Quick Navigation

Report Overview

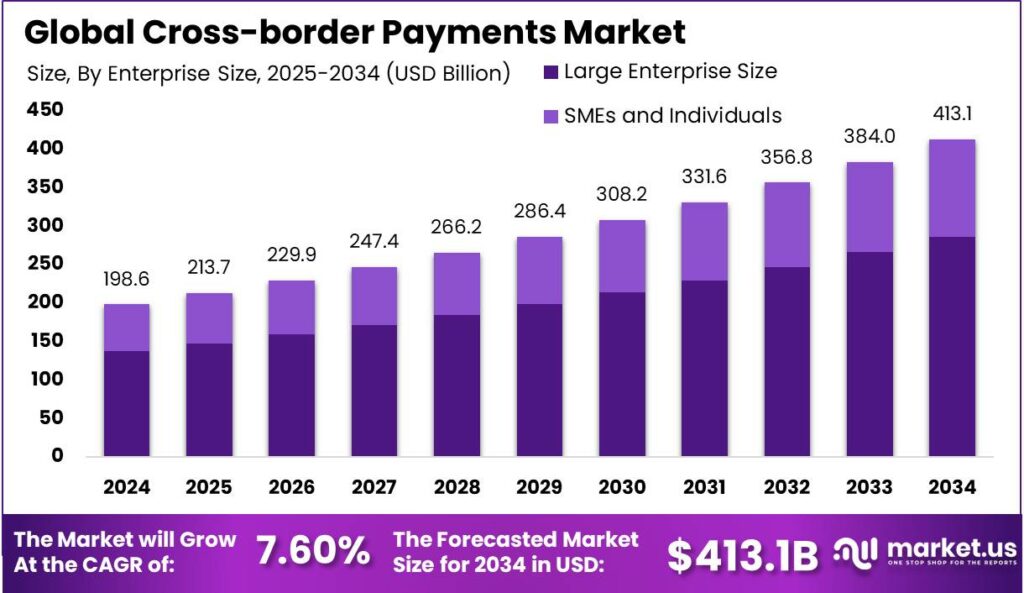

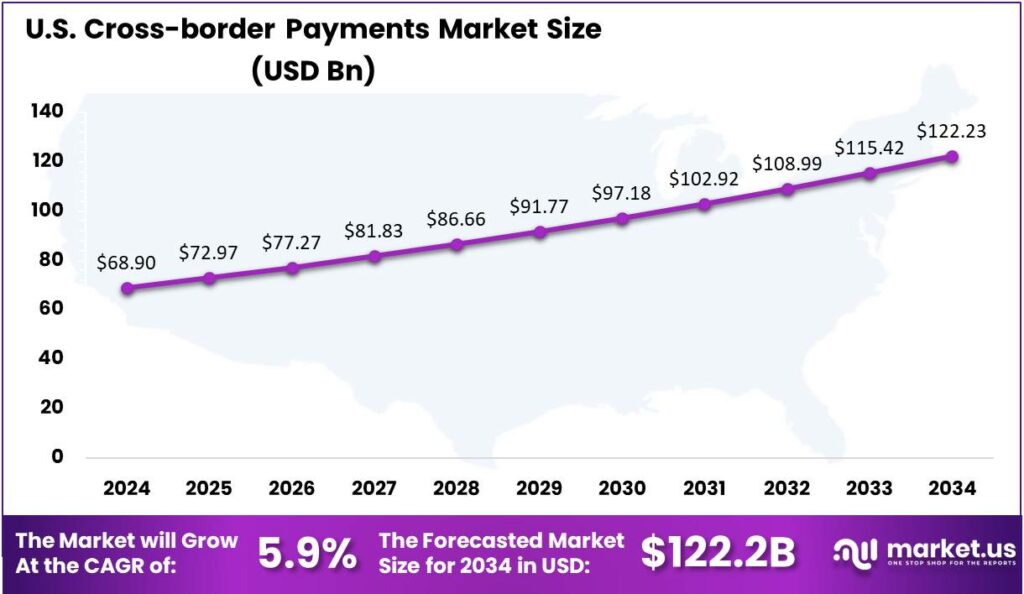

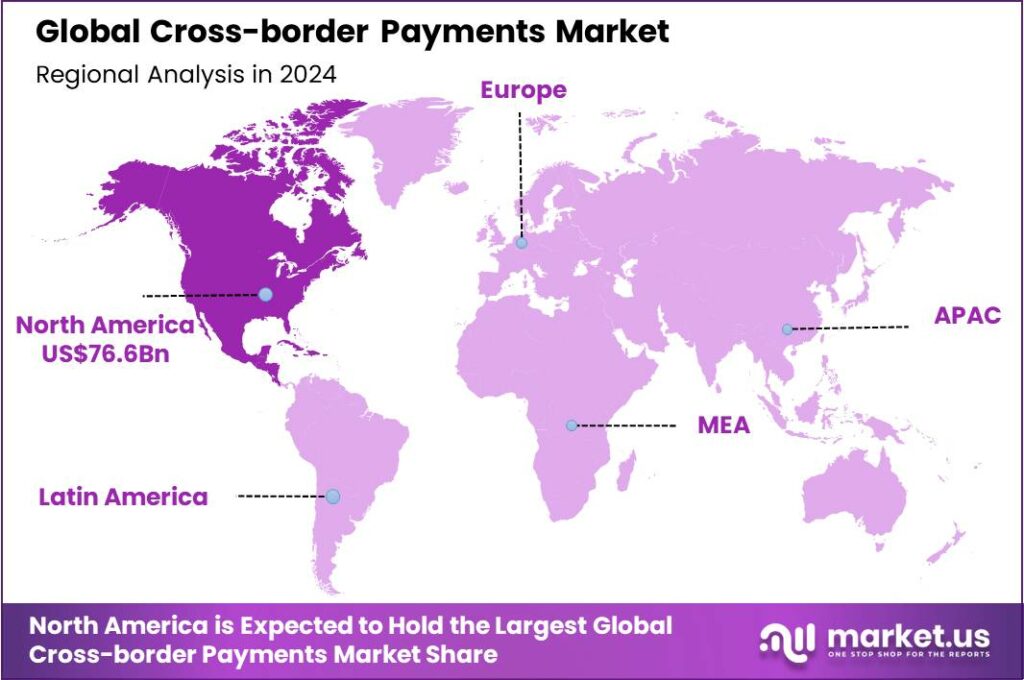

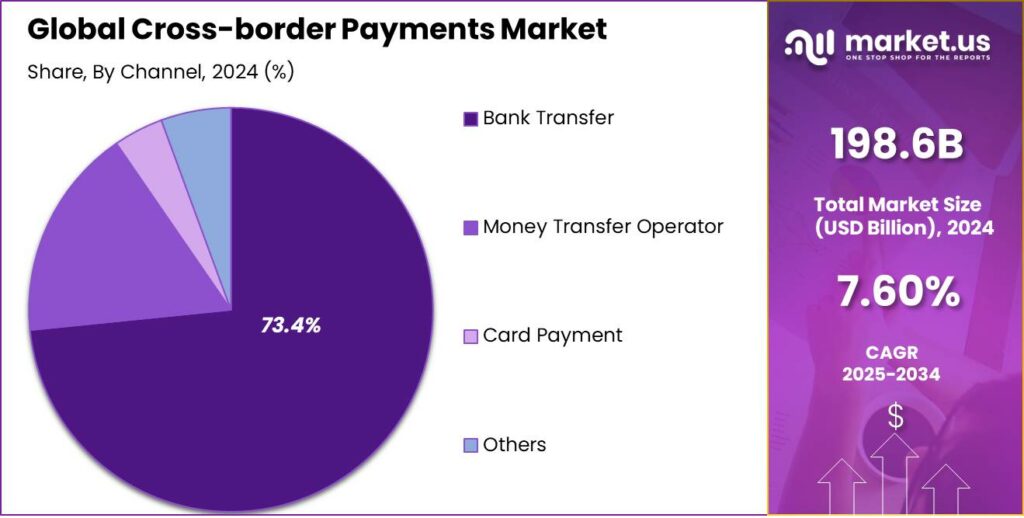

The Global Cross-border Payments Market size is expected to be worth around USD 413.1 Billion By 2034, from USD 198.6 Billion in 2024, growing at a CAGR of 7.60% during the forecast period from 2025 to 2034. In 2024, North America led the market with a 38.6% share, generating USD 76.6 billion. The U.S. market was valued at USD 68.9 billion and is expected to grow at a 5.9% CAGR, driven by trade, remittances, and e-commerce.

The cross-border payments market is undergoing significant transformation, driven by technological advancements, regulatory changes, and evolving consumer expectations. Key drivers of this expansion include the rise of e-commerce, increased international trade, and the proliferation of digital payment technologies. Businesses and consumers alike are seeking faster, more secure, and cost-effective methods for transferring funds across borders.

The adoption of mobile payment platforms and digital wallets has further facilitated this trend, offering convenience and accessibility to a broader user base. Businesses are increasingly adopting cross-border payment solutions to expand their customer base, simplify international transactions, and enhance cash flow management.

As smartphones become more affordable and remote lifestyles grow, consumers are rapidly embracing e-payment solutions for their time-saving convenience. According to GSMA, as of 2024, there are 4.88 billion smartphone users globally, reflecting a sharp increase of 635 million new users in just one year. This accelerating adoption is projected to continue annually, reinforcing the expanding role of mobile devices in digital financial ecosystems.

According to KarbonCard research, B2B transactions account for nearly 97% of all cross-border payments, driven by the rapid rise of e-commerce and global trade activity. Currently, global cross-border payment flows exceed $150 trillion annually, highlighting their critical role in enabling international commerce and economic growth. By 2027, the market is projected to grow by 60%, potentially reaching over $250 trillion in annual flows.

Investment opportunities in cross-border payments are strong, especially in regions experiencing rapid digital transformation. The Asia-Pacific region stands out with growth driven by rising e-commerce and favorable regulations. Investors are targeting fintech startups that use advanced technologies to deliver innovative payment solutions for global businesses and consumers.

Latest trends in cross-border payments include the adoption of real-time payment systems for instant transfers and blockchain technology to ensure secure and transparent transactions. Blockchain ensures secure, transparent transactions with fewer intermediaries. Digital currencies, including CBDCs, aim to cut costs and speed up payments.

Key Takeaways

- The Global Cross-border Payments Market size is expected to reach around USD 413.1 Billion by 2034, up from USD 198.6 Billion in 2024, growing at a CAGR of 7.60% during the forecast period from 2025 to 2034.

- In 2024, the Business to Business (B2B) segment dominated the market, capturing more than 52.7% share of the global cross-border payments market.

- The Large Enterprise Size segment held a dominant position in 2024, accounting for over 69.4% share in the cross-border payments market.

- The Bank Transfer segment was the leading payment method in 2024, with a market share exceeding 73.4% of the global cross-border payments market.

- In 2024, North America dominated the market, accounting for approximately 38.6% of the total market share, generating revenue of USD 76.6 billion.

- The U.S. cross-border payments market was valued at USD 68.9 billion in 2024 and is projected to grow at a CAGR of 5.9%, driven by factors such as international trade, remittances, and global e-commerce.

Business Benefits

Cross-border payments allow businesses to reach global markets, access new customers, and diversify revenue. They reduce reliance on a single market, support international trade, and boost competitiveness and growth. According to Citcon report, around 73% of U.S. companies make cross-border payments every day, showing how routine and essential these transactions have become for modern businesses.

Efficient cross-border payment systems improve cash flow by reducing transaction times and costs. Real-time payments meet consumer expectations and allow businesses to access funds faster, supporting timely reinvestment and operational efficiency. As per the Integrated Research report, a striking 75% of consumers now expect every digital payment to be processed in real-time.

Adopting advanced cross-border payment solutions positions businesses ahead of competitors still reliant on traditional methods. Modern payment systems provide speed, transparency, and security, helping businesses stand out and strengthen relationships with international partners and customers.

U.S. Market Size

In 2024, the U.S. cross-border payments market was valued at USD 68.9 billion, reflecting its strategic importance in facilitating international trade, remittances, and global e-commerce transactions. This sizable valuation underscores the continued demand from multinational corporations, financial institutions, small and medium-sized enterprises (SMEs), and individuals involved in global financial interactions.

The market is expected to expand at a compound annual growth rate (CAGR) of 5.9%, driven by increasing globalization, the proliferation of real-time payment networks, and greater collaboration between financial technology providers and traditional banks. U.S.-based fintech players are actively enhancing the speed, transparency, and cost-efficiency of international money transfers by leveraging blockchain, artificial intelligence, and open banking frameworks.

As AML regulations tighten, the U.S. is investing in RegTech and fraud detection to enhance trust, security, and compliance in international transactions. Government and regulators are working to harmonize global payment systems and promote innovation while protecting consumers. This is transforming the U.S. cross-border payments ecosystem with greater efficiency, lower costs, and improved user experiences.

In 2024, North America held a dominant position in the global cross-border payments market, accounting for approximately 38.6% of the total market share and generating revenue of USD 76.6 billion. This leadership is primarily attributed to the region’s advanced financial infrastructure, widespread adoption of digital payment technologies, and a robust regulatory environment that fosters innovation and trust in cross-border transactions.

The region’s dominance is further reinforced by the presence of major financial institutions and fintech companies that continuously invest in developing efficient and secure cross-border payment solutions. The integration of technologies such as blockchain, artificial intelligence, and open banking APIs has significantly improved transaction speed, transparency, and cost-effectiveness.

North America’s clear regulatory frameworks and strong consumer protections have built confidence among users and providers, fostering the growth of innovative payment platforms. This blend of technology, regulation, and economic activity positions the region as a leading hub for efficient and reliable cross-border payments worldwide.

Transaction Type Analysis

In 2024, the Business to Business (B2B) segment held a dominant market position, capturing more than a 52.7% share of the global cross-border payments market. This dominance was primarily driven by the increasing globalization of supply chains, growing import-export volumes, and a surge in international trade partnerships.

Moreover, the B2B segment benefits from the integration of advanced technologies such as real-time tracking systems, API-enabled treasury solutions, and blockchain-based transaction infrastructures. These tools enhance transparency, cut down processing times, and reduce intermediary costs, making them ideal for large-scale commercial transactions.

Rising demand for compliance-driven solutions in cross-border B2B transactions strengthens the segment’s leadership. Strict AML and KYC rules push businesses to use trusted platforms with built-in regulatory screening and audit trails, reducing legal risks and easing coordination with foreign banks. Financial institutions and fintechs are developing scalable, industry-specific B2B payment solutions to meet this need.

B2B payments have higher transaction values and frequency, boosting their market share. With growing digital trade and international collaboration, especially in emerging markets, B2B cross-border payment systems are set to become even more strategically important, strengthening their dominance.

Enterprise Size Analysis

In 2024, Large Enterprise Size segment held a dominant market position, capturing more than a 69.4% share in the cross-border payments market. This dominance was primarily attributed to the high transaction volumes, complex international payment needs, and frequent multi-currency dealings that large corporations typically manage.

Large enterprises have shown a strong inclination toward integrating real-time payment systems, blockchain networks, and digital ledger technologies to reduce payment delays and reconciliation issues. They benefit significantly from digital automation and API-based integrations that support seamless operations across multiple countries and currencies.

The increasing pressure on global corporations to manage liquidity efficiently across global subsidiaries is another key factor contributing to this segment’s leadership. These companies are focused on reducing costs associated with transaction fees, foreign exchange spreads, and compliance processing delays, which makes investment in advanced cross-border payment ecosystems a strategic priority.

Multinational companies’ focus on centralized cash management has boosted the use of unified global payment platforms, offering real-time payment tracking, improved supplier relations, and better working capital management. With ongoing globalization and growth in emerging markets, large enterprises are set to maintain their dominance in cross-border payments.

Channel Analysis

In 2024, the Bank Transfer segment held a dominant market position, capturing more than a 73.4% share of the global cross-border payments market. This commanding lead can be attributed to the entrenched trust and reliability associated with traditional banking institutions when it comes to handling international money transfers.

The dominance of bank transfers is driven by widespread digital banking integration supporting cross-border payments. Major banks have upgraded infrastructure for faster settlements, greater transparency via SWIFT gpi, and better user experiences. Growing mobile and online banking adoption, especially in developed regions, further boosts the convenience of bank-based cross-border payments.

Corporate clients prefer bank transfers for cross-border payments due to strong regulatory compliance, fraud protection, and efficient bulk processing. Banks’ extensive networks and multi-currency access make them essential for international trade and treasury, reinforcing their reliability across jurisdictions.

While fintech and money transfer operators grow in consumer remittances and low-value payments, banks maintain their lead in cross-border payments due to scale, trust, and robust infrastructure. Continued investments in real-time payment systems and regulatory compliance reinforce banks’ vital role in seamless global financial flows.

Key Market Segments

By Transaction Type

- Business to Business (B2B)

- Customer to Business (C2B)

- Business to Customer (B2C)

- Customer to Customer (C2C)

By Enterprise Size

- Large Enterprise Size

- SMEs and Individuals

By Channel

- Bank Transfer

- Money Transfer Operator

- Card Payment

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Global E-commerce Expansion

The proliferation of global e-commerce has significantly propelled the demand for efficient cross-border payment solutions. As businesses increasingly operate beyond domestic borders, the necessity for seamless international transactions has become paramount.

The growth of digital marketplaces and mobile commerce has heightened the demand for efficient cross-border payment systems. As buyers and sellers connect globally, seamless payment solutions are needed to navigate diverse financial systems and support the rise in international transactions.

Financial institutions and payment providers are adopting technologies like real-time payments and digital wallets to enable faster, more secure, and cost-effective international transactions, meeting the rising demands of global users.

Restraint

Regulatory Fragmentation

Despite technological advancements, regulatory fragmentation remains a significant barrier to the efficiency of cross-border payments. Different countries have varying regulations concerning anti-money laundering (AML), know-your-customer (KYC) requirements, and data protection laws. This lack of harmonization complicates compliance for payment providers operating in multiple jurisdictions.

Divergent regulatory frameworks raise costs and slow down cross-border payments, as providers navigate complex legal requirements. This can discourage smaller businesses from international trade due to added risks and burdens. While global efforts aim to standardize regulations, achieving consensus is challenging, and fragmentation still disrupts smooth payment flows.

Opportunity

Financial Inclusion in Emerging Markets

Cross-border payments offer a key opportunity to improve financial inclusion in emerging markets. By using mobile technology and digital platforms, they can give unbanked individuals access to essential financial services and connect them to the global economy.

Remittances are a key part of enhancing financial inclusion, allowing migrant workers to send money home quickly and securely through efficient cross-border payment systems. These funds support families and drive economic development in recipient countries. Additionally, accessible payment solutions help SMEs in emerging markets engage in global trade, fostering growth, job creation, and reducing poverty.

Challenge

Infrastructure Limitations

Infrastructure limitations, such as outdated systems, limited banking access, and weak telecommunications, significantly hinder the efficiency and reliability of cross-border payments, causing delays and higher costs. Infrastructural gaps can undermine the security of cross-border payments, increasing the risk of fraud and errors.

Poor interoperability between systems often requires manual processing, reducing efficiency. Addressing these issues calls for significant investment in modern payment infrastructure and digital connectivity. Collaboration among governments, financial institutions, and tech providers is crucial to building secure, inclusive, and efficient cross-border payment ecosystems.

Emerging Trends

Cross-border payments are undergoing significant changes, driven by technological advancements and evolving global trade dynamics. One notable trend is the shift towards real-time payment systems. Businesses and consumers increasingly expect immediate transaction settlements, prompting financial institutions to adopt faster payment infrastructures.

Another emerging trend is the integration of blockchain technology and digital currencies. These innovations offer the potential for more secure and transparent transactions by minimizing intermediaries and reducing the risk of errors. Additionally, the adoption of central bank digital currencies (CBDCs) is gaining traction, aiming to streamline cross-border transactions and enhance monetary policy efficiency.

The use of application programming interfaces (APIs) is also transforming the cross-border payment landscape. APIs facilitate seamless communication between different financial systems, enabling more efficient and cost-effective transactions. This interoperability is crucial for businesses operating in multiple countries, as it simplifies payment processes and reduces operational complexities.

Key Player Analysis

As Cross-border Payments Market becomes more competitive, a few key players stand out for their unique strengths and innovative solutions.

PayPal Holdings, Inc. is one of the most recognized names in global digital payments. PayPal’s cross-border services are popular with individuals and businesses, offering multi-currency support and strong security. Its Xoom acquisition further boosts its global transfer capabilities, making it a top choice for fast, reliable payments.

UniTeller, Inc. is known for its strong focus on remittances and international money transfers. Its unique strength lies in providing end-to-end payment solutions, especially for customers sending money to family or businesses in developing countries. UniTeller’s partnerships with banks, retailers, and mobile platforms give it a broad network and an edge in delivering fast, cost-effective transfers.

Banking Circle Group is a newer but rapidly growing player in the cross-border payments space. Banking Circle stands out with its fintech-focused banking infrastructure, providing direct access to cross-border payment networks that reduce costs and processing time. Its emphasis on B2B payments and financial inclusion makes it a next-gen global payments solution.

Top Key Players in the Market

- PayPal Holdings, Inc.

- UniTeller, Inc.

- Banking Circle Group

- FIS

- Brightwell Payments, Inc.

- MoneyGram International, Inc.

- PingPong Global Solutions Inc.

- Adyen N.V.

- Visa Inc.

- Payoneer Inc.

- American Express Company

- Western Union Holdings, Inc.

- Thunes Ltd.

- Stripe, Inc.

- TransferMate

- Others

Top Opportunities for Players

- Real-Time Payments Infrastructure: The demand for instant cross-border transactions is increasing, prompting the development of real-time payment systems. Implementing such infrastructure can improve cash flow management for businesses and provide consumers with faster transaction experiences.

- Digital Wallet Integration: The proliferation of digital wallets offers an avenue for cross-border payment providers to reach a broader customer base. By integrating with popular digital wallets, companies can facilitate seamless international transactions, catering to the growing preference for mobile and contactless payments.

- Regulatory Technology (RegTech) Solutions: Navigating the complex regulatory landscape of cross-border payments is a significant challenge. Investing in RegTech solutions can streamline compliance processes, reduce the risk of regulatory breaches, and enhance operational efficiency. These technologies enable real-time monitoring and reporting, which are crucial for maintaining compliance in multiple jurisdictions.

- Expansion into Emerging Markets: Emerging markets present substantial growth opportunities for cross-border payment providers. These regions often have underserved populations with increasing access to digital technologies. By offering tailored payment solutions that address local needs and preferences, companies can tap into new customer segments and drive financial inclusion.

- Adoption of Blockchain Technology: Blockchain technology has the potential to revolutionize cross-border payments by enhancing transparency, reducing transaction costs, and minimizing settlement times. Implementing blockchain-based solutions can address common pain points in international transactions, such as currency conversion inefficiencies and lack of traceability.

Industry News

- In April 2025, PayPal Holdings, Inc. formed a partnership with TerraPay to enhance cross-border payments in the Middle East and Africa, aiming to connect banks, mobile wallets, and financial institutions for faster money transfers.

- In March 2025, UniTeller, Inc. acquired MORE Payment Evolution to expand its global payment network and improve remittance and business payment capabilities.

- In March 2025, TransferMate and Boost Payment Solutions joined forces, merging Boost’s enterprise payment tech with TransferMate’s global infrastructure to meet the growing demand for seamless cross-border transactions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 198.6 Bn |

| Forecast Revenue (2034) | USD 413.1 Bn |

| CAGR (2025-2034) | 7.60% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Transaction Type (Business to Business (B2B), Customer to Business (C2B), Business to Customer (B2C), Customer to Customer (C2C)), By Enterprise Size (Large Enterprise Size, SMEs and Individuals), By Channel (Bank Transfer, Money Transfer Operator, Card Payment, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | PayPal Holdings, Inc., UniTeller, Inc., Banking Circle Group, FIS, Brightwell Payments, Inc., MoneyGram International, Inc., PingPong Global Solutions Inc., Adyen N.V., Visa Inc., Payoneer Inc., American Express Company, Western Union Holdings, Inc., Thunes Ltd., Stripe, Inc., TransferMate, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |