Global Drilling Fluid Market Size, Share, And Industry Analysis Report By Product (Water-based (WBF), Oil-based (OBF), Synthetic Based (SBF), Others), By Well Type (Conventional, HPHT), By End-Use (Onshore, Offshore), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 179958

- Number of Pages: 287

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

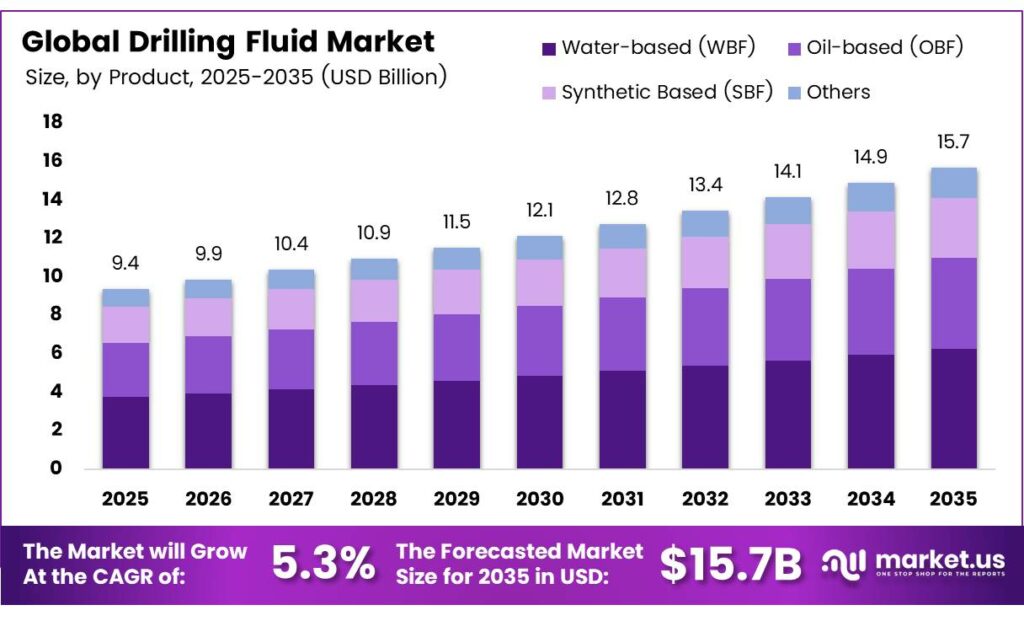

The Global Drilling Fluid Market size is expected to be worth around USD 15.7 billion by 2035 from USD 9.4 billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

Drilling fluids, also known as drilling muds, are specialized fluid systems used during the drilling of oil and gas wells. These fluids serve multiple functions, including cooling and lubricating the drill bit, removing drill cuttings, and maintaining wellbore stability. Consequently, they remain a critical input for every upstream drilling operation worldwide.

The market covers water-based, oil-based, and synthetic-based fluid systems used across onshore and offshore environments. Each fluid type addresses specific geological and operational requirements. Moreover, evolving well conditions, such as extreme pressures and temperatures, continue to push demand for advanced high-performance formulations across global exploration programs.

- U.S. oil and natural gas wells totalled 918,481 producing wells in 2024, while the share of horizontal wells increased from 10% in 2014 to 22% in 2024. This scale and evolving technology mix illustrates the substantial base of drilling activity that continuously requires fluid systems across U.S. basins.

Government energy policies and national upstream investment programs play a strong role in shaping drilling fluid demand. Countries across the Asia Pacific, the Middle East, and North America continue to expand their oil and gas exploration mandates. Additionally, regulatory frameworks around fluid disposal and environmental compliance are pushing operators toward greener and more efficient fluid chemistries.

- U.S. oil production averaged 13.4 million barrels per day in 2024, while natural gas gross withdrawals averaged 128.8 billion cubic feet per day in December 2024. This sustained high output reflects continued drilling and completion activity that directly underpins global demand for drilling fluid products and services.

The transition toward horizontal and directional drilling techniques has significantly increased fluid consumption per well. Operators now require more sophisticated fluid systems that maintain stability across longer lateral sections. Therefore, this technical shift creates sustained demand for premium fluid products, especially in unconventional shale and tight oil plays.

Key Takeaways

- The Global Drilling Fluid Market is valued at USD 9.4 billion in 2025 and is projected to reach USD 15.7 billion by 2035, at a CAGR of 5.3% during the forecast period 2026 to 2035.

- Water-based Fluids (WBF) dominate the market with a 52.5% share in 2025.

- Conventional wells lead the segment with a 78.2% market share in 2025.

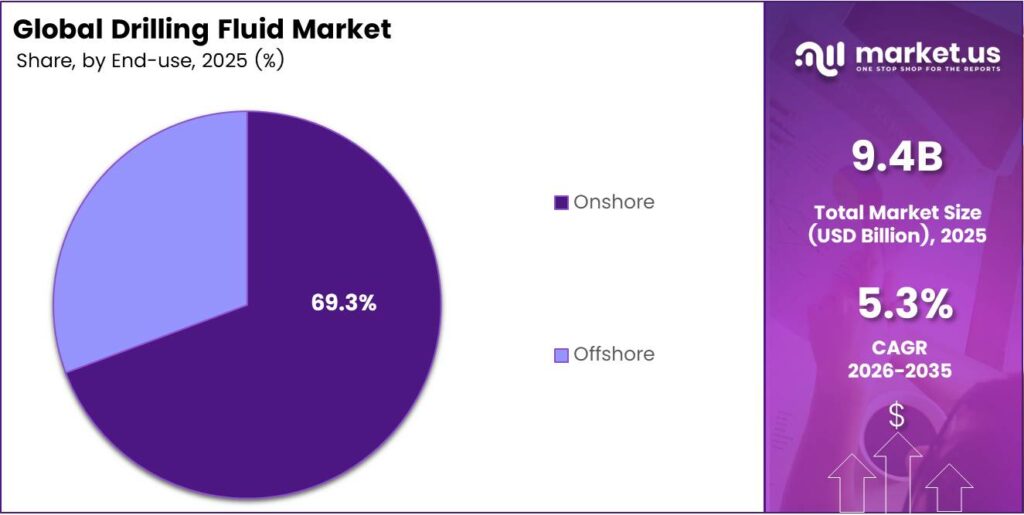

- Onshore applications hold the largest share at 69.3% in 2025.

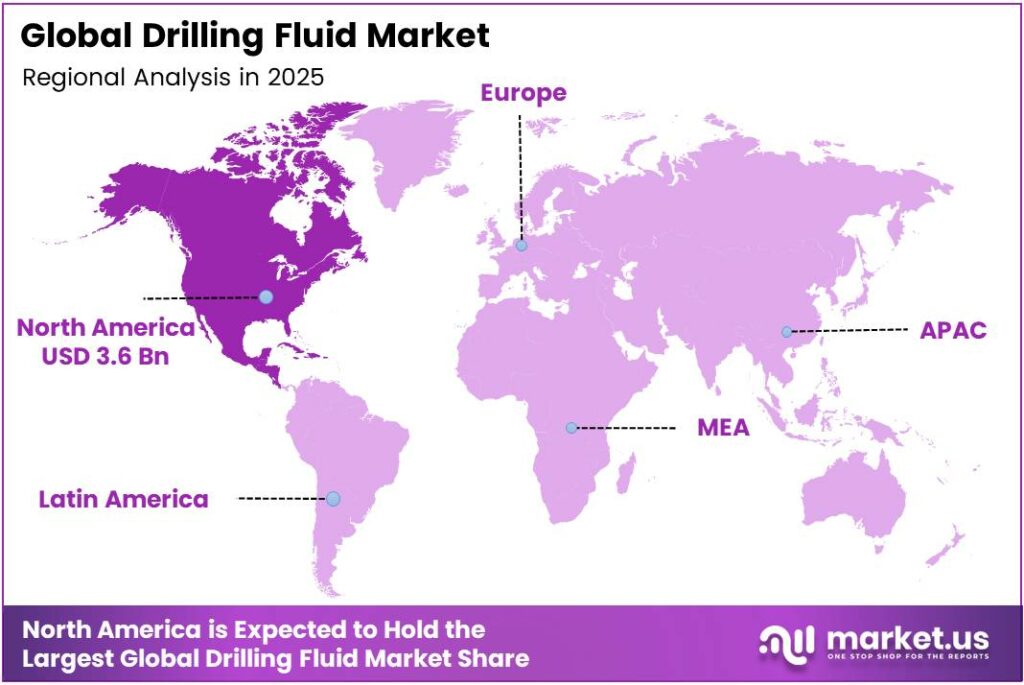

- North America dominates the regional market with a 38.1% share, valued at approximately USD 3.6 billion in 2025.

By Product Analysis

Water-based Fluids (WBF) dominate with 52.5% due to cost efficiency and environmental compliance advantages.

In 2025, Water-based Fluids (WBF) held a dominant market position in the By Product segment of the Drilling Fluid Market, with a 52.5% share. WBF systems attract operators because they are cost-effective, easy to treat, and align with tightening environmental regulations. Moreover, their versatility across onshore and shallow offshore formations makes them the go-to choice for a majority of global drilling programs.

Oil-based Fluids (OBF) serve high-demand applications where wellbore stability, lubrication, and shale inhibition are critical priorities. These fluids perform well in complex formations and deepwater environments. However, their higher cost and stricter disposal requirements limit adoption to technically demanding wells where performance requirements outweigh economic and regulatory concerns.

Synthetic-based Fluids (SBF) offer a performance-driven alternative that bridges the gap between OBF and WBF systems. Operators increasingly select SBF for offshore and environmentally sensitive areas where discharge restrictions apply. Additionally, SBF formulations deliver superior lubricity and thermal stability. The Others category includes specialty foams and air-based systems used in niche low-pressure or depleted reservoir applications.

By Well Type Analysis

Conventional wells dominate with 78.2% due to the large installed base of traditional vertical and deviated wells globally.

In 2025, Conventional wells held a dominant market position in the By Well Type segment of the Drilling Fluid Market, with a 78.2% share. The global oil and gas industry still operates a vast number of conventional vertical and deviated wells across mature basins. Consequently, routine drilling, workover, and maintenance activities in these formations generate steady and predictable demand for standard fluid systems.

High Pressure High Temperature (HPHT) wells represent a fast-growing niche where extreme downhole conditions demand specialized fluid formulations. These environments require fluids that maintain stability at temperatures above 150°C and pressures exceeding 10,000 psi. Therefore, HPHT drilling is a strong value driver for premium fluid manufacturers who develop advanced chemistries that outperform conventional fluid systems in these challenging reservoirs.

By End-Use Analysis

Onshore applications dominate with 69.3% due to the higher volume of land-based drilling activity worldwide.

In 2025, Onshore applications held a dominant market position in the By End-Use segment of the Drilling Fluid Market, with a 69.3% share. Land-based drilling dominates because of the large number of active shale, tight oil, and conventional wells across North America, the Middle East, and the Asia Pacific. Additionally, lower logistical costs and easier fluid handling on land support higher onshore fluid consumption volumes.

Offshore applications account for the remaining share and represent a high-value segment within the global drilling fluid industry. Deepwater and ultra-deepwater projects require technically sophisticated fluid systems that can withstand extreme hydrostatic pressures and low seabed temperatures. Moreover, the push toward new offshore discoveries in West Africa, Southeast Asia, and the Gulf of Mexico continues to expand offshore fluid demand over the forecast period.

Key Market Segments

By Product

- Water-based (WBF)

- Oil-based (OBF)

- Synthetic Based (SBF)

- Others

By Well Type

- Conventional

- HPHT

By End-Use

- Onshore

- Offshore

Emerging Trends

Environmental Compliance and Digital Innovation Reshape Drilling Fluid Technologies

Operators across global markets are shifting toward water-based and synthetic-based fluids that meet stricter environmental standards. Regulatory pressure in offshore zones and onshore sensitive areas is accelerating this transition. Moreover, fluid suppliers are reformulating product lines to reduce toxicity, improve biodegradability, and ensure compliance with local discharge regulations across all major drilling regions.

Nanoparticle-enhanced drilling fluids are gaining traction as a next-generation technology for improving lubrication, filtration control, and borehole stability. These advanced formulations offer superior performance in complex geological formations. Nanoparticle additives help reduce fluid losses and extend drill bit life, making them increasingly attractive for operators drilling in HPHT and deepwater environments.

Digital transformation is reshaping how operators manage drilling fluid systems in real time. Smart fluid management platforms use sensor data and AI algorithms to monitor fluid properties and optimize performance during drilling. Consequently, these technologies reduce non-productive time and improve wellbore quality. The adoption of intelligent fluid systems reflects a broader industry push toward data-driven drilling operations.

Drivers

Expanding Upstream Oil and Gas Operations Drive Sustained Drilling Fluid Demand

Global upstream oil and gas companies continue to expand their drilling programs across conventional and unconventional resource plays. Rising energy demand and strategic energy security initiatives push national oil companies and independents to accelerate exploration. Halliburton Drilling and Evaluation segment revenue reached USD 9,693 million in 2024, up from USD 9,222 million in 2023, reflecting sustained drilling activity that directly fuels fluid consumption.

Surging shale gas production and gas-fired power generation requirements are creating additional demand for drilling fluids in North America and other unconventional basins. Hydraulic fracturing and horizontal drilling programs require large volumes of customized fluid systems. Moreover, natural gas infrastructure buildout in Asia and Europe is encouraging more aggressive upstream drilling campaigns that require advanced fluid solutions across diverse geological settings.

Rapid growth in offshore and deepwater hydrocarbon exploration is another powerful driver for the drilling fluid market. Energy companies are targeting new reserves in technically challenging deepwater blocks across the Gulf of Mexico, West Africa, and Southeast Asia. Consequently, these complex environments demand high-performance fluid systems that can withstand extreme pressure, temperature, and wellbore stability challenges throughout the drilling process.

Restraints

Oil Price Volatility and Environmental Regulations Constrain Drilling Fluid Market Growth

Persistent volatility in global crude oil and natural gas prices remains the most significant restraint on drilling fluid demand. Operators reduce exploration budgets when commodity prices decline sharply, leading to fewer new well starts and lower fluid consumption. EU crude oil production fell to a record low of 15.5 million tonnes in 2023, reflecting how mature market contraction further limits European fluid demand.

Stringent environmental regulations governing fluid composition, handling, and disposal impose significant compliance costs on operators and fluid manufacturers. Offshore discharge restrictions and onshore waste management rules require expensive treatment systems and reformulated fluid chemistries. However, these regulations also create opportunities for suppliers who can offer compliant, low-toxicity alternatives that meet evolving regulatory standards without sacrificing drilling performance.

High formulation and logistics costs associated with advanced oil-based and synthetic-based fluid systems limit adoption among cost-sensitive operators. Smaller independent drilling companies often lack the capital to invest in premium fluid technologies. Therefore, price sensitivity in emerging markets slows the uptake of high-performance fluids, keeping a large portion of global drilling activity reliant on lower-cost water-based systems with limited technical capabilities.

Growth Factors

Biodegradable Formulations and Deepwater Investments Accelerate Market Expansion

Development of biodegradable and low-toxicity drilling fluid formulations presents a major commercial opportunity for suppliers targeting environmentally regulated markets. Companies that invest in green chemistry research can capture premium pricing in offshore and onshore sensitive zones. India drilled 741 oil and gas wells in FY 2023-24, including 132 exploratory wells, illustrating the active Asian upstream pipeline that demands modern fluid solutions.

- Rising investments in ultra-deepwater and complex reservoir exploration are expanding the addressable market for advanced drilling fluid systems. Energy majors are committing multi-billion-dollar programs to access new reserves in technically demanding offshore blocks. Additionally, NOV Inc. reported 2024 Adjusted EBITDA rising 11% to USD 1.11 billion, reflecting strong revenue growth across the oilfield services value chain driven by increased drilling equipment and fluid management activity.

Integration of AI-enhanced fluid management systems enables real-time optimization of fluid properties during drilling operations. These platforms reduce fluid waste, minimize non-productive time, and improve wellbore quality across complex well profiles. Moreover, expansion of solid waste management and borehole stability solutions adds value for operators seeking to reduce total well costs while maintaining compliance with increasingly demanding environmental and operational performance standards.

Regional Analysis

North America Dominates the Drilling Fluid Market with a Market Share of 38.1%, Valued at USD 3.6 Billion

North America leads the global drilling fluid market, holding a 38.1% share valued at approximately USD 3.6 billion in 2025. The United States drives this dominance through its large-scale shale and tight oil drilling programs across the Permian Basin, Eagle Ford, and Bakken formations. Moreover, Canada’s oil sands and unconventional gas plays contribute additional fluid demand, reinforcing North America as the single largest regional consumer of drilling fluid products worldwide.

Europe maintains a moderate but stable presence in the global drilling fluid market. The North Sea remains the primary hub for offshore drilling activity, with the UK and Norway operating active exploration and production programs. However, declining onshore production across EU member states and tight environmental regulations constrain overall fluid consumption growth. The region increasingly favors synthetic and water-based fluid systems that meet offshore discharge standards.

Asia Pacific represents the fastest-growing region for drilling fluid demand, driven by expanding upstream programs in China, India, Australia, and Southeast Asia. National oil companies in the region are accelerating both onshore and offshore exploration campaigns. Additionally, India’s active well-drilling program and China’s deepwater ambitions in the South China Sea create strong long-term demand for advanced fluid formulations across diverse geological environments.

The Middle East and Africa region holds a significant share of global drilling fluid consumption, anchored by high-volume drilling activity in Saudi Arabia, the UAE, Iraq, and Kuwait. State-owned energy companies in the Gulf Cooperation Council continue to invest heavily in oilfield development and enhanced recovery programs. Furthermore, sub-Saharan Africa’s growing offshore exploration sector in Nigeria, Angola, and Mozambique adds incremental demand for offshore-grade fluid systems.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Baker Hughes, Inc. is a leading global oilfield technology and services company with a strong portfolio across drilling fluids and completion solutions. Its Oilfield Services and Equipment segment, which includes drilling and completion fluid services, contributed the bulk of this expansion, reflecting strong international drilling demand.

Halliburton, Inc. is one of the world’s largest providers of products and services to the energy industry, with deep expertise in drilling fluid engineering. The company operates an extensive global network that supports both onshore and offshore drilling programs. Halliburton continues to invest in fluid technology innovation and digital solutions that help operators improve wellbore quality and reduce total drilling costs across complex well environments.

Newpark Resources, Inc. focuses specifically on drilling and completion fluid systems, giving it a specialized market position in the global oilfield services industry. The company’s Fluids Systems segment delivers tailored water-based, oil-based, and synthetic fluid programs for diverse geological environments. Newpark continues to expand its service capabilities in North America and select international markets, emphasizing technical differentiation and environmental compliance in its product development strategy.

Schlumberger Ltd. (SLB) represents a 10% year-over-year increase driven by robust international drilling and exploration activity. SLB’s well construction and drilling fluid-related technologies form a core part of its value proposition to global operators. The company actively integrates digital and AI capabilities into its fluid management platforms, positioning itself at the forefront of smart drilling fluid optimization globally.

Top Key Players in the Market

- Baker Hughes, Inc.

- CES Energy Solutions Corp.

- Halliburton, Inc.

- Newpark Resources, Inc.

- Petrochem Performance Chemical Ltd. LLC

- Schlumberger Ltd.

- Scomi Group Bhd

- Weatherford International

- Chevron Phillips Chemical Company

- BASF SE

- DuPont

- Dow

Recent Developments

- In 2025, Halliburton signed an MOU with PT Pertamina (Persero) to accelerate the adoption of advanced well-construction and stimulation technologies in Indonesia. The agreement covers evaluation of multi-stage hydraulic fracturing, acid stimulation, advanced cementing services, closed-loop automation, and AI to improve drilling and fracturing performance in onshore fields.

- In 2025, CES highlighted record drilling-fluids market share: 26% in the US (Q3 and nine months, up from 22% in 2024) and 42% in Canada for Q3 (40% for nine months, up from 35%/33%). The company cited “growing demand for increasingly complex drilling fluids and production chemical technology requirements” amid high service intensity.

Report Scope

Report Features Description Market Value (2025) USD 9.4 Billion Forecast Revenue (2035) USD 15.7 Billion CAGR (2026-2035) 5.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Water-based (WBF), Oil-based (OBF), Synthetic-based (SBF), Others), By Well Type (Conventional, HPHT), By End-Use (Onshore, Offshore) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Baker Hughes Inc., CES Energy Solutions Corp., Halliburton Inc., Newpark Resources Inc., Petrochem Performance Chemical Ltd., Schlumberger Ltd., Scomi Group Bhd, Weatherford International, Chevron Phillips Chemical Company, BASF SE, DuPont, Dow Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Baker Hughes, Inc.

- CES Energy Solutions Corp.

- Halliburton, Inc.

- Newpark Resources, Inc.

- Petrochem Performance Chemical Ltd. LLC

- Schlumberger Ltd.

- Scomi Group Bhd

- Weatherford International

- Chevron Phillips Chemical Company

- BASF SE

- DuPont

- Dow

Our Clients

- 179958

- March 2026