Quick Navigation

- Market Overview

- Key Takeaways

- Flap Type Analysis

- Application Analysis

- Procedure Type Analysis

- End User Analysis

- Instrument Type Used Analysis

- Distribution Channel Analysis

- Key Market Segments

- Driver

- Challenge

- Perioperative infection risks

- Restraints

- Opportunity

- Regional Analysis

- Key Player Analysis

- Recent Developments

- Report Scope

Market Overview

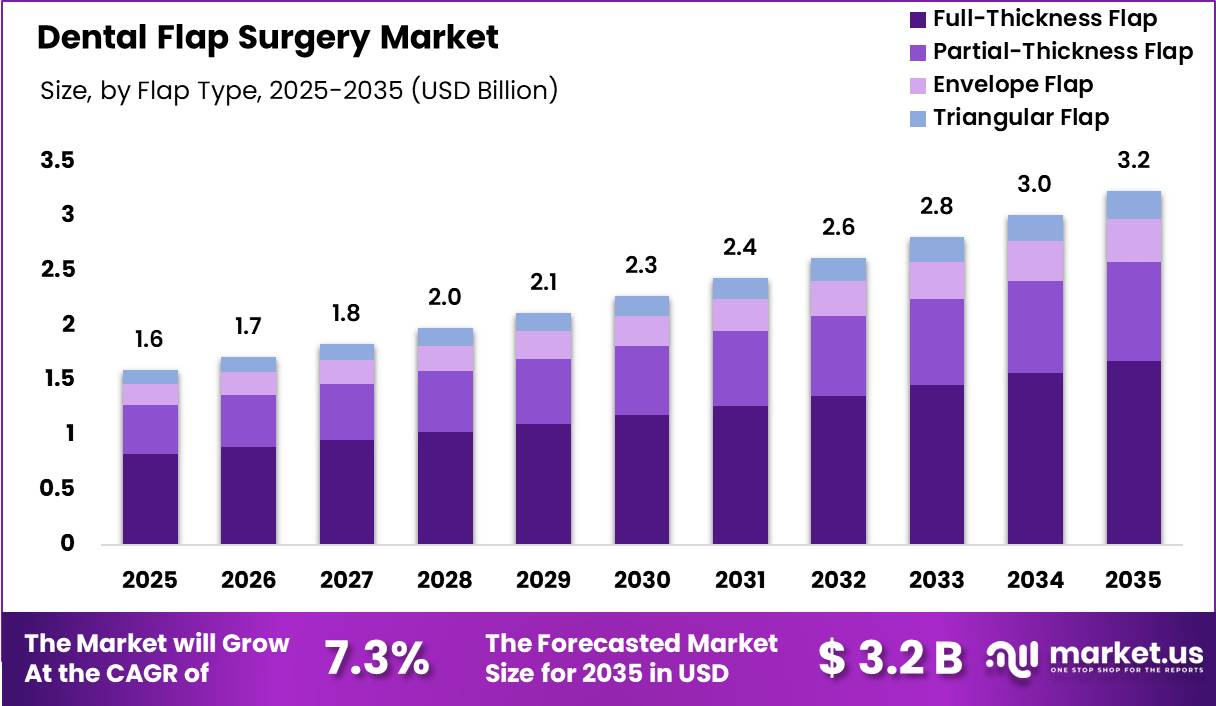

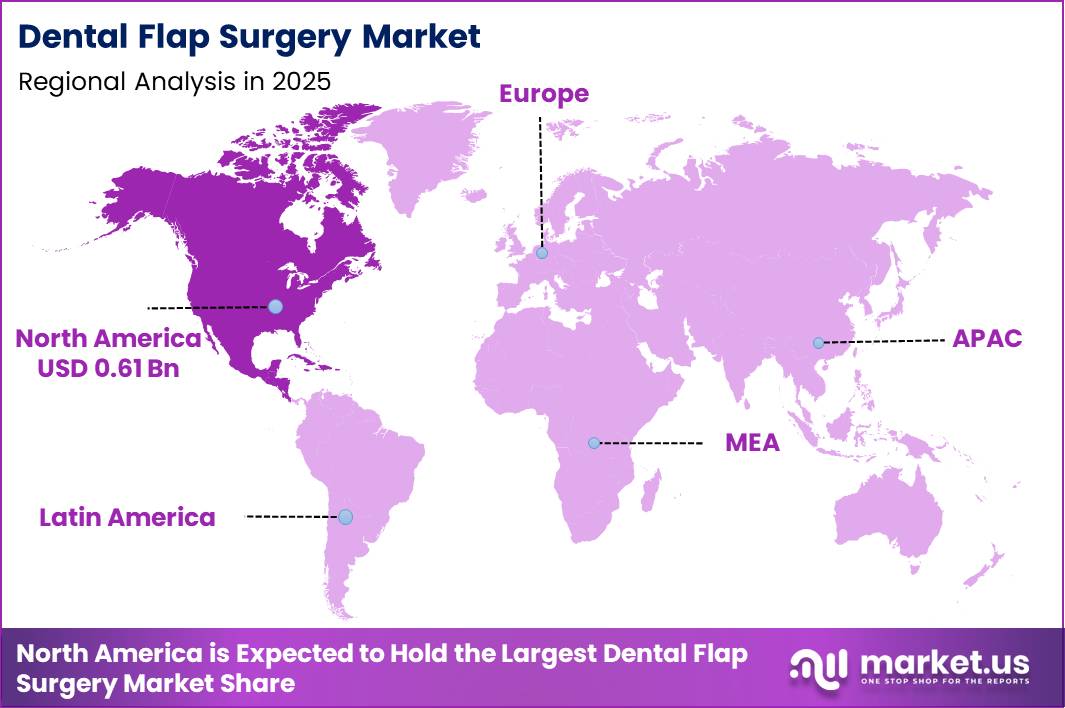

Global Dental Flap Surgery Market size is expected to be worth around US$ 3.2 Billion by 2035 from US$ 1.6 Billion in 2025, growing at a CAGR of 7.3% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 38.00% share with a revenue of US$ 0.61 Billion.

Dental flap surgery is a well-established periodontal procedure used to treat moderate to severe periodontitis by lifting the gum tissue to enable deep cleaning of tooth root surfaces and underlying bone. The procedure helps reduce periodontal pocket depths and preserve natural dentition when non-surgical therapy alone is insufficient.

According to the U.S. Centres for Disease Control and Prevention, 47% of adults aged 30 years and older in the United States show signs of periodontitis, with prevalence rising to 70% among adults aged 65 and above. The World Health Organisation estimates that severe periodontal disease affects over 1 billion people worldwide, making it one of the most common chronic inflammatory conditions globally.

Dental flap surgery is usually performed under local anaesthesia as an outpatient intervention. Clinical protocols from the National Institutes of Health (NIH) confirm that flap procedures significantly reduce probing depths and enhance periodontal attachment levels in cases unresponsive to scaling and root planing.

Infections are controlled through strict sterilisation and antibiotic stewardship, aligning with CDC dental infection control standards. With high periodontal disease prevalence and proven clinical benefits, dental flap surgery remains a critical component of comprehensive periodontal care worldwide.

Key Takeaways

- Market Size: The Global Dental Flap Surgery Market size was US$ 1.6 billion in 2025. The market is estimated to grow to US$ 3.2 billion by 2035.

- Market Share: The Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be 7.3%.

- Flap Type: Full-Thickness (Mucoperiosteal) Flap has the largest market share, accounting for 52% of total sales.

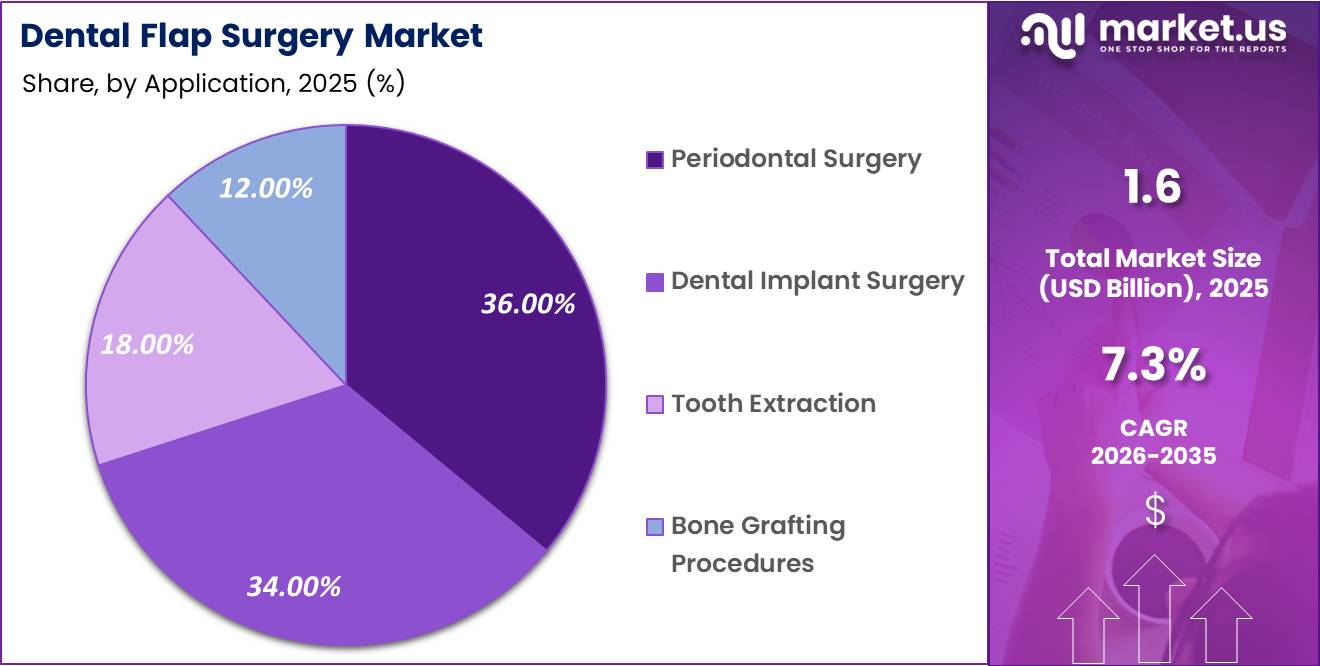

- Application: Periodontal Surgery leads the segment, accounting for 36% of total revenue.

- Procedure Type: Open Flap Debridement dominates the segment, accounting for 41% of total revenue.

- End User: Dental Clinics lead the segment, accounting for 57% of total revenue.

- Instrument Type Used: Manual Surgical Instruments dominate the segment, accounting for 66% of total revenue.

- Distribution Channel: Direct Institutional Sales dominate the segment, accounting for 74% of total revenue.

- Regional Anlaysis: North America is the dominant regional market, accounting for 38% of global sales.

Flap Type Analysis

Flap-type segmentation plays a critical role in determining clinical outcomes, surgical visibility, and postoperative healing in the dental flap surgery market. Full-Thickness (Mucoperiosteal) Flaps dominate the market, accounting for 52.00% of total market share in 2025, due to their widespread use in advanced periodontal therapy, implant placement, and osseous surgery. These flaps provide complete access to underlying bone and root surfaces, making them the preferred choice for procedures requiring extensive debridement and regenerative intervention.

Partial-Thickness (Split-Thickness) Flaps account for 28.00% of the market and are primarily used in mucogingival surgeries where the preservation of the periosteal blood supply is critical. Their growing adoption reflects increasing emphasis on minimally invasive techniques and soft tissue aesthetics.

Envelope Flaps, holding 12.00%, are commonly utilised in routine surgical extractions and minor periodontal procedures due to their simplicity and reduced surgical time. Meanwhile, Triangular Flaps, with an 8.00% share, are selectively applied in complex surgical extractions and impacted tooth removal where enhanced access is required. Overall, flap type selection continues to be driven by procedure complexity, anatomical considerations, and clinician expertise.

Application Analysis

Application-based segmentation highlights the diverse clinical use of dental flap surgery across therapeutic and surgical domains. Periodontal Surgery leads the market with a 36.00% share in 2025, driven by the high global prevalence of periodontal disease and the continued demand for flap-based access for root debridement, pocket reduction, and regenerative procedures. The increasing awareness of oral-systemic health links further supports sustained demand in this segment.

Dental Implant Surgery closely follows with a 34.00% market share, reflecting the growing preference for implant-supported restorations. Flap surgery remains essential for implant site preparation, guided bone regeneration, and soft tissue contouring. Surgical Tooth Extraction accounts for 18.00%, supported by the need for controlled access during impacted tooth removal and complex extractions.

Bone Grafting Procedures, representing 12.00%, rely heavily on flap elevation to enable graft placement, membrane stabilisation, and defect management. Collectively, application trends indicate a strong shift toward restorative and regenerative dentistry, positioning flap surgery as a foundational technique across multiple dental specialities.

Procedure Type Analysis

Procedure type segmentation reflects the therapeutic objectives addressed through dental flap surgery. Open Flap Debridement dominates this category, holding a 41.00% market share in 2025, due to its effectiveness in managing moderate to severe periodontal disease. This procedure enables thorough removal of plaque, calculus, and inflamed tissue under direct visualisation, making it a standard approach in periodontal care.

Flap Surgery for Regeneration represents a significant and growing segment, driven by advancements in bone graft materials and biologics aimed at restoring lost periodontal structures. Reconstructive Oral Surgery utilises flap techniques for anatomical correction, trauma repair, and functional restoration, contributing steadily to overall demand.

Cosmetic Periodontal Surgery is gaining prominence as patient interest in gingival aesthetics increases, particularly in smile correction and soft tissue contouring procedures. Although smaller in share compared to therapeutic procedures, cosmetic applications benefit from rising disposable income and elective dental treatments. Overall, procedural segmentation highlights the balance between disease management and aesthetic-driven interventions within the dental flap surgery market.

End User Analysis

End-user segmentation underscores the settings in which dental flap surgeries are most frequently performed. Dental Clinics dominate the market with a 57.00% share in 2025, supported by the high volume of outpatient periodontal and implant procedures conducted in private and group practices. Clinics benefit from faster patient turnover, specialised dental equipment, and the growing preference for office-based surgical care.

Hospitals represent a substantial portion of the remaining market, particularly for complex oral surgeries, medically compromised patients, and cases requiring multidisciplinary collaboration. Hospital-based procedures often involve advanced diagnostic imaging and surgical support infrastructure, making them suitable for high-risk interventions.

Academic & Research Institutes account for a smaller but strategically important segment, contributing to clinical training, procedural innovation, and adoption of evidence-based surgical techniques. These institutions play a pivotal role in advancing flap surgery methodologies and validating new materials and instruments. Overall, the dominance of dental clinics reflects the decentralisation of surgical dental care, while hospitals and academic centres continue to support complex case management and innovation.

Instrument Type Used Analysis

Instrument type segmentation illustrates the technological preferences shaping dental flap surgery practices. Manual Surgical Instruments lead the market with a 66.00% share in 2025, owing to their cost-effectiveness, precision control, and widespread familiarity among dental professionals. Instruments such as scalpels, periosteal elevators, and curettes remain essential across nearly all flap procedures.

Powered Surgical Instruments are increasingly adopted in complex surgeries requiring enhanced efficiency and reduced operative time. These tools offer consistent performance in bone modification and tissue management, particularly in implant and reconstructive procedures.

Laser-Assisted Tools represent a growing niche segment, driven by their ability to reduce bleeding, improve healing outcomes, and enhance patient comfort. While adoption remains limited due to higher capital costs and training requirements, laser technology continues to gain acceptance in minimally invasive and cosmetic periodontal applications. The overall instrument landscape reflects a balance between traditional manual tools and emerging technologies that enhance surgical precision and patient experience.

Distribution Channel Analysis

Distribution channel segmentation highlights procurement patterns within the dental flap surgery market. Direct Institutional Sales dominate with a 74.00% market share in 2025, as hospitals and large dental clinic networks prefer direct sourcing from manufacturers to ensure product authenticity, volume discounts, and technical support. This channel also supports customized instrument kits and long-term supply agreements.

Distributors play a vital role in serving small and mid-sized dental practices, offering flexible purchasing options and localised inventory availability. They help expand market reach, particularly in developing regions where direct manufacturer presence is limited.

Online Procurement represents a smaller but rapidly emerging segment, driven by digitalisation, transparent pricing, and convenience. Online platforms enable clinics to compare products, access a wider supplier base, and streamline ordering processes. While regulatory compliance and product verification remain critical considerations, online procurement is expected to grow steadily. Overall, distribution trends emphasise efficiency, reliability, and cost optimisation, reinforcing the dominance of direct institutional sales while supporting diversified purchasing channels.

Key Market Segments

By Flap Type

- Full-Thickness (Mucoperiosteal) Flap

- Partial-Thickness (Split-Thickness) Flap

- Envelope Flap

- Triangular Flap

By Application

- Periodontal Surgery

- Dental Implant Surgery

- Tooth Extraction (Surgical)

- Bone Grafting Procedures

By Procedure Type

- Open Flap Debridement

- Flap Surgery for Regeneration

- Reconstructive Oral Surgery

- Cosmetic Periodontal Surgery

By End User

- Dental Clinics

- Hospitals

- Academic & Research Institutes

By Instrument Type Used

- Manual Surgical Instruments

- Powered Surgical Instruments

- Laser-Assisted Tools

By Distribution Channel

- Direct Institutional Sales

- Distributors

- Online Procurement

Driver

Severe periodontitis case pool driving flap conversion

The strongest near-term demand driver is the sheer size of the treatable advanced periodontitis pool that can no longer be managed adequately by hygiene instruction and routine non-surgical debridement alone. WHO states oral diseases affect nearly 3.7 billion people globally, while CDC describes periodontitis as an irreversible condition involving bone loss and notes that surgical procedures become part of treatment for more severe disease.

NIDCR estimates that 42.2% of U.S. adults aged 30+ had total periodontitis, including 7.8% severe disease, and StatPearls notes probing depths above 5 mm often require more intensive treatment because they are harder to manage mechanically. For the flap-surgery market, that matters because every increase in residual deep-pocket prevalence expands the subset of patients escalated from scaling/root planing into open-flap debridement, osseous access, or defect-directed surgery, which lifts average revenue per treated patient far more than preventive or hygiene visits do.

In economic terms, the driver works through conversion rather than incidence alone: if even a low-single-digit share of moderate-to-severe periodontal patients migrates into surgery because of persistent pockets of 5 mm or more, specialty chair-time, graft usage, membrane attach rates, and follow-up maintenance all rise, creating an estimated +2.1 percentage-point uplift to CAGR in 2026-based forecasts

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe periodontitis case pool driving flap conversion | +2.1% | North America core, EU, Japan, urban China, GCC | Short term (≤ 2 years) |

| Diabetes-linked periodontal complexity raising surgical intensity | +1.7% | U.S., EU5, India, China, Middle East | Medium term (2-4 years) |

| Regenerative defect management improving flap economics | +1.4% | U.S., Western Europe, South Korea, Japan, tier-1 APAC | Medium term (2-4 years) |

| Dental-medical integration and coding formalization | +1.2% | U.S. core, EU reimbursement-watch, selected APAC private pay | Short term (≤ 2 years) |

| Minimally invasive laser and soft-tissue adjunct adoption | +1.0% | U.S., EU, South Korea, Japan, premium APAC clinics | Short term (≤ 2 years) |

| Ageing dentition retention extending periodontal surgery demand | +1.3% | Europe, Japan, U.S., China urban, Australia | Long term (≥ 4 years) |

Challenge

Perioperative infection risks

Persistent perioperative infection risk and variable adherence to surgical infection-prevention protocols create friction in both patient willingness and institutional throughput, even though flap surgery itself is a highly controllable procedure when standard aseptic techniques are rigorously applied.

Facilities with inconsistent sterilization practices or suboptimal antibiotic stewardship may report post-operative infection rates of 3–6% versus 1–2% in centers aligned with international norms, translating into extended healing times (from 7–10 days to 14–21 days in complicated cases), additional follow-up visits (1–2 extra appointments per patient), and higher direct costs (extra antibiotic courses and consumables adding 10–20% per-case cost), which disincentivizes both providers (due to medicolegal risk and bed-blocking) and patients (due to perceived safety concerns).

At a system level, these infection-related inefficiencies can lower effective operating room availability by 5–10% as blocks are reserved for potential complication management, and increase average length of stay to 1.5–2.0 days in cases that otherwise could be outpatient, cumulatively imposing an estimated 0.9 percentage point drag on CAGR.

Strategic mitigation over a 2–4 year horizon includes universal adoption of standardized periodontal surgery bundles (pre-op chlorhexidine mouthwash, single-dose prophylactic antibiotics where indicated, sterile instrument tracking), compulsory infection-control audits tied to accreditation by national health authorities and hospital commissions, continuous monitoring of surgical site infection rates with thresholds (e.g., <2% for reaccreditation), and targeted training for nursing and sterilization teams, supported by low-cost digital checklists integrated into electronic health records to ensure compliance.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Surgical talent gaps | -1.6% | Africa, South Asia, LatAm urban | Long term (≥ 4 years) |

| Uneven surgical access | -1.4% | Rural APAC, Sub-Saharan Africa | Long term (≥ 4 years) |

| Technology adoption lag | -1.2% | EU periphery, Emerging APAC | Medium term (2-4 years) |

| Perioperative infection risks | -0.9% | Global hospital networks | Medium term (2-4 years) |

| Reimbursement complexity | -1.3% | North America, EU hubs | Medium term (2-4 years) |

| Data & outcomes gaps | -0.8% | Global, especially LMICs | Long term (≥ 4 years) |

Restraints

Tightening medical device regulations

Regulatory tightening around dental surgical instruments and adjunctive materials used in flap surgery, particularly in the US, EU and high‑income APAC markets, is increasingly elongating product approval cycles and expanding compliance overhead, thereby eroding manufacturer margins and delaying the introduction of new flap‑surgery kits and regenerative adjuncts into clinical practice.

In the US, reclassification nuances and more conservative interpretations of 510(k) substantial equivalence for Class II instruments (e.g., ultrasonic scalers, bone grafting tools and periodontal surgery systems) are adding 12–18 months to launch timelines and pushing regulatory spending toward 7–9% of total project CapEx for mid‑sized firms, compared with 3–4% a decade ago.

Parallel requirements for Unique Device Identification (UDI), post‑market surveillance, and stricter labeling/advertising scrutiny mean that global dental OEMs now carry recurring compliance Opex that can approach USD 0.8–1.0 million per year per product family across large markets, translating into 80–150 basis points of margin compression on high‑value flap surgery portfolios.

This is compounded in the EU by evolving MDR enforcement and in regions such as Japan or South Korea by additional local quality system audits, which collectively force manufacturers to prioritize fewer SKUs, defer borderline innovation projects, and slow regional line extensions, effectively trimming achievable market CAGR by an estimated 2.2 percentage points as CapEx is reallocated to regulatory remediation rather than new surgical platform investments.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening medical device regulations | -2.2% | North America, EU, advanced APAC | Medium term (2-4 years) |

| Limited surgical capacity & periodontal specialists | -1.9% | India, broader Asia, LATAM, MENA | Long term (≥ 4 years) |

| Patient affordability constraints & reimbursement gaps | -2.5% | LMICs, US self-pay, Eastern Europe | Medium term (2-4 years) |

| Supply chain volatility in surgical disposables & equipment | -1.6% | Global, with higher impact in import-dependent markets | Short term (≤ 2 years) |

| Slow adoption of guideline-driven periodontal surgery | -1.8% | Global, stronger in primary-care dominated systems | Long term (≥ 4 years) |

Opportunity

Tiered access platforms in underserved regions

Tiered access platforms combining low‑cost periodontal screening, triage, and scalable flap surgery programs across public and private providers represent a structural opportunity to convert currently untreated disease burden in South Asia, Latin America, and African markets into surgical demand, above and beyond baseline trends driven by population growth and urbanization.

Global estimates indicate over 1 billion cases of severe periodontal disease and several hundred million cases concentrated in middle- and low‑SDI regions where dental specialist density is limited, out‑of‑pocket payments dominate, and universal oral health coverage is still emerging, meaning that only a small share often below 10–15% of clinically indicated surgical cases reaches advanced interventions like flap surgery.

WHO regional action plans for oral health in South‑East Asia target universal coverage for oral health by 2030, along with large relative reductions in untreated dental caries and oral cancer, creating a policy environment favorable to multi‑tier platforms that blend basic screening at primary care, tele‑periodontology consults, and referral of complex pockets (≥6 mm) to regional centers equipped for flap surgery and regenerative procedures.

If such platforms can lower effective patient acquisition costs by deploying community screening and digital triage cutting traditional marketing and referral costs per surgical case by 30–40% and negotiate subsidized tariffs through public programs, they could unlock treatment for an additional 10–15% of currently untreated severe periodontitis cases across these regions by 2035, roughly translating to high single‑digit to low double‑digit annual procedure growth on top of current organic trends.

This upside is not a baseline driver because present market forecasts generally assume slow, linear improvements in access without specific structural innovations in tiered deliver. The opportunity depends on platform-build investments, cross‑provider contracting, and targeted workforce expansion that convert policy aspirations around universal oral health coverage into actual high‑complexity surgical capacity, yielding an estimated 2.3 percentage‑point CAGR uplift in these geographies if executed at scale.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Value-based periodontal surgical bundles | +2.0% | North America, EU, mature APAC | Short term (≤ 2 years) |

| Tiered access platforms in underserved regions | +2.3% | South Asia, Latin America, Africa | Medium term (2-4 years) |

| Digitally guided minimally invasive flap protocols | +1.6% | North America core, EU, advanced APAC | Medium term (2-4 years) |

| Integrated diabetes–periodontal co-management programs | +1.4% | North America, EU, Middle East | Medium term (2-4 years) |

| Surgical capacity consolidation and M&A roll-ups | +1.8% | North America, EU, urban APAC | Long term (≥ 4 years) |

| AI-driven risk stratification and prevention pathways | +1.2% | Global, especially high-burden middle-SDI markets | Long term (≥ 4 years) |

Regional Analysis

In 2025, North America led the market, achieving over 38.00% share with a revenue of US$ 0.61 billion. The global dental flap surgery market shows distinct regional patterns driven by oral disease prevalence, access to dental care, and healthcare spending.

United States and the broader North American region hold a leading position due to high awareness of periodontal health, widespread insurance coverage for dental procedures, and strong adoption of advanced surgical techniques. According to public health data, nearly half of adults in the U.S. experience some form of periodontal disease, sustaining demand for flap-based interventions.

Europe represents a mature and stable market, supported by well-established public dental systems and ageing populations requiring periodontal and implant-related surgeries. Countries with strong preventive care frameworks continue to report steady procedure volumes, particularly for full-thickness flap techniques.

The Asia–Pacific region is the fastest-growing market, led by India and China, where large populations, rising urbanisation, and increasing disposable incomes are improving access to dental services. Expanding private dental clinics and growing awareness of gum disease treatment are accelerating procedural growth.

Latin America shows moderate growth as private dental care expands in urban centres, while the Middle East & Africa region remains comparatively smaller due to limited access to specialised periodontal surgery, though gradual improvements in healthcare infrastructure are expected to support long-term market development.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Competitive advantage in the global dental flap surgery market is achieved through comprehensive surgical instrument portfolio breadth spanning periodontal, implant, and oral surgery applications, established relationships with periodontists and oral surgeons through clinical education and training programs, and integration of complementary product lines including suture materials, regenerative membranes, and bone grafting substitutes that are frequently used alongside flap surgery procedures.

Major strategic priorities for leading manufacturers include continued investment in precision surgical instrument design, expansion of minimally invasive flap surgery technique-compatible instrumentation, and development of regenerative biomaterials supporting guided tissue regeneration procedures performed in conjunction with flap surgery.

Strong distribution relationships with dental schools, periodontal speciality practices, and hospital oral surgery departments represent a critical competitive differentiator for manufacturers seeking sustained institutional procurement across both surgical instrument and complementary biomaterial product categories.

Top Key Players

- Dentsply Sirona

- Straumann Group

- Zimmer Biomet Dental

- Hu-Friedy (STERIS)

- KLS Martin Group

- Integra LifeSciences

- B. Braun Melsungen AG

- 3M Health Care

- Ivoclar Vivadent

- GC Corporation

- Osstem Implant

- Nobel Biocare (Envista)

- Medtronic Dental

- Brasseler USA

- LM-Dental

- Other Key Players

Recent Developments

- In January 2026, Dentsply Sirona launched an expanded periodontal surgical instrument kit designed for minimally invasive flap surgery techniques, targeting periodontal speciality practices and oral surgery centres seeking improved precision and reduced patient recovery times.

- In February 2026, Straumann Group introduced a new regenerative membrane product line designed for use alongside flap surgery procedures, targeting periodontists and implant surgeons performing guided tissue and bone regeneration treatments globally.

- In March 2026, KLS Martin Group expanded its periodontal and oral surgery instrument portfolio with new ergonomic flap surgery instrument sets, targeting hospital oral surgery departments and periodontal speciality clinics across European and North American markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.6 Billion |

| Forecast Revenue (2035) | US$ 3.2 Billion |

| CAGR (2026-2035) | 7.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Flap Type (Full-Thickness (Mucoperiosteal) Flap, Partial-Thickness (Split-Thickness) Flap, Envelope Flap, Triangular Flap), By Application (Periodontal Surgery, Dental Implant Surgery, Tooth Extraction (Surgical), Bone Grafting Procedures), By Procedure Type (Open Flap Debridement, Flap Surgery for Regeneration, Reconstructive Oral Surgery, Cosmetic Periodontal Surgery), By End User (Dental Clinics, Hospitals, Academic & Research Institutes), By Instrument Type Used (Manual Surgical Instruments, Powered Surgical Instruments, Laser-Assisted Tools), By Distribution Channel (Direct Institutional Sales, Distributors, Online Procurement) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Dentsply Sirona, Straumann Group, Zimmer Biomet Dental, Hu-Friedy (STERIS), KLS Martin Group, Integra LifeSciences, B. Braun Melsungen AG, 3M Health Care, Ivoclar Vivadent, GC Corporation, Osstem Implant, Nobel Biocare (Envista), Medtronic Dental, Brasseler USA, LM-Dental, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |