Quick Navigation

- Report Overview

- Key Takeaway

- Role of Generative AI

- Investment and Business Benefits

- Regional Analysis

- Storage System Analysis

- Storage Architecture Analysis

- Storage Medium Analysis

- End-User Analysis

- Key Market Segments

- Emerging Trends

- Growth Factors

- Market Dynamics

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

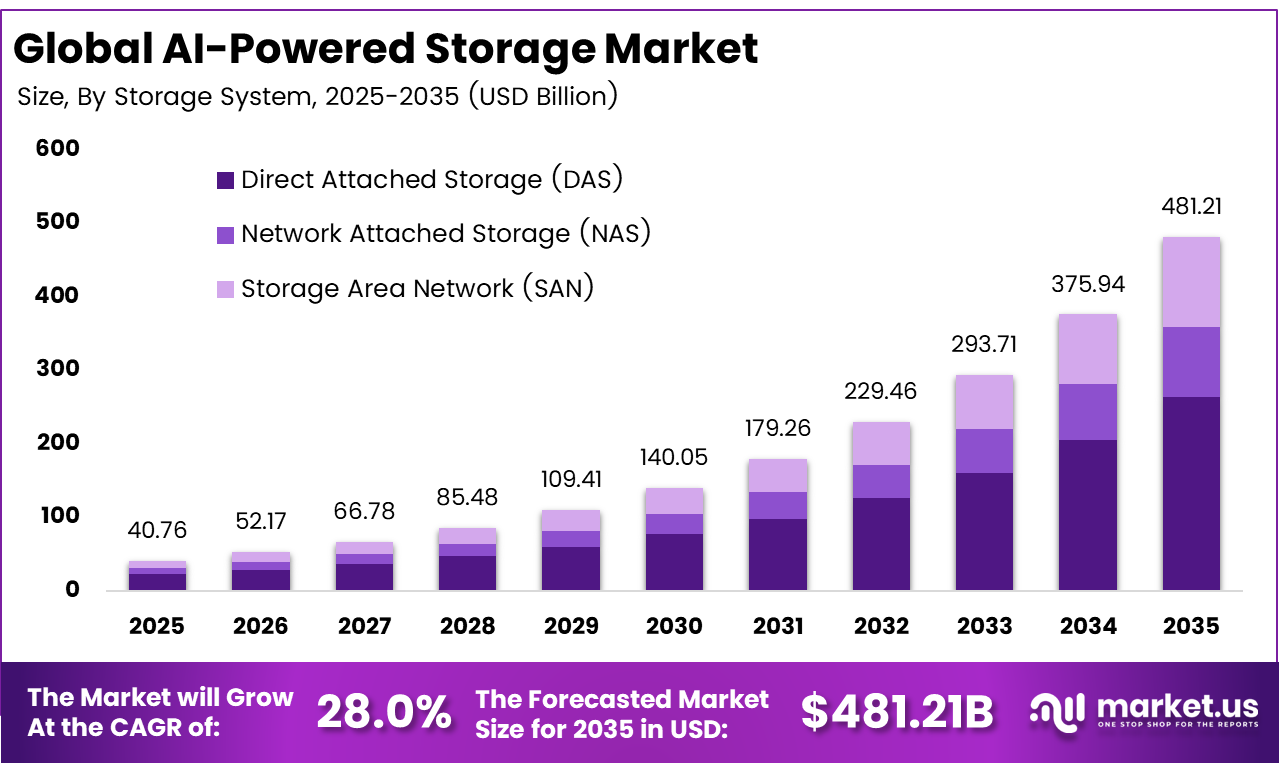

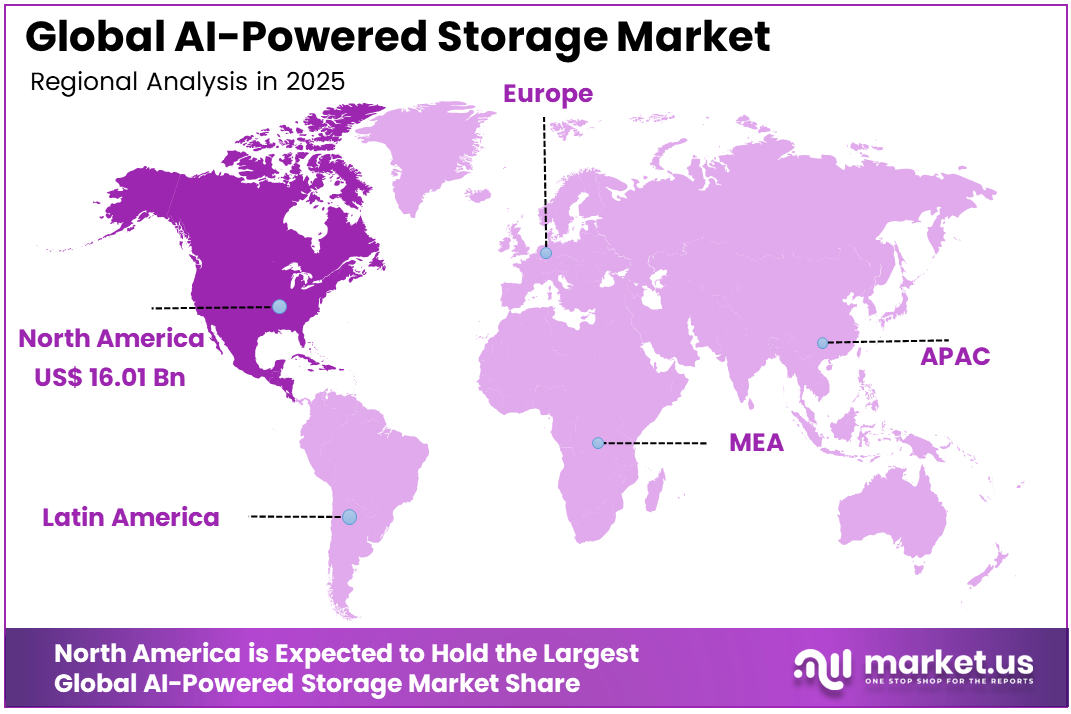

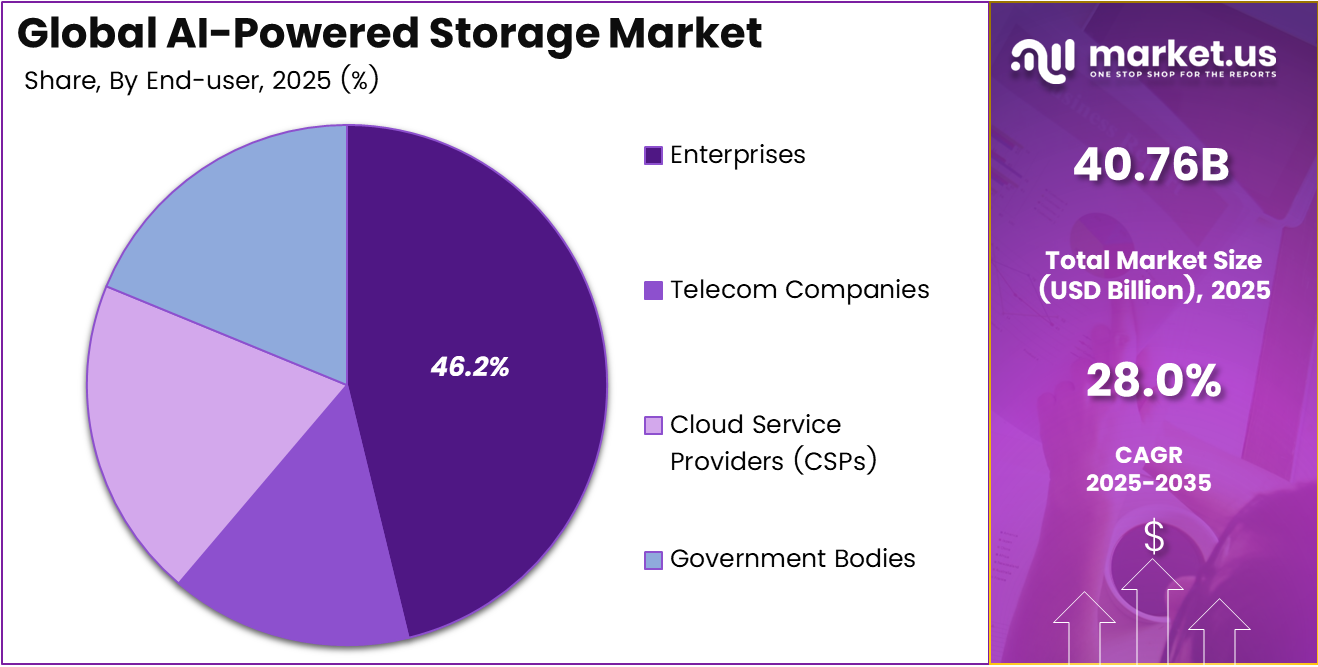

The Global AI-Powered Storage Market size is expected to be worth around USD 481.21 billion by 2035, from USD 40.76 billion in 2025, growing at a CAGR of 28.0% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 39.3% share, holding USD 16.01 billion in revenue.

AI-powered storage relies on artificial intelligence to manage data in a smarter way across data centers, clouds, and edge devices. It handles massive amounts of information from sources like IoT devices and analytics tools that overwhelm older systems. Automating tasks such as data organization and protection ensures faster access and better reliability. This approach fits well with today’s needs for quick processing and secure storage. Teams find it easier to scale operations without constant manual tweaks, keeping everything running smoothly even as data volumes grow.

Businesses deal with endless data streams from digital tools and connected devices every day. Over 90% of fresh data comes from these everyday sources, putting pressure on standard storage setups. AI-powered storage fixes this by automatically sorting data and speeding up retrieval times. It cuts down on wait times and makes operations more efficient overall. This shift helps companies stay ahead in fast-moving environments where delays cost real money.

The market for AI-Powered Storage is driven by the rapid rise in data volumes from IoT devices, cloud apps, and AI workloads that overwhelm traditional systems. Businesses need smart storage to sort, process, and retrieve huge unstructured data sets in real time, cutting delays and boosting efficiency. Edge computing and hybrid clouds further push demand for scalable solutions that automate workflows and handle growth without constant tweaks. This shift helps firms to turn data into quick insight across various sectors, like healthcare and finance.

Demand keeps rising as firms manage more messy data from AI applications and cloud platforms. Real-time tasks call for storage with almost no delays, and solid-state drives stand out for handling intense AI workloads with high input-output speeds. Edge computing adds to the need by processing data right where it’s created, skipping central server jams. Companies turn to these solutions to keep pace with growing data flows without breaking their setups.

For instance, in November 2025, Hewlett Packard Enterprise doubled down on Alletra Storage MP with X10000 Data Intelligence Nodes for private Cloud AI factories. Houston-headquartered HPE’s in-line data intelligence unlocks unstructured data value via NVIDIA partnerships, targeting AI querying and business insights. This positions HPE strongly in scalable AI storage deployments.

Key Takeaway

- In 2025, the Direct Attached Storage (DAS) segment held a dominant market position, capturing a 54.7% share of the Global AI-Powered Storage Market.

- In 2025, the file-based segment held a dominant market position, capturing a 68.9% share of the Global AI-Powered Storage Market.

- In 2025, the Solid State Drive (SSD) segment held a dominant market position, capturing a 65.3% share of the Global AI-Powered Storage Market.

- In 2025, the Enterprises segment held a dominant market position, capturing a 46.2% share of the Global AI-Powered Storage Market.

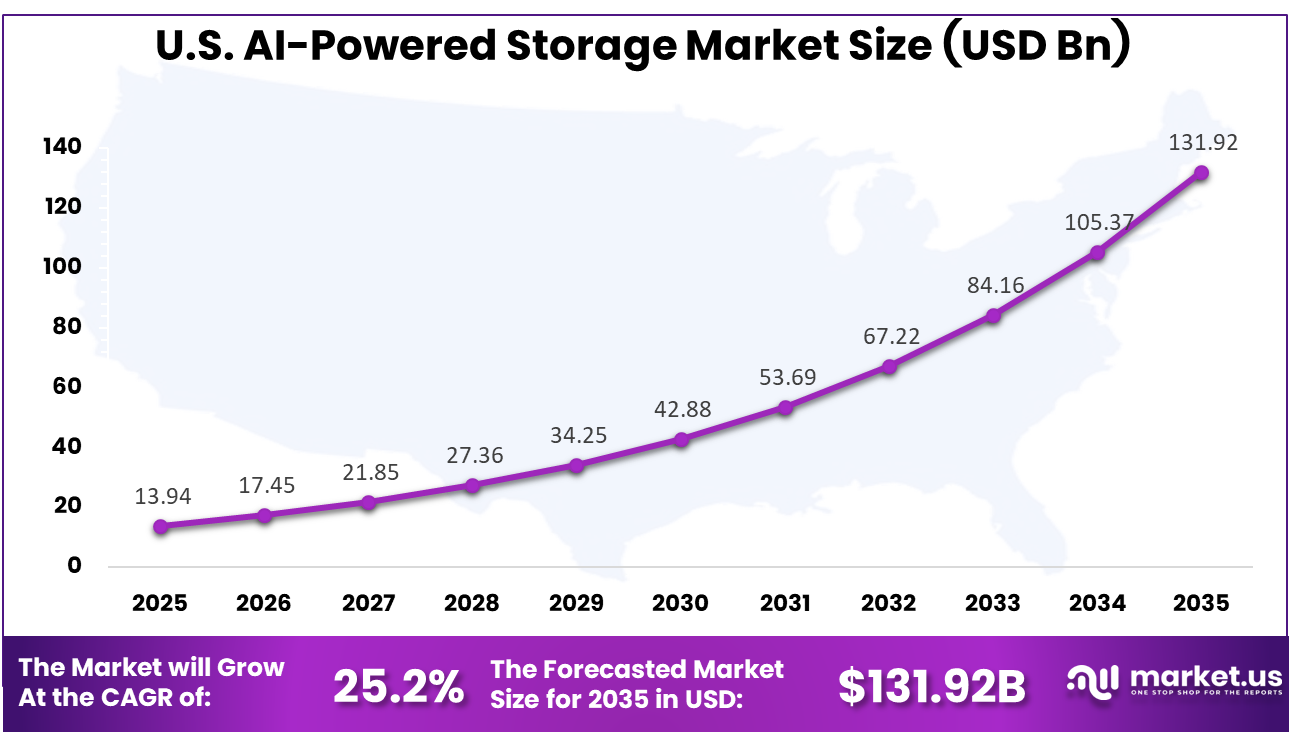

- The U.S. AI-Powered Storage Market was valued at USD 13.94 Billion in 2025, with a robust CAGR of 25.2%.

- In 2025, North America held a dominant market position in the Global AI-Powered Storage Market, capturing more than a 39.3% share.

Role of Generative AI

Generative AI shapes storage by processing huge datasets for training models and creating outputs, demanding fast and scalable systems. Storage now holds up to 50% of unstructured data in formats suited for quick retrieval, compared to under 10% just a few years ago. This enables smoother handling of complex tasks like image and text generation.

Inference processes in generative AI push storage needs further, with server demands rising 105% yearly due to repeated data access. Enterprises often copy data locally for faster processing, relying on intelligent storage to maintain efficiency. These roles make storage essential for generative AI deployment.

Investment and Business Benefits

Upgrading current hardware for AI clusters brings solid returns through better scalability. Edge and mixed cloud systems create chances for solutions focused on low delays. Healthcare data demands push spending higher, especially for imaging and screening powered by AI. Investors see value in areas where data growth meets real-world needs, like quick analysis.

Companies cut expenses by shifting data to lower-cost areas automatically, often saving up to 50% on storage budgets. Day-to-day work speeds up since AI takes over routine jobs, letting IT focus on bigger plans. It also keeps systems always ready with automatic fixes, making full use of resources, no matter the cloud setup.

Regional Analysis

In 2025, North America held a dominant market position in the Global AI-Powered Storage Market, capturing more than a 39.3% share, holding USD 16.01 billion in revenue. This lead stems from early adoption of AI technologies, strong cloud infrastructure, and the presence of major players like Dell and Pure Storage. Enterprises prioritize data protection amid rapid digitization in finance and healthcare. High investments in data centers and skilled professionals boost growth. Exponential data from AI workloads demands efficient storage solutions.

For instance, in July 2025, Micron unveiled industry-first PCIe Gen6 NVMe SSDs with G9 NAND, offering high capacity and low latency for AI data centers. These SSDs deliver energy-efficient performance for diverse AI workloads, strengthening North America’s position in next-gen AI storage technology.

U.S. AI-Powered Storage Market Size

The market for AI-Powered Storage within the U.S. is growing tremendously and is currently valued at USD 13.94 billion; the market has a projected CAGR of 25.2%. The market is growing due to exploding data volumes from AI, IoT, and cloud apps that demand smart management. Enterprises need scalable systems for real-time analytics and machine learning workloads. Early tech adoption, hyperscale data centers, and heavy investments in AI research speed this up. Edge computing and high-performance needs push for low-latency storage. Security and automation features help handle unstructured data growth.

For instance, in January 2026, NVIDIA announced that BlueField-4 data processor powers the NVIDIA Inference Context Memory Storage Platform, creating a new class of AI-native storage infrastructure for advanced AI applications. This innovation revolutionizes storage for intelligent AI collaborators with long-term memory capabilities, reinforcing U.S. leadership in AI-powered storage technology.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Storage System Analysis

In 2025, the Direct Attached Storage (DAS) segment held a dominant market position, capturing a 54.7% share of the Global AI-Powered Storage Market. It connects straight to servers without networks, which means faster data access for AI tasks. This setup cuts latency and handles high workloads well. Teams values its simplicity for quick processing needs. Real-time AI applications run smoothly since data moves directly. Many setups favor DAS for its reliability in demanding environments.

The dominance of DAS grows from its cost-effective design for specific server needs. It avoids complex network management, saving time and resources. AI training benefits from this direct path, keeping data flows steady. Users report better performance in intensive jobs. As AI demands rise, DAS fits well for focused storage tasks. Its straightforward nature appeals to practical operations.

For Instance, in December 2025, NVIDIA Corporation teamed up with SK hynix to develop “Storage Next” SSDs aimed at high-performance AI inference. These drives target AI workloads on Rubin GPUs, promising up to 10x better performance than standard SSDs. This push supports direct server connections for low-latency DAS setups in AI clusters.

Storage Architecture Analysis

In 2025, the File-Based segment held a dominant market position, capturing a 68.9% share of the Global AI-Powered Storage Market. It organizes data into familiar folders, ideal for unstructured AI files. This structure supports easy access during model training and analysis. Common tools integrate smoothly with file systems. Large datasets stay manageable this way. Adoption stays high due to its proven handling of varied data types.

File-based leads because it matches everyday AI workflows without major changes. Teams handle images, videos, and logs efficiently in hierarchies. It scales for growing data volumes in AI projects. Simplicity reduces setup hurdles for users. This architecture supports collaboration across departments. Its flexibility keeps it ahead in practical use cases.

For instance, in November 2025, Huawei Technologies released OceanStor Next-Gen High-Performance Distributed File Storage for AI. It supports file formats like NFS and S3 for training data lakes, boosting bandwidth to hundreds of TB/s. File-based handling speeds up AI model processes.

Storage Medium Analysis

In 2025, the Solid State Drive (SSD) segment held a dominant market position, capturing a 65.3% share of the Global AI-Powered Storage Market. SSDs offer fast read and write speeds with low latency. This keeps AI processors active on large datasets. They outperform traditional drives in speed-critical tasks. Training models completes quickly, boosting productivity. Their endurance suits constant AI operations.

SSDs dominate due to reliability in high-intensity AI environments. No moving parts means less failure risk under heavy loads. Energy use stays lower, aiding data center efficiency. AI workloads thrive on consistent performance. Users see clear gains in processing times. This makes SSD the go-to choice for modern storage needs.

For Instance, in January 2026, NVIDIA standardized GPU cluster KV cache offload to NVMe SSDs for AI inference. With BlueField-4 DPUs, it manages cache on SSDs for long-context tasks. Partners like Pure Storage and Dell support this SSD shift in AI pipelines.

End-User Analysis

In 2025, the Enterprises segment held a dominant market position, capturing a 46.2% share of the Global AI-Powered Storage Market. Large businesses use it for data-heavy operations in finance and healthcare. Automation improves with smart storage integration. Decisions get sharper from better data access. Scale matches their vast needs across locations. Adoption drives from clear operational gains.

Enterprise focus stems from the need for secure, fast data handling. AI storage helps analyze trends and automate routines effectively. Teams across sectors report streamlined workflows. Investments pay off through efficiency boosts. This segment leads as businesses prioritize data-driven strategies. Growth reflects real-world demands.

For Instance, in June 2025, NetApp and Intel partnered on integrated AI inferencing solutions for enterprises. Using Intel Xeon processors, it accelerates AI on AFF A-Series storage. Enterprises benefit from a secure, unified data infrastructure.

Key Market Segments

By Storage System

- Direct Attached Storage (DAS)

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

By Storage Architecture

- File Based

- Object Based

By Storage Medium

- Hard Disk Drive (HDD)

- Solid State Drive (SSD)

By End-User

- Enterprises

- Telecom Companies

- Cloud Service Providers (CSPs)

- Government Bodies

Emerging Trends

Solid-state drives gain traction in AI storage for their low latency and high-speed operations, ideal for rapid data pulls. Hybrid cloud setups combine on-site control with cloud flexibility, while AI-driven automation handles capacity planning and data sorting without manual input. These shifts meet the speed requirements of AI workloads effectively.

Predictive tools powered by machine learning spot potential issues early, preventing downtime in storage environments. Real-time threat detection strengthens security, and multi-cloud strategies enhance scalability across platforms.

Growth Factors

The unstructured data from sensors, videos, and logs floods systems, pushing storage to organize and fetch it instantly without human input. AI steps in to classify files, move them to the right tiers, and spot usage trends ahead of time. This automation frees staff for higher-value work amid rising volumes.

Edge computing is also growing as devices process data on-site, reducing lag for apps like autonomous vehicles or smart factories. Local AI storage handles quick reads and writes right where action happens, easing pressure on central networks. It enables real-time decisions that central setups often miss.

Market Dynamics

Drivers - Rising Data Volumes

The surge in data from cloud platforms, IoT devices, and digital applications pushes businesses to find smarter storage options. AI-powered storage systems help manage these growing volumes by automatically organizing, tiering, and retrieving data as needed. This automation reduces downtime and makes it easier for enterprises to handle ongoing data influx without heavy manual input.

These systems also improve how organizations deal with complex data structures. Instead of spending time on sorting and maintaining files, teams can focus on analytical and strategic tasks. As daily data levels rise, AI-driven storage ensures consistent performance and adaptability, making it a reliable choice for companies managing large-scale digital operations.

For instance, in January 2026, NVIDIA announced the BlueField-4 data processor powering the Inference Context Memory Storage Platform for AI-native storage. This platform handles vast context data from trillion-parameter AI models and multi-step reasoning. It extends GPU memory for high-speed sharing across nodes, reducing data movement. The solution boosts tokens per second and power efficiency for long-context AI systems. Storage partners like Dell and Pure Storage plan to integrate it in 2026.

Restraint - High Setup Costs

Implementing AI-powered storage solutions involves considerable investment in equipment, software, and integration services. Many smaller businesses struggle to justify such expenses, especially when traditional storage systems meet their immediate needs at lower costs. This cost barrier restricts adoption, particularly in sectors that operate on tight budgets.

Even after setup, these systems need continuous maintenance and updates to stay efficient. The extra spending on technical support and operational resources can strain companies with limited IT capacity. This ongoing requirement slows down adoption and makes it harder for organizations to fully benefit from AI-enabled storage technologies.

For instance, in September 2025, Pure Storage enhanced its Enterprise Data Cloud with AI capabilities and cloud-native services like Pure Storage Cloud Azure Native. These updates aim to unify data management but require significant investment in hybrid infrastructure. The Intelligent Control Plane automates workflows across ecosystems, adding to initial software and integration costs. Smaller firms may hesitate due to the scale of deployment. Maintenance for AI-driven features further increases long-term expenses.

Opportunities - Edge Computing Growth

The expansion of edge computing presents a key opportunity for AI-powered storage technologies. By processing data close to its source, such as in smart factories or autonomous vehicles, businesses can cut delays and make faster decisions. This localized data handling improves performance and supports real-time analytics where quick action matters most.

As networks evolve, integrating AI storage with edge systems allows smoother data movement across distributed environments. Companies gain better control over their data without needing to rely on central data centers. This approach enhances responsiveness and creates new use cases across industries where time-sensitive decisions are crucial.

For instance, in January 2026, Infortrend released the EonStor GS 5024U, its top U.2 NVMe SSD storage for AI workloads. The system supports GPUDirect Storage and parallel file systems like Lustre for edge-to-core data flows. It scales to 20PB with automated tiering for real-time analytics in factories or vehicles. High-speed 200GbE and NVMe-oF enable low-latency processing near data sources. This fits edge computing needs in AI training and inference.

Challenges - Skilled Staff Shortage

A major challenge facing AI-powered storage adoption is the lack of trained professionals capable of running and maintaining these complex systems. Managing AI-driven storage requires knowledge of both data science and IT infrastructure, which many organizations find hard to source. This limited expertise can lead to configuration errors or inefficient performance.

Developing the necessary technical skills takes time, and many teams already face stretched workloads. As a result, training often competes with other priorities, making it difficult for organizations to keep pace with rapid technology changes. Without skilled staff, even advanced storage setups may fail to deliver their full potential.

For instance, in October 2025, Intel announced the Crescent Island data center GPU optimized for AI inference with large memory capacity. The Xe3P architecture targets enterprise servers but requires expertise in tuning for diverse data types. Deployment involves configuring high-bandwidth LPDDR5X for tokens-as-a-service. Teams need advanced skills to maximize performance-per-watt gains. Skill gaps slow rollout in air-cooled environments.

Key Players Analysis

One of the leading players in March 2025, Pure Storage, Inc., integrated NVIDIA’s AI Data Platform into its FlashBlade/EXA, delivering high-performance guarantees for large-scale AI training and inference. The Mountain View-based firm also unveiled FlashBlade//EXA for AI/HPC workloads, emphasizing multi-tenancy and QoS. Pure’s focus on eliminating bottlenecks solidifies its role in enterprise AI storage.

Top Key Players in the Market

- NVIDIA Corporation

- Intel Corporation

- Pure Storage, Inc.

- Infortrend Technology Inc.

- Huawei Technologies Co., Ltd.

- IBM Corporation

- NetApp

- Hewlett Packard Enterprise Development LP

- Dell Inc.

- Micron Technology, Inc.

- Others

Recent Developments

- In January 2026, NVIDIA Corporation launched the BlueField-4 data processors, which power the new NVIDIA Inference Context Memory Storage Platform for AI-native infrastructure. This breakthrough enables intelligent collaborators with long-term memory capabilities, revolutionizing storage for physical-world understanding and tool use in AI applications.

- In November 2025, Hewlett Packard Enterprise doubled down on Alletra Storage MP with X10000 Data Intelligence Nodes for private Cloud AI factories. Houston-headquartered HPE’s in-line data intelligence unlocks unstructured data value via NVIDIA partnerships, targeting AI querying and business insights. This positions HPE strongly in scalable AI storage deployments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 40.76 Billion |

| Forecast Revenue (2035) | USD 481.21 Billion |

| CAGR (2026-2035) | 28.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Storage System (Direct Attached Storage (DAS), Network Attached Storage (NAS), Storage Area Network (SAN), By Storage Architecture (File Based, Object Based), By Storage Medium (Hard Disk Drive (HDD), Solid State Drive (SSD), By End-user (Enterprises, Telecom Companies, Cloud Service Providers (CSPs), Government Bodies) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | NVIDIA Corporation, Intel Corporation, Pure Storage, Inc., Infortrend Technology Inc., Huawei Technologies Co., Ltd., IBM Corporation, NetApp, Hewlett Packard Enterprise Development LP, Dell Inc., Micron Technology Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |