Global Data Anomaly Detection Market Size, Share and Analysis Report By Component (Software, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Application (Fraud Detection, Network Intrusion Detection, System Health Monitoring, Industrial IoT Monitoring, Others), By End-User Industry (Banking, Financial Services, and Insurance, IT and Telecommunications, Healthcare, Manufacturing, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 177580

- Number of Pages: 222

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaway

- Key Insights Summary

- Drivers Impact Analysis

- Restraint Impact Analysis

- By Component Analysis

- By Deployment Mode Analysis

- By Organization Size Analysis

- By Application Analysis

- By End User Industry Analysis

- Regional Analysis

- Investor Type Impact Matrix

- Technology Enablement Analysis

- Emerging Trends Analysis

- Growth Factors Analysis

- Opportunity Analysis

- Challenge Analysis

- Key Market Segments

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

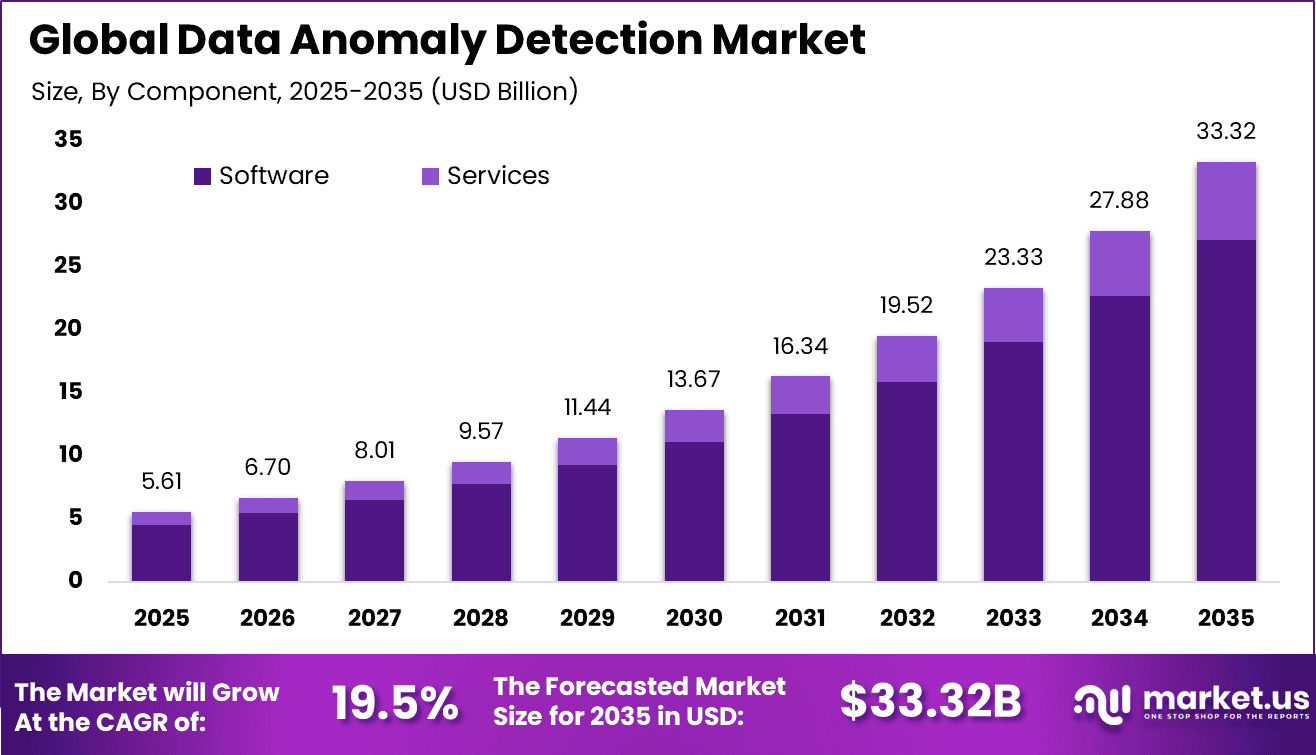

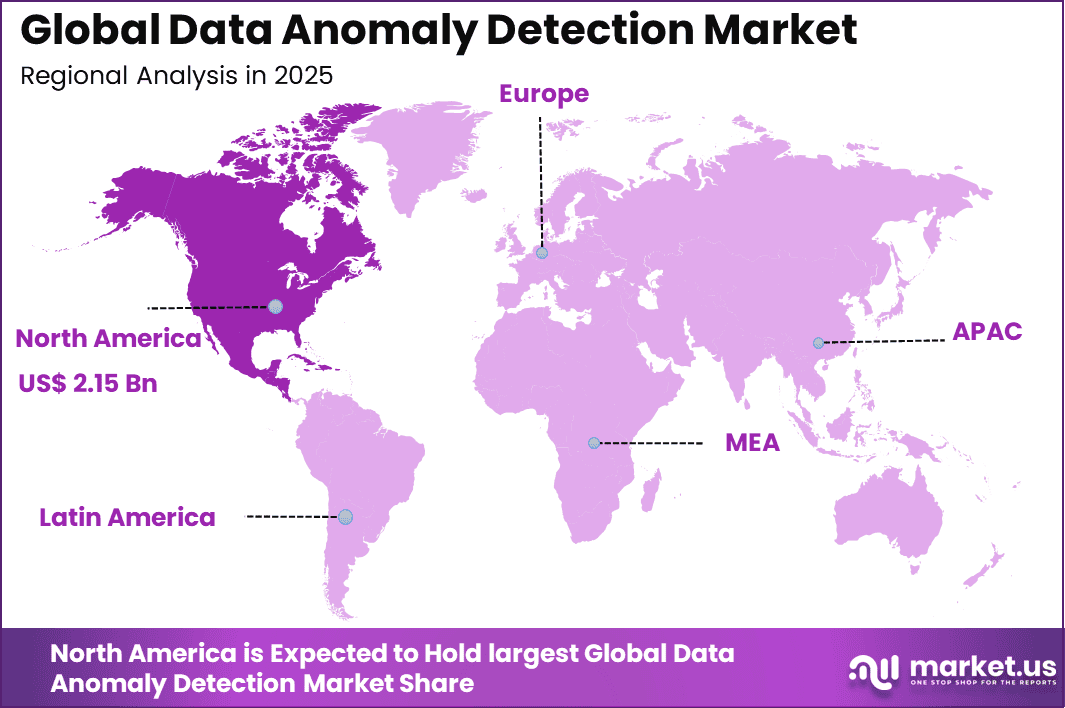

The Global Data Anomaly Detection Market size is expected to be worth around USD 33.32 billion by 2035, from USD 5.61 billion in 2025, growing at a CAGR of 19.5% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 38.5% share, holding USD 2.15 billion in revenue.

The Data Anomaly Detection Market refers to platforms and analytical systems designed to identify unusual patterns, outliers, or deviations within datasets that may indicate errors, risks, or abnormal behavior. These solutions are used across data pipelines, applications, networks, financial systems, and operational processes. Anomaly detection helps organizations identify issues that traditional rule based monitoring fails to capture.

The market has gained importance as data volumes grow and real time decision making becomes critical. Data anomaly detection operates as a proactive control layer within modern data and analytics environments. It supports early identification of data quality issues, fraud signals, system failures, and operational irregularities. Industry observations indicate that more than 60% of critical data incidents are first detected through pattern deviation rather than predefined thresholds.

One of the main driving factors is the increasing complexity of data environments. Data flows across multiple systems, formats, and teams, making manual validation impractical. Small deviations can quickly escalate into major business issues. Anomaly detection provides continuous oversight without relying on static rules. Studies show that organizations can lose over 25% of productivity time addressing downstream effects of data issues.

For instance, in February 2026, DataDog expanded Watchdog AI with log anomaly detection, auto-baselining patterns like text changes or error spikes. It proactively surfaces hidden log issues before they blow up. Solid update that keeps DataDog competitive in the fast-moving observability space

Demand for data anomaly detection is strong among enterprises that rely on automated analytics and real time data processing. Financial services, ecommerce, and digital platforms require high data accuracy to function effectively. Anomaly detection helps ensure that insights and decisions are based on reliable inputs. This operational dependency sustains market demand.

Key Takeaway

- In 2025, the Software segment led the Global Data Anomaly Detection Market with a 81.6% share, reflecting strong demand for advanced analytics platforms.

- In 2025, Cloud based deployment accounted for 72.8% of the market, supported by scalable infrastructure and real time data processing needs.

- In 2025, Large Enterprises represented 74.3% of total adoption, driven by complex data environments and higher security requirements.

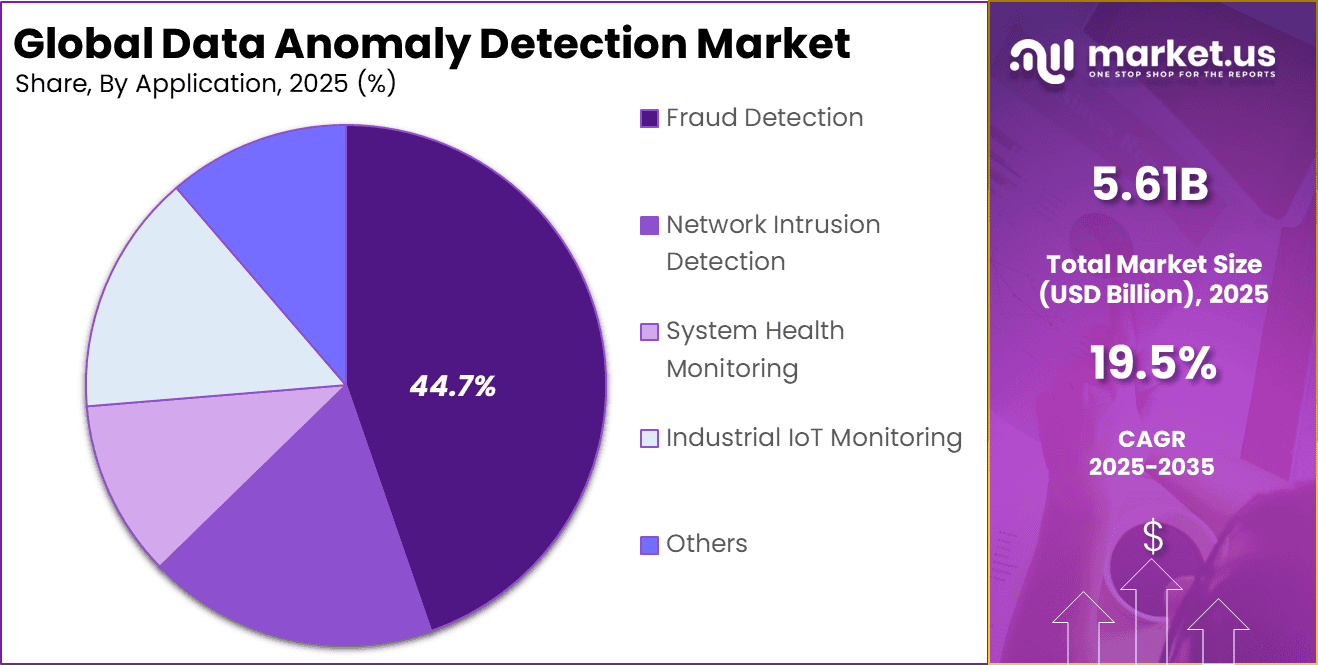

- In 2025, Fraud Detection emerged as the leading application, capturing 44.7% of the market due to rising financial crime risks.

- In 2025, the Banking, Financial Services, and Insurance sector held a 52.4% share, supported by strict compliance and risk management frameworks.

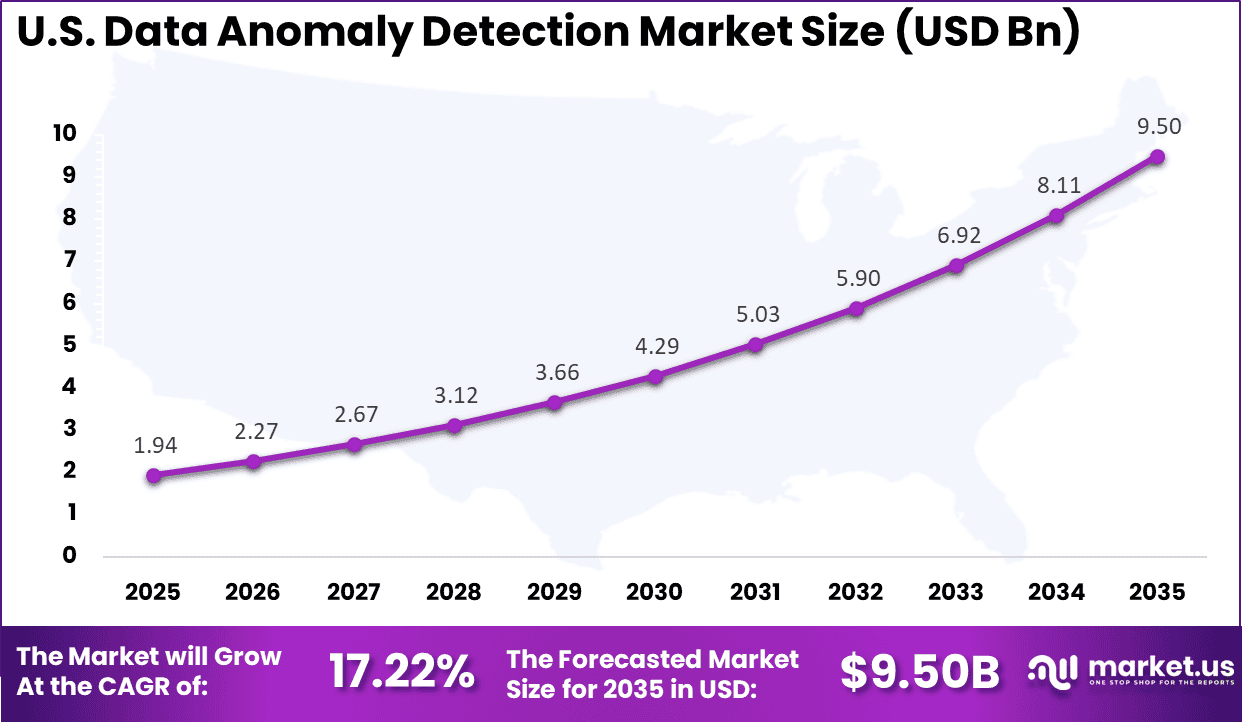

- In 2025, the US Data Anomaly Detection Market was valued at USD 1.94 billion and recorded a CAGR of 17.22%, reflecting increased cybersecurity investment.

- In 2025, North America held more than 38.5% of the Global Data Anomaly Detection Market, supported by mature digital infrastructure and regulatory focus on data protection.

Key Insights Summary

- By 2025, more than 60% of large enterprises are expected to deploy AI driven anomaly detection systems to address rising cyber threats.

- Machine Learning remains the core technology, holding 56% of the technology segment share in 2025, supported by its ability to process large and complex datasets.

- Cloud based infrastructure represents about 64% of total deployment in 2025, reflecting preference for scalable environments capable of handling high velocity data streams.

- Organizations adopting modern anomaly detection platforms report error rate reductions of up to 25%, improving overall system reliability.

- Advanced self supervised models can detect revenue inflation patterns at 38.6% and expense concealment at 21.7%, with a false alarm rate as low as 0.068.

- AI powered detection systems have reduced fraud investigation time by up to 70% and increased identification of complex cases such as money laundering by 50%, strengthening compliance and risk management outcomes.

Drivers Impact Analysis

Key Driver Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Rising cyber threats and insider risk incidents +5.1% Global Short to medium term Increasing adoption of AI and machine learning across enterprises +4.4% North America, Europe Medium term Rapid growth of big data and real-time analytics environments +3.8% Global Medium term Expansion of cloud-native and distributed IT systems +3.2% North America, Asia Pacific Medium term Regulatory requirements for fraud detection and compliance monitoring +3.0% Europe, North America Medium to long term Restraint Impact Analysis

Key Restraint Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline High implementation and model training costs -3.4% Emerging Markets Short to medium term Shortage of skilled data science professionals -2.9% Global Medium term Data quality and integration challenges -2.5% Global Medium term False positives and model explainability concerns -2.1% Europe, North America Medium term Privacy and data governance restrictions -1.8% Europe Medium to long term By Component Analysis

By component, software solutions accounted for 81.6% of adoption. Organizations prefer software based tools that integrate directly with existing data systems. These solutions offer flexibility and scalability across multiple use cases. This makes them suitable for complex enterprise environments.

Software platforms support continuous updates and model improvements. Vendors enhance algorithms without requiring hardware changes. This reduces total cost of ownership. Enterprises benefit from faster deployment and easier maintenance.

Customization has further strengthened software dominance. Users can configure detection rules based on specific risk profiles. This improves relevance and operational alignment. As data volumes grow, software centric solutions remain dominant.

For Instance, in March 2025, RapidMiner reinforced the software‑led shift in anomaly detection with updates to its Anomaly Detection Extension, which brings unsupervised outlier‑detection algorithms directly into its low‑code analytics platform. This makes it easier for non‑technical users to assign anomaly scores to rows and operationalize anomaly‑driven analysis inside existing workflows without building custom code.

By Deployment Mode Analysis

By deployment mode, cloud based systems represented 72.8% of usage. Cloud platforms enable real time processing of large datasets. Enterprises benefit from elastic compute resources. This supports high frequency anomaly detection. Cloud deployment also reduces infrastructure overhead. Organizations avoid upfront hardware investments.

Subscription models improve cost predictability. This aligns with broader cloud adoption trends. Remote accessibility has added further value. Teams can monitor systems across locations. Alerts and insights are available in real time. This has reinforced cloud based adoption.

For instance, in June 2025, Google Cloud promoted its cloud‑first approach to anomaly detection with enhanced time‑series anomaly APIs that can be consumed as managed services across infrastructure and application workloads. By offering streaming‑detection modes and auto‑scaling models, Google is helping enterprises run anomaly‑driven observability in multi‑cloud environments without owning specialized infrastructure.

By Organization Size Analysis

By organization size, large enterprises accounted for 74.3% of demand. These organizations manage complex and high volume data environments. Anomaly detection supports governance and compliance needs. Large enterprises also face higher financial and reputational risk. Large organizations operate across multiple systems and geographies.

Automated detection provides centralized oversight. This improves risk visibility. It also reduces reliance on manual controls. Investment capacity supports adoption. Large enterprises can deploy advanced analytics solutions. This has accelerated market penetration within this segment. Their dominance reflects scale and risk exposure.

For Instance, in November 2025, Glassbox’s acquisition of Anodot in late 2025 brought advanced autonomous anomaly engines into a digital‑experience platform used heavily by large global enterprises. Anodot’s unsupervised‑ML engines are now embedded across enterprise‑scale digital journeys, helping product, operations, and analytics teams detect business‑impacting anomalies early.

By Application Analysis

By application, fraud detection represented 44.7% of usage. Fraud risks have increased with digital payments and online transactions. Anomaly detection helps identify unusual behavior patterns. This enables early intervention. Financial losses from fraud can be significant. Automated detection improves response time. This reduces financial impact.

Organizations increasingly prioritize fraud related use cases. Detection models continuously learn from new fraud patterns. This improves effectiveness over time. As fraud tactics evolve, anomaly detection remains central. Fraud detection continues to be the leading application area.

For Instance, in November 2025, Haiqu, using IBM Quantum, demonstrated superior fraud anomaly detection on complex financial datasets via quantum embedding. The approach outperforms classical methods by compactly representing high‑dimensional data on current hardware. It signals quantum ML’s potential for precise, scalable fraud pattern spotting.

By End User Industry Analysis

By end user industry, banking, financial services, and insurance accounted for 52.4% of adoption. These sectors process sensitive and high volume transactions. Risk detection is critical to operations. Anomaly detection supports compliance and security. Financial institutions face strict regulatory requirements.

Early detection of irregular activity supports reporting obligations. This reduces regulatory risk. Automated systems improve audit readiness. Digital banking growth has further increased data exposure. Anomaly detection tools help manage this complexity. As digital finance expands, BFSI remains the primary end user industry.

For Instance, in April 2025, Sumo Logic unveiled security features at RSAC for BFSI threat detection, unifying telemetry, context, and AI for faster responses. The platform processes massive data volumes to spot anomalies in transactions and access patterns accurately. It reduces false alarms while enhancing compliance in regulated financial environments.

Regional Analysis

North America accounted for 38.5% of market adoption, supported by advanced digital infrastructure. Organizations in the region invest heavily in data analytics and security. Regulatory standards also drive adoption. This has supported strong regional uptake.

For instance, in November 2025, AWS Cost Anomaly Detection introduced an improved detection algorithm using rolling 24-hour windows for faster, more accurate identification of unusual spending patterns. This enhancement eliminates delays from incomplete daily data comparisons and reduces false positives, strengthening North America’s leadership in real-time cloud cost management and anomaly detection capabilities.

The United States leads the region with market value of USD 1.94 Bn and a CAGR of 17.22%. Financial institutions and large enterprises are key adopters. Investment in fraud prevention and analytics remains strong. Innovation continues to reinforce regional leadership. Integration with cloud and AI platforms has improved detection performance. As data volumes increase, anomaly detection remains a critical capability in North America.

For instance, in October 2025, IBM released updates to Z Anomaly Analytics 5.1, enhancing machine learning capabilities for log-based and metric-based anomaly detection. The integration of authentication services and new gateway URLs simplifies administrative access, strengthening real-time anomaly monitoring across enterprise systems. This innovation reinforces U.S. leadership in robust, scalable anomaly detection solutions for mission-critical operations.

Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook AI and analytics software providers Very High Medium North America, Europe Strong recurring SaaS growth Cybersecurity platform vendors High Medium Global Cross-sell into security stacks Cloud service providers Medium Low to Medium Global Infrastructure-driven demand Private equity firms Medium Medium North America, Europe Consolidation of analytics platforms Venture capital investors High High North America Innovation in AI-based detection models Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Primary Function Geographic Relevance Adoption Timeline Machine learning-based anomaly detection algorithms +5.4% Automated pattern recognition Global Short to medium term Real-time streaming data analytics platforms +4.2% Instant anomaly identification Global Medium term Cloud-native deployment and scalable processing +3.6% Elastic workload management Global Medium term AI-driven behavioral analytics models +3.1% Insider threat detection North America, Europe Medium to long term Explainable AI and compliance reporting tools +2.4% Transparency and audit readiness Europe, North America Long term Emerging Trends Analysis

An emerging trend in the data anomaly detection market is the use of unsupervised and self-learning models. These models adapt to evolving patterns without requiring extensive labelled training data. Self-learning enhances detection capability in dynamic environments where normal behaviour changes over time. Adaptive detection approaches improve accuracy and reduce tuning requirements.

Another trend is embedding anomaly detection into data observability and monitoring platforms. Instead of standalone tools, detection capabilities are integrated with pipeline monitoring, lineage tools, and infrastructure performance dashboards. This unified observability approach supports comprehensive oversight and faster root cause identification.

Growth Factors Analysis

One of the key growth factors for the data anomaly detection market is rising regulatory and compliance requirements. Organisations must demonstrate controls that identify irregular activity and support audit readiness. Anomaly detection provides evidence of monitoring and risk management. This compliance driven demand supports sustained adoption.

Another growth factor is increasing automation of operational processes. As organisations rely on automated systems for customer service, production workflows, and financial transactions, the cost of undetected anomalies increases. Early detection reduces downtime, prevents costly errors, and supports continuous operation. Automation driven reliance on detection tools reinforces long term market growth.

Opportunity Analysis

A significant opportunity in the data anomaly detection market lies in integration with predictive analytics and business intelligence. Linking anomaly insights with forecasting and trend analysis provides richer context for decision makers. For example, anomaly detection can trigger deeper investigations or automated corrective actions. Platforms that offer unified analytics and detection provide higher value to enterprise users.

Another opportunity is expansion into edge and IoT monitoring. Industrial IoT, smart infrastructure, and connected devices generate continuous streams of data. Anomaly detection at the edge enables real time fault identification and rapid local response. This reduces latency and supports operational continuity in manufacturing, logistics, and smart city environments.

Challenge Analysis

A major challenge for the data anomaly detection market is explainability and interpretability of detection outcomes. Machine learning driven models may identify deviations without clear reasoning that is easily understood by users. Organisations require transparent explanations to support decision making and compliance. Improving interpretability without sacrificing performance remains a challenge.

Another challenge is integrating anomaly detection with existing workflows and incident management systems. Detection alerts must align with operational processes so that meaningful events trigger appropriate responses. Poor integration can lead to response delays or misdirected action, reducing the effectiveness of detection investments.

Key Market Segments

By Component

- Software

- Services

By Deployment Mode

- Cloud-based

- On-premises

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

By Application

- Fraud Detection

- Network Intrusion Detection

- System Health Monitoring

- Industrial IoT Monitoring

- Others

By End-User Industry

- Banking, Financial Services, and Insurance

- IT and Telecommunications

- Healthcare

- Manufacturing

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Global cloud and enterprise technology providers such as IBM, Microsoft, Amazon Web Services, and Google lead the data anomaly detection market. Their platforms integrate machine learning models into data pipelines and security systems. Real-time analytics and scalable cloud infrastructure support enterprise-wide monitoring. These vendors benefit from strong ecosystem integration and global reach. Demand is driven by rising cyber threats and the need for proactive operational monitoring.

Analytics and observability-focused vendors such as Splunk, SAS Institute, and Elastic emphasize pattern recognition and event correlation. Sumo Logic, Dynatrace, New Relic, and DataDog strengthen real-time anomaly detection across applications and infrastructure. These platforms help reduce downtime and detect suspicious activity early. Adoption is strong in finance, telecom, and digital commerce sectors.

Specialized AI and data science providers such as Anodot, RapidMiner, TIBCO Software, and H2O.ai focus on automated model building and explainable AI. Their tools support business anomaly detection in sales, fraud, and operational metrics. Other vendors enhance regional presence and innovation. This competitive landscape supports steady expansion of data anomaly detection across enterprise environments.

Top Key Players in the Market

- IBM

- Microsoft

- Amazon Web Services

- Splunk

- SAS Institute

- RapidMiner

- Anodot

- Elastic

- Sumo Logic

- Dynatrace

- New Relic

- DataDog

- TIBCO Software

- H2O.ai

- Others

Recent Developments

- In February 2026, IBM launched the next-generation FlashSystem portfolio with agentic AI for autonomous storage, featuring built-in anomaly detection that spots issues like ransomware threats in real time. This helps IT teams act fast on storage anomalies, cutting downtime and boosting efficiency.

- In July 2025, Splunk enhanced its App for Anomaly Detection with better handling of missing data and uneven timestamps, plus confidence scores and sustained deviation alerts. You can now schedule jobs and tweak sensitivity easily. It’s practical stuff that makes spotting real problems in messy datasets way less frustrating for analysts.

Report Scope

Report Features Description Market Value (2025) USD 5.6 Billion Forecast Revenue (2035) USD 33.3 Billion CAGR(2025-2035) 19.5% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Application (Fraud Detection, Network Intrusion Detection, System Health Monitoring, Industrial IoT Monitoring, Others), By End-User Industry (Banking, Financial Services, and Insurance, IT and Telecommunications, Healthcare, Manufacturing, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape IBM, Microsoft, Amazon Web Services, Google, Splunk, SAS Institute, RapidMiner, Anodot, Elastic, Sumo Logic, Dynatrace, New Relic, DataDog, TIBCO Software, H2O.ai, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Data Anomaly Detection MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

Data Anomaly Detection MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- IBM

- Microsoft

- Amazon Web Services

- Splunk

- SAS Institute

- RapidMiner

- Anodot

- Elastic

- Sumo Logic

- Dynatrace

- New Relic

- DataDog

- TIBCO Software

- H2O.ai

- Others

Our Clients

- 177580

- Feb. 2026