Quick Navigation

- Market Overview

- Key Takeaways

- Product Type (Diagnostics) Analysis

- Product Type (Surgical) Analysis

- Procedure Type Analysis

- End User Analysis

- Technology Type Analysis

- Distribution Channel Analysis

- Market Segmentations

- Opportunity

- Driver

- Challenge

- Restraints

- Regional Analysis

- Key Player Analysis

- Recent Developments

- Report Scope

Market Overview

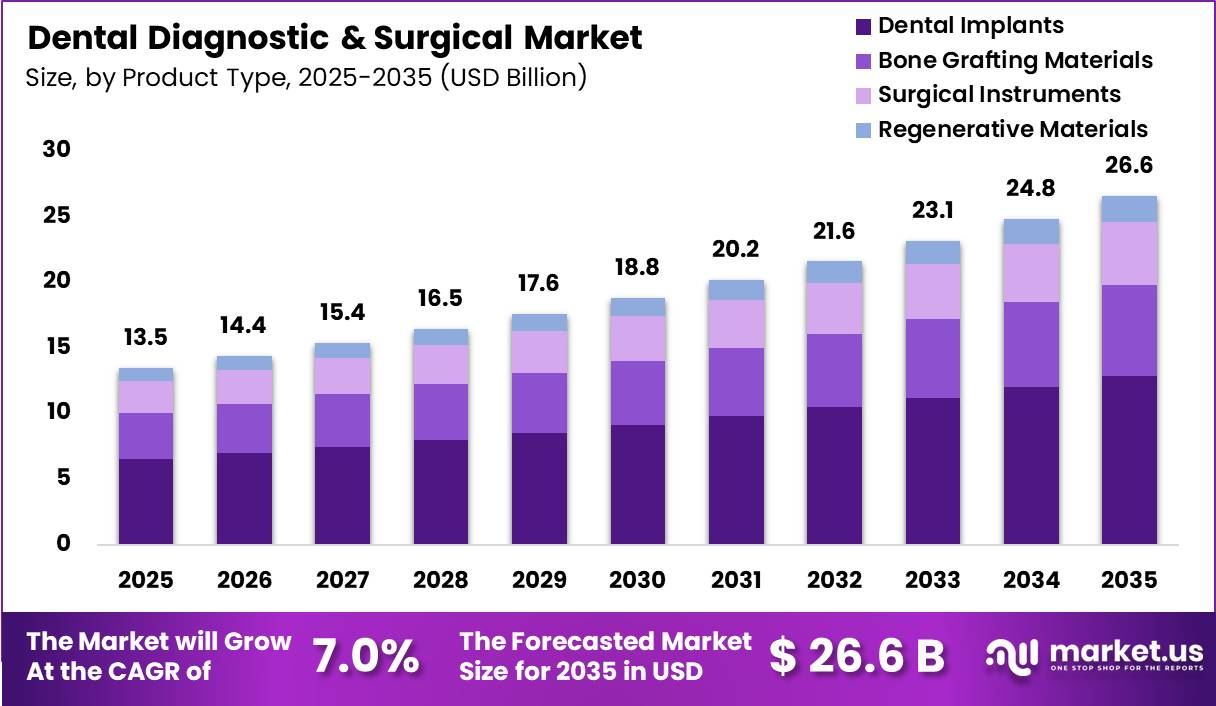

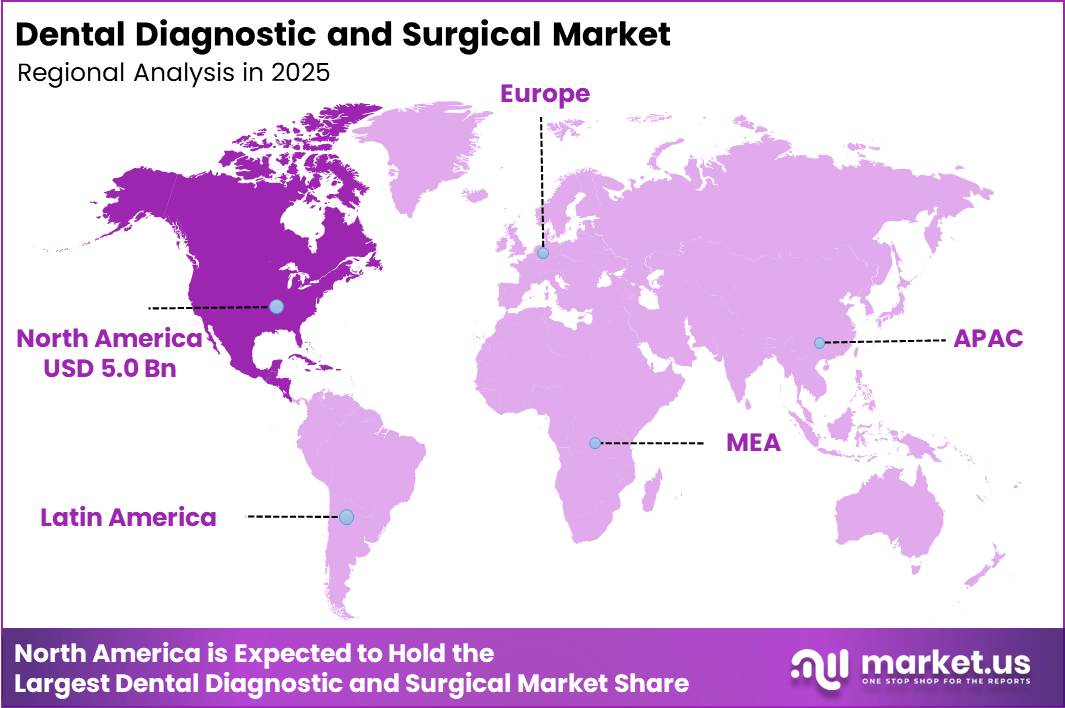

Global Dental Diagnostic and Surgical Market size is expected to be worth around US$ 26.6 Billion by 2035 from US$ 13.5 Billion in 2025, growing at a CAGR of 7.0% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 37% share with a revenue of US$ 5 Billion.

The global Dental Diagnostic and Surgical Market is gaining significant attention as oral diseases continue to affect billions of people worldwide, increasing demand for advanced diagnostic technologies, imaging systems, restorative procedures, and minimally invasive dental surgeries. According to the World Health Organization (WHO), oral diseases impact nearly 3.7 billion people globally, making oral healthcare one of the largest and most persistent healthcare challenges worldwide.

Untreated dental caries in permanent teeth remains the most common health condition globally, while severe periodontal disease affects more than 1 billion people. Furthermore, approximately 389,846 new oral cancer cases and 188,438 related deaths were reported worldwide in 2022, highlighting the growing need for early diagnosis and surgical intervention.

The market is being driven by rising patient awareness, increasing adoption of digital dentistry, and expanding access to preventive oral healthcare services. WHO data indicates that around 45% of the global population equivalent to 3.5 billion people suffers from at least one oral disease, with cases increasing by nearly 1 billion over the past three decades. Tooth loss also remains a major concern, affecting nearly 7% of adults aged 20 years and older and approximately 23% of individuals aged 60 years and above.

Growing utilization of digital radiography, cone-beam computed tomography (CBCT), intraoral scanners, AI-assisted diagnostics, and computer-guided surgical systems is improving diagnostic accuracy and treatment outcomes. As healthcare systems increasingly emphasize early detection and preventive care, demand for dental diagnostic and surgical solutions is expected to remain strong across hospitals, dental clinics, and specialized oral healthcare centers worldwide.

Key Takeaways

- Market Size: Global Dental Diagnostic and Surgical Market size is expected to be worth around US$ 26.6 Billion by 2035 from US$ 13.5 Billion in 2025.

- Market Share: The market is growing at a CAGR of 7.0% during the forecast period from 2026 to 2035.

- Product Type (Diagnostics) Analysis: In 2025, Dental Imaging Systems dominate the segment, accounting for 54% of the market share.

- Product Type (Surgical) Analysis: In 2025, Dental Implants lead the segment with a dominant 48.5% market share.

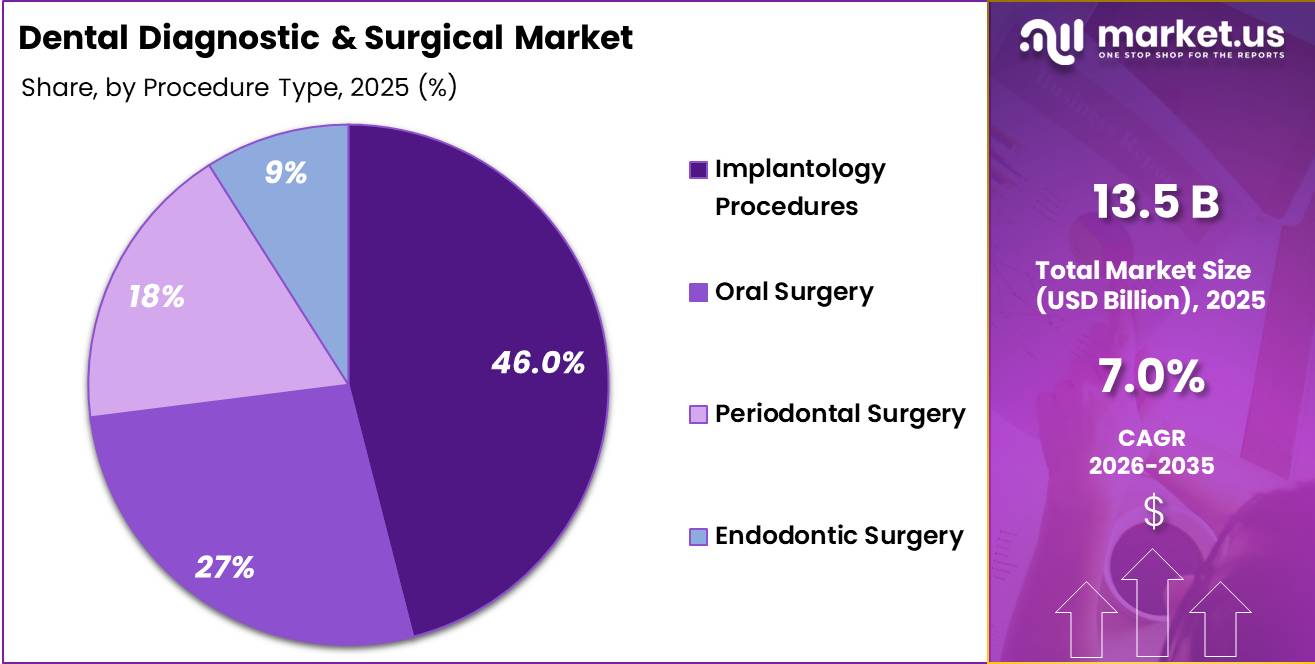

- Procedure Type Analysis: Implantology Procedures dominate the Dental Diagnostic and Surgical Market with a 46% market share

- End User Analysis: Dental Clinics remain the leading segment in the Dental Diagnostic and Surgical Market, accounting for 52% of the market share in 2025.

- Technology Type Analysis: Digital Imaging & CAD/CAM technologies dominate the Dental Diagnostic and Surgical Market, accounting for 61% of the market share.

- Distribution Channel Analysis: Direct Institutional Sales dominate the market with a substantial 74% share.

- Regional Analysis: In 2025, North America led the market, achieving over 37% share with a revenue of US$ 5.0 Billion.

Product Type (Diagnostics) Analysis

The diagnostics segment of the Dental Diagnostic and Surgical Market plays a critical role in early disease detection, treatment planning, and clinical decision-making. In 2025, Dental Imaging Systems dominate the segment, accounting for 54% of the market share. The widespread adoption of Cone-Beam Computed Tomography (CBCT), intraoral X-ray systems, and panoramic imaging solutions has strengthened this segment due to their ability to provide high-resolution images, improve diagnostic accuracy, and support implant planning and orthodontic procedures. Growing investments in digital radiography and AI-assisted imaging technologies are further accelerating demand.

Intraoral Scanners represent the second-largest segment with a 22% share in 2025. Their increasing use in digital dentistry workflows, restorative procedures, and chairside CAD/CAM systems has significantly improved patient comfort while reducing treatment turnaround times. Caries Detection Devices account for 14% of the market, supported by rising emphasis on preventive dentistry and early identification of tooth decay through fluorescence and laser-based technologies.

Meanwhile, Digital Periodontal Probes contribute 10% of the segment, benefiting from growing awareness of periodontal diseases and the need for accurate pocket depth measurement and disease monitoring. Collectively, these technologies are driving the transition toward fully digital and precision-oriented dental diagnostics worldwide.

Product Type (Surgical) Analysis

The surgical segment represents a substantial portion of the Dental Diagnostic and Surgical Market, supported by increasing demand for tooth replacement procedures, periodontal treatments, and oral reconstruction surgeries. In 2025, Dental Implants lead the segment with a dominant 48.5% market share.

The growing prevalence of tooth loss, aging populations, and rising acceptance of implant-supported restorations continue to fuel demand. Advances in implant materials, surface technologies, and guided implant surgery systems have further enhanced treatment outcomes and patient satisfaction.

Bone Grafting Materials account for 26% of the surgical segment. These materials are extensively utilized in implantology procedures to restore alveolar bone volume and support successful implant placement. Increasing adoption of synthetic grafts, xenografts, and allografts is contributing to segment growth. Surgical Instruments hold an 18% market share, driven by the consistent demand for extraction tools, implant placement kits, surgical handpieces, and precision instruments used in oral and maxillofacial procedures.

Meanwhile, Regenerative Materials represent 7.5% of the market and are gaining traction due to their ability to support tissue regeneration, wound healing, and periodontal reconstruction. The integration of biomaterials and regenerative technologies continues to improve clinical outcomes and expand the scope of advanced dental surgical procedures globally.

Procedure Type Analysis

Procedure-based segmentation highlights the evolving demand for specialized dental interventions aimed at restoring oral function and aesthetics. In 2025, Implantology Procedures dominate the Dental Diagnostic and Surgical Market with a 46% market share.

The segment’s leadership is attributed to the increasing incidence of tooth loss, growing patient preference for permanent tooth replacement solutions, and continuous technological advancements in implant planning and placement techniques. Digital workflows and guided surgery systems have significantly improved procedural accuracy and success rates.

Oral Surgery procedures, including tooth extractions, trauma management, cyst removal, and corrective interventions, constitute a significant portion of the market. Demand remains strong due to increasing cases of impacted teeth, oral infections, and maxillofacial injuries requiring surgical treatment.

Periodontal Surgery represents another important segment, driven by the high prevalence of gum diseases and the growing focus on preserving natural dentition through flap surgery, grafting, and regenerative procedures.

Endodontic Surgery also contributes meaningfully to market growth, supported by rising demand for apicoectomy and root-end procedures when conventional root canal treatments prove insufficient. Increasing patient awareness, technological advancements, and the expansion of specialized dental care services continue to drive growth across all procedure categories within the market.

End User Analysis

Based on end users, Dental Clinics remain the leading segment in the Dental Diagnostic and Surgical Market, accounting for 52% of the market share in 2025. Their dominance is driven by the increasing number of private dental practices, growing patient preference for outpatient treatments, and widespread adoption of advanced diagnostic and surgical technologies. Dental clinics offer cost-effective care, shorter waiting times, and specialized treatment options, making them the primary destination for preventive, restorative, and implant procedures.

Hospitals represent the second-largest end-user segment, supported by the availability of multidisciplinary healthcare services and specialized oral and maxillofacial surgery departments. Hospitals are particularly important for complex surgical procedures, trauma cases, and patients requiring comprehensive medical management alongside dental treatment.

Academic and Research Institutes also contribute significantly to market development by facilitating clinical research, technology validation, and professional training programs. These institutions play a crucial role in advancing digital dentistry, biomaterials research, and innovative surgical techniques.

Increasing collaboration between universities, healthcare providers, and dental technology manufacturers is accelerating the adoption of next-generation solutions. Overall, growing demand for specialized oral healthcare services and continuous technological innovation are supporting expansion across all end-user categories within the global market.

Technology Type Analysis

Technology-based segmentation reflects the industry’s transition toward precision-driven and digitally integrated dental care solutions. In 2025, Digital Imaging & CAD/CAM technologies dominate the Dental Diagnostic and Surgical Market, accounting for 61% of the market share.

Their leadership is attributed to the growing use of digital radiography, CBCT systems, intraoral scanners, and computer-aided design and manufacturing platforms that enhance diagnostic accuracy, treatment planning, and restorative outcomes. These technologies enable faster workflows, improved patient experiences, and highly customized prosthetic solutions.

Digital integration has become particularly valuable in implantology, orthodontics, and restorative dentistry, where precision and efficiency are critical. The increasing implementation of artificial intelligence, cloud-based imaging systems, and chairside manufacturing capabilities further strengthens this segment’s position. Conventional Surgical Tools continue to hold a significant share of the market despite ongoing digital transformation.

Instruments such as forceps, elevators, curettes, surgical handpieces, and manual diagnostic devices remain indispensable for a wide range of routine and complex procedures. Their reliability, affordability, and widespread availability ensure continued utilization across diverse healthcare settings. The coexistence of digital technologies and conventional instruments reflects a balanced approach to modern dental practice while supporting comprehensive patient care.

Distribution Channel Analysis

The distribution landscape of the Dental Diagnostic and Surgical Market is largely influenced by institutional purchasing patterns and long-term supplier relationships. In 2025, Direct Institutional Sales dominate the market with a substantial 74% share.

Manufacturers increasingly prefer direct sales channels to strengthen customer relationships, provide technical support, offer product training, and ensure efficient installation and maintenance services. Large dental clinic networks, hospitals, and academic institutions frequently procure advanced diagnostic and surgical equipment directly from manufacturers to secure competitive pricing and customized service agreements.

Distributors remain an important channel within the market, particularly for reaching smaller dental practices and regional healthcare providers. These intermediaries facilitate product availability across broader geographic areas while offering inventory management and local customer support.

Online Procurement Platforms are emerging as a growing segment due to increasing digitalization and changing purchasing preferences among healthcare professionals. These platforms provide convenient product comparisons, transparent pricing structures, and streamlined procurement processes.

The expansion of e-commerce infrastructure and digital supply chain management solutions is supporting their adoption globally. Despite this growth, direct institutional sales continue to maintain market leadership owing to the complexity, cost, and technical requirements associated with advanced dental diagnostic and surgical equipment.

Market Segmentations

Product Type (Diagnostics)

- Dental Imaging Systems (CBCT, Intraoral X-ray, Panoramic)

- Caries Detection Devices

- Periodontal Probes (Digital)

- Intraoral Scanners

Product Type (Surgical)

- Dental Implants

- Bone Grafting Materials

- Surgical Instruments

- Regenerative Materials

Procedure Type

- Implantology Procedures

- Oral Surgery (extractions, trauma)

- Periodontal Surgery

- Endodontic Surgery

End User

- Dental Clinics

- Hospitals

- Academic & Research Institutes

Technology Type

- Digital Imaging & CAD/CAM

- Conventional Surgical Tools

Distribution Channel

- Direct Institutional Sales

- Distributors

- Online Procurement Platforms

Opportunity

DSO roll-up digital retrofit

This is not a baseline driver because it depends on a strategic ownership and integration play consolidating fragmented clinics and retrofitting them with standardized imaging, navigation-ready workflows, and centralized procurement rather than on normal same-store equipment demand. The white space is meaningful because access remains uneven, with about 57 million Americans living in dental health professional shortage areas and 67% of those shortages concentrated in rural communities.

Meanwhile affordability barriers remain high due to incomplete dental coverage and significant out-of-pocket burden. A roll-up model can create upside through multi-site purchasing discounts of 8-15%, equipment utilization gains of 12-18%, and back-office savings of 300-600 basis points of EBITDA margin.

While also supporting hub-and-spoke referrals for surgery and implant diagnostics; in practical terms, a 50- to 200-clinic platform that standardizes imaging and surgical workflows can compress payback periods on capital equipment by 12-24 months and add about 1.4 percentage points to market CAGR through accelerated refresh cycles and higher per-site equipment intensity.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| AI-led diagnostic SaaS layers | +1.8% | North America core, EU, Japan, South Korea | Short term |

| DSO roll-up digital retrofit | +1.4% | North America, Western Europe, GCC, urban APAC | Short term |

| Chairside surgery-as-a-platform | +1.6% | North America, EU, Australia, premium APAC | Medium term |

| Mid-tier emerging market bundles | +2.1% | India, ASEAN, LATAM, MENA, Africa urban hubs | Medium term |

| Senior oral-care integrated pathways | +1.3% | U.S., EU, Japan, China tier-1 cities | Medium term |

| Cross-border implant tourism networks | +1.7% | Mexico, Türkiye, Thailand, India, CEE | Long term |

Driver

Digital workflow adoption across imaging, scanning, and guided surgery

Digital workflow is now a primary revenue unlock because it compresses diagnosis-to-treatment intervals, raises case acceptance, and pulls consumables, software, and service revenue around the installed base.

Straumann reported 2025 revenue of CHF 2.6 billion with 8.9% organic growth and explicitly highlighted leadership in digital workflows and intraoral scanning, while Dentsply Sirona’s 2025 commentary pointed to high single-digit imaging growth in Europe and the rest of world even as weaker CAD/CAM volumes weighed elsewhere, indicating that imaging-led modernization remains one of the healthiest capex pockets inside dental equipment.

Align’s 2025 systems and services revenue reached $789.6 million and its clear aligner cases rose to 2.6 million, showing that scanner-linked ecosystems increasingly monetize beyond hardware through recurring service, treatment-planning, and downstream procedural revenue.

For the diagnostic and surgical market, this shifts economics from one-time equipment replacement toward multi-layer revenue stacks that include CBCT, intraoral scanning, guided implant planning, chairside design, and digitally assisted surgery; the practical effect is faster utilization of imaging assets, better referral capture for implant/restorative cases, and higher software attachment rates in large DSOs and specialist clinics

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital workflow adoption across imaging, scanning, and guided surgery | +2.4% | North America core, Western Europe core, Japan/South Korea, urban China, Gulf hubs | Short term (≤ 2 years) |

| AI-enabled diagnostics and treatment planning software scaling into routine practice | +1.9% | North America core, EU, UK, South Korea, Australia, selective APAC private chains | Short term (≤ 2 years) |

| Rising oral disease burden and deferred-care conversion into restorative/surgical demand | +2.1% | Global broad-base, strongest in India, Southeast Asia, Latin America, Middle East, underserved U.S./EU pockets | Medium term (2-4 years) |

| Premiumization of implants, aligners, and esthetic rehabilitation | +1.6% | North America, DACH, Nordics, Japan, South Korea, coastal China, affluent urban APAC | Medium term (2-4 years) |

| Regulatory tightening favoring compliant, software-rich platforms and consolidation | +1.3% | EU core, U.S., UK, Canada, advanced APAC | Medium term (2-4 years) |

| Clinic productivity pressure and labor constraints driving capital upgrades | +1.5% | U.S. core, Canada, UK, Germany, Australia, private-chain APAC | Short term (≤ 2 years) |

Challenge

Skilled Chairside Labor Gap

A persistent shortage of trained dentists, hygienists, assistants, imaging operators, and sterile-processing staff continues to suppress utilization efficiency rather than device demand itself, because clinics can still buy scanners, CBCT systems, surgical kits, and digital planning software but cannot fully convert installed capacity into billable procedures when operator rosters run 8% to 15% below target, same-day chair availability slips by 3 to 7 days, and advanced procedure rooms run at only 68% to 82% of designed throughput.

This friction is reinforced by WHO-led calls for workforce reform, expanded task-sharing, and stronger oral-health staffing systems through 2030, indicating the gap is structural and not cyclical. For manufacturers, the result is slower consumable pull-through and longer ramp times after equipment placements, while providers face overtime inflation of roughly 6% to 10%, temporary labor premiums of 12% to 20%, and underused digital assets that can shave about 1.4 percentage points from achievable market CAGR until training pipelines, credential harmonization, and scope-of-practice redesign improve labor elasticity.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Skilled Chairside Labor Gap | -1.4% | North America core, Western Europe, urban APAC | Medium term (2-4 years) |

| Imaging Component Lead-Time Volatility | -1.1% | APAC manufacturing hubs, North America import channels, EU device assemblers | Medium term (2-4 years) |

| AI-Software Compliance Burden | -0.9% | EU regulatory hubs, U.S. FDA pathway markets, advanced APAC | Medium term (2-4 years) |

| Workflow Interoperability Fragmentation | -0.8% | North America DSO networks, EU multisite clinics, developed APAC | Long term (≥ 4 years) |

| Reimbursement Mix Instability | -1.0% | U.S. Medicaid states, Latin America private-pay markets, mixed-funding APAC | Medium term (2-4 years) |

| Sterilization Throughput Pressure | -0.7% | High-volume urban clinics globally, hospital dental units, emerging-market referral centers | Short term (≤ 2 years) |

Restraints

Practice affordability squeeze

Demand is being restrained by the economics of the dental practice itself, because patient out-of-pocket exposure remains high and fee inflation is colliding with uneven household spending power, especially in private-pay diagnostics, implant planning, and elective surgical procedures. In the U.S., national dental care expenditures reached $189 billion in 2024 and consumer dental spending was up 4% as of January 2026. Mean

while an industry readout citing ADA-related 2025 conditions noted that 65.8% of dentists raised fees by an average of 6.7% to protect margins, a pattern that supports revenue per visit but can reduce visit frequency and case acceptance for high-ticket procedures.

When clinics face softer conversion on treatment plans, they defer scanner upgrades, stretch replacement cycles from roughly 5 to 7 years toward 7 to 9 years, and ration purchases of premium surgical tools, so the immediate business effect is slower premium-mix expansion, lower utilization of newly installed equipment, and weaker aftermarket attachment rates.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory recertification drag | -1.6% | EU core, UK spillover, global exporters | Medium term (2-4 years) |

| Tariff-led equipment inflation | -1.4% | North America core, China-linked supply routes, EU importers | Short term (≤ 2 years) |

| Component and imaging parts bottlenecks | -1.2% | APAC corridors, North America, EU | Short term (≤ 2 years) |

| Practice affordability squeeze | -1.8% | North America core, urban private-pay markets, LATAM metros | Short term (≤ 2 years) |

| Workforce and chair-capacity shortages | -1.5% | Africa, rural North America, India, selected EU markets | Medium term (2-4 years) |

| High-cost financing and CapEx deferral | -1.1% | North America, EU, developed APAC | Short term (≤ 2 years) |

Regional Analysis

North America dominated the Dental Diagnostic and Surgical Market in 2025, accounting for more than 37% of the global market and generating approximately US$ 5.0 billion in revenue. The region’s leadership is primarily attributed to its highly developed dental healthcare infrastructure, widespread adoption of advanced diagnostic technologies, and strong presence of leading dental equipment manufacturers.

The United States represents the largest contributor within the region, supported by a high concentration of dental clinics, specialty practices, and dental service organizations (DSOs) that continuously invest in digital dentistry solutions.

The increasing use of cone beam computed tomography (CBCT), intraoral scanners, digital radiography systems, and computer-aided design/computer-aided manufacturing (CAD/CAM) technologies has significantly enhanced diagnostic accuracy and treatment efficiency across North America. Additionally, growing awareness regarding preventive dental care, cosmetic dentistry, and oral health maintenance has increased the demand for both diagnostic and surgical dental procedures.

Favorable reimbursement structures for selected dental treatments, rising healthcare expenditures, and continuous technological advancements further support market expansion. The region also benefits from a substantial aging population requiring restorative and implant-based procedures, alongside increasing demand for minimally invasive dental surgeries.

Furthermore, ongoing research collaborations between dental institutions, technology providers, and healthcare organizations continue to accelerate innovation, strengthening North America’s position as the leading regional market for dental diagnostic and surgical solutions.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

The Dental Diagnostic and Surgical Market is highly competitive, with the top five companies focusing on digital dentistry, diagnostic imaging, treatment planning, and surgical innovation. Dentsply Sirona remains a leading player through its broad portfolio of CAD/CAM systems, imaging solutions, and digital workflow technologies that support efficient diagnosis and treatment. Align Technology continues to strengthen its position with advanced intraoral scanners and digital treatment platforms that improve clinical accuracy and patient engagement.

Envista Holdings leverages its strong implant, imaging, and orthodontic businesses to expand its presence across both diagnostic and surgical applications. Danaher Corporation contributes through its well-established dental equipment, imaging, and clinical workflow solutions, helping dental professionals improve operational efficiency.

Meanwhile, 3M Health Care supports the market with a diverse range of dental materials, restorative products, and clinical solutions. These companies continue to invest in digital technologies, artificial intelligence, and integrated treatment workflows, driving innovation and raising the standard of dental care worldwide.

Top Key Players

- Dentsply Sirona

- Danaher Corporation (KaVo Kerr)

- Align Technology

- Envista Holdings

- 3M Health Care

- Straumann Group

- Zimmer Biomet Dental

- Nobel Biocare (Envista)

- Planmeca Group

- Carestream Dental

- Vatech Co., Ltd.

- GC Corporation

- Ivoclar Vivadent

- Henry Schein Inc.

- Medtronic (dental surgery division)

Recent Developments

- In 2025, Planmeca signed a strategic agreement with Aspen Dental to deploy its imaging technology (including CBCT and digital imaging systems) across approximately 1,100+ dental clinics in the United States, expanding large-scale clinical adoption of integrated dental diagnostic ecosystems.

- In 2025, Dentsply Sirona continued global expansion of its digital dentistry ecosystem including CAD/CAM, imaging, and treatment planning solutions across over 120 countries, reinforcing integration of diagnostic and surgical workflows.

- In July 2025 – Straumann Group completed the acquisition of the remaining shares of Promaton B.V., increasing ownership from 88.11% to 100%. The Netherlands-based company specializes in artificial intelligence applications for dental diagnostics and treatment planning. The transaction was disclosed in Straumann’s official financial filing, making it one of the strongest verified M&A developments in 2025.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 13.5 Billion |

| Forecast Revenue (2035) | US$ 26.6 Billion |

| CAGR (2026-2035) | 7.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | Product Type (Diagnostics) (Dental Imaging Systems (CBCT, Intraoral X-ray, Panoramic), Caries Detection Devices, Periodontal Probes (Digital), Intraoral Scanners), Product Type (Surgical) (Dental Implants, Bone Grafting Materials, Surgical Instruments, Regenerative Materials), Procedure Type (Implantology Procedures, Oral Surgery (extractions, trauma), Periodontal Surgery, Endodontic Surgery), End User (Dental Clinics, Hospitals, Academic & Research Institutes), Technology Type (Digital Imaging & CAD/CAM, Conventional Surgical Tools), Distribution Channel (Direct Institutional Sales, Distributors, Online Procurement Platforms) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Dentsply Sirona, Danaher Corporation (KaVo Kerr), Align Technology, Envista Holdings, 3M Health Care, Straumann Group, Zimmer Biomet Dental, Nobel Biocare (Envista), Planmeca Group, Carestream Dental, Vatech Co., Ltd., GC Corporation, Ivoclar Vivadent, Henry Schein Inc., Medtronic (dental surgery division) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |