Quick Navigation

Report Overview

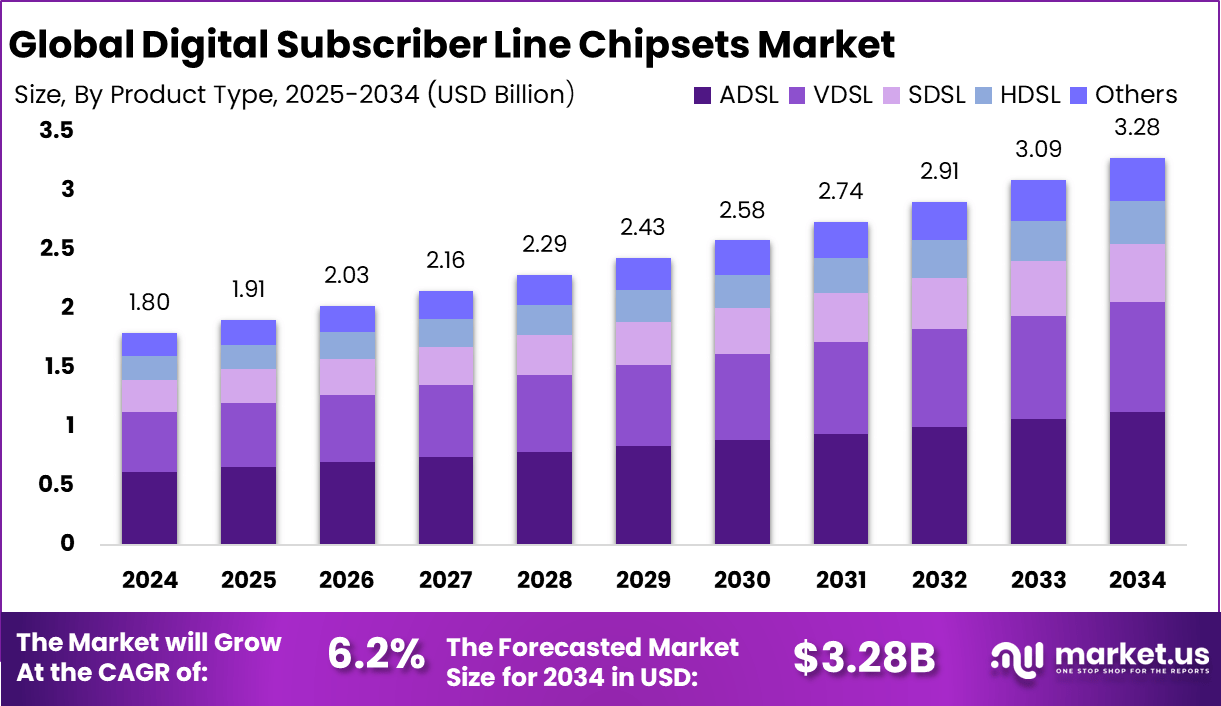

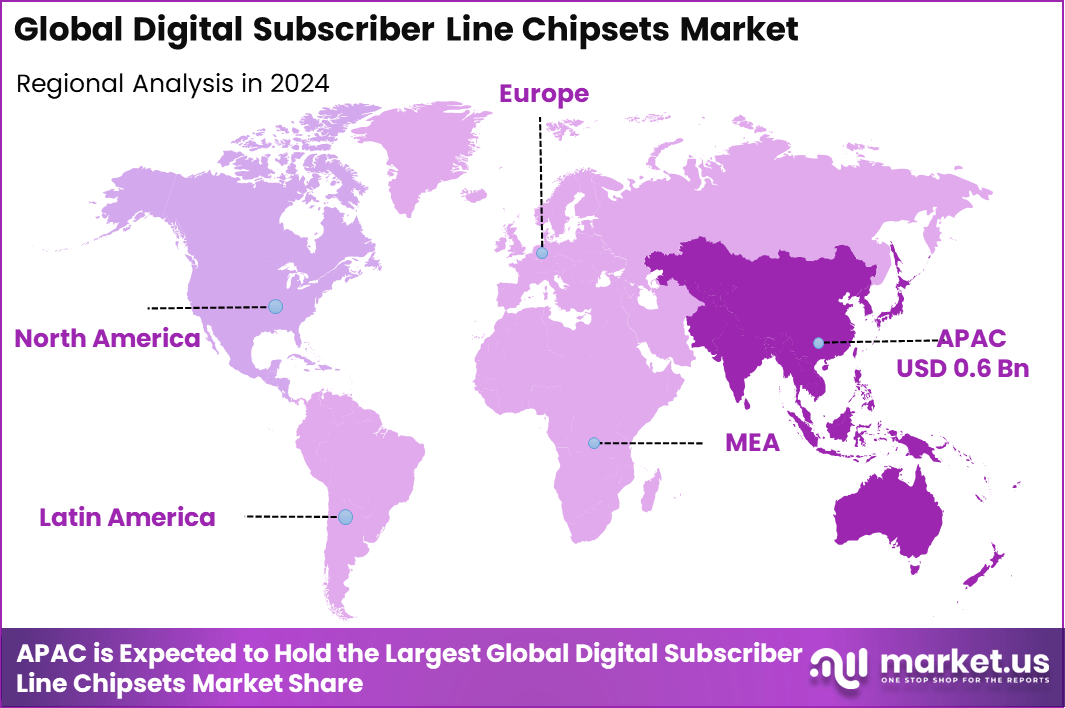

The Global Digital Subscriber Line (DSL) Chipsets Market size is expected to be worth around USD 3.28 billion by 2034, from USD 1.8 billion in 2024, growing at a CAGR of 6.2% during the forecast period from 2025 to 2034. In 2024, Asia Pacific held a dominant market position, capturing more than a 35.8% share, holding USD 0.6 Billion in revenue.

Digital Subscriber Line (DSL) chipsets are specialized semiconductor components that enable high-speed data transmission over traditional copper telephone lines. These chipsets are integral to DSL modems, facilitating broadband internet access without necessitating new infrastructure. By employing advanced modulation techniques, DSL chipsets allow simultaneous voice and data services, making them a cost-effective solution for enhancing internet connectivity, particularly in areas where fiber-optic deployment is limited.

The Digital Subscriber Line (DSL) Chipsets Market is witnessing growth due to increasing demand for inexpensive, high-speed Internet solutions, particularly in rural or underserved areas where deployment of a fiber-optic infrastructure is not viable. DSL technology mainly uses existing copper wiring, which can significantly bring the costs of deployment down while providing an efficient broadband solution.

In addition, the new technologies are pushing DSL performance ever higher; for example, advancements in VDSL2 and G.fast technologies have resulted in massively increased DSL speeds, making DSL quite competitive relative to fiber and cable alternatives. After COVID-19, the need for broadband increased tremendously all around the world due to the recent developments in remote working, online education, and streaming services.

For instance, In March 2025, Broadcom introduced two advanced chips Sian3 and Sian2M designed to enhance optical data center networks. These chips aim to improve power efficiency and scalability in artificial intelligence (AI) clusters by optimizing the conversion of electrical signals to light and vice versa. The Sian3 chip, built on a three-nanometer process, supports long-range single-mode fiber (SMF) connections, offering 20% better power efficiency compared to previous models.

Technological advancements are playing a crucial role in the evolution of DSL chipsets. The development of G.fast technology, which enables gigabit speeds over copper lines, is extending the viability of DSL in the broadband market. Additionally, AI-driven diagnostics and network optimization are improving the performance and reliability of DSL services, making them more appealing to both service providers and consumers.

Key Takeaway

- In 2024, the ADSL segment led the global Digital Subscriber Line (DSL) Chipsets Market, accounting for 34.4% of the total share, supported by its continued usage in cost-effective broadband access for residential and small business users.

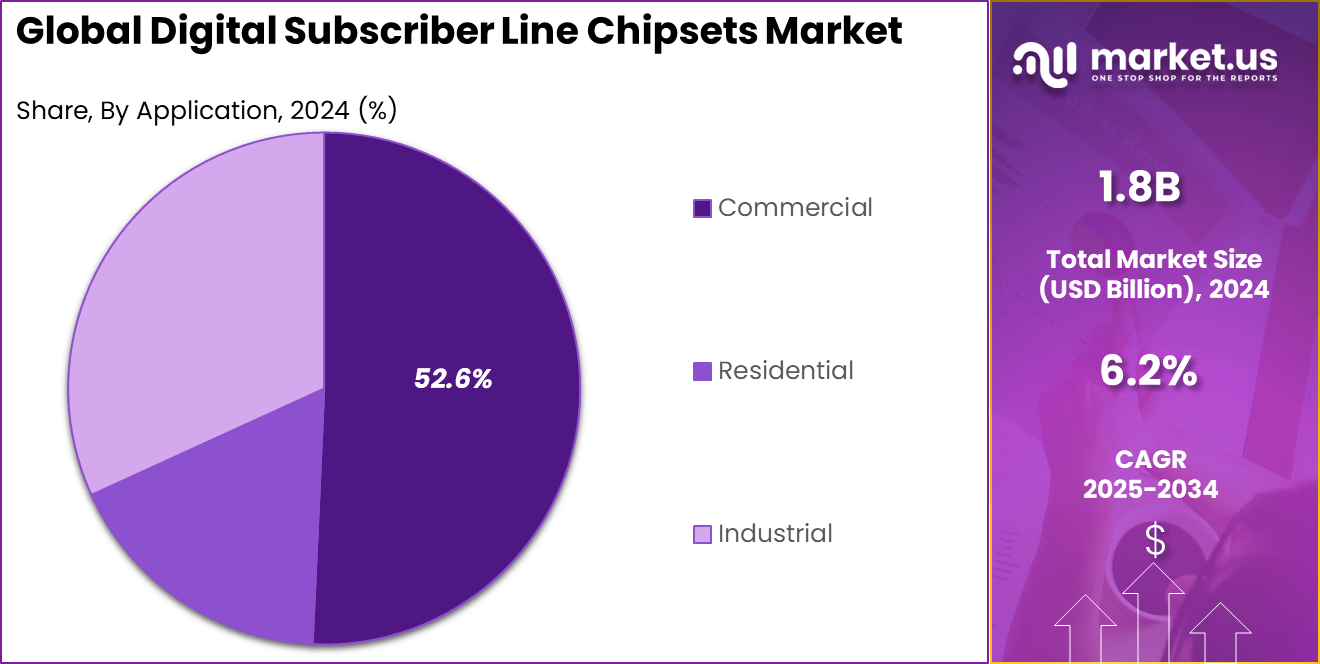

- The Commercial segment dominated by end-user, securing 52.6% of the market in 2024, driven by growing internet bandwidth needs across enterprise environments and office networks.

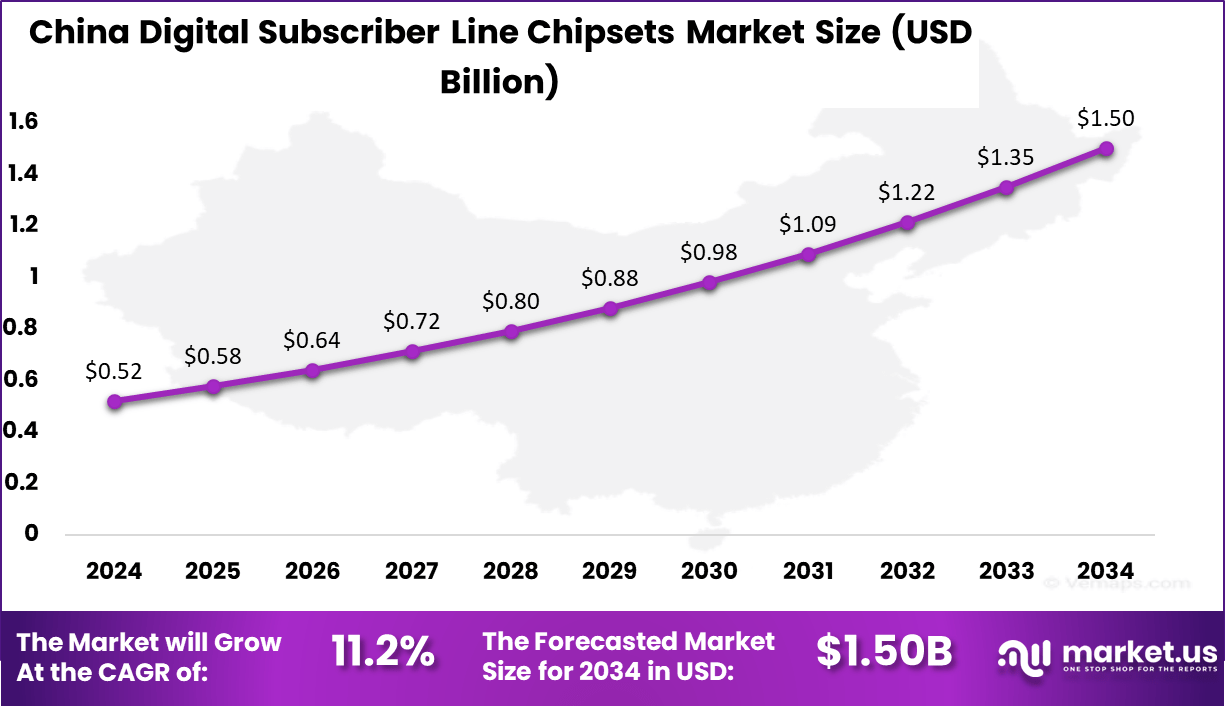

- The China DSL Chipsets Market was valued at USD 0.52 Billion in 2024 and is expected to expand at a steady CAGR of 11.2%, indicating consistent demand for legacy and hybrid internet infrastructure in suburban and rural areas.

- APAC held a dominant regional position in 2024, capturing more than 35.8% of the global DSL chipsets market, due to broad telecom infrastructure and sustained investments in fixed broadband technology.

AI’s Role

Artificial Intelligence (AI) is playing a transformative role in optimizing Digital Subscriber Line (DSL) networks, which continue to be a vital part of broadband infrastructure in many parts of the world, especially where fiber deployment remains economically or logistically challenging.

AI enables DSL providers to enhance performance, improve efficiency, and extend the lifecycle of existing copper-based networks. With the growing reliance on high-speed internet for digital services, the integration of AI into DSL systems is being seen as both a strategic and cost-effective solution to meet increasing consumer demands.

One of the most significant contributions of AI in DSL optimization is its ability to conduct real-time diagnostics and automate fault detection across millions of DSL lines. This capability allows service providers to identify disruptions and address them before users are impacted, thereby improving uptime and customer satisfaction.

Advanced machine learning algorithms are being used to implement Dynamic Spectrum Management (DSM), a method that minimizes interference between lines by intelligently allocating frequency bands. This directly results in better data throughput and more stable connections.

Furthermore, AI-powered predictive analytics can assess historical usage patterns and system behavior to forecast potential performance degradation or equipment failures. Such foresight reduces operational costs and enhances network reliability

China Market Size

The China Digital Subscriber Line (DSL) Chipsets Market is valued at approximately USD 0.52 Billion in 2024 and is predicted to increase from USD 0.58 Billion in 2025 to approximately USD 1.5 Billion by 2034, projected at a CAGR of 11.2% from 2025 to 2034.

In 2024, Asia-Pacific (APAC) held a dominant market position, capturing more than a 35.8% share of the Global Digital Subscriber Line (DSL) Chipsets Market, with an estimated revenue of approximately USD 0.6 billion. This regional dominance was primarily driven by the rapid digital infrastructure expansion across emerging economies such as China, India, and Southeast Asian countries.

The surge in broadband penetration, fueled by national digital inclusion initiatives and population-scale internet rollouts, significantly contributed to the widespread deployment of DSL networks. The region’s vast subscriber base and strong government backing for rural broadband connectivity programs have made DSL a cost-effective last-mile access solution.

Moreover, the growing number of small and medium-sized enterprises (SMEs) in APAC continues to rely on DSL technologies for affordable internet connectivity, especially in areas where fiber deployment remains economically challenging.

Product Type Analysis

In 2024, the Asymmetric Digital Subscriber Line (ADSL) segment held a dominant position in the global Digital Subscriber Line (DSL) chipsets market, capturing more than a 34.4% share. This leadership can be attributed to ADSL’s widespread adoption, cost-effectiveness, and compatibility with existing copper infrastructure, making it a preferred choice for broadband connectivity, especially in regions where fiber deployment is limited.

ADSL technology offers a balanced solution by providing sufficient bandwidth for typical internet activities such as web browsing, email, and streaming, without necessitating significant infrastructure investments. Its ability to deliver higher download speeds compared to upload speeds aligns well with consumer usage patterns, further enhancing its appeal.

The extensive deployment of ADSL in residential areas, particularly in emerging economies, has reinforced its market dominance. Governments and service providers in these regions have leveraged ADSL to expand internet access rapidly and cost-effectively, bridging the digital divide and fostering economic development.

Despite the emergence of advanced technologies like VDSL and fiber optics, ADSL’s established user base and the substantial costs associated with transitioning to newer infrastructures have sustained its relevance. Consequently, ADSL continues to play a crucial role in global broadband connectivity, maintaining its significant share in the DSL chipsets market.

Application Analysis

In 2024, the commercial segment held a dominant position in the global Digital Subscriber Line (DSL) chipsets market, capturing more than a 52.6% share. This leadership is attributed to the escalating demand for reliable and cost-effective broadband solutions among small and medium-sized enterprises (SMEs), retail chains, educational institutions, and healthcare facilities.

The necessity for stable internet connectivity to support cloud-based applications, video conferencing, and data-intensive operations has propelled the adoption of DSL technologies in commercial settings. The preference for DSL in commercial applications is further reinforced by its ability to leverage existing copper infrastructure, offering a cost-effective alternative to fiber-optic deployments.

This is particularly advantageous for businesses operating in regions where fiber installation is economically unfeasible or logistically challenging. Moreover, advancements in DSL technologies, such as VDSL and G.fast, have enhanced data transmission rates, meeting the bandwidth requirements of modern commercial operations.

Government initiatives aimed at enhancing digital connectivity have also played a pivotal role in the commercial segment’s growth. Programs focused on expanding broadband access in underserved areas have encouraged businesses to adopt DSL solutions, thereby fostering economic development and bridging the digital divide.

Key Market Segments

By Product Type

- ADSL

- VDSL

- SDSL

- HDSL

- Others

By Application

- Residential

- Commercial

- Industrial

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Cost-Effective Broadband Expansion in Underserved Regions

The global DSL chipsets market is experiencing growth driven by the need for affordable broadband solutions, particularly in regions where fiber-optic infrastructure is limited. DSL technology leverages existing copper telephone lines, enabling rapid and cost-effective deployment of internet services.

This approach is especially beneficial in rural and underserved areas, where laying new fiber-optic cables may be economically unfeasible. The ability of DSL to provide reliable internet access without significant infrastructure investments makes it a practical choice for expanding connectivity in these regions.

Furthermore, advancements in DSL technologies, such as VDSL and G.fast, have enhanced data transmission rates, making DSL a competitive option for high-speed internet access. These improvements have allowed service providers to offer better services without overhauling existing infrastructure.

Restraint

Competition from Fiber-Optic and Wireless Technologies

Despite its advantages, the DSL chipsets market faces challenges due to the increasing adoption of fiber-optic and wireless broadband technologies. Fiber-optic networks offer significantly higher data transmission speeds and greater reliability, making them an attractive alternative for consumers and businesses seeking superior internet performance.

Additionally, the proliferation of wireless broadband, including 4G and 5G networks, provides users with high-speed internet access without the need for fixed-line connections. This mobility and ease of deployment further diminish the appeal of DSL, particularly in urban areas where wireless coverage is robust.

Opportunities

Integration of DSL in Hybrid Network Solutions

An emerging opportunity for the DSL chipsets market lies in the integration of DSL technology within hybrid network solutions. By combining DSL with other technologies, such as fiber-optic and wireless networks, service providers can create versatile and resilient broadband infrastructures.

For instance, DSL can serve as a complementary technology in areas where fiber deployment is incomplete, ensuring continuous service and expanding coverage. Moreover, the development of hybrid modems and routers that support multiple connection types allows for seamless switching between networks, optimizing performance and reliability.

This adaptability is particularly valuable in regions with diverse geographical and infrastructural challenges. By positioning DSL as a component of integrated broadband solutions, the market can capitalize on its strengths while addressing the limitations posed by standalone DSL deployments.

Challenges

Aging Infrastructure and Maintenance Costs

A significant challenge confronting the DSL chipsets market is the reliance on aging copper infrastructure. Many existing DSL networks operate over decades-old telephone lines, which are susceptible to degradation and may not support higher-speed DSL technologies effectively.

Maintaining and upgrading this infrastructure incurs substantial costs, and service providers must balance these expenses against the benefits of continued DSL service provision. Furthermore, as consumer demand for higher bandwidth and more reliable internet connections grows, the limitations of legacy copper networks become more pronounced.

In some cases, the investment required to modernize DSL infrastructure may approach or exceed the cost of deploying alternative technologies, such as fiber-optic networks. This financial consideration poses a strategic dilemma for providers, potentially hindering the long-term viability of DSL services in certain markets.

Growth Factors

The expansion of the DSL chipsets market is primarily driven by the increasing demand for affordable and reliable broadband services, particularly in emerging economies. In regions where fiber-optic deployment is limited, DSL technology offers a practical alternative by utilizing existing copper infrastructure. Government initiatives aimed at enhancing digital connectivity further bolster the adoption of DSL solutions.

Technological advancements, such as the development of Very-high-bit-rate Digital Subscriber Line (VDSL) and G.fast technologies, have significantly improved the performance of DSL networks. These innovations enable higher data transmission rates, making DSL a competitive option for high-speed internet access. The integration of Artificial Intelligence (AI) in network management has also enhanced the efficiency and reliability of DSL connections.

Emerging Trends

A notable trend in the DSL chipsets market is the integration of advanced features like vectoring and bonding. Vectoring technology mitigates crosstalk interference between multiple DSL lines, enhancing overall network performance, while bonding allows the aggregation of multiple lines to increase bandwidth .

The convergence of DSL with other technologies, such as fiber and wireless networks, is also gaining traction. Hybrid models that combine DSL with fiber-optic or wireless solutions are being explored to extend broadband coverage and improve service quality. These approaches aim to leverage the strengths of each technology to deliver enhanced connectivity solutions.

Business Benefits

For businesses, DSL chipsets offer a cost-effective means to achieve high-speed internet connectivity without the need for extensive infrastructure investments. This is particularly beneficial for small and medium-sized enterprises (SMEs) operating in areas where fiber-optic networks are not readily available. DSL technology enables these businesses to access essential online services, such as cloud computing and VoIP, thereby enhancing operational efficiency.

Moreover, the scalability of DSL solutions allows businesses to adjust their bandwidth requirements based on evolving needs. This flexibility ensures that companies can maintain optimal performance levels without incurring significant costs associated with infrastructure upgrades. The reliability and stability of DSL connections further contribute to uninterrupted business operations.

Key Players Analysis

Broadcom Corporation has strategically shifted its focus towards AI and cloud infrastructure, notably through its significant acquisition of VMware. In 2025, the company confirmed it is not pursuing further mergers or acquisitions, including a speculated deal with Intel’s chip design unit.

This decision underscores Broadcom’s commitment to consolidating its current assets and enhancing its position in the AI and cloud sectors. By prioritizing internal development and integration, Broadcom aims to strengthen its market presence and deliver advanced solutions in these rapidly evolving industries.

MediaTek Inc. has made remarkable strides in semiconductor innovation. In 2025, the company announced plans to tape out its first 2nm chip at TSMC by September, marking a significant advancement in chip design and manufacturing.

Additionally, MediaTek unveiled the Dimensity 9400e chipset, designed to enhance performance and energy efficiency in upcoming devices. These developments highlight MediaTek’s commitment to staying at the forefront of semiconductor technology and its strategic collaboration with TSMC to achieve cutting-edge manufacturing capabilities.

Intel Corporation is actively exploring strategic partnerships to revitalize its manufacturing capabilities. In 2025, Intel and TSMC discussed a preliminary agreement to form a joint venture aimed at operating Intel’s chipmaking facilities.

This collaboration is part of Intel’s broader strategy to enhance its production efficiency and competitiveness in the semiconductor industry. By leveraging TSMC’s expertise in chip manufacturing, Intel seeks to address challenges in its foundry business and strengthen its position in the global market.

Top Key Players in the Market

- Broadcom Corporation

- MediaTek Inc.

- Intel Corporation

- Qualcomm Incorporated

- Infineon Technologies AG

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Marvell Technology Group Ltd.

- Lantiq (acquired by Intel)

- Sckipio Technologies

- Ikanos Communications (acquired by Qualcomm)

- ZTE Corporation

- Huawei Technologies Co., Ltd.

- Alcatel-Lucent (now part of Nokia)

- Realtek Semiconductor Corp.

- Analog Devices, Inc.

- Microchip Technology Inc.

- Vitesse Semiconductor Corporation

- Cavium, Inc.

- Others

Recent Developments

- In April 2025, Qualcomm acquired Movian AI, a generative artificial intelligence unit from Vietnamese research company VinAI. This strategic move enhances Qualcomm’s capabilities in AI-driven network optimization, potentially benefiting DSL technologies through improved performance and efficiency.

- In Q1 2025, MediaTek introduced the M90 5G modem, supporting both sub-6GHz and mmWave frequencies, with peak speeds up to 12Gbps and satellite (NTN) connectivity. While primarily a 5G product, the underlying technologies may influence DSL chipset advancements, particularly in hybrid network solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.8 Bn |

| Forecast Revenue (2034) | USD 3.28 Bn |

| CAGR (2025-2034) | 6.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Product Type (ADSL, VDSL, SDSL, HDSL, Others), By Application (Residential, Commercial, Industrial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Broadcom Corporation, MediaTek Inc., Intel Corporation, Qualcomm Incorporated, Infineon Technologies AG, STMicroelectronics N.V., NXP Semiconductors N.V., Texas Instruments Incorporated, Marvell Technology Group Ltd., Lantiq (acquired by Intel), Sckipio Technologies, Ikanos Communications (acquired by Qualcomm), ZTE Corporation, Huawei Technologies Co., Ltd., Alcatel-Lucent (now part of Nokia), Realtek Semiconductor Corp., Analog Devices, Inc., Microchip Technology Inc., Vitesse Semiconductor Corporation, Cavium, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |