identify treatment-resistant infections, supporting more personalized therapeutic decision-making. Additionally, antimicrobial stewardship initiatives are encouraging appropriate antibiotic selection and usage, while digital health tools are enhancing treatment monitoring, patient adherence, and long-term disease management. These developments are contributing to more effective and individualized duodenal ulcer care.

Restraint – Increasing Complexity of Treatment Management

A major challenge in the duodenal ulcer treatment market is the increasing complexity of treatment management resulting from evolving antimicrobial resistance patterns. Reduced effectiveness of commonly prescribed antibiotic regimens may require alternative treatment combinations, additional diagnostic testing, and prolonged therapy durations.

These factors can increase treatment costs and place additional burdens on healthcare systems and patients. Furthermore, recurrent disease, medication non-adherence, and variability in regional treatment practices can complicate clinical management and limit the standardization of care, potentially affecting overall treatment outcomes.

Opportunity – Development of Novel Therapeutics and Expansion in Emerging Markets

Significant growth opportunities exist through the development of next-generation ulcer therapeutics and expanding access to gastrointestinal healthcare services in emerging economies. Pharmaceutical companies are increasingly focused on innovative treatment approaches that improve efficacy, simplify treatment regimens, and address antimicrobial resistance concerns.

Expanding healthcare infrastructure, growing insurance coverage, and increasing availability of specialized diagnostic services in developing regions are expected to improve access to ulcer treatment. Additionally, the integration of telemedicine, remote patient monitoring, and digital healthcare platforms presents opportunities to enhance treatment adherence, follow-up care, and overall disease management, supporting future market expansion.

Regional Analysis

In 2025, North America dominated the global duodenal ulcer treatment market, accounting for over 42.5% of total market share and generating approximately US$ 2.1 billion in revenue. The region’s leadership is supported by a well-established healthcare infrastructure, high healthcare expenditure, and widespread access to advanced diagnostic and treatment options.

The increasing prevalence of Helicobacter pylori infections, the extensive use of nonsteroidal anti-inflammatory drugs (NSAIDs), and rising awareness regarding gastrointestinal disorders have contributed significantly to market growth. In addition, the strong presence of major pharmaceutical companies and ongoing research activities have facilitated the development and commercialization of effective proton pump inhibitors, antibiotics, and combination therapies for duodenal ulcer management.

The United States represents the largest contributor within the region due to its large patient population, favorable reimbursement policies, and high adoption of innovative therapeutics. Canada also contributes steadily, supported by increased screening initiatives and improved access to healthcare services.

Furthermore, the growing emphasis on early diagnosis and preventive care, along with advancements in endoscopic procedures, is expected to sustain market expansion across North America. The region’s robust healthcare ecosystem and continuous investment in gastrointestinal disease management are likely to maintain its leading position in the global duodenal ulcer treatment market over the forecast period.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The duodenal ulcer treatment market is characterized by the presence of several leading pharmaceutical companies focused on developing effective therapies for acid suppression, Helicobacter pylori eradication, and ulcer healing. Key market participants include AstraZeneca, Takeda Pharmaceutical Company Limited, Pfizer Inc., GlaxoSmithKline plc, Eisai Co., Ltd., and Abbott Laboratories. These companies maintain strong market positions through extensive product portfolios, robust distribution networks, and continuous investments in research and development.

Market participants are actively engaged in strategic initiatives such as product innovations, partnerships, acquisitions, and geographic expansion to strengthen their competitive presence. The increasing focus on advanced proton pump inhibitors (PPIs), combination therapies, and patient-friendly formulations has intensified competition within the market.

Furthermore, the growing availability of generic drugs has encouraged companies to differentiate their offerings through improved efficacy, safety profiles, and treatment outcomes. As demand for effective gastrointestinal disorder management continues to rise, leading players are expected to focus on innovation and clinical research to enhance their market share and maintain long-term growth.

Market Key Players

- AstraZeneca plc

- Pfizer Inc.

- GlaxoSmithKline plc

- Merck & Co., Inc.

- Takeda Pharmaceutical Company Limited

- Novartis AG

- Bayer AG

- Teva Pharmaceutical Industries Ltd.

- Mylan N.V. (Viatris)

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy’s Laboratories Ltd.

- Cipla Inc.

- Lupin Limited

- Hikma Pharmaceuticals PLC

- Abbott Laboratories

- Others

Recent Developments

- January 2026 – Takeda Pharmaceutical Company Limited announced a global collaboration and licensing agreement with Halozyme Therapeutics to utilize ENHANZE® drug-delivery technology for vedolizumab. The partnership is expected to strengthen Takeda’s gastroenterology franchise and enhance long-term delivery options for patients with gastrointestinal disorders.

- March 2026 – Lupin Limited entered into a licensing and supply agreement with Zydus Lifesciences for the co-marketing of innovative semaglutide injection products in India. The agreement expands Lupin’s specialty portfolio and demonstrates the company’s continued focus on strengthening its presence in chronic disease and gastrointestinal-related therapeutic markets.

- October 2025 – AstraZeneca plc signed an artificial intelligence-driven drug discovery partnership with Algen Biotechnologies valued at up to US$555 million. The agreement provides AstraZeneca with exclusive rights to develop therapies identified through Algen’s AI-enabled gene-editing platform, supporting the company’s broader strategy of accelerating next-generation therapeutic development.

- May 2025 – Sun Pharmaceutical Industries Ltd. disclosed plans to invest an additional US$100 million toward the commercialization and expansion of its specialty product pipeline in the United States. The investment is intended to strengthen the company’s specialty business and support future growth opportunities across advanced therapeutic segments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 4.9 Billion |

| Forecast Revenue (2035) | US$ 7.2 Billion |

| CAGR (2026-2035) | 3.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Class (Beta-blockers, Calcium Channel Blockers, Nitrates, Antiplatelet Agents, Ranolazine, Others) By Route of Administration (Oral, Sublingual, Intravenous, Topical, Others) By End User (Hospitals, Specialty Clinics, Homecare Settings, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | AstraZeneca plc, Pfizer Inc., GlaxoSmithKline plc, Merck & Co., Inc., Takeda Pharmaceutical Company Limited, Novartis AG, Bayer AG, Teva Pharmaceutical Industries Ltd., Mylan N.V. (Viatris), Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Cipla Inc., Lupin Limited, Hikma Pharmaceuticals PLC, Abbott Laboratories, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |