Quick Navigation

Report Overview

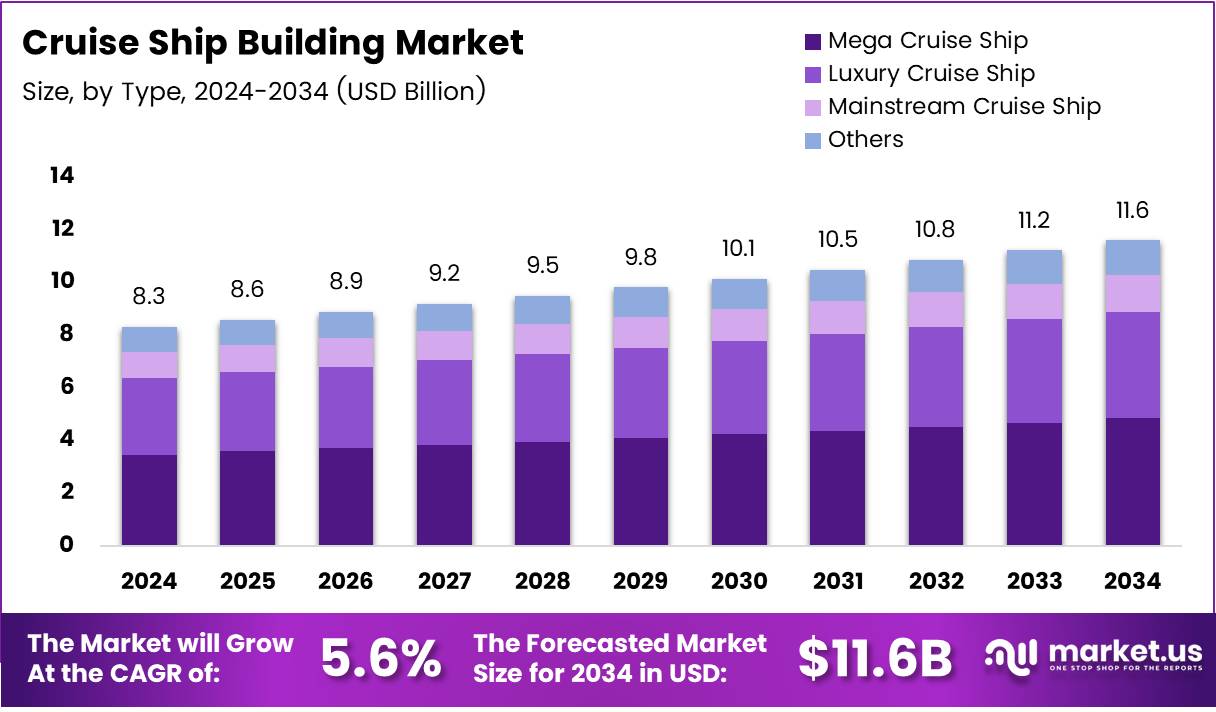

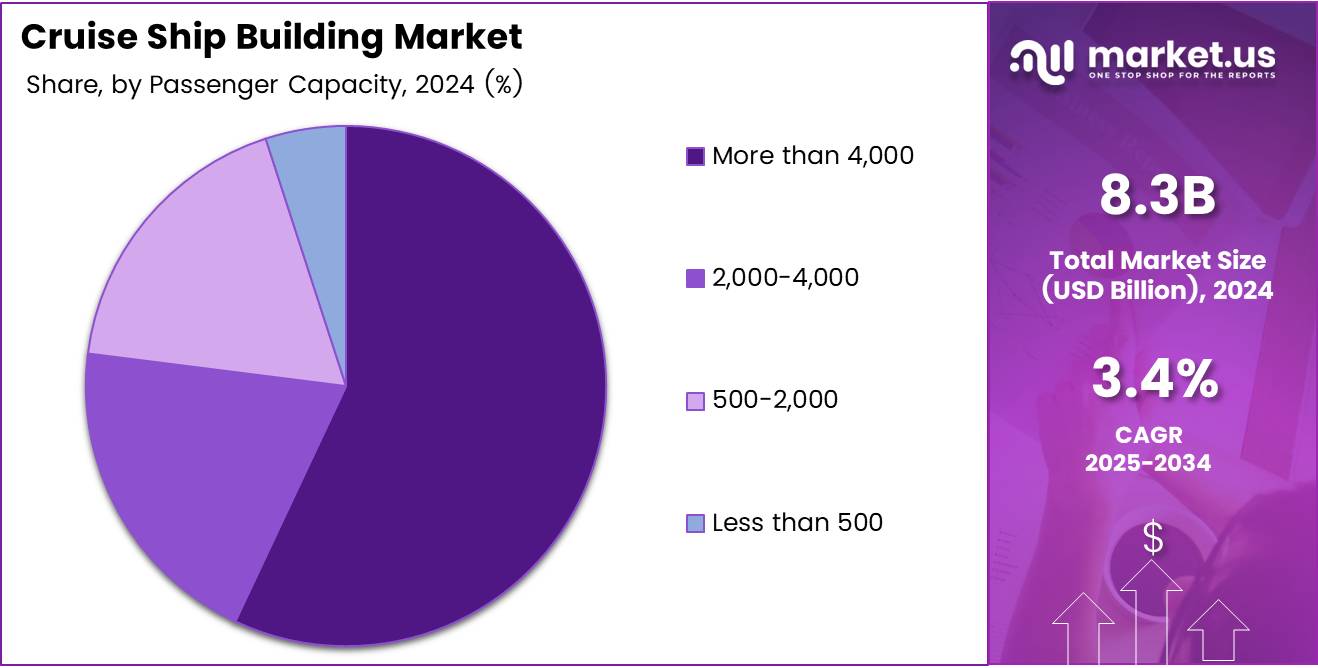

The Global Cruise Ship Building Market size is expected to be worth around USD 11.6 Billion by 2034, from USD 8.3 Billion in 2024, growing at a CAGR of 3.4% during the forecast period from 2025 to 2034.

The cruise shipbuilding market represents the specialized segment of the broader shipbuilding industry focused on designing and constructing vessels for leisure cruising. This market includes cruise shipbuilders, cruise ship manufacturers, and cruise shipyards that deliver innovative cruise vessel manufacturing solutions. Its growth is propelled by rising demand for cruise travel and evolving cruise ship design to enhance passenger experience.

Growth in the cruise shipbuilding sector has been robust, largely fueled by rising global passenger volumes. According to ScienceDirect, the Asian cruise market has experienced remarkable expansion, with over 68% of total passengers generated in the past decade and nearly 40% in the last five years alone. This surge reflects broader shifts in cruise demand, emphasizing new geographic opportunities and the need for modern cruise ship production facilities.

Opportunities abound as cruise ship construction adapts to changing traveler preferences. The rise in multigenerational cruising is notable; CaribbeanShipping reports that over 30% of families now cruise with at least two generations onboard, while nearly 28% travel with three to five generations. Such trends push cruise shipbuilders to innovate in ship design, offering flexible spaces that cater to families of all sizes and preferences.

Government investment and regulatory dynamics also play a critical role in shaping the shipbuilding industry. AidData reveals that China has committed over US$10 billion in financing to developing countries for shipbuilding and vessel acquisition. This investment supports China’s domestic shipbuilding industry while securing critical transport routes, underscoring the strategic importance of cruise ship shipyards and broader maritime infrastructure development.

Additionally, the luxury cruise segment is gaining momentum. According to EscalonTimes, the number of luxury small ships is expected to double by 2030, providing up to 50% more personal space per passenger compared to traditional mega-ships. This trend highlights a growing market niche within cruise vessel manufacturing focused on exclusivity, comfort, and personalized experiences.

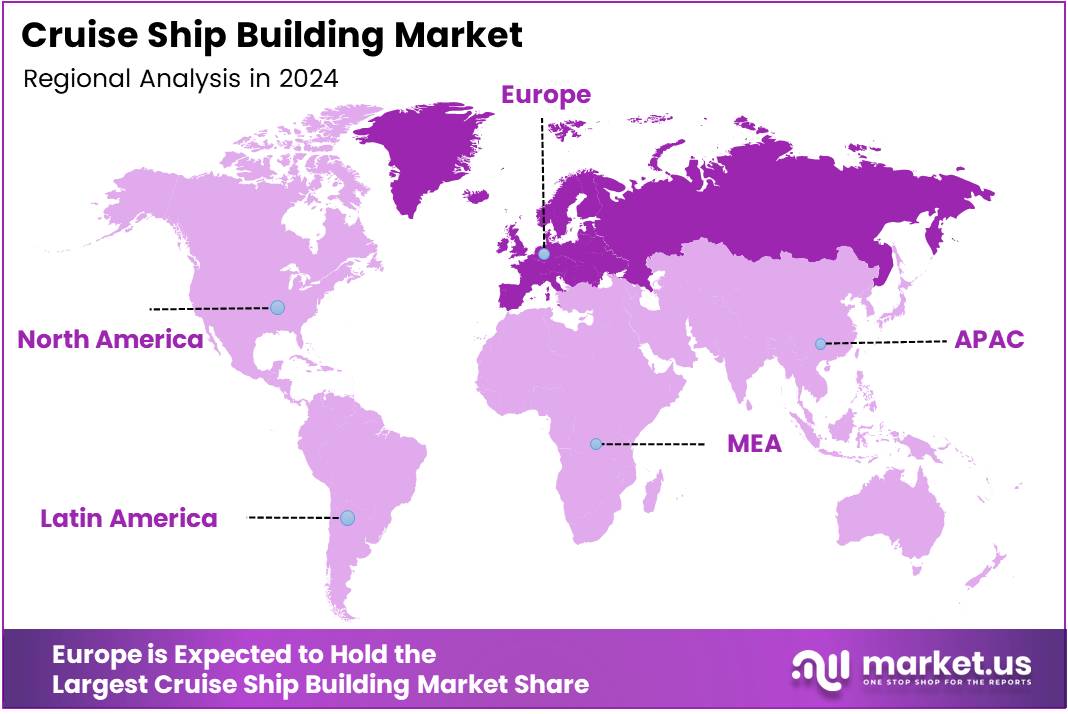

Most cruise ships continue to be built in Europe, with the Cruise Lines International Association noting that Europe accounts for 98% of global cruise ship production. This concentration underscores the region’s expertise in cruise shipbuilding, from advanced ship design to the skilled labor force required for sophisticated cruise ship construction.

Key Takeaways

- The global cruise ship building market is projected to reach USD 11.6 billion by 2034, growing from USD 8.3 billion in 2024 at a CAGR of 3.4%.

- In 2024, Mega Cruise Ships dominated the By Type segment, driven by demand for larger vessels with extensive facilities.

- The Transportation application segment led in 2024, boosted by expanding international cruise routes and improved seaport infrastructure.

- Vessels weighing more than 150,000 GT held the largest share in the By Weight segment in 2024, favored for high passenger capacity and amenities.

- Liquified Natural Gas (LNG) was the leading fuel type in 2024, chosen for its lower emissions and compliance with environmental regulations.

- Cruise ships with a passenger capacity of more than 4,000 dominated the market in 2024 due to trends favoring large-scale cruise experiences.

- Europe remains the dominant region in cruise ship building, supported by advanced shipbuilding infrastructure and maritime expertise.

Type Analysis

Mega Cruise Ship leads due to its large passenger capacity and onboard amenities.

In 2024, Mega Cruise Ship held a dominant market position in the By Type Analysis segment of the Cruise Ship Building Market. This dominance is attributed to the rising preference for larger vessels that offer extensive entertainment, dining, and accommodation facilities. These ships are often viewed as floating cities, ideal for long-haul and international cruises.

Luxury Cruise Ships followed closely behind, appealing to affluent travelers seeking exclusive experiences and high-end services. With emphasis on premium interiors and personalized offerings, this segment is growing steadily as luxury travel demand increases.

Mainstream Cruise Ships also maintained a substantial portion of the market. These vessels cater to a wide demographic, balancing affordability with comfort, and are a popular choice among first-time cruisers and families.

The Others category includes smaller and niche cruise vessels, such as expedition and river cruise ships. While they account for a smaller share, they are steadily gaining traction due to their unique itineraries and personalized experiences.

Application Analysis

Transportation holds a leading share driven by increasing global maritime travel demand.

In 2024, Transportation held a dominant market position in the By Application Analysis segment of the Cruise Ship Building Market. The growing number of international cruise routes and improved seaport infrastructure globally has fueled the use of cruise ships for transportation, especially in coastal and island regions.

Leisure, while representing a smaller portion, continues to thrive due to rising disposable incomes and interest in luxury vacations. The leisure segment is characterized by short-duration trips focused on entertainment, sightseeing, and relaxation.

Despite its smaller market share, the leisure cruise segment plays a vital role in enhancing passenger experiences and driving innovation in onboard amenities and cruise itineraries.

Weight Analysis

More than 150,000 GT ships dominate due to their capacity to house larger infrastructure and more passengers.

In 2024, More than 150,000 GT held a dominant market position in the By Weight Analysis segment of the Cruise Ship Building Market. These massive vessels are favored for their ability to accommodate thousands of passengers, vast onboard entertainment facilities, and diverse dining options.

Ships in the 100,000–150,000 GT category also contributed significantly. They strike a balance between capacity and operational efficiency, making them a common choice among major cruise lines.

The 50,000–100,000 GT and 1,000–50,000 GT segments represent mid-size vessels suitable for regional and specialty routes. These are increasingly used in emerging markets where port infrastructure limits ultra-large ships.

Meanwhile, Less than 1,000 GT vessels cater to niche markets such as luxury yachts and expedition ships. Although their share is comparatively smaller, these ships are gaining attention for their customized services and exploration-focused itineraries.

Fuel Type Analysis

Liquified Natural Gas (LNG) takes the lead as cruise lines prioritize cleaner energy alternatives.

In 2024, Liquified Natural Gas (LNG) held a dominant market position in the By Fuel Type Analysis segment of the Cruise Ship Building Market. LNG is increasingly being adopted due to its lower emissions profile, aligning with global environmental regulations and sustainability goals.

Marine Diesel Oil (MDO) remained a widely used fuel due to its availability and relatively cleaner combustion compared to traditional heavy fuels. It serves as a transition fuel for cruise lines not yet equipped for LNG.

Heavy Fuel Oil (HFO), while still used in some older vessels, continues to decline in preference due to its environmental impact and rising regulatory restrictions.

The shift towards LNG reflects the cruise industry’s long-term strategy to meet climate goals while enhancing operational efficiency and passenger satisfaction through greener solutions.

Passenger Capacity Analysis

More than 4,000 passengers segment dominates as mega ships cater to growing global cruise demand.

In 2024, More than 4,000 held a dominant market position in the By Passenger Capacity Analysis segment of the Cruise Ship Building Market. This dominance is driven by the increasing trend toward large-scale cruise experiences, where economies of scale allow operators to offer more amenities and services to a higher number of travelers. Mega cruise ships in this category appeal to a broad demographic and are especially popular on high-traffic international routes.

The 2,000–4,000 segment also captured a significant share of the market. These mid-to-large vessels are widely favored by major cruise lines as they strike a balance between capacity, onboard offerings, and port accessibility. They are versatile for both short and long-haul itineraries.

Ships with a capacity of 500–2,000 are typically deployed for regional routes or specialized voyages. This segment serves niche markets where personalized service and destination-focused cruising are key selling points.

The Less than 500 segment caters to ultra-luxury, expedition, and river cruising markets. Although smaller in scale, this category is gaining attention among high-income travelers looking for intimate and exclusive experiences on less crowded vessels. Their flexibility in accessing remote destinations adds to their appeal.

Key Market Segments

By Type

- Mega Cruise Ship

- Luxury Cruise Ship

- Mainstream Cruise Ship

- Others

By Application

- Transportation

- Leisure

By Weight

- More than 150,000 GT

- Less than 1,000 GT

- 50,000-100,000 GT

- 1,000-50,000 GT

- 100,000-150,000 GT

By Fuel Type

- Liquified Natural Gas (LNG)

- Marine Diesel Oil (MDO)

- Heavy Fuel Oil (HFO)

By Passenger Capacity

- More than 4,000

- 2,000-4,000

- 500-2,000

- Less than 500

Drivers

Rise in Multi-Generational Travel Demand on Cruise Vacations Drives Market Growth

The cruise ship building market is seeing a strong push due to rising interest in vacations that cater to multiple generations. Families now prefer cruise experiences that suit children, adults, and seniors alike, creating a higher demand for larger, more versatile ships with inclusive amenities. This trend is encouraging shipbuilders to design vessels with broader activity options and accessible features.

Asia is rapidly becoming a key player in the global cruise industry. Countries like China, Singapore, and Japan are expanding port infrastructure and improving maritime services to attract more cruise liners. This regional growth is leading to more shipbuilding contracts in Asia, further driving market expansion.

In response to the need for faster and more cost-efficient ship production, builders are now using modular construction techniques. These methods allow for parts of the ship to be built separately and then assembled quickly. This innovation reduces production time and helps meet increasing demand.

Government support is another important factor. Many governments are investing in coastal infrastructure and promoting maritime tourism. This financial and policy backing encourages shipbuilders to invest in new projects and adopt advanced technologies, ensuring the industry’s steady growth.

Restraints

Environmental Regulations on Emission Control and Waste Disposal Challenge Market Expansion

Stringent environmental regulations are a major restraint for the cruise ship building market. International rules now require ships to limit emissions and manage waste more effectively. Compliance with these rules raises costs for shipbuilders, as they must include complex systems and cleaner engines.

Fuel prices are also a concern. Marine fuel costs are highly volatile, and fluctuations can significantly impact operational budgets. For shipbuilders, this means designing more fuel-efficient ships, which adds to construction complexity and expense.

Another limitation is the lack of skilled labor in the marine engineering sector. As demand grows, there is a shortage of professionals with expertise in ship design, marine systems, and construction. This slows down production and affects quality control.

Finally, the cruise industry is sensitive to public perception, especially regarding safety and health. Maritime accidents or outbreaks like COVID-19 increase consumer concerns. These events can delay new orders and reduce investor confidence, directly affecting shipbuilding activities.

Growth Factors

Custom-Built Expedition and Arctic Cruise Ship Segments Offer New Growth Opportunities

The cruise ship building market has strong growth potential in the expedition and Arctic cruise segments. Travelers are increasingly interested in exploring remote and adventurous destinations, which requires specialized vessels built to withstand extreme conditions. This creates opportunities for custom-built ships with unique features.

Partnerships between shipbuilders and luxury hotel brands are another growing trend. Co-branded vessels bring high-end hospitality to the seas, combining luxury service with tailored cruise experiences. These collaborations can open new market segments and increase demand for premium shipbuilding.

Sustainability is also driving innovation. The integration of hydrogen and battery-powered propulsion systems allows for cleaner, eco-friendly cruises. This not only helps meet environmental standards but also appeals to environmentally conscious travelers.

Regional markets such as South America and Africa are also seeing rising demand for cruise travel. These regions offer unique destinations and are less saturated compared to traditional routes. As infrastructure develops, the need for mid-sized, regional cruise ships will provide new building contracts for manufacturers.

Emerging Trends

Smart Ship Technology Integration for Real-Time Monitoring and Automation Trends in Market

Smart ship technology is a key trend shaping the cruise ship building market. Modern vessels are now equipped with sensors, automation systems, and real-time monitoring tools. These technologies improve navigation, safety, and fuel efficiency, making smart systems a standard expectation in new builds.

There’s also growing demand for cruise ships that offer private villas, themed experiences, and tailored luxury. Travelers seek more personalized and unique vacations, pushing shipbuilders to design interiors that cater to different lifestyle preferences and high-end comforts.

A noticeable shift is occurring toward smaller, destination-focused luxury yachts. These vessels offer more intimate experiences and access to ports that larger ships can’t reach. This trend supports demand for boutique shipbuilding and opens niche markets.

Finally, the use of circular economy principles is gaining momentum. Builders are increasingly using recyclable materials and planning for lifecycle management. This approach not only reduces environmental impact but also aligns with global sustainability goals, shaping the future of cruise ship construction.

Regional Analysis

Europe Dominates the Cruise Ship Building Market

Europe holds a commanding position in the cruise ship building market due to its advanced shipbuilding infrastructure and longstanding maritime expertise. The region continues to lead through significant investments and technological advancements in vessel construction.

Regional Mentions:

The Asia Pacific region is rapidly expanding its presence, driven by growing passenger demand and increasing shipbuilding capabilities as countries aim to capture a larger share of the cruise tourism market. This region is expected to experience substantial growth in the coming years.

North America maintains steady growth supported by a strong cruise tourism industry and established shipyards that foster innovation in marine engineering.

The Middle East & Africa region shows emerging opportunities fueled by expanding cruise routes and ongoing development of tourism infrastructure, although its current market share remains relatively small.

Latin America is witnessing gradual growth, with investments in port facilities and rising consumer interest in cruise vacations positioning it as an evolving market in the global cruise shipbuilding industry.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, Meyer Werft continues to strengthen its position as a leading player in the global cruise ship building market by leveraging its advanced shipbuilding technologies and strong European heritage. The company focuses on delivering highly customized and environmentally sustainable vessels that meet evolving regulatory requirements and customer preferences.

Fincantieri S.p.A. maintains its competitive edge by expanding its production capacity and investing in innovative design solutions that enhance passenger experience and operational efficiency. The company’s strategic collaborations and diversified portfolio across luxury and mainstream cruise segments enable it to capture a broad client base globally.

Mitsubishi Heavy Industries plays a significant role by integrating cutting-edge engineering and precision manufacturing capabilities, focusing on fuel efficiency and emission reduction technologies. Their strong presence in the Asian shipbuilding sector positions them well to capitalize on the growing cruise demand in the region.

China State Shipbuilding Corporation (CSSC) is rapidly advancing through significant government support and investment, aiming to increase its share in the global cruise ship market. CSSC’s focus on scaling up production capabilities and adopting modern shipbuilding standards allows it to compete effectively with established European builders.

Together, these key players drive innovation and growth in the cruise ship building industry by responding to market demands for larger, greener, and more technologically advanced vessels, thereby shaping the future trajectory of the market.

Top Key Players in the Market

- Meyer Werft

- Fincantieri S.p.A.

- Mitsubishi Heavy Industries

- China State Shipbuilding Corporation (CSSC)

- STX France

- Samsung Heavy Industries

- Cochin Shipyard Limited

- Carnival Corporation

- Royal Caribbean International

- Norwegian Cruise Line Holdings

Recent Developments

- In February 2025, Italy’s Fincantieri secured a significant contract from Norwegian Line, receiving a cruise ship order valued at US$9 billion, marking a major milestone in its shipbuilding portfolio. This deal reinforces Fincantieri’s position as a leading player in the global cruise ship construction industry.

- In February 2025, Spanish shipbuilder Navantia finalized the acquisition of Harland & Wolff, expanding its capabilities and footprint in the shipbuilding sector. This strategic takeover enhances Navantia’s presence in the European market and strengthens its competitive edge.

- In December 2024, Hanwha completed a US$100 million acquisition of Philly Shipyard, becoming the first Korean shipbuilder to establish operations in the U.S. This move signifies Hanwha’s commitment to expanding its global shipbuilding reach and tapping into new markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 8.3 Billion |

| Forecast Revenue (2034) | USD 11.6 Billion |

| CAGR (2025-2034) | 3.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Mega Cruise Ship, Luxury Cruise Ship, Mainstream Cruise Ship, Others), By Application (Transportation, Leisure), By Weight (More than 150,000 GT, Less than 1,000 GT, 50,000-100,000 GT, 1,000-50,000 GT, 100,000-150,000 GT), By Fuel Type (Liquified Natural Gas, Marine Diesel Oil, Heavy Fuel Oil), By Passenger Capacity (More than 4,000, 2,000-4,000, 500-2,000, Less than 500) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |