Global Computational Pathology Market By Component (Software and Services), By Technology (Machine Learning (Deep Learning, Supervised, Unsupervised), Natural Language Processing (NLP) Models and Computer Vision), By Application (Disease Diagnosis, Drug Discovery & Development and Academic Research), By End-User (Hospitals and Diagnostic Labs, Biotechnology and Pharmaceutical Companies and Academic and Research Institutes), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179559

- Number of Pages: 285

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

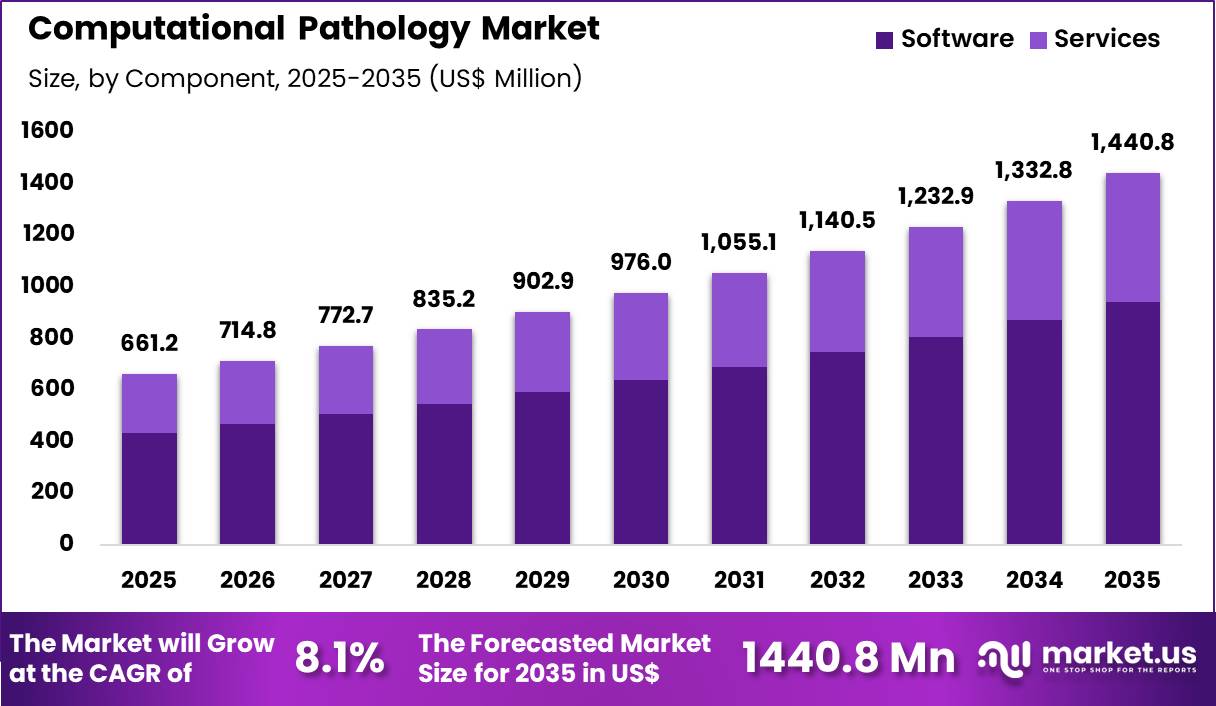

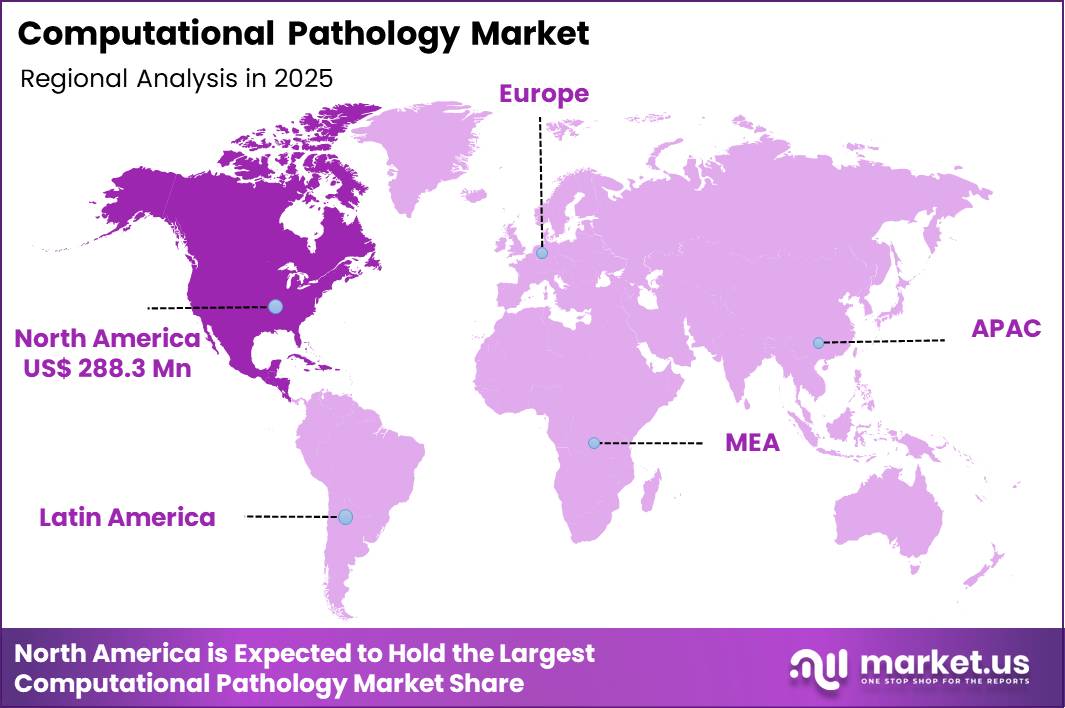

The Global Computational Pathology Market size is expected to be worth around US$ 1440.8 Million by 2035 from US$ 661.2 Million in 2025, growing at a CAGR of 8.1% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 43.6% share with a revenue of US$ 288.3 Million.

Increasing demand for precise diagnostic tools in oncology and pathology accelerates the computational pathology market as healthcare providers adopt AI-driven platforms that analyze digital slides for faster, more accurate disease detection.

Pathologists increasingly apply these systems in cancer diagnostics, where algorithms quantify tumor morphology, mitotic activity, and biomarker expression in breast and prostate biopsies to guide staging and treatment selection.

These platforms support infectious disease pathology by identifying microbial patterns in tissue samples, enabling rapid differentiation of bacterial, viral, or fungal infections in immunocompromised patients. Researchers utilize computational pathology in drug development assays, evaluating tissue responses to therapies through automated image analysis of cellular proliferation and apoptosis markers.

Clinical laboratories employ the technology for autoimmune disorder evaluations, assessing immune cell infiltration and fibrosis in skin or renal biopsies to inform immunosuppressive regimens. Hospitals integrate these tools into workflow automation, streamlining slide scanning and annotation for high-volume caseloads in routine histopathology.

Manufacturers pursue opportunities to embed machine learning models that predict patient outcomes from histopathological data, expanding applications in personalized medicine where prognostic scoring informs adjuvant therapy decisions. Developers advance hybrid systems combining computational pathology with genomic sequencing, broadening utility in companion diagnostics for targeted cancer therapies.

These innovations facilitate remote consultations through cloud-based image sharing, supporting collaborative reviews in multidisciplinary tumor boards. Opportunities emerge in sustainable digital workflows that reduce chemical use in slide preparation while maintaining analytical precision.

Companies invest in user-friendly interfaces with real-time feedback loops, enhancing adoption among pathologists. Recent trends emphasize interoperability with electronic health records and ethical AI frameworks, positioning the market for growth in data-driven pathology focused on efficiency and clinical impact.

Key Takeaways

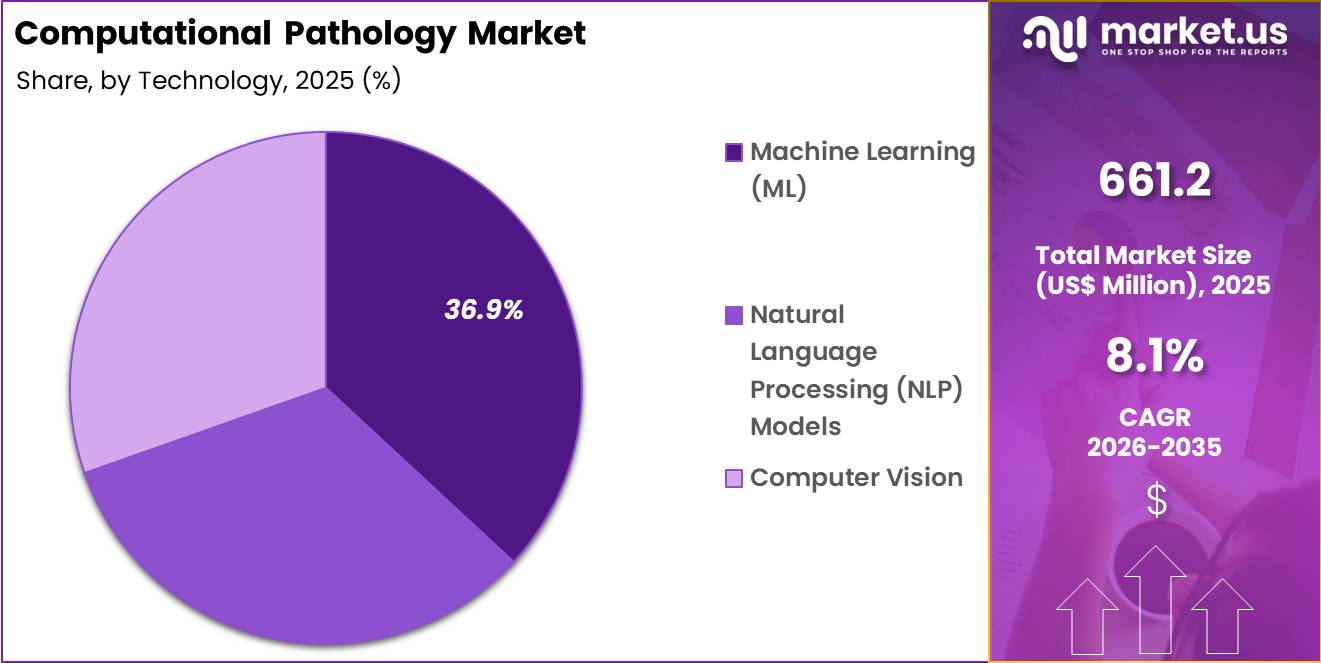

- In 2025, the market generated a revenue of US$ 661.2 Million, with a CAGR of 8.1%, and is expected to reach US$ 1440.8 Million by the year 2035.

- The component segment is divided into software and services, with software taking the lead with a market share of 65.5%.

- Considering technology, the market is divided into machine learning, natural language processing (NLP) models and computer vision. Among these, machine learning (ML)held a significant share of 36.9%.

- Furthermore, concerning the application segment, the market is segregated into disease diagnosis, drug discovery & development and academic research. The disease diagnosis sector stands out as the dominant player, holding the largest revenue share of 43.2% in the market.

- The end-user segment is segregated into hospitals and diagnostic labs, biotechnology and pharmaceutical companies and academic and research institutes, with the hospitals and diagnostic labs segment leading the market, holding a revenue share of 53. 0%.

- North America led the market by securing a market share of 43.6%.

Component Analysis

Software accounted for 65.5% of growth within components and dominates the computational pathology market due to its ability to integrate vast histopathology datasets with predictive analytics. Hospitals and diagnostic labs increasingly adopt software solutions to streamline workflows, improve diagnostic accuracy, and reduce turnaround times.

The segment growth is projected to continue as machine learning algorithms, image recognition tools, and cloud-based platforms enhance pathology automation. Continuous development of user-friendly interfaces and regulatory approvals supports widespread adoption.

Vendors are offering scalable solutions tailored for high-volume laboratories, accelerating implementation. Hospitals leverage software to support multidisciplinary teams and evidence-based decision-making, further driving adoption. Segment growth is anticipated to strengthen as integration with electronic health records and interoperability standards increases system efficiency.

Technology Analysis

Machine learning accounted for 36.9% of growth within technologies and leads due to its capacity to analyze complex tissue patterns and identify subtle diagnostic markers. Integration of ML into pathology workflows allows for rapid, accurate detection of cancers, infectious diseases, and rare conditions.

Hospitals and diagnostic labs adopt ML models to improve diagnostic confidence and optimize patient treatment plans. Segment growth is expected to strengthen as algorithmic precision, continuous learning models, and large annotated datasets enhance prediction capabilities.

Investments in AI research and partnerships with computational pathology vendors accelerate technology adoption. ML-based solutions are increasingly deployed for automated slide analysis, image segmentation, and pattern recognition, supporting clinical decision-making. Growth is projected to continue as validation studies and real-world performance data reinforce reliability and regulatory acceptance.

Application Analysis

Disease diagnosis accounted for 43.2% of growth within applications and remains the leading driver due to rising demand for accurate, fast, and cost-effective pathology solutions. Hospitals and diagnostic labs implement computational pathology tools to detect cancers, autoimmune disorders, and infectious diseases more efficiently.

Segment growth is projected to continue as technological advancements in AI-driven image analysis and predictive analytics improve diagnostic workflows. Integration with laboratory information systems enables streamlined reporting and real-time insights.

Hospitals adopt these solutions to support multidisciplinary teams and precision medicine initiatives. Segment expansion is anticipated as increased awareness, regulatory guidance, and reimbursement incentives encourage adoption across developed and emerging markets.

End-User Analysis

Hospitals and diagnostic labs contributed 53.0% of growth within end-users and dominate due to their high patient volumes and capacity for advanced pathology workflows. These institutions deploy computational pathology to enhance diagnostic accuracy, reduce human error, and optimize treatment planning.

Segment growth is expected to strengthen as hospitals integrate AI tools with existing laboratory infrastructure and invest in staff training programs. Collaboration with software vendors and research organizations facilitates access to cutting-edge algorithms and image analysis platforms.

Demand is projected to increase as hospitals adopt computational pathology for routine diagnostics, clinical trials, and precision medicine initiatives. Growing emphasis on early detection, efficiency, and cost reduction further fuels segment adoption globally.

Key Market Segments

By Component

- Software

- Services

By Technology

- Machine Learning (Deep Learning, Supervised, Unsupervised)

- Natural Language Processing (NLP) Models

- Computer Vision

By Application

- Disease Diagnosis

- Drug Discovery & Development

- Academic Research

By End-User

- Hospitals and Diagnostic Labs

- Biotechnology and Pharmaceutical Companies

- Academic and Research Institutes

Drivers

Increasing adoption of digital pathology systems is driving the market.

The rapid integration of digital pathology systems in laboratories has significantly boosted the computational pathology market by enabling efficient slide scanning and data storage for AI analysis. Healthcare institutions are increasingly transitioning from traditional microscopy to digital workflows to improve diagnostic speed and accuracy.

Pathologists benefit from digital platforms that facilitate remote consultations and collaborative case review. The correlation between digital adoption and reduced diagnostic errors further amplifies demand for computational tools. Government health initiatives promote digital transformation to enhance pathology services in underserved areas.

Digital pathology systems provide scalable infrastructure for large-volume case handling in high-throughput labs. National digital health strategies emphasize interoperability to support computational applications. Key vendors are developing integrated solutions to meet this growing requirement. This driver fosters collaboration between pathologists and IT specialists for optimized workflows.

Restraints

High implementation costs of digital infrastructure is restraining the market.

The substantial capital investment required for digital pathology scanners, storage servers, and software poses a major barrier to computational pathology adoption in smaller laboratories. Complex IT integration with existing hospital systems adds significant setup expenses and technical challenges. Many facilities lack the budget for dedicated personnel to manage digital workflows and data security.

The correlation between implementation costs and delayed ROI deters investment in resource-limited settings. Government funding for digital health is often insufficient to cover full deployment in public institutions. Digital infrastructure demands ongoing maintenance and upgrades, straining operational budgets.

National healthcare policies highlight affordability issues in pathology digitization. Key stakeholders are exploring shared service models to mitigate these costs. This restraint limits scalability for computational tools in non-academic environments. High implementation costs, due to expensive equipment and need for dedicated personnel, remain a key market restraint.

Opportunities

Growing government initiatives for AI in healthcare is creating growth opportunities.

The expansion of national AI programs in healthcare offers avenues for computational pathology to integrate machine learning for automated image analysis. Governmental grants support research into AI-assisted diagnostics to address pathologist shortages.

Increasing focus on precision medicine amplifies potential for computational tools in biomarker detection. Partnerships with public health agencies facilitate pilot programs for AI in cancer screening. The large volume of pathology slides in national health systems magnifies prospects for scalable computational solutions.

Educational initiatives for pathologists promote standardized AI adoption in clinical practice. This opportunity enables vendors to collaborate on government-funded digital pathology projects. Key organizations are establishing AI centers of excellence for pathology applications.

Overall, AI initiatives align with efforts to improve diagnostic equity. Government initiatives and funding for AI in healthcare are a key growth opportunity.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic shifts shape the computational pathology market by influencing hospital budgets, IT infrastructure investment, and healthcare R&D spending. Rising inflation and high interest rates increase costs for advanced imaging software and machine learning platforms, which can slow adoption in smaller labs.

Geopolitical tensions disrupt access to specialized algorithms, cloud services, and high-performance computing components, creating operational challenges. Current US tariffs on imported servers, GPUs, and medical imaging hardware raise acquisition expenses, which squeeze margins and delay deployment timelines. These factors may constrain expansion in cost-sensitive regions and limit upgrades in underfunded facilities.

On the positive side, trade pressures encourage local development of software, service networks, and data centers, improving long-term resilience. Increasing reliance on AI-driven diagnostics and personalized medicine sustains strong demand. With strategic sourcing, software innovation, and scalable services, the market continues on a growth-oriented trajectory.

Latest Trends

FDA clearances for AI-powered pathology tools is a recent trend in the market.

In 2024, regulatory approvals for AI algorithms in pathology have accelerated the integration of computational tools for tissue analysis and disease classification. These clearances enable automated detection of cancer cells in digitized slides with high sensitivity. Manufacturers have prioritized clinical validation to meet FDA requirements for diagnostic use.

Clinical studies in 2024 demonstrated improved workflow efficiency with AI assistance. This development addresses pathologist workload by providing decision support in high-volume cases. The trend emphasizes interoperability with digital pathology scanners for seamless implementation.

Regulatory pathways have evolved to accommodate software as a medical device in pathology. Industry collaborations refine AI models for diverse tissue types. These advancements aim to elevate diagnostic precision while reducing turnaround times in laboratory practice.

Regional Analysis

North America is leading the Computational Pathology Market

North America experienced strong growth in the computational pathology market in 2024, driven by the rapid adoption of digital slide imaging and AI‑assisted analytics in hospitals and diagnostic laboratories. The region accounted for 43.6 % of the global market, reflecting widespread clinical integration of computational tools to enhance diagnostic accuracy and reduce turnaround times.

Growth was supported by increasing cancer prevalence and rising demand for precision medicine, which encouraged healthcare providers to invest in advanced image analysis platforms. Large hospital networks implemented digital workflows that streamline tissue evaluation and enable consistent results across multiple sites.

Collaborations between academic research centers and technology developers accelerated validation of machine-learning algorithms for complex tissue pattern recognition. Government initiatives supporting the adoption of AI and digital diagnostics strengthened confidence in these technologies, prompting faster deployment.

Training programs for pathologists on computational tools further increased adoption in routine clinical practice. A verifiable supporting statistic is that over 70 % of pathology laboratories in the United States had adopted digital pathology systems by 2023, reflecting high uptake of computational solutions.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness significant expansion in the computational pathology market during the forecast period, as hospitals and research institutions modernize pathology infrastructure and adopt AI‑enabled image analysis. Rising incidence of chronic diseases, particularly cancer, is driving demand for more accurate and efficient diagnostic solutions.

Government investments in healthcare digitalization and supportive policies have enabled hospitals in China, India, Japan, and South Korea to integrate computational tools into standard workflows. Partnerships with international technology providers facilitate knowledge transfer and local adaptation of advanced analytical platforms.

Hospitals are increasingly implementing digital pathology systems to handle growing tissue sample volumes while maintaining accuracy. Training initiatives strengthen pathologists’ ability to use computational workflows, encouraging broader adoption.

Telemedicine and remote consultation services further increase the need for digital solutions that enable image sharing and collaborative review. A supporting data point is that approximately 65 % of tertiary care hospitals in China had adopted digital pathology systems by 2023, highlighting growing acceptance of computational analysis in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the computational pathology market grow by advancing machine learning algorithms, high‑resolution imaging platforms, and interoperable software that help pathology teams extract deeper diagnostic insights and streamline workflows. They also strengthen customer value by integrating data management tools and analytics dashboards that support multidisciplinary collaboration and accelerate case turnaround in clinical and research settings.

Firms pursue strategic partnerships with hospitals, academic medical centers, and digital health platforms to embed solutions into existing clinical infrastructure and expand recurring utilization across care networks. Geographic expansion into North America, Europe, and high‑growth Asia Pacific diversifies revenue streams and captures rising demand for precision diagnostics and AI‑enabled pathology services.

Indica Labs, Inc. exemplifies a specialized digital pathology company with a robust suite of image analysis and artificial intelligence tools, strong engagement with research and clinical partners, and coordinated commercialization strategies that align technological innovation with end‑user needs.

The company advances its competitive agenda through disciplined investment in algorithm development, targeted collaborations that extend scientific reach, and a customer‑centric approach that translates analytical power into measurable operational benefit.

Top Key Players

- Danaher Corporation (Leica Biosystems)

- Hamamatsu Photonics K.K.

- F. Hoffmann-La Roche Ltd. (Ventana)

- Aiforia

- Olympus Corporation (Evident)

- Paige AI, Inc.

- Mindpeak GmbH

- Visiopharm A/S

- Proscia Inc.

- Epredia (3DHISTECH Ltd.)

- Akoya Biosciences, Inc.

- Koninklijke Philips N.V.

Recent Developments

- In 2025, Roche reported that its Diagnostics Division, which includes digital and computational pathology solutions, generated annual revenues of US$ 16.52 billion (CHF 14.1 billion). As per the company’s year-end financial report, growth was supported by the increased adoption of the Navify Digital Pathology platform and the expansion of its AI-based image analysis algorithms for oncology diagnostics in the US.

- In 2026, Philips disclosed that its Enterprise Diagnostic Informatics business, encompassing its digital pathology portfolio, contributed to a total professional healthcare revenue of US$ 19.1 billion (EUR 18.2 billion) for the prior fiscal year. According to company disclosures in early 2026, the integration of generative AI into its pathology workflow has improved slide digitization speeds, supporting large-scale laboratory transitions to digital primary diagnosis.

Report Scope

Report Features Description Market Value (2025) US$ 661.2 Million Forecast Revenue (2035) US$ 1440.8 Million CAGR (2026-2035) 8.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component (Software and Services), By Technology (Machine Learning (Deep Learning, Supervised, Unsupervised), Natural Language Processing (NLP) Models and Computer Vision), By Application (Disease Diagnosis, Drug Discovery & Development and Academic Research), By End-User (Hospitals and Diagnostic Labs, Biotechnology and Pharmaceutical Companies and Academic and Research Institutes) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Danaher, Hamamatsu, Roche, Aiforia, Olympus, Paige AI, Mindpeak, Visiopharm, Proscia, Epredia, Akoya Biosciences, Philips. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Computational Pathology MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Computational Pathology MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Danaher Corporation (Leica Biosystems)

- Hamamatsu Photonics K.K.

- F. Hoffmann-La Roche Ltd. (Ventana)

- Aiforia

- Olympus Corporation (Evident)

- Paige AI, Inc.

- Mindpeak GmbH

- Visiopharm A/S

- Proscia Inc.

- Epredia (3DHISTECH Ltd.)

- Akoya Biosciences, Inc.

- Koninklijke Philips N.V.

Our Clients

- 179559

- Feb 2026