Quick Navigation

Report Overview

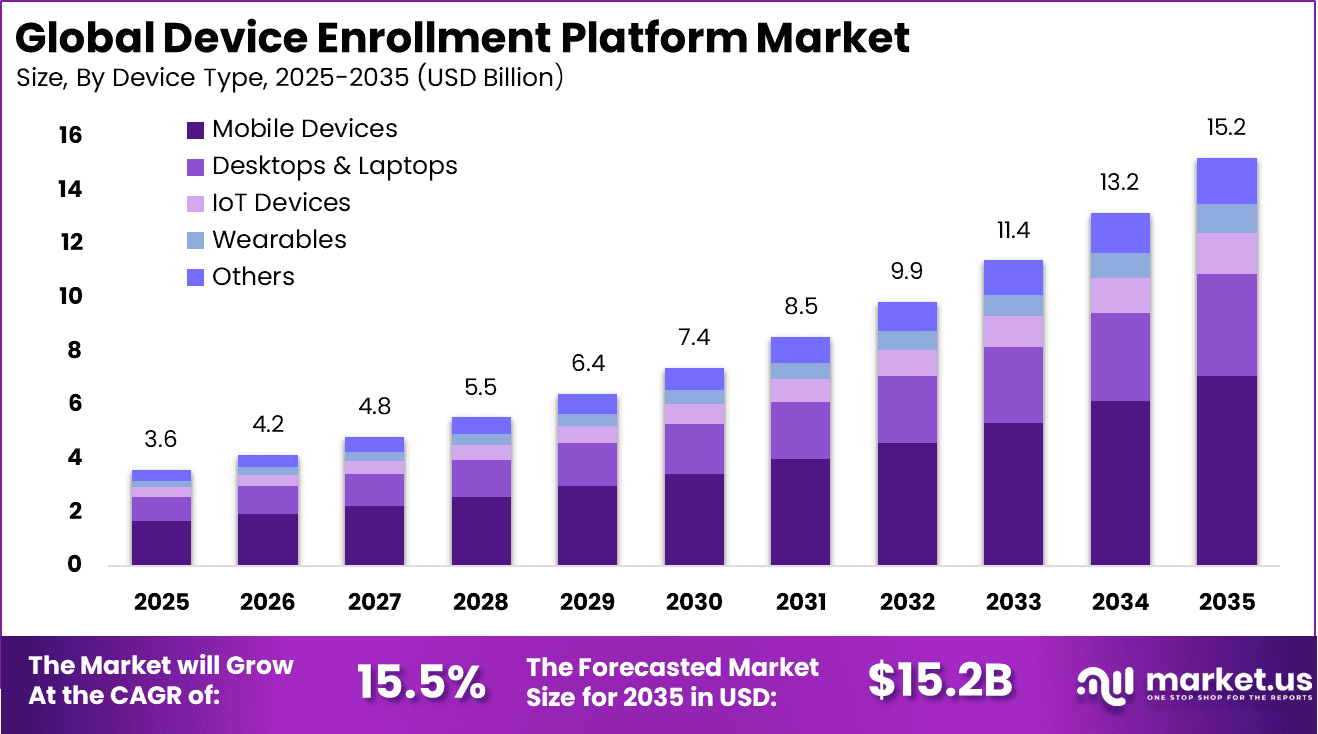

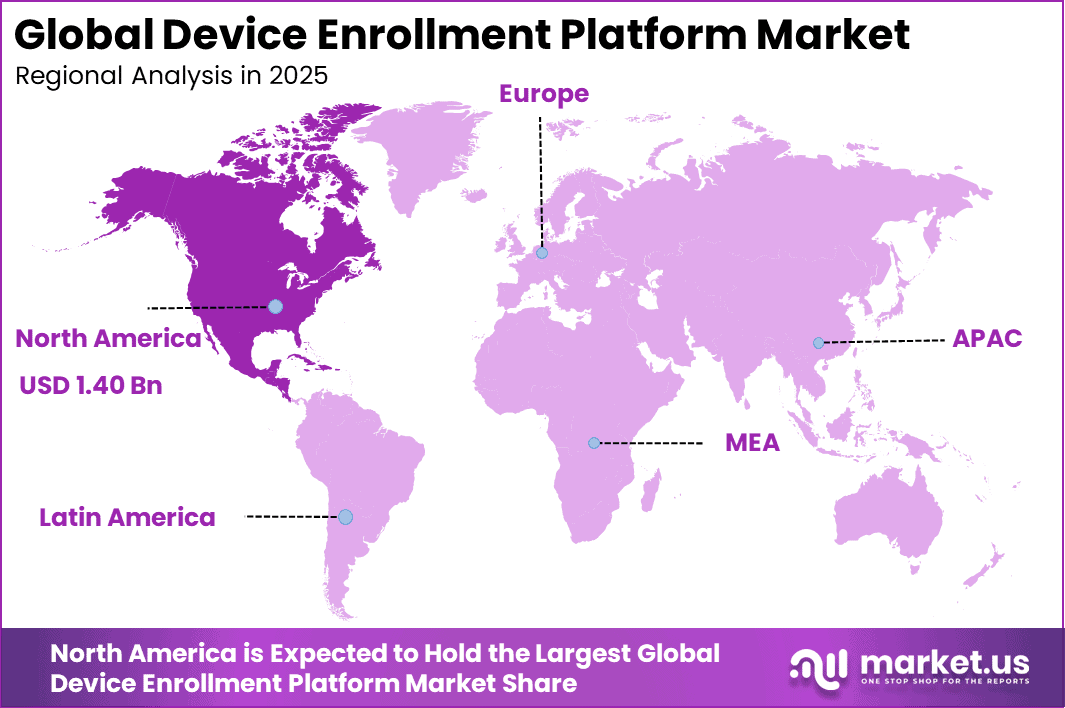

The Global Device Enrollment Platform Market size is expected to be worth around USD 15.2 billion by 2035, from USD 3.6 billion in 2025, growing at a CAGR of 15.5% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 38.9% share, holding USD 1.40 billion in revenue.

The device enrollment platform market refers to solutions that enable organizations to securely register, configure, and onboard devices into enterprise networks and management systems. These platforms automate the initial setup process for devices such as smartphones, laptops, tablets, and IoT endpoints, ensuring that they are properly authenticated, configured, and compliant with organizational policies from the moment they are activated.

Device enrollment platforms are a critical component of enterprise mobility management and unified endpoint management frameworks. As organizations expand digital operations and adopt distributed work environments, managing large numbers of devices has become increasingly complex. Device enrollment platforms streamline onboarding by enabling zero-touch or automated provisioning, where devices are configured remotely without manual intervention.

Demand is rising as companies manage a growing number of endpoints, including IoT devices that already count in the billions worldwide. Small and medium businesses account for around 60% of new adopters because they need affordable tools that reduce IT effort. Healthcare and finance show strong demand as frequent hiring and turnover, near 25% annually, raise onboarding needs.

For instance, in January 2026, JAMF Software LLC launched Jamf Pro 11 with revolutionary Apple Vision Pro enrollment support, positioning itself as the go-to solution for AR/VR corporate deployments. This first-mover advantage cements Jamf’s leadership among 85% of Fortune 500 companies using Apple ecosystems.

Key Takeaway

- In 2025, Mobile Devices led the Global Device Enrollment Platform Market, accounting for 46.7% of total share.

- In 2025, Cloud based deployment dominated with a 66.5% market share.

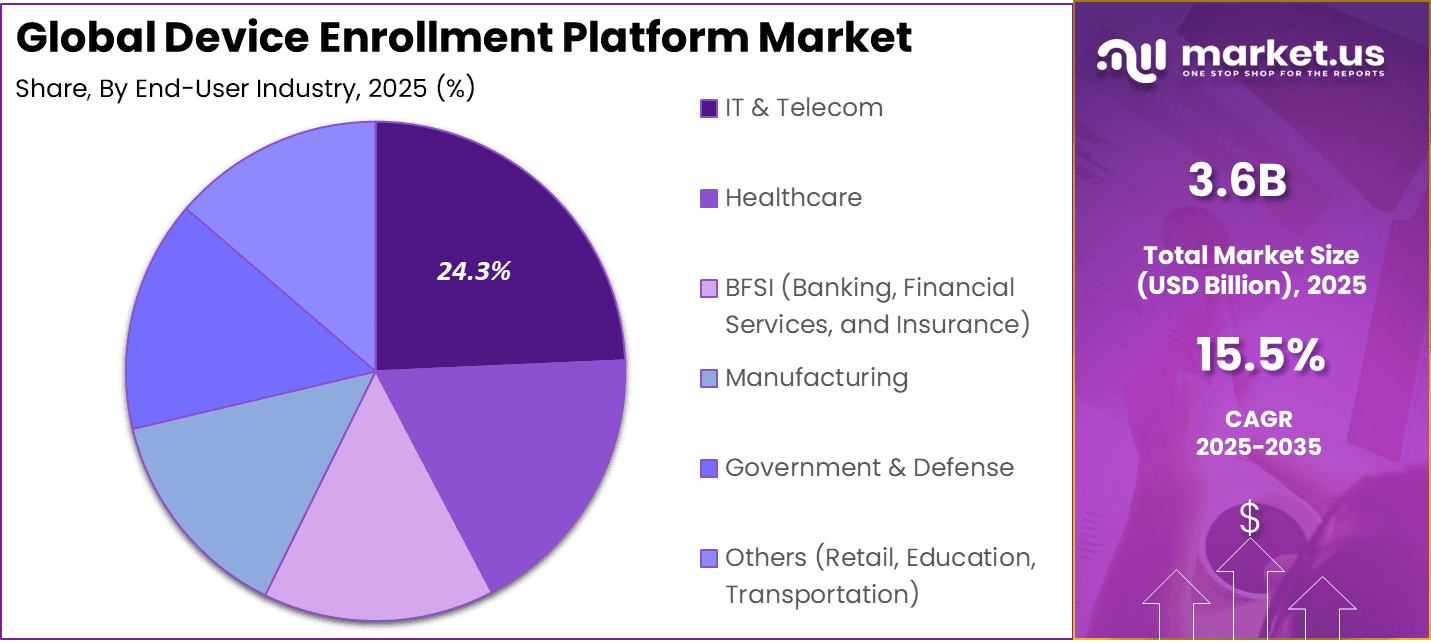

- In 2025, the IT and Telecom sector represented the leading end user segment, capturing 24.3% of overall demand.

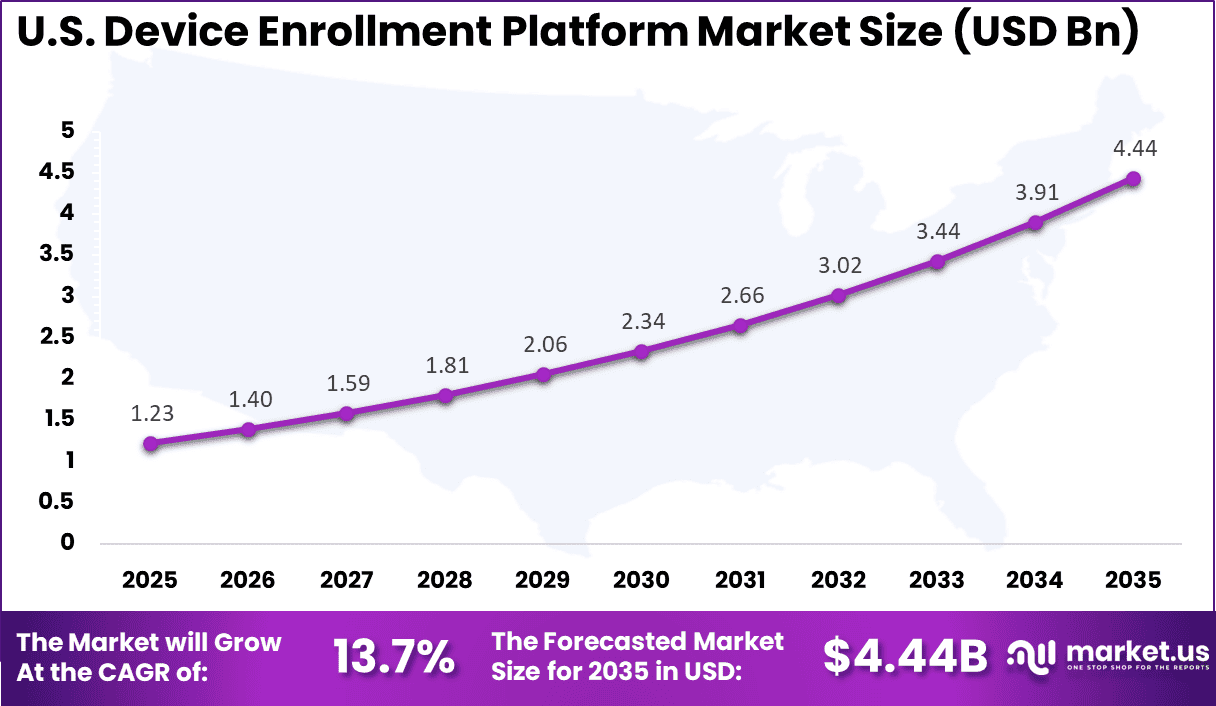

- In 2025, the U.S. Device Enrollment Platform Market reached USD 1.23 billion and recorded a growth rate of 13.7%.

- In 2025, North America maintained regional leadership, securing more than 38.9% of the Global Device Enrollment Platform Market.

By Device Type: Mobile Devices

Mobile devices account for 46.7% of the market, reflecting the widespread use of smartphones and tablets across enterprise operations. Organizations increasingly rely on mobile devices for communication, remote access, and business applications. Device enrollment platforms enable automated provisioning of these devices, ensuring that security policies and configurations are applied consistently.

The adoption of mobile device enrollment solutions is also driven by the need to support bring your own device environments. Enterprises must manage a diverse range of devices while maintaining security and compliance standards. As mobile workforce adoption continues to grow, mobile device enrollment remains a key focus area within the market.

For Instance, in January 2026, Apple pushed updates to its device enrollment program, adding new certificate tech for iOS and macOS setups. The change strengthens security during onboarding, so enterprises can trust quicker rollouts for employee mobiles. It fits right into the rush for secure, hands-off mobile access across networks.

By Deployment Mode: Cloud Based

Cloud based deployment represents 66.5% of the market, indicating strong enterprise preference for scalable and centralized device management systems. Cloud platforms allow organizations to enroll and manage devices across multiple locations through unified dashboards. This approach simplifies device provisioning and ensures consistent policy enforcement.

Cloud deployment also supports real time updates and integration with enterprise mobility management and security platforms. Organizations benefit from reduced infrastructure complexity and improved accessibility. As enterprises adopt cloud driven IT strategies, cloud based device enrollment platforms continue to gain strong adoption.

For instance, in February 2026, VMware patched its Workspace ONE platform with security fixes for cloud deployments, tackling key vulnerabilities in Workstation tools. This keeps cloud enrollment flows reliable for large fleets, letting teams scale devices without worry. Companies lean on these updates to maintain trust in remote cloud management.

By End User Industry: IT and Telecom

The IT and telecom sector accounts for 24.3% of market adoption due to its reliance on large scale device management and connectivity infrastructure. Organizations in this sector manage extensive networks of mobile devices, communication systems, and enterprise applications. Device enrollment platforms help streamline device onboarding and ensure secure access to enterprise resources.

IT and telecom companies also use these platforms to support remote workforce management and maintain device compliance across distributed environments. Automated enrollment systems improve operational efficiency and reduce manual configuration efforts. As digital infrastructure expands, the IT and telecom sector remains a significant user of device enrollment platforms.

For Instance, in March 2026, IBM teamed up with NVIDIA on AI tools that boost cloud analytics, aiding IT and telecom firms with smarter device oversight. The combo helps manage enrolled devices across networks with sharper insights. Telecom giants use this to handle data flows and secure connections in high-stakes operations.

By Region: North America

North America holds 38.9% of the market share due to strong adoption of enterprise mobility solutions and advanced IT infrastructure. Organizations in the region invest in device management platforms to support remote work, improve security, and streamline operations. The presence of mature technology ecosystems further supports regional market growth.

For instance, in October 2025, Citrix Endpoint Management reinforced North American leadership by adding ChromeOS Zero-Touch Enrollment support to its platform. The update enables seamless device provisioning for education and enterprise sectors, strengthening Citrix’s secure access solutions across diverse device ecosystems.

Within North America, the United States contributes USD 1.23 billion with a growth rate of 13.7%. The country’s large enterprise base and increasing adoption of mobile workforce strategies have strengthened demand for device enrollment platforms. Continued investment in enterprise mobility and security solutions is expected to sustain market expansion across the region.

For instance, in February 2025, Microsoft Intune enhanced its device enrollment capabilities with AI-driven zero-touch provisioning, dominating North American enterprise deployments. The platform now supports seamless Windows, iOS, and Android enrollment across hybrid workforces, maintaining Microsoft’s leadership in secure device management solutions.

Growth Factors

One of the primary growth factors driving the device enrollment platform market is the rapid adoption of remote and hybrid work models. Employees increasingly use devices from different locations, requiring secure and efficient onboarding processes. Device enrollment platforms enable organizations to provision devices remotely and enforce security policies regardless of user location.

Another growth factor is the expansion of enterprise mobility and IoT ecosystems. Organizations deploy a wide range of connected devices that must be managed centrally. Enrollment platforms provide the foundation for managing these devices by ensuring that they are properly registered and integrated into management systems.

Emerging Trends

One emerging trend in the device enrollment platform market is the adoption of zero-touch enrollment technologies. These solutions allow devices to be automatically configured and enrolled into enterprise systems as soon as they are powered on. Zero-touch enrollment reduces manual effort and improves scalability for organizations managing large device fleets.

Another trend is the integration of enrollment platforms with identity and access management systems. By linking device enrollment with user identity verification, organizations can ensure that only authorized users and devices gain access to enterprise resources, strengthening overall security.

Key Market Segments

By Device Type

- Mobile Devices

- Desktops & Laptops

- IoT Devices

- Wearables

- Others

By Deployment Mode

- Cloud-Based

- On-Premises

By End-User Industry

- IT & Telecom

- Healthcare

- BFSI (Banking, Financial Services, and Insurance)

- Manufacturing

- Government & Defense

- Others (Retail, Education, Transportation)

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Remote Work Expansion

The market is driven by the rapid rise of remote and hybrid work across industries. Companies need fast and secure ways to onboard employee devices from different locations. This increases demand for platforms that simplify enrollment while maintaining consistent access to business systems and applications.

Remote work also creates pressure on IT teams to manage multiple device types efficiently. Employees expect quick access without delays, which pushes organizations to adopt automated onboarding solutions. This trend supports higher productivity and ensures smooth operations as distributed work environments continue to expand across sectors.

For instance, in March 2025, Microsoft will be tightening integration between Microsoft Entra ID and Intune, enabling organizations to enroll Windows, iOS, and Android devices directly over the internet as part of remote‑onboarding flows. This lets IT teams ship new laptops to employees at home and have them automatically enroll in company policies and apps.

Restraint

Security and Privacy Complexity

Security and privacy complexity remain a major restraint because device enrollment often involves sensitive business data and employee information. Companies must make sure every enrolled device follows internal rules and compliance standards. This creates extra pressure during setup, especially when devices connect from different networks and unmanaged environments.

Privacy concerns also slow adoption in sectors where data protection is closely monitored. Businesses may hesitate if enrollment tools appear intrusive or difficult to govern. Managing permissions, access control, and policy enforcement across multiple devices adds more layers of work, making deployment harder for firms with limited internal security expertise.

For instance, in January 2025, JAMF described how user‑driven and account‑driven enrollment for iOS devices has helped organizations balance security and user experience. The company published guidance on setting up BYOD user enrollment with Managed Apple IDs, service‑discovery files, and clear consent steps. Even with these tools, many IT teams find it challenging to align enrollment flows with data‑privacy regulations and internal risk policies.

Opportunities

IoT Device Growth

The growing number of connected IoT devices creates strong opportunities for device enrollment platforms. Businesses are expanding their use of smart devices across operations, which increases the need for efficient onboarding and management systems that can handle diverse device ecosystems.

As IoT adoption rises, companies require platforms that support automated enrollment and real-time monitoring. This opens opportunities for solutions that simplify device integration and improve visibility. Organizations can enhance operational efficiency by managing multiple connected devices through a single, streamlined onboarding framework.

For instance, in December 2025, Cisco reinforced the role of device enrollment in scaling IoT deployments across logistics, manufacturing, and smart‑infrastructure sites. The company showcased how its endpoint‑management ecosystem can onboard large fleets of sensors, gateways, and industrial controllers using standardized protocols.

Challenges

Skills and Integration Gaps

Skills and integration gaps remain a key challenge because many organizations lack teams with deep knowledge of device onboarding tools. Setting up workflows, policies, and system connections often requires technical understanding. When internal expertise is limited, businesses face delays, configuration mistakes, and higher dependence on outside support during implementation.

Integration is also difficult when companies use older systems alongside newer cloud tools. Enrollment platforms must work smoothly with identity systems, security controls, and device management software. If connections are weak or incomplete, the onboarding process becomes fragmented, creating frustration for users and extra workload for already stretched IT teams.

For instance, in March 2025, Citrix pointed to integration gaps between device‑enrollment systems, identity providers, and legacy application stacks as a practical barrier for many customers. The company’s recent updates to its digital‑workspace platform focused on simplifying how enrolled devices connect to virtual desktops and cloud‑based apps, yet IT teams still report needing specialized skills to map conditional‑access policies, directory groups, and endpoint profiles correctly.

Key Players Analysis

The Device Enrollment Platform Market is led by enterprise technology providers that deliver unified endpoint management and device provisioning solutions across corporate environments. Microsoft Corporation, VMware, Inc., IBM Corporation, and Cisco Systems, Inc. provide platforms that automate device onboarding, policy enforcement, and lifecycle management. These solutions support secure enrollment of smartphones, laptops, and IoT devices within enterprise networks.

Endpoint management and mobility solution providers contribute advanced device security and management capabilities. Ivanti, Inc., Sophos Ltd., BlackBerry Limited, Citrix Systems, Inc., JAMF Software LLC, and MobileIron offer solutions that enable secure device provisioning, application management, and compliance monitoring. These platforms are widely used in regulated industries where device security and data protection are critical.

Device manufacturers and ecosystem providers further strengthen the competitive landscape. Apple Inc., Google LLC, Samsung Electronics, Dell Technologies, and Zebra Technologies integrate device enrollment capabilities within operating systems and hardware ecosystems. These companies enable seamless provisioning and remote configuration of devices at scale. The market remains competitive, with differentiation driven by automation, security integration, and support for diverse device environments.

Top Key Players in the Market

- Microsoft Corporation

- VMware, Inc.

- IBM Corporation

- Citrix Systems, Inc.

- Cisco Systems, Inc.

- MobileIron, Inc.

- JAMF Software LLC

- Ivanti, Inc.

- Sophos Ltd.

- Apple Inc.

- Google LLC

- BlackBerry Limited

- Samsung Electronics Co., Ltd.

- Dell Technologies Inc.

- Zebra Technologies Corporation

- Others

Recent Developments

- In November 2025, IBM Corporation partnered with major U.S. healthcare providers to deploy secure device enrollment for 50,000+ medical IoT devices via its MaaS360 platform. This initiative showcases IBM’s leadership in regulated industry compliance, ensuring HIPAA-grade security during mass rollouts.

- In December 2025, Cisco Systems, Inc. introduced Meraki Systems Manager 3.0, featuring seamless Google Workspace integration for ChromeOS enrollment. This innovation helps U.S. education districts deploy 100,000+ student devices annually while maintaining robust network-level security controls.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.6 Bn |

| Forecast Revenue (2035) | USD 15.2 Bn |

| CAGR (2026-2035) | 15.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Device Type (Mobile Devices, Desktops & Laptops, IoT Devices, Wearables, Others), By Deployment Mode (Cloud-Based, On-Premises), By End-User Industry (IT & Telecom, Healthcare, BFSI (Banking, Financial Services, and Insurance), Manufacturing, Government & Defense, Others (Retail, Education, Transportation) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Microsoft Corporation, VMware, Inc., IBM Corporation, Citrix Systems, Inc., Cisco Systems, Inc., MobileIron, Inc., JAMF Software LLC, Ivanti, Inc., Sophos Ltd., Apple Inc., Google LLC, BlackBerry Limited, Samsung Electronics Co., Ltd., Dell Technologies Inc., Zebra Technologies Corporation, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |