Global Commercial Aircraft Manufacturing Market Size, Share, Growth Analysis By Aircraft Type (Narrowbody Aircraft, Widebody Aircraft, Regional Jets, Turboprop Aircraft, Business Jets, Helicopters, Amphibious Aircraft, Others), By Component (Airframe, Engine, Avionics, Landing Gear, Others), By End-User (Passenger Airlines, Cargo Airlines, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 183398

- Number of Pages: 398

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

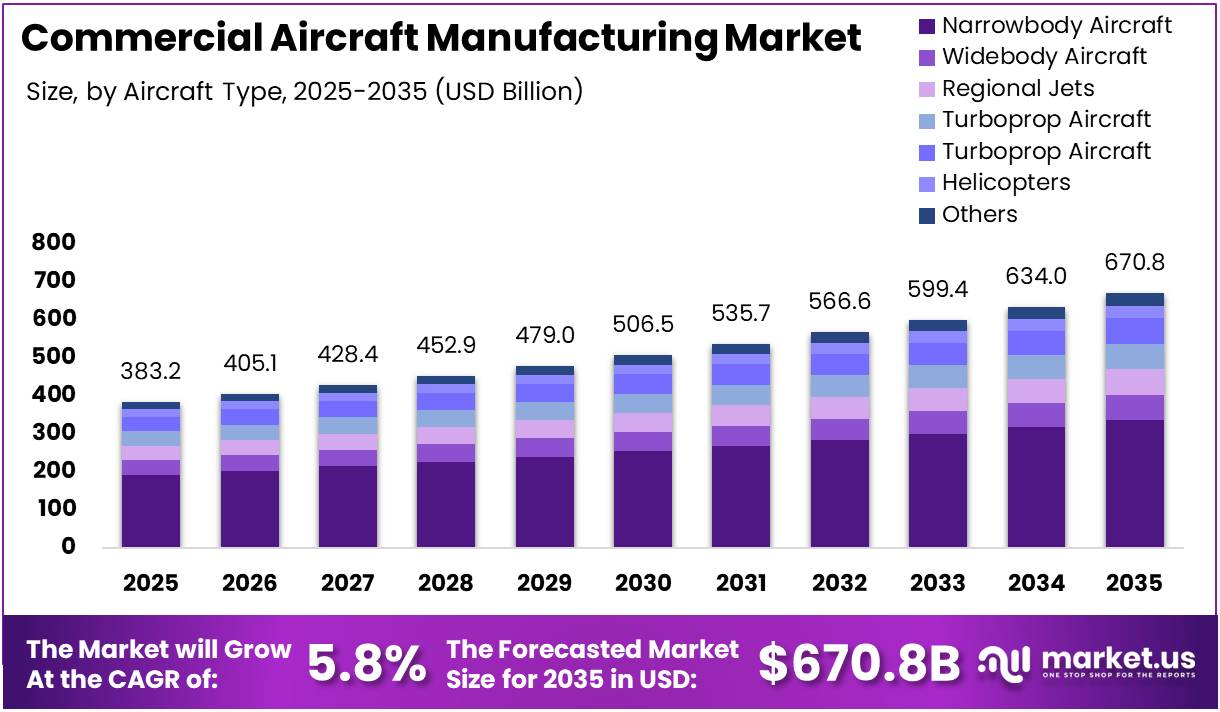

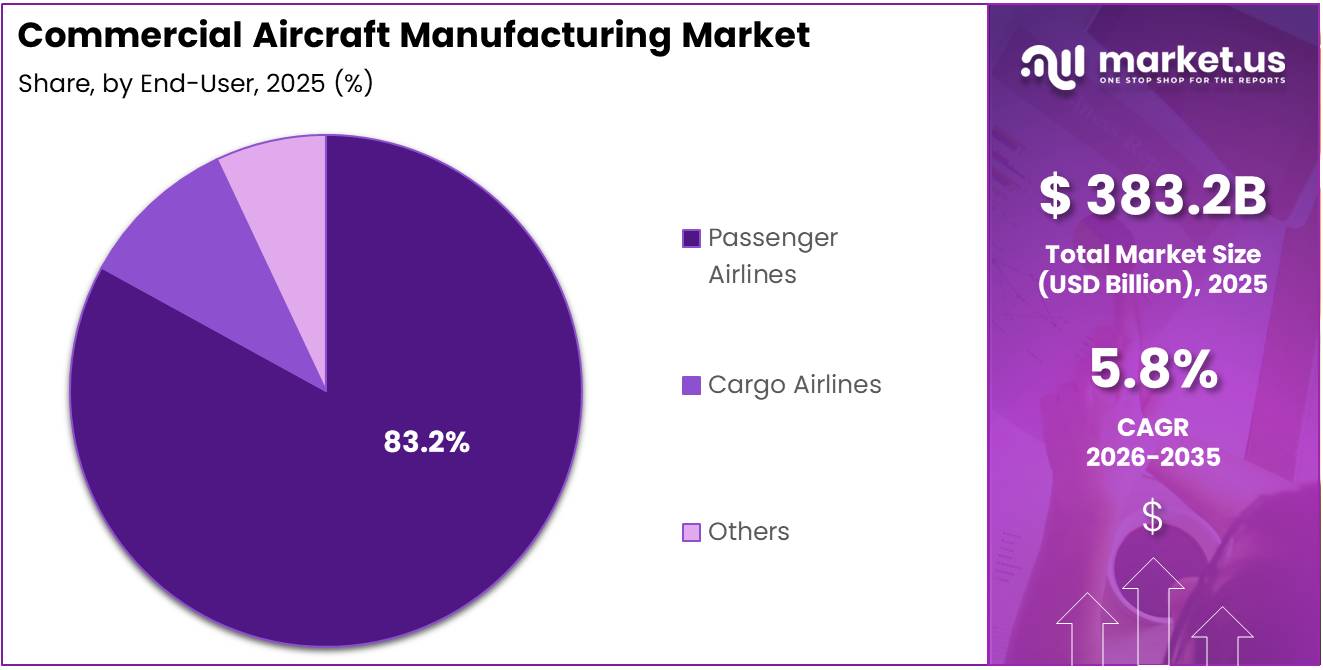

The Global Commercial Aircraft Manufacturing Market size is expected to be worth around USD 670.8 Billion by 2035 from USD 383.2 Billion in 2025, growing at a CAGR of 5.8% during the forecast period 2026 to 2035.

The commercial aircraft manufacturing market encompasses the design, production, and assembly of civil aviation aircraft for passenger and cargo operations. It covers a wide range of aircraft types including narrowbody jets, widebody platforms, regional jets, turboprops, business jets, and helicopters. The industry spans complex global supply chains involving airframe fabrication, engine integration, avionics installation, and rigorous systems testing.

Post-pandemic recovery has significantly boosted global air travel demand, creating strong order pipelines for commercial aircraft worldwide. Airlines across all regions are renewing aging fleets with more fuel-efficient models to reduce operational costs and emissions. Consequently, original equipment manufacturers are scaling production capacity to meet growing backlogs from both established and emerging aviation markets.

Governments and aviation authorities are actively investing in sustainable aviation technologies including electric propulsion and hybrid-electric aircraft development. Regulatory frameworks supporting carbon-neutral aviation goals are accelerating research and development spending industry-wide. Moreover, strategic partnerships between aerospace OEMs and technology startups are driving innovation in lightweight materials and advanced manufacturing processes.

Regulatory agencies such as the FAA and EASA continue to enforce stringent certification requirements for new aircraft platforms. These standards ensure passenger safety while encouraging manufacturers to adopt advanced materials and digital design tools. Therefore, compliance-driven investments are reshaping product development cycles and pushing manufacturers toward more rigorous quality management systems globally.

According to a study published on arXiv, advanced morphing wing designs can achieve up to 25% drag reduction and 40% improvement in control authority, highlighting major efficiency gains in next-generation aircraft. Additionally, according to Reuters, US factory orders for commercial aircraft surged 97.6% in November 2025, reflecting strong demand momentum across the industry.

According to Reuters, defects from key supplier Spirit AeroSystems on Boeing 737 fuselages fell approximately 60% after enhanced inspections, while Boeing now spends 40% fewer hours resolving supplier-related quality issues compared with 2024. Furthermore, according to Forecast International, the average production-to-delivery lead time in January 2026 was 28.8 days for narrowbodies and 33.5 days for widebodies, indicating evolving delivery cadence across the sector.

Key Takeaways

- The Global Commercial Aircraft Manufacturing Market was valued at USD 383.2 Billion in 2025.

- The market is projected to reach USD 670.8 Billion by 2035, growing at a CAGR of 5.8% from 2026 to 2035.

- By Aircraft Type, Narrowbody Aircraft holds the leading position with a 49.6% market share.

- By Component, the Airframe segment dominates with a 39.4% share.

- By End-User, Passenger Airlines account for the largest share at 83.2%.

- North America leads all regions with a 45.80% market share, valued at USD 175.5 Billion.

Aircraft Type Analysis

Narrowbody Aircraft dominates with 49.6% due to high demand from low-cost and short-haul carriers.

In 2025, Narrowbody Aircraft held a dominant market position in the By Aircraft Type segment of the Commercial Aircraft Manufacturing Market, with a 49.6% share. These aircraft are the preferred choice of low-cost and short-to-medium haul operators due to lower operational costs and higher frequency capabilities. Strong order pipelines for fuel-efficient narrowbody platforms continue to reinforce this segment’s leading position globally.

Widebody Aircraft serve long-haul international routes and are the preferred choice of full-service airlines seeking high passenger capacity per flight. These platforms support transoceanic and intercontinental operations where range and efficiency are critical priorities. Moreover, growing demand from Gulf-based and Asian carriers for new long-haul fleets is sustaining strong widebody order activity globally.

Regional Jets connect smaller cities and secondary airports to major aviation hubs, playing a vital role in national connectivity strategies. These aircraft are well-suited for thinner routes where full-size narrowbody jets are not commercially viable. Additionally, rising demand in Asia Pacific and Latin America is driving incremental fleet expansion among regional and commuter airline operators.

Turboprop Aircraft serve remote and short-distance routes that require lower infrastructure investment and shorter runway capabilities. These aircraft are essential for island connectivity, rural air services, and developing aviation markets with limited airport facilities. Consequently, turboprops remain a preferred and cost-effective solution for operators serving geographically challenging destinations.

Business Jets cater to premium charter, private, and corporate travel segments requiring flexible scheduling and exclusive cabin experiences. Demand for business aviation has expanded steadily, supported by high-net-worth individual travel and corporate fleet procurement. Furthermore, manufacturers are introducing newer, more fuel-efficient business jet platforms with extended range capabilities to attract premium buyers.

Helicopters serve a broad range of commercial applications including offshore energy support, emergency medical services, and search and rescue operations. Their vertical takeoff and landing capability makes them indispensable in environments where fixed-wing aircraft cannot operate. Therefore, helicopter demand remains closely tied to energy sector activity, emergency services investment, and urban air mobility development programs.

Amphibious Aircraft are uniquely designed to operate from both land runways and open water surfaces, making them essential for island communities and coastal service operators. These platforms are widely used in firefighting, maritime patrol, and remote wilderness access missions. Consequently, steady procurement from government agencies and utility operators ensures consistent demand within this specialized segment.

Others in the aircraft type segment include experimental platforms, special mission aircraft, and emerging aviation categories that do not fit within standard commercial classifications. These aircraft are typically procured for government-linked programs, scientific research, or early-stage commercial aviation development initiatives. Therefore, this category continues to grow gradually as new aviation technologies and unconventional aircraft concepts move closer to operational deployment.

Component Analysis

Airframe dominates with 39.4% due to its role as the core structural element of every aircraft.

In 2025, Airframe held a dominant market position in the By Component segment of the Commercial Aircraft Manufacturing Market, with a 39.4% share. The airframe forms the fundamental structural backbone of any commercial aircraft, making it the most cost-intensive component category. Increasing adoption of lightweight composite materials is enhancing structural performance while reducing overall aircraft weight significantly.

Engine programs represent one of the most investment-intensive areas within commercial aircraft manufacturing, with a strong focus on fuel efficiency and emissions reduction. Advanced turbofan engines are being developed to deliver significantly lower fuel burn per flight cycle. Moreover, leading propulsion manufacturers are actively investing in next-generation engine architectures to meet tightening global emissions standards.

Avionics systems are evolving rapidly as digital transformation accelerates across the commercial aviation sector. Modern avionics platforms integrate digital cockpit displays, AI-assisted navigation tools, and real-time aircraft health monitoring capabilities. Additionally, increasing regulatory requirements for enhanced situational awareness and communication systems are driving sustained investment in avionics upgrades across global airline fleets.

Landing Gear systems are a critical safety component undergoing continuous material and engineering innovation to reduce weight and improve durability. These systems must meet rigorous certification standards and perform reliably across thousands of flight cycles throughout an aircraft’s operational life. Consequently, manufacturers are adopting advanced alloys and composite materials to enhance landing gear performance while reducing overall structural weight.

Others within the component segment include hydraulic systems, aircraft cabin interiors, electrical assemblies, and fuel management systems that collectively support full aircraft functionality. These components are essential to operational reliability, passenger comfort, and overall maintenance efficiency for airline operators. Therefore, sustained demand for component upgrades and replacements ensures steady and recurring revenue opportunities across the broader commercial aircraft manufacturing supply chain.

End-User Analysis

Passenger Airlines dominate with 83.2% due to sustained global demand for commercial passenger air travel.

In 2025, Passenger Airlines held a dominant market position in the By End-User segment of the Commercial Aircraft Manufacturing Market, with a 83.2% share. Passenger airlines represent the single largest and most consistent source of commercial aircraft demand worldwide. Post-pandemic travel recovery and large-scale fleet renewal programs have driven sustained aircraft procurement across both full-service and low-cost carriers.

Cargo Airlines have emerged as an increasingly important end-user segment following the global e-commerce expansion and pandemic-driven freight demand surge. Dedicated freighter aircraft orders have grown substantially as logistics operators seek higher-capacity and more fuel-efficient cargo platforms. This segment is expected to sustain demand, particularly for widebody freighter variants and new-build cargo aircraft orders.

Others in this end-user category include government fleets, charter operators, and special mission aircraft buyers. These customers typically require customized aircraft configurations that differ from standard commercial production specifications. Therefore, this segment creates unique manufacturing opportunities for OEMs capable of offering tailored solutions to government-linked and defense-adjacent commercial aviation operators worldwide.

Key Market Segments

By Aircraft Type

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Jets

- Turboprop Aircraft

- Business Jets

- Helicopters

- Amphibious Aircraft

- Others

By Component

- Airframe

- Engine

- Avionics

- Landing Gear

- Others

By End-User

- Passenger Airlines

- Cargo Airlines

- Others

Drivers

Rising Air Travel Demand and Green Aviation Investments Drive Commercial Aircraft Manufacturing Market Growth

The commercial aircraft manufacturing market is strongly driven by the rapid recovery of global air travel demand following the pandemic. Passenger traffic has rebounded to pre-pandemic levels across most key regions, prompting airlines to accelerate fleet renewal and expansion programs. Consequently, aircraft order backlogs at major OEMs have grown substantially, creating robust and sustained production demand globally.

Technological advancements in fuel-efficient aircraft design represent another critical market driver. Manufacturers are developing next-generation turbofan engines, lightweight composite airframes, and improved aerodynamic configurations to reduce fuel burn and operating costs. Moreover, airlines are actively prioritizing modern, sustainable aircraft to meet both evolving regulatory requirements and growing passenger expectations for environmentally responsible air travel.

Increasing government and private sector investment in sustainable and green aviation technologies is reshaping aircraft manufacturing priorities worldwide. Significant funding is being directed toward electric propulsion research, hydrogen-powered aircraft development, and sustainable aviation fuel adoption programs. Therefore, these initiatives are creating new aircraft product categories and generating long-term demand for cleaner, more efficient commercial aircraft across global markets.

Restraints

Regulatory Complexity and Supply Chain Disruptions Restrain Commercial Aircraft Manufacturing Market Growth

Stringent regulatory and certification requirements represent one of the most significant barriers in the commercial aircraft manufacturing market. New aircraft models must undergo extensive safety certification processes governed by authorities such as the FAA and EASA. Consequently, the time and cost required to bring new aircraft designs to market are substantially higher than in many other advanced manufacturing industries.

Supply chain disruptions continue to impact production timelines and aircraft delivery schedules across the entire industry. Material shortages, labor constraints, and quality control issues at key suppliers have created notable bottlenecks in manufacturing workflows. Moreover, geopolitical tensions and trade restrictions add further complexity to a global supply chain that relies on thousands of components sourced from multiple countries simultaneously.

These combined challenges force aircraft manufacturers to balance innovation priorities with compliance obligations and operational efficiency demands. Delays in certification approvals can push back aircraft entry-into-service dates, directly affecting airline operational planning and order commitments. Therefore, manufacturers must invest heavily in supply chain resilience, regulatory engagement, and quality management infrastructure to sustain reliable long-term production growth.

Growth Factors

Electric Aircraft Development and Advanced Materials Adoption Accelerate Commercial Aircraft Manufacturing Market Expansion

The development of electric aircraft and hybrid-electric commercial aircraft represents a transformational growth opportunity for the commercial aircraft manufacturing market. Airlines and regulators are increasingly supportive of zero-emission aviation solutions designed for short-haul routes. Consequently, investment in electric propulsion technology is accelerating, with multiple prototype aircraft already undergoing active flight testing and early-stage certification processes globally.

Adoption of advanced materials such as carbon fiber composites is enabling manufacturers to build significantly lighter, stronger, and more fuel-efficient aircraft. These materials reduce structural weight considerably, improving overall performance and lowering lifecycle operating costs for airline operators. Moreover, growing material availability and declining production costs are making composite adoption increasingly practical across multiple commercial aircraft categories and production volumes.

Strategic partnerships between OEMs and aerospace technology startups are emerging as a key growth catalyst across the commercial aircraft manufacturing market. Startups are contributing innovations in digital manufacturing, advanced propulsion systems, and novel materials science that larger manufacturers can integrate at production scale. Therefore, these collaborative ecosystems between established aerospace firms and agile technology companies are driving faster and more efficient innovation cycles industry-wide.

Emerging Trends

Digital Twin Technology and Net-Zero Aviation Goals Reshape the Commercial Aircraft Manufacturing Market Landscape

The implementation of digital twin and predictive maintenance technologies is one of the most impactful emerging trends in the commercial aircraft manufacturing market. Digital twins create real-time virtual replicas of aircraft systems, enabling manufacturers and operators to anticipate component failures before they occur. Consequently, this approach reduces unplanned maintenance costs, improves aircraft operational availability, and shortens overall production cycle times.

The aviation industry’s focus on reducing carbon emissions and achieving net-zero aviation goals is fundamentally reshaping product development priorities across the market. Manufacturers are investing heavily in sustainable aviation fuel compatibility, aerodynamic optimization, and next-generation low-emission engine technologies. Moreover, international frameworks such as CORSIA are accelerating the adoption of cleaner aircraft designs across global airline fleets and procurement strategies.

Integration of artificial intelligence and automation in both manufacturing and design processes is transforming how commercial aircraft are engineered and produced. AI-driven tools are enhancing quality control precision, optimizing production scheduling, and accelerating engineering design iteration cycles. Therefore, manufacturers that are adopting smart factory technologies are gaining measurable competitive advantages through faster production ramp-ups, lower defect rates, and improved resource utilization.

Regional Analysis

North America Dominates the Commercial Aircraft Manufacturing Market with a Market Share of 45.80%, Valued at USD 175.5 Billion

North America holds the leading position in the commercial aircraft manufacturing market, accounting for a dominant 45.80% share valued at USD 175.5 Billion in 2025. The United States is home to major global OEMs and a highly developed aerospace supply chain ecosystem. Strong government defense investments, large-scale fleet modernization programs by US carriers, and high production activity from established manufacturers firmly support this region’s leading market position.

Europe Commercial Aircraft Manufacturing Market Trends

Europe is a premier hub for commercial aircraft production, anchored by a strong industrial base across Germany, France, the United Kingdom, and Spain. The region benefits from world-class manufacturing infrastructure and a mature, deeply integrated supplier ecosystem. Additionally, European manufacturers are at the forefront of sustainable aviation innovation and continue to attract substantial aircraft orders from airlines across all global markets.

Asia Pacific Commercial Aircraft Manufacturing Market Trends

Asia Pacific is among the fastest-growing regions in the commercial aircraft manufacturing market, driven by surging air travel demand in China, India, and Southeast Asia. Domestic fleet expansion programs and strong economic growth are accelerating aircraft procurement across the region. Moreover, several Asia Pacific governments are actively investing in building local aerospace manufacturing capabilities to reduce long-term dependence on imported aircraft and components.

Latin America Commercial Aircraft Manufacturing Market Trends

Latin America presents moderate but steady growth potential for the commercial aircraft manufacturing market. Brazil remains the primary aviation production hub in the region, with a globally recognized manufacturer contributing regional jet platforms to airlines worldwide. Additionally, airlines in Mexico and Brazil are gradually expanding their fleets, generating incremental and consistent demand for narrowbody and regional commercial aircraft.

Middle East and Africa Commercial Aircraft Manufacturing Market Trends

The Middle East and Africa region is emerging as a growing market for commercial aircraft procurement and aviation infrastructure investment. Gulf-based carriers continue to place significant widebody aircraft orders to expand their extensive international route networks. Furthermore, African aviation markets are developing gradually, supported by regional connectivity initiatives and infrastructure investment programs that are steadily driving demand for smaller and medium-sized commercial aircraft platforms.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Boeing is the world’s largest commercial aircraft manufacturer and a foundational pillar of the global aerospace industry. The company produces a wide portfolio of narrowbody and widebody aircraft, including the widely operated 737 MAX and 787 Dreamliner families. Boeing has been actively addressing supply chain quality improvements and working through a substantial global order backlog. These efforts reflect a renewed focus on manufacturing excellence and long-term delivery commitments.

Airbus has established itself as the world’s leading commercial aircraft deliveries provider and a dominant force in the global aerospace market. The A320neo family leads the narrowbody segment, while the A350 and A330neo effectively serve long-haul international routes for major carriers. Airbus continues to scale production rates, secure large new orders, and expand its industrial footprint across Europe and Asia to meet growing and sustained global aircraft demand.

Lockheed Martin is primarily a defense-focused aerospace manufacturer with deep capabilities in advanced aircraft systems and military aviation platforms. While its direct commercial aviation footprint is more limited, the company contributes critical innovations in aerodynamics, composite materials, and avionics systems that influence the broader aerospace manufacturing sector. Its technology investments frequently serve as a foundation for next-generation civil aircraft development programs pursued by the wider industry.

Northrop Grumman operates as a leading aerospace and defense technology company with strong expertise in advanced aircraft structures, systems integration, and autonomous aviation technologies. The company’s manufacturing capabilities and materials science research are increasingly relevant to emerging commercial aircraft platforms. Additionally, its strategic role within global aerospace supply chains provides key structural components and specialized systems that are used across multiple active aviation programs worldwide.

Key Players

- Boeing

- Airbus

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- General Dynamics

- Embraer

- Bombardier

- Textron Aviation

- Dassault Aviation

Recent Developments

- March 2026 – Airbus received a landmark order for 101 A320neo aircraft from China Eastern Airlines, with the deal valued at approximately USD 15.8 Billion. This transaction reinforces strong demand for narrowbody aircraft across Asia Pacific’s rapidly expanding aviation market.

- January 2026 – Embraer confirmed its participation at Wings India 2026, showcasing two of its commercial aircraft, the E195-E2 and E175, to a key South Asian aviation audience. The event underscored Embraer’s strategic focus on expanding its presence in the growing Indian aviation market.

- January 2026 – Embraer and Adani Defence and Aerospace signed an expanded strategic partnership aimed at deepening collaboration in aerospace manufacturing and MRO services in India. This agreement signals growing momentum for regional aircraft platform development and local production capabilities across the Indian subcontinent.

- December 2025 – Boeing completed a USD 4.7 Billion acquisition of Spirit AeroSystems, bringing a critical fuselage and component supplier directly under its ownership. This move is expected to improve Boeing’s supply chain control, production quality, and overall delivery performance going forward.

- December 2025 – Airbus completed the acquisition of selected Spirit AeroSystems manufacturing sites as part of a broader restructuring of the global aerospace supply chain. This strategic step allows Airbus to strengthen vertical integration and enhance oversight of key component production for its commercial aircraft programs.

Report Scope

Report Features Description Market Value (2025) USD 383.2 Billion Forecast Revenue (2035) USD 670.8 Billion CAGR (2026-2035) 5.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Aircraft Type (Narrowbody Aircraft, Widebody Aircraft, Regional Jets, Turboprop Aircraft, Business Jets, Helicopters, Amphibious Aircraft, Others), By Component (Airframe, Engine, Avionics, Landing Gear, Others), By End-User (Passenger Airlines, Cargo Airlines, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Boeing, Airbus, Lockheed Martin, Northrop Grumman, Raytheon Technologies, General Dynamics, Embraer, Bombardier, Textron Aviation, Dassault Aviation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Commercial Aircraft Manufacturing MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Commercial Aircraft Manufacturing MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Boeing

- Airbus

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- General Dynamics

- Embraer

- Bombardier

- Textron Aviation

- Dassault Aviation

Our Clients

- 183398

- March 2026