Global Chromatography Instrumentation Market By Chromatography Systems (Liquid Chromatography, Thin-Layer Chromatography, Gas Chromatography and Supercritical Fluid Chromatography), By Consumables (Columns, Solvents, Syringes and Others), By Accessories (Column Accessories, Pumps, Auto-Sampler Accessories and Others), By Application (Pharmaceutical firms, Agriculture, Clinical research organizations and Environmental Testing), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178480

- Number of Pages: 219 and 221

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

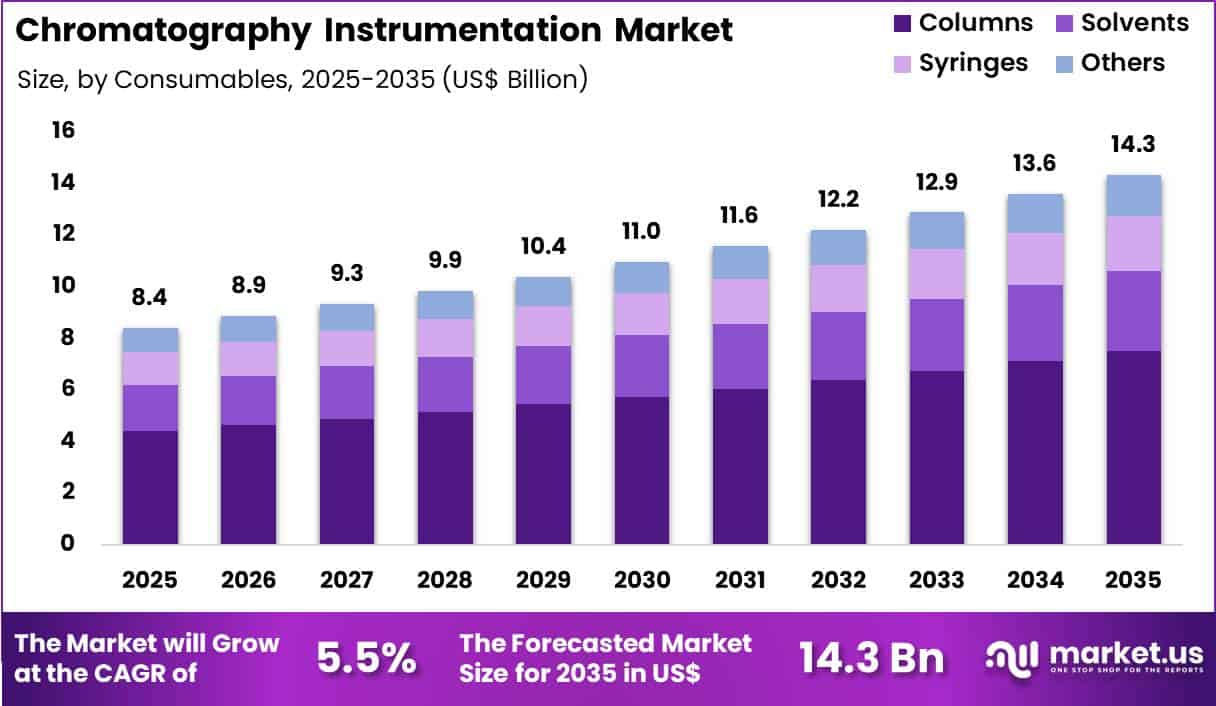

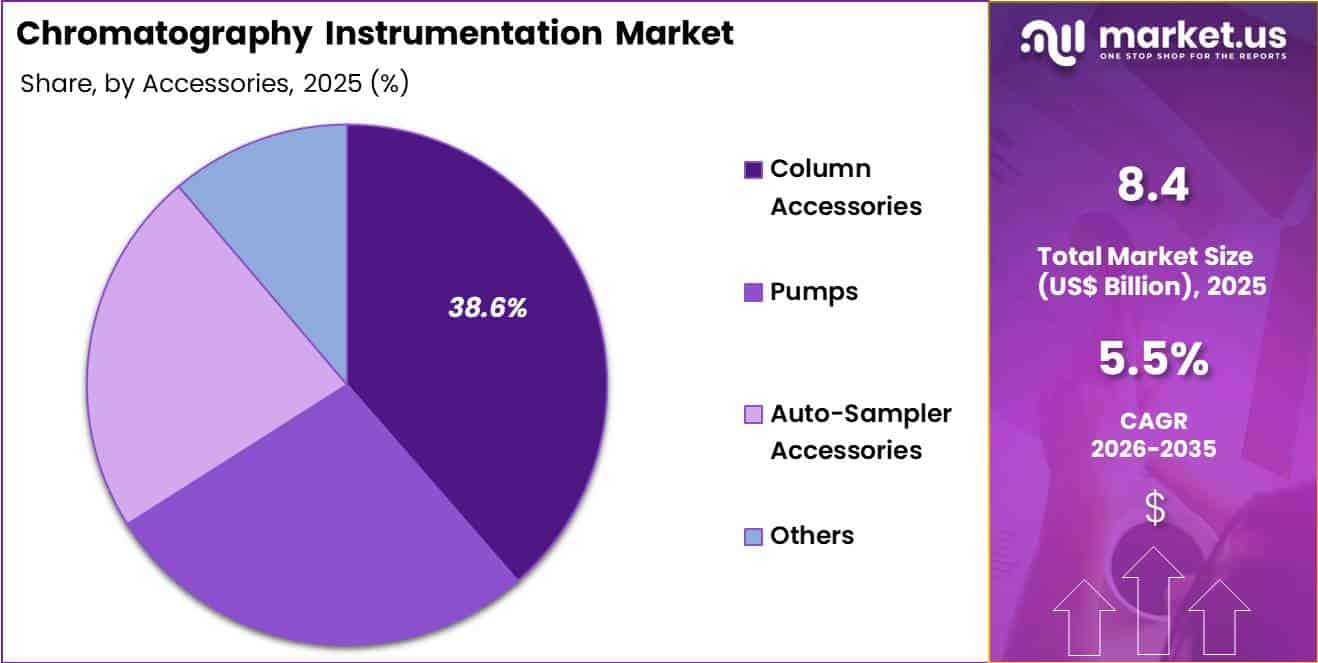

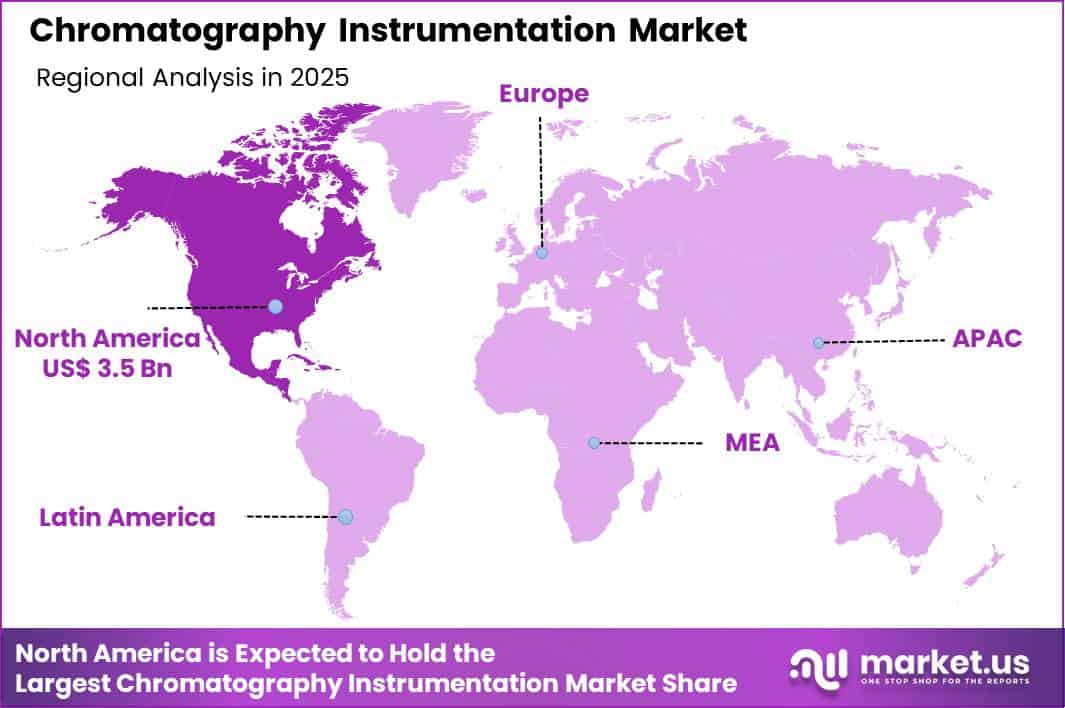

The Global Chromatography Instrumentation Market size is expected to be worth around US$ 14.3 Billion by 2035 from US$ 8.4 Billion in 2025, growing at a CAGR of 5.5% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 41.1% share with a revenue of US$ 3.5 Billion.

Growing complexity in pharmaceutical development and stringent quality requirements drive the chromatography instrumentation market as laboratories require precise separation and quantification techniques to ensure product purity and regulatory compliance.

Analytical chemists increasingly apply high-performance liquid chromatography systems to quantify active pharmaceutical ingredients and impurities in drug formulations, supporting stability studies and batch release testing. These instruments facilitate gas chromatography applications in volatile compound analysis, enabling accurate detection of residual solvents in finished pharmaceuticals and excipients.

Researchers utilize ultra-high-performance liquid chromatography coupled with mass spectrometry for metabolite identification in pharmacokinetic studies, accelerating drug candidate optimization. Chromatography systems also support biopharmaceutical characterization by separating monoclonal antibodies and biosimilars based on charge variants and glycosylation patterns. Food safety laboratories employ these tools to detect pesticide residues and contaminants in agricultural products, ensuring adherence to maximum residue limits.

Manufacturers pursue opportunities to integrate artificial intelligence and machine learning algorithms that automate method development and data interpretation, expanding applications in high-throughput screening for drug discovery and process analytical technology in continuous manufacturing.

Developers advance compact, portable chromatography systems that enable on-site testing in quality control environments, broadening utility in field-based environmental monitoring and forensic analysis. These innovations facilitate multi-dimensional chromatography techniques that achieve superior resolution for complex biological samples, supporting proteomics and metabolomics research.

Opportunities emerge in sustainable systems with reduced solvent consumption and recyclable columns, aligning with green chemistry initiatives. Companies invest in modular platforms that allow seamless upgrades, enhancing flexibility for evolving analytical needs.

Recent trends emphasize hyphenated techniques and real-time monitoring capabilities, positioning chromatography instrumentation as a cornerstone of analytical excellence in life sciences and quality assurance.

Key Takeaways

- In 2025, the market generated a revenue of US$ 8.4 Billion, with a CAGR of 5.5%, and is expected to reach US$ 14.3 Billion by the year 2035.

- The chromatography systems segment is divided into liquid chromatography, thin-layer chromatography, gas chromatography and supercritical fluid chromatography, with liquid chromatography taking the lead with a market share of 46.8%.

- Considering consumables, the market is divided into columns, solvents, syringes and others. Among these, columns held a significant share of 52.3%.

- Furthermore, concerning the accessories segment, the market is segregated into column accessories, pumps, auto-sampler accessories and others. The column accessories sector stands out as the dominant player, holding the largest revenue share of 38.6% in the market.

- The application segment is segregated into pharmaceutical firms, agriculture, clinical research organizations and environmental testing, with the pharmaceutical firms segment leading the market, holding a revenue share of 44.5%.

- North America led the market by securing a market share of 41.1%.

Chromatography Systems Analysis

Liquid chromatography contributed 46.8% of growth within chromatography systems and led the chromatography instrumentation market due to its versatility in separating complex biological and chemical mixtures.

Pharmaceutical and research laboratories rely on liquid chromatography for drug purity analysis, impurity profiling, and biomolecule characterization. Compatibility with mass spectrometry strengthens its analytical power and expands application scope. Increasing biologics development further elevates demand for high-resolution liquid separation techniques.

Growth strengthens as laboratories upgrade to high-performance and ultra-high-performance platforms to improve speed and sensitivity. Regulatory requirements for stringent quality control reinforce routine usage in drug development and manufacturing.

Expanding analytical testing across food safety and clinical diagnostics further broadens adoption. Training familiarity and method standardization support sustained demand. The segment is expected to remain dominant as liquid chromatography continues to anchor advanced analytical workflows.

Consumables Analysis

Columns generated 52.3% of growth within consumables and emerged as the leading segment due to their central role in chromatographic separation. Each analytical method requires specific column chemistry, which drives recurring replacement demand.

Pharmaceutical quality control laboratories frequently replace columns to maintain resolution and reproducibility. Expanding research pipelines increase experiment frequency, which elevates column consumption.

Growth accelerates as specialty stationary phases expand application diversity. Advances in column design enhance durability and separation efficiency. Increased outsourcing to analytical service providers further increases volume usage.

Method validation and regulatory compliance reinforce routine replacement cycles. The segment is anticipated to maintain leadership as columns remain indispensable components of chromatographic analysis.

Accessories Analysis

Column accessories accounted for 38.6% of growth within accessories and dominated the chromatography instrumentation market due to their importance in maintaining system performance. Laboratories use guard columns, fittings, and connectors to protect primary columns and ensure leak-free operation. These accessories extend equipment lifespan and improve analytical consistency. Routine maintenance schedules further strengthen steady demand.

Growth continues as laboratories emphasize uptime and workflow efficiency. Increasing automation in chromatography systems raises the need for compatible accessory components. Technical training programs encourage proactive system maintenance. High-throughput laboratories prioritize reliability, which supports accessory procurement. The segment is projected to remain dominant as operational optimization continues to guide laboratory investments.

Application Analysis

Pharmaceutical firms contributed 44.5% of growth within application and led the chromatography instrumentation market due to stringent regulatory standards and continuous drug development activity. Drug discovery, formulation development, and stability testing require extensive chromatographic analysis. Biopharmaceutical pipelines increase analytical complexity, which drives instrumentation and consumable demand. Quality assurance protocols mandate routine testing at multiple production stages.

Growth strengthens as global drug approval rates and generic manufacturing expand. Investment in research and development infrastructure increases instrument installations. Regulatory audits emphasize validated analytical methods, reinforcing routine usage. Outsourcing partnerships further elevate instrument utilization rates. The segment is expected to remain dominant as pharmaceutical firms continue to depend on chromatography for compliance and innovation.

Key Market Segments

By Chromatography Systems

- Liquid Chromatography

- Thin-Layer Chromatography

- Gas Chromatography

- Supercritical Fluid Chromatography

By Consumables

- Columns

- Solvents

- Syringes

- Others

By Accessories

- Column Accessories

- Pumps

- Auto-Sampler Accessories

- Others

By Application

- Pharmaceutical firms

- Agriculture

- Clinical research organizations

- Environmental Testing

Drivers

Increasing adoption of chromatography in pharmaceutical quality control is driving the market.

The expanding use of chromatography techniques for ensuring product purity and regulatory compliance in pharmaceutical manufacturing has substantially increased demand for advanced instrumentation. Enhanced quality assurance requirements compel companies to implement high-performance systems for routine testing and validation.

Laboratories prioritize instruments capable of separating complex mixtures with high resolution and reproducibility. The correlation between stringent drug approval standards and the need for precise analytical tools further accelerates procurement. Government regulatory bodies emphasize validated methods to safeguard public health.

Chromatography instrumentation enables detection of impurities at trace levels, supporting batch release decisions. National pharmacopeial standards require these techniques for identity and purity assessments. Key manufacturers continue to refine systems for better sensitivity and throughput. This driver fosters sustained investment in laboratory infrastructure worldwide.

According to Thermo Fisher Scientific’s 2024 annual report, the company’s Analytical Instruments segment, which includes chromatography systems, contributed to overall growth in pharmaceutical and industrial applications.

Restraints

High capital expenditure requirements are restraining the market.

The substantial initial investment needed for advanced chromatography systems, including high-performance liquid chromatography and gas chromatography instruments, limits adoption in resource-constrained laboratories. Complex engineering for pumps, detectors, and autosamplers contributes to elevated purchase prices. Smaller research facilities often delay upgrades due to budget limitations.

Regulatory validation processes for new instruments add further financial burdens. In academic institutions, funding constraints favor basic equipment over premium systems. Providers must balance analytical capabilities against economic feasibility when planning purchases. This restraint particularly affects emerging laboratories in developing regions.

Industry efforts to offer modular configurations provide partial mitigation. Despite superior performance, cost barriers slow replacement cycles and technological refreshment. Addressing affordability through financing mechanisms remains essential for broader market penetration.

Opportunities

Expansion of biopharmaceutical manufacturing capacity is creating growth opportunities.

The rapid increase in biopharmaceutical production facilities worldwide presents significant potential for chromatography instrumentation in downstream processing and quality control. Governmental incentives for biotechnology infrastructure support the establishment of new manufacturing sites requiring analytical tools.

Rising demand for monoclonal antibodies and vaccines amplifies the need for high-throughput purification systems. Strategic partnerships between biopharma companies and instrument suppliers facilitate customized solutions. The large-scale production volumes in emerging hubs magnify prospects for instrument deployment.

Training programs for bioprocess engineers promote standardized use of chromatography in quality assurance. This opportunity enables manufacturers to diversify beyond traditional research applications. Key corporations are establishing dedicated service networks to support expanded capacity.

Overall, biopharmaceutical growth aligns with efforts to accelerate therapeutic development. Focused initiatives in this segment can secure substantial market positions.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the chromatography instrumentation market through research funding, pharma capital expenditure, and quality control investments across industries. Inflation and higher interest rates increase the cost of financing analytical equipment, which slows procurement decisions in academic labs and smaller manufacturers.

Geopolitical tensions disrupt supplies of precision pumps, detectors, columns, and electronic components, creating sourcing risk and extended lead times. Current US tariffs on imported instruments, spare parts, and specialized materials raise acquisition and maintenance costs, which compresses margins and intensify pricing negotiations. These pressures affect contract labs and emerging biotech firms with tighter budgets.

On the positive side, trade exposure encourages regional manufacturing, diversified component sourcing, and stronger service infrastructure. Ongoing regulatory requirements in pharmaceuticals, food safety, and environmental testing sustain consistent demand for reliable analytical systems. With operational discipline, technology upgrades, and service led value, the market remains positioned for steady and confident growth.

Latest Trends

Integration of artificial intelligence for method optimization is a recent trend in the market.

In 2024, the incorporation of artificial intelligence algorithms in chromatography software has advanced automated method development and optimization. These systems analyze experimental data to predict optimal separation conditions with reduced trial-and-error. Manufacturers have prioritized machine learning models trained on extensive chromatographic datasets.

Clinical and industrial laboratories benefit from faster development of robust methods. Agilent Technologies introduced AI-driven capabilities in its OpenLab software suite in 2024 for predictive method optimization. This innovation reduces development time while maintaining regulatory compliance.

The trend emphasizes user-friendly interfaces for non-expert operators. Regulatory evaluations in 2024 confirmed suitability for validated workflows. Industry collaborations refine algorithms for complex sample matrices. These advancements aim to enhance efficiency and reproducibility in analytical laboratories.

Regional Analysis

North America is leading the Chromatography Instrumentation Market

North America captured a 41.1% share of the Chromatography Instrumentation market in 2024, reflecting sustained investment in pharmaceutical R&D, bioprocessing, and analytical testing. Drug developers expanded high-performance liquid and gas chromatography workflows to support complex biologics, biosimilars, and small molecule pipelines.

Regulatory expectations for impurity profiling and quality control strengthened demand across commercial manufacturing sites. Academic laboratories and contract research organizations increased use of advanced separation systems for proteomics and metabolomics studies. Environmental and food safety agencies also relied on precise analytical platforms to monitor contaminants.

Automation and software integration improved throughput and data integrity across laboratories. A strong supporting indicator comes from the US Food and Drug Administration, which reported 55 novel drug approvals through its CDER program in 2023, underscoring robust pharmaceutical development activity that directly drives demand for advanced separation and analytical systems.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Chromatography Instrumentation market in Asia Pacific is expected to grow steadily during the forecast period as regional pharmaceutical production and quality standards continue to advance. Governments strengthen regulatory oversight for drug safety and environmental monitoring, encouraging laboratories to upgrade analytical capabilities.

Expanding generic and biosimilar manufacturing in countries such as India, China, and South Korea increases reliance on validated separation techniques. Universities and research institutes broaden life sciences and chemical research programs, boosting equipment adoption. Food and beverage testing laboratories also enhance contaminant detection frameworks to meet export requirements.

Local distributors improve technical support and service networks, which accelerates purchasing decisions. A verifiable indicator appears in 2023 data from India’s Ministry of Chemicals and Fertilizers, which highlighted the country’s position as one of the largest suppliers of generic medicines globally, reinforcing sustained analytical testing needs that support regional market expansion.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the chromatography instrumentation market grow by advancing system performance, expanding detector sensitivity, and integrating automation that help laboratories accelerate complex separations and improve data quality across pharmaceutical, environmental, and food testing applications.

They also strengthen customer value by bundling intuitive software, remote diagnostics, and service contracts that reduce downtime and support consistent results in high-throughput environments. Firms pursue strategic partnerships with reagent and column specialists to offer complete, validated workflows that shorten method development and attract repeat business.

Geographic expansion into North America, Europe, and fast-growing Asia Pacific diversifies revenue streams while capturing rising investment in analytical infrastructure and regulatory compliance initiatives. Agilent Technologies exemplifies a global leader with a comprehensive portfolio of chromatography systems, detectors, and informatics backed by extensive technical support and strong global sales operations.

The company advances its competitive agenda through disciplined R&D investment, targeted acquisitions that broaden capabilities, and a customer-centric commercialization strategy that aligns innovation with evolving laboratory requirements.

Top Key Players

- Agilent Technologies

- Shimadzu Corporation

- Thermo Fisher Scientific

- Waters Corporation

- PerkinElmer

- Metrohm

- Hitachi High‑Tech

- JASCO

- Bio‑Rad Laboratories

- Knauer Wissenschaftliche Geräte

Recent Developments

- In October 2024, Agilent Technologies Inc. introduced the latest generation of its InfinityLab LC Series systems, advancing its liquid chromatography portfolio. The upgraded platforms are designed to simplify laboratory workflows through enhanced automation, improved system connectivity, real-time predictive diagnostics, and built-in safeguards that help minimize operational errors.

- In February 2024, Thermo Fisher Scientific Inc. launched the Thermo Scientific Dionex Inuvion Ion Chromatography system to broaden analytical flexibility within a single IC platform. The system is engineered to streamline ion analysis across laboratories of varying sizes, offering expanded application capability while improving usability and workflow clarity.

Report Scope

Report Features Description Market Value (2025) US$ 8.4 Billion Forecast Revenue (2035) US$ 14.3 Billion CAGR (2026-2035) 5.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Chromatography Systems (Liquid Chromatography, Thin-Layer Chromatography, Gas Chromatography and Supercritical Fluid Chromatography), By Consumables (Columns, Solvents, Syringes and Others), By Accessories (Column Accessories, Pumps, Auto-Sampler Accessories and Others), By Application (Pharmaceutical firms, Agriculture, Clinical research organizations and Environmental Testing) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Agilent Technologies, Shimadzu Corporation, Thermo Fisher Scientific, Waters Corporation, PerkinElmer, Metrohm, Hitachi High-Tech, JASCO, Bio-Rad Laboratories, Knauer Wissenschaftliche Geräte Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Chromatography Instrumentation MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Chromatography Instrumentation MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Agilent Technologies

- Shimadzu Corporation

- Thermo Fisher Scientific

- Waters Corporation

- PerkinElmer

- Metrohm

- Hitachi High‑Tech

- JASCO

- Bio‑Rad Laboratories

- Knauer Wissenschaftliche Geräte

Our Clients

- 178480

- Feb 2026