Quick Navigation

Report Overview

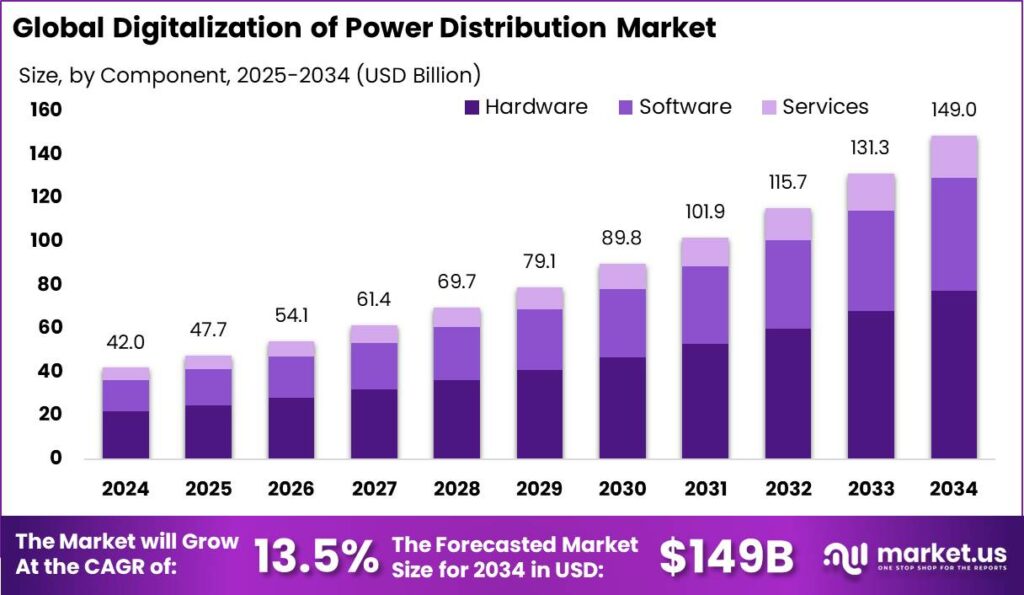

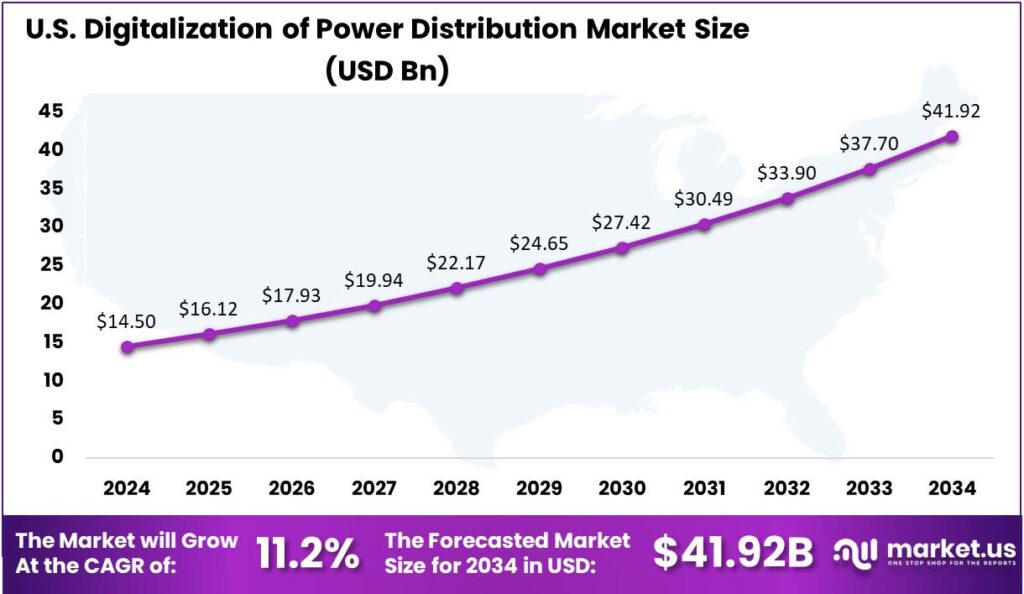

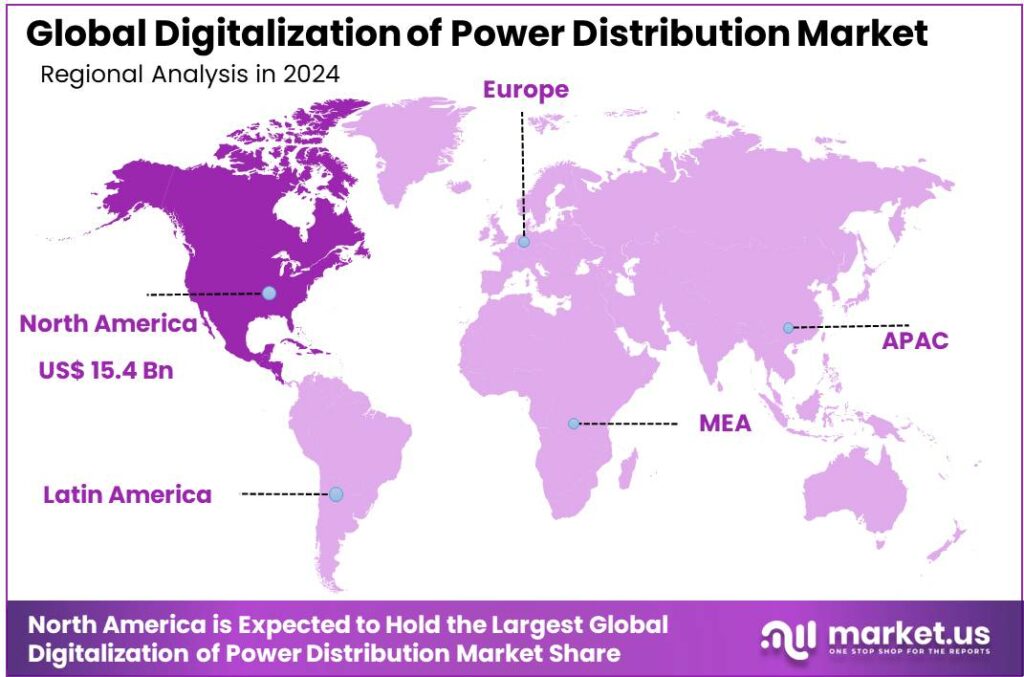

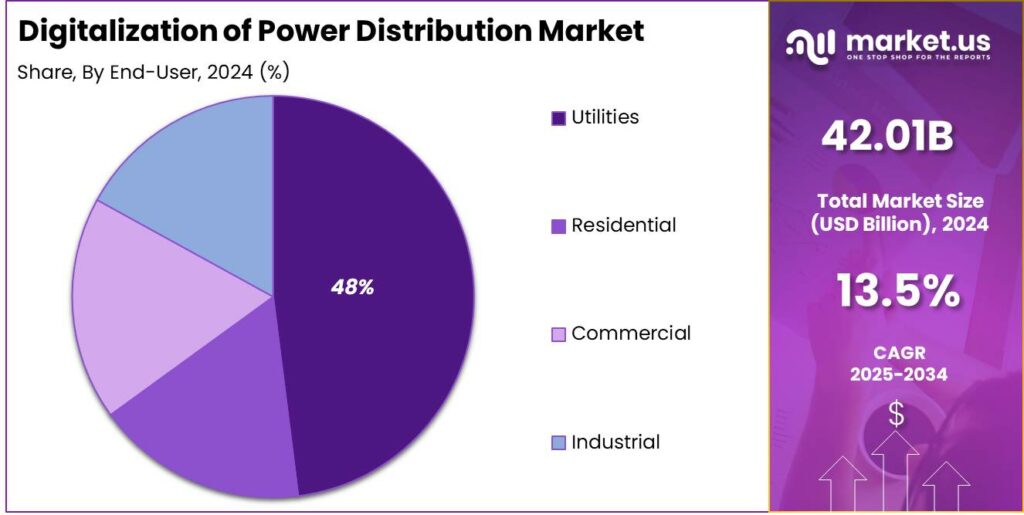

The Global Digitalization of Power Distribution Market size is expected to be worth around USD 149 Billion By 2034, from USD 42.01 Billion in 2024, growing at a CAGR of 13.50% during the forecast period from 2025 to 2034. In 2024, North America dominated the digitalization of power distribution market with over 36.7% market share, translating to USD 15.4 billion in revenue. The U.S. market was valued at USD 14.5 billion, growing at a CAGR of 11.2%.

Digitalization of power distribution refers to the integration of advanced digital technologies into the electrical distribution network. This transformation uses smart sensors, automated systems, and data analytics to optimize electricity flow, enhancing grid monitoring, reliability, and the integration of renewable energy while reducing outages.

Primary growth factors driving the digitalization of the power distribution market include advancements in technologies like the Internet of Things (IoT) and artificial intelligence (AI), which enhance grid efficiency and responsiveness. The rise of renewable energy requires smarter grids to handle fluctuating inputs, while growing electricity demand, especially in developing regions, drives investments in digital infrastructure for reliable power delivery.

Businesses stand to benefit from the digitalization of power distribution through improved operational efficiency, reduced maintenance costs, and enhanced customer satisfaction. Advanced analytics and predictive maintenance capabilities allow for proactive management of grid assets, minimizing downtime and extending equipment life.

The regulatory environment is evolving to support the digitalization of power distribution. Policies promoting renewable energy and reducing carbon emissions are driving utilities to invest in digital technologies. Updated regulatory frameworks address cybersecurity and data privacy, crucial for the connected energy landscape.

The opportunities in this space are vast, from data-driven grid management platforms to mobile apps for real-time consumption tracking. Companies focused on cybersecurity, AI-based fault detection, and local job creation for smart grid infrastructure are well-positioned. Additionally, developing countries seek affordable digital solutions for resilient grids, opening new markets and partnerships.

Key factors driving this market include rising demand for reliable, sustainable energy, the need for grid modernization, and a focus on energy efficiency. These trends are prompting utilities and governments to prioritize digital infrastructure investments to meet energy transition goals and improve power system resilience.

Key Takeaways

- The Global Digitalization of Power Distribution Market is projected to grow from USD 42.01 billion in 2024 to USD 149 billion by 2034, reflecting a CAGR of 13.50% during the forecast period from 2025 to 2034.

- In 2024, the Advanced Metering Infrastructure (AMI) segment held a dominant market position, capturing more than 22% of the digitalization of power distribution market.

- In 2024, the Hardware segment held a dominant market share, accounting for more than 52% of the digital power distribution market.

- In 2024, the Utilities segment dominated the digitalization of power distribution market, capturing more than 48% of the market share.

- In 2024, North America held a dominant position in the digitalization of power distribution market, capturing more than 36.7% of the market share, which equated to a market revenue of approximately USD 15.4 billion.

- The U.S. Digitalization of Power Distribution Market was valued at USD 14.5 billion in 2024, with a CAGR of 11.2%.

Business Benefits

Digitalization facilitates the incorporation of renewable energy sources like solar and wind into the power grid. Smart grids can manage the variability of these sources, ensuring a consistent energy supply. This not only promotes cleaner energy but also helps in achieving sustainability goals by reducing reliance on fossil fuels.

Integrating digital technologies enables power companies to monitor energy flows in real time, improving demand forecasting, load balancing, and enabling cost-saving predictive maintenance by identifying issues before failures occur. According to the report by AVEVA, Power plants that adopt digital solutions can cut major costs like fuel by 28%, maintenance by 20%, and operations by 19.5%.

Digital meters and user-friendly platforms provide consumers with clear insights into their energy use, enabling informed decisions and potential savings. Utilities can also deliver personalized services and pricing, enhancing customer satisfaction and engagement.

Impact Of AI

- Smarter Grid Management: AI helps power grids become more intelligent by analyzing vast amounts of data to predict energy demand and supply patterns. This enables utilities to balance electricity flow more effectively, reducing waste and improving reliability.

- Predictive Maintenance: Instead of waiting for equipment to fail, AI can forecast potential issues by monitoring system performance. This proactive approach allows for timely maintenance, minimizing downtime and enhancing service continuity.

- Enhanced Renewable Integration: AI facilitates the integration of renewable energy sources like solar and wind into the power grid. By forecasting weather patterns and energy production, AI ensures a stable and efficient energy supply.

- Improved Energy Forecasting: AI algorithms can accurately predict energy consumption trends, helping utilities plan and allocate resources more efficiently. This leads to cost savings and better energy management.

- Strengthened Grid Security: With the increasing threat of cyberattacks, AI enhances the security of power distribution networks by detecting and responding to anomalies in real-time, safeguarding critical infrastructure.

U.S. Market Leadership

The digitalization of power distribution in the U.S. has emerged as a transformative shift in how electricity is monitored, managed, and delivered across the nation. In 2024, this market was valued at USD 14.5 billion, highlighting strong momentum in the adoption of digital technologies within the power grid. Digital power distribution integrates advanced software, smart sensors, cloud-based analytics, and automation to improve grid reliability, minimize losses, and enhance real-time decision-making.

Reflecting this growth trajectory, the U.S. digitalization of power distribution market is expanding at a compound annual growth rate (CAGR) of 11.2%. Rising electricity demand, aging infrastructure, and sustainability mandates are driving the market. Utilities are adopting digital substations, automated fault detection, and predictive maintenance to boost efficiency and reduce downtime.

The growing pace highlights a strong demand for innovation from both public and private utilities. Major investments are being made in smart grids, advanced metering infrastructure (AMI), and cybersecurity to protect data-driven operations. As climate and grid reliability challenges increase, the shift to digital power distribution is crucial for advancing the U.S. toward a smarter, cleaner, and more resilient energy future.

In 2024, North America held a dominant market position, capturing more than 36.7% share, which translated to a market revenue of approximately USD 15.4 billion. This leadership is primarily driven by the region’s mature utility infrastructure, aggressive smart grid initiatives, and widespread adoption of advanced digital technologies.

The U.S., in particular, has heavily invested in grid modernization programs, smart metering systems, and the integration of renewable energy sources. With consistent support from federal and state-level policies, utilities in the region are accelerating digital transformation to enhance reliability, reduce operational costs, and meet stringent carbon reduction goals.

The market is driven by decentralization and real-time energy flow optimization, particularly with the growth of renewable energy. Digital twins and IoT devices are rapidly deployed to monitor infrastructure health and improve demand forecasting. The region has captured a significant portion of the global market, with continued growth fueled by regulatory mandates for grid flexibility and cross-border energy trading.

The Asia-Pacific region is rapidly digitalizing power distribution, driven by urbanization and industrial growth, especially in China, India, and South Korea. China leads with its “New Infrastructure” strategy, focusing on AI, 5G, and smart grids. In Latin America, digitalization is slower, with efforts to improve grid efficiency and combat power theft, supported by regulatory reforms and privatization.

Technology Analysis

In 2024, Advanced Metering Infrastructure (AMI) segment held a dominant market position, capturing more than a 22% share of the digitalization of power distribution market. This leadership is largely driven by the growing global focus on energy efficiency, real-time consumption monitoring, and accurate billing.

AMI systems enable utilities to collect, analyze, and respond to energy usage data remotely, reducing manual labor and enhancing service reliability. As utilities strive to meet evolving consumer expectations and regulatory demands, the demand for smart meters and two-way communication technologies continues to surge, solidifying AMI’s role as a central pillar of smart grid development.

The Distribution Management System (DMS) is gaining traction for enhancing efficiency in distribution networks with real-time data, outage management, and fault detection. However, its adoption is slower than AMI due to integration challenges and high initial costs, particularly in emerging markets. Still, DMS adoption is expected to accelerate as global grid reliability becomes a key focus.

SCADA systems and Substation Automation are crucial for modernizing power distribution by enabling remote monitoring and quick decision-making in wide-area networks. However, SCADA faces competition from AI-driven platforms, and the adoption of substation automation is often limited by the constraints of legacy equipment in older grids.

Component Analysis

In 2024, the Hardware segment held a dominant market position, capturing more than 52% of the digital power distribution market. This lead is primarily due to the massive infrastructure upgrades undertaken by utility providers globally, aiming to modernize aging grids.

Hardware components like smart meters and intelligent electronic devices (IEDs) are critical for capturing real-time data and automating grid operations. Their deployment has surged as governments and private players alike focus on energy efficiency, real-time monitoring, and reducing technical losses in transmission and distribution networks.

Smart meters, in particular, are the backbone of digital power systems. They allow two-way communication between consumers and utility providers, enabling accurate billing and consumption analysis. The push for transparent and efficient billing in both developed and emerging economies has significantly boosted their installation.

Software solutions like analytics platforms and energy management systems are essential but typically follow the deployment of hardware. Utilities need to install devices that collect and transmit data before leveraging it for insights. Real-time hardware feedback is crucial for software to function effectively. This explains why hardware leads in adoption and revenue, especially with government-backed grid modernization efforts.

End-User Analysis

In 2024, the Utilities segment held a dominant position in the digitalization of power distribution market, capturing more than 48% share. This dominance is largely due to utilities being at the center of national power grids and responsible for managing large-scale energy distribution.

The industrial sector is growing due to rising demand for reliable, high-quality power in manufacturing, oil and gas, and data centers. As operations expand and automate, industries are adopting advanced distribution management systems (ADMS) to track energy use, prevent outages, and reduce costs. Though not as dominant as utilities, industries are quickly seeing the ROI from predictive maintenance and real-time fault detection through digital systems.

The commercial sector, including offices, malls, hospitals, and schools, is adopting digital power distribution to boost energy efficiency and reduce costs. Smart infrastructure allows for monitoring energy use, controlling HVAC systems, and automating lighting. This trend is growing as property owners pursue green certifications and digital upgrades to meet sustainability goals and appeal to tenants seeking lower operating expenses.

Meanwhile, the residential segment is gradually adopting digitalization, particularly in urban areas and smart home environments. While it holds a smaller share compared to other sectors, growth is steady, thanks to the rising adoption of smart meters, home energy management systems, and rooftop solar integration.

Key Market Segments

By Technology

- Advanced Metering Infrastructure (AMI)

- Distribution Management System (DMS)

- Supervisory Control and Data Acquisition (SCADA)

- Substation Automation

- Energy Management Systems (EMS)

- Remote Terminal Units (RTU)

- Communication Infrastructure (Fiber, RF Mesh, Cellular)

By Component

- Hardware

- Smart Meters

- Intelligent Electronic Devices (IEDs)

- Sensors and Actuators

- Communication Devices

- Software

- Analytics Platforms

- Grid Monitoring Software

- Energy Management Software

- Services

- Consulting & Integration

- Maintenance & Support

- Managed Services

By End-User

- Residential

- Commercial

- Industrial

- Utilities

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Enhancing Grid Efficiency and Reliability

Digitalization is transforming power distribution by enabling smarter, more responsive grids. Through technologies like smart meters, sensors, and real-time analytics, utilities can monitor and manage electricity flow more effectively.

Digital tools enable faster fault detection, reduced outages, and optimized energy distribution. The IEA highlights their role in balancing supply and demand, especially with renewable energy sources. Digitalization also supports predictive maintenance, reducing downtime and extending infrastructure lifespan. Consumers benefit from accurate billing and real-time energy usage monitoring, promoting conservation.

Restraint

High Implementation Costs

While the benefits of digitalizing power distribution are clear, the initial investment required poses a significant barrier. Upgrading infrastructure with smart technologies, training personnel, and ensuring cybersecurity measures demand substantial financial resources.

Integrating new digital systems with legacy infrastructure is complex and costly, with interoperability challenges between different technologies and vendors. These technical and organizational barriers can hinder digital solution adoption in power distribution. While digitalization promises long-term savings and efficiency, the high upfront costs and integration issues can slow adoption, especially for smaller utilities or those in developing regions, where such costs can be prohibitive.

Opportunity

Integration of Renewable Energy Sources

Digitalization presents a significant opportunity to integrate renewable energy sources into the power grid effectively. With the rise of decentralized energy generation, such as rooftop solar panels and wind turbines, managing the variability and distribution of power becomes complex.

Digital tools enable real-time monitoring and control, facilitating the integration of renewable energy sources. Advanced analytics and forecasting help utilities predict renewable energy production and adjust supply, ensuring grid stability and maximizing clean energy use. Digitalization enhances the flexibility and resilience of power distribution systems, supporting the global shift to sustainable energy and improving grid reliability.

Challenge

Cybersecurity Risks

As power distribution systems become more digitalized, they also become more vulnerable to cyber threats. The increased connectivity and reliance on digital technologies open up potential entry points for malicious attacks.

Robust cybersecurity measures are essential to protect critical infrastructure, including secure communication protocols, regular system updates, and employee training on best practices. Collaboration between utilities, technology providers, and government agencies is key to developing standardized security frameworks. Addressing cybersecurity challenges is vital to maintaining trust in digital power distribution systems and ensuring a continuous, reliable electricity supply.

Emerging Trends

Power distribution is undergoing a significant shift, embracing digital technologies to enhance efficiency and reliability. One notable trend is the integration of the Internet of Things (IoT), which connects devices across the grid, allowing for real-time monitoring and control. This connectivity enables utilities to detect issues promptly and optimize energy flow.

Artificial Intelligence (AI) and machine learning are also playing a crucial role. These technologies analyze vast amounts of data to predict demand patterns, identify potential faults, and suggest maintenance schedules, thereby reducing downtime and improving service quality.

Another emerging trend is the use of digital twins virtual replicas of physical systems. They provide a dynamic model of the power grid, enabling operators to simulate scenarios, test responses, and plan upgrades without affecting the actual infrastructure. Additionally, the adoption of smart grids is facilitating two-way communication between utilities and consumers.

Key Player Analysis

Key players in this market are investing heavily in innovation, developing digital tools and platforms that bring intelligence to power distribution systems.

Schneider Electric is one of the top leaders in the digital power distribution space. Schneider is renowned for its energy management and automation solutions, particularly its EcoStruxure platform. This innovative platform integrates IoT, cloud computing, and analytics to optimize energy usage, enabling smarter decisions, improved efficiency, and reduced downtime across industries.

Siemens AG is another key player bringing advanced digital solutions to the power distribution market. With its deep expertise in industrial automation and electrification, Siemens offers smart grid technologies that enable real-time data monitoring and predictive maintenance. Their digital grid solutions help utilities and industries better manage load, prevent outages, and ensure grid stability.

ABB Ltd. stands out for its digital innovation in power and automation technologies. ABB’s Ability platform is central to its digital strategy, offering cloud-connected devices and services that enhance visibility and control over electrical systems. ABB’s strength lies in its ability to deliver customized solutions for different sectors, including utilities, transport, and infrastructure.

Top Key Players in the Market

- Schneider Electric

- Siemens AG

- ABB Ltd.

- General Electric (GE) Digital

- Eaton Corporation

- Honeywell International Inc.

- Cisco Systems, Inc.

- Oracle Corporation

- IBM Corporation

- Landis+Gyr

- Hitachi

- Legrand

- CHINT

- Others

Top Opportunities for Players

Digitalizing power distribution is creating major opportunities, with smart technologies driving innovation in grid automation, data analytics, and system efficiency.

- Smart Grids and Real-Time Monitoring: The integration of smart grids equipped with sensors and digital communication systems allows utilities to monitor and manage electricity distribution in real time. This capability enhances the efficiency and reliability of power delivery, enabling quick responses to demand fluctuations and system anomalies.

- Predictive Maintenance and Asset Management: Utilizing AI and machine learning algorithms, utilities can predict equipment failures before they occur. This proactive approach to maintenance reduces downtime, extends the lifespan of assets, and lowers operational costs by addressing issues before they escalate.

- Integration of Renewable Energy Sources: Digital tools facilitate the seamless integration of renewable energy sources, such as solar and wind, into the existing grid. Advanced forecasting and real-time data analytics help balance supply and demand, ensuring a stable and sustainable energy mix.

- Enhanced Customer Engagement through Digital Platforms: Digital platforms enable utilities to offer personalized services, real-time updates on energy usage, and digital billing options. These tools improve customer satisfaction by providing greater transparency and control over energy consumption.

- Decentralized Energy Trading and Blockchain Applications: Blockchain technology supports the development of decentralized energy markets, allowing consumers to trade excess energy directly. This innovation empowers consumers, known as prosumers, to participate actively in the energy market, promoting efficiency and sustainability.

Recent Developments

- In March 2025, Landis, a global pioneer in energy management solutions, has launched the Revelo Cellular grid sensor, all-in-one device that empowers utilities with advanced meter-level edge computing and real-time grid sensing capabilities.

- In December 2024, Legrand, a global leader in electrical and digital infrastructure, has acquired Toronto-based Power Bus Way, a top provider of custom cable bus solutions for data centers, industrial sites, and commercial projects.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 42.01 Bn |

| Forecast Revenue (2034) | USD 149 Bn |

| CAGR (2025-2034) | 13.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Technology (Advanced Metering Infrastructure (AMI), Distribution Management System (DMS), Supervisory Control and Data Acquisition (SCADA), Substation Automation, Energy Management Systems (EMS), Remote Terminal Units (RTU), Communication Infrastructure (Fiber, RF Mesh, Cellular)), By Component (Hardware (Smart Meters, Intelligent Electronic Devices (IEDs), Sensors and Actuators, Communication Devices), Software (Analytics Platforms, Grid Monitoring Software, Energy Management Software), Services (Consulting & Integration, Maintenance & Support, Managed Services)), By End-User (Residential, Commercial, Industrial, Utilities) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Schneider Electric, Siemens AG, ABB Ltd., General Electric (GE) Digital, Eaton Corporation, Honeywell International Inc., Cisco Systems, Inc., Oracle Corporation, IBM Corporation, Landis+Gyr, Hitachi, Legrand, CHINT, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |