Quick Navigation

Report Overview

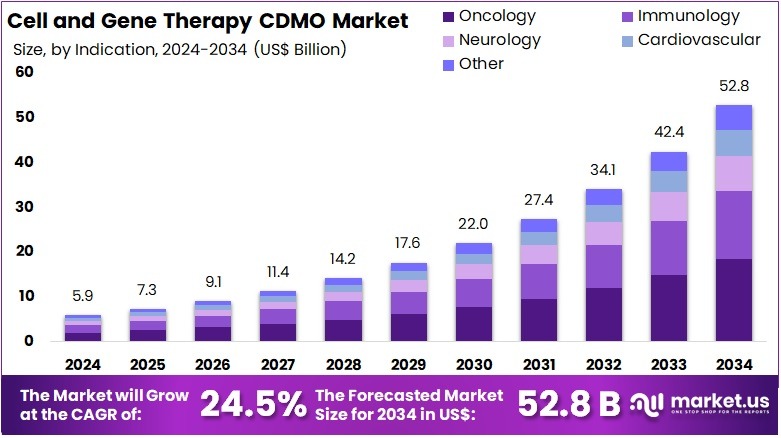

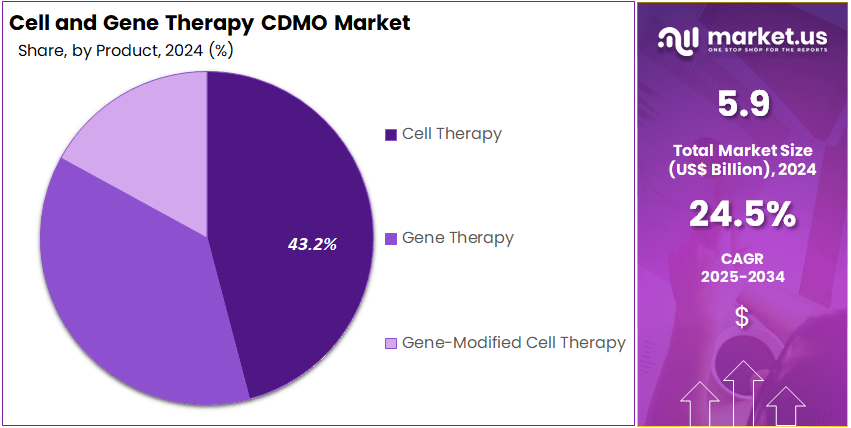

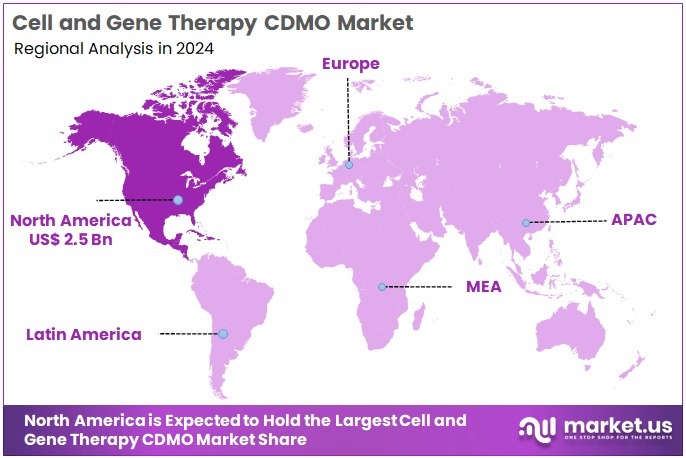

The Global Cell and Gene Therapy CDMO Market Size is expected to be worth around US$ 52.8 Billion by 2034, from US$ 5.9 Billion in 2024, growing at a CAGR of 24.5% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 43.2% share and holds US$ 2.5 Billion market value for the year.

The Cell and Gene Therapy Contract Development and Manufacturing Organization (CDMO) sector has witnessed remarkable expansion in recent years. This growth can be attributed to a sharp increase in clinical trials and product approvals. According to the World Health Organization’s International Clinical Trials Registry Platform (ICTRP), a consistent year-on-year rise in registered cell and gene therapy trials has been observed globally. For instance, in the United States, the Food and Drug Administration (FDA) approved 19 gene therapy products as of June 2024. This marks a substantial increase from just one approval in 2017, highlighting a robust and advancing pipeline.

Advancements in manufacturing technologies have played a pivotal role in accelerating the CDMO sector’s growth. The World Health Organization has stressed the importance of adhering to good manufacturing practices (GMP) for biological products, including cell and gene therapies. The adoption of automated and scalable manufacturing processes has enabled CDMOs to meet rising global demand. According to industry studies, such technologies have enhanced production efficiency and lowered manufacturing costs, making cell and gene therapies more accessible to patients worldwide.

Regulatory support has further driven the expansion of the CDMO sector. For example, the FDA’s introduction of the Regenerative Medicine Advanced Therapy (RMAT) designation in 2017 provides an expedited review process for innovative cell and gene therapies. As of March 2025, multiple therapies have received RMAT designation, underlining the regulatory commitment to fostering advanced treatment development. Additionally, the European Medicines Agency (EMA) has implemented guidelines specifically for advanced therapy medicinal products (ATMPs), streamlining approval processes and ensuring high safety and efficacy standards across Europe.

A significant focus within the cell and gene therapy sector remains on rare diseases. According to the World Health Organization, approximately 300 million people globally are affected by rare diseases. The development of gene therapies for these conditions has led to significant advancements in treatment options. For example, the FDA has approved therapies such as Zolgensma for spinal muscular atrophy and Elevidys for Duchenne muscular dystrophy, providing new hope for affected patients and stimulating specialized manufacturing capabilities within the CDMO sector.

The cell and gene therapy CDMO sector continues to grow due to increasing clinical activity, technological advancements, regulatory support, and a dedicated focus on rare diseases. This positive trend is expected to drive further investment and innovation in the sector, improving patient access to novel therapies.

Key Takeaways

- The global Cell and Gene Therapy CDMO market is forecast to grow from US$ 5.9 Billion in 2024 to US$ 52.8 Billion by 2034.

- This expansion reflects a strong CAGR of 24.5% between 2025 and 2034, driven by rising demand for advanced therapeutic development.

- In 2024, Cell Therapy emerged as the leading product category, accounting for over 45.8% of the total CDMO market share.

- Oncology was the top application segment in 2024, representing more than 45.8% of the Cell and Gene Therapy CDMO market demand.

- North America led the regional landscape in 2024, securing over 43.2% market share and generating US$ 2.5 Billion in revenue.

Product Analysis

In 2024, the Cell Therapy section held a dominant market position in the Product Segment of the Cell and Gene Therapy CDMO Market, and captured more than a 45.8% share. This leadership was driven by the growing number of cell therapy programs in clinical development. Demand increased for autologous and allogeneic treatments, particularly in oncology and rare diseases. CDMOs with GMP-grade cell processing capabilities gained traction. Their ability to support expansion, cryopreservation, and regulatory compliance made them essential to therapy developers.

Gene Therapy emerged as the second-largest product segment in 2024. It showed strong performance due to the rise in clinical trials for genetic and neuromuscular disorders. The production of viral vectors, such as AAV and lentivirus, remained a technical challenge for many firms. As a result, many sponsors turned to CDMOs for manufacturing support. The growing need for scalable and compliant vector production pushed the demand for specialized contract services.

Gene-Modified Cell Therapy displayed the fastest growth rate within the market. Its rise was mainly linked to the success of CAR-T cell therapies in treating blood cancers. Developers sought partners who could offer integrated services, from gene editing to final fill-finish. Increasing investments and favorable regulatory pathways also contributed to segment growth. CDMOs with experience in complex workflows gained preference, reinforcing the shift toward outsourcing in advanced therapy manufacturing.

Application Indication Analysis

In 2024, the Oncology Section held a dominant market position in the Application Indication Segment of Cell and Gene Therapy CDMO Market, and captured more than a 45.8% share. This dominance was largely due to the growing demand for cancer-targeted therapies such as CAR-T cells. An increase in approvals for cell and gene therapies in oncology further supported this growth. Manufacturing partnerships also rose, driven by the need for scalable production of tumor-targeting treatments across global markets.

Immunology emerged as the second-leading application in the same year. This growth was driven by advancements in immune cell therapy for treating autoimmune and rare immunodeficiency disorders. The segment also benefited from innovations in gene delivery technologies. Regulatory incentives for orphan and rare diseases encouraged development in this space. Several clinical-stage therapies moved forward, increasing outsourcing demand from CDMOs for both viral vector manufacturing and cell processing services.

Neurology and Cardiovascular applications showed steady growth but held smaller shares. Neurological disorders such as ALS and Parkinson’s attracted attention, especially for gene-based interventions. Cardiovascular therapies were still in early-stage trials and had limited commercial use. The Other Diseases category included rare metabolic and inherited conditions. Though this group had a lower market share in 2024, it showed long-term promise due to growing investments and ongoing advancements in precision gene-editing platforms.

Key Market Segments

By Product

- Cell Therapy

- Gene Therapy

- Gene-Modified Cell Therapy

By Application Indication

- Oncology

- Immunology

- Neurology

- Cardiovascular

- Other Diseases

Drivers

Rising Clinical Trial Volume Fuels Demand for Specialized CDMO Services

The surge in clinical trials for cell and gene therapies is driving the need for advanced CDMO services. As more therapies enter early-phase development, biopharmaceutical firms are under pressure to accelerate timelines and meet regulatory requirements. Outsourcing to CDMOs allows companies to access established infrastructure and technical know-how without incurring the cost of in-house capabilities. This is especially critical for complex therapies involving viral vectors, cell lines, and gene editing tools, where CDMOs offer essential support from development through clinical production.

CDMOs are increasingly becoming strategic partners rather than just service providers. Their involvement begins in preclinical stages and extends through late-stage clinical manufacturing. As the clinical pipeline for advanced therapies expands, CDMOs are scaling their operations to meet rising demand. Investments in high-containment facilities, modular cleanrooms, and GMP-compliant environments are being made to cater to the unique production requirements of cell and gene therapies. This trend is a key growth engine for the CDMO market in regenerative medicine and genetic therapeutics.

Moreover, regulatory bodies such as the FDA and EMA have streamlined processes to fast-track approvals for promising cell and gene therapies. This has encouraged more clinical trial initiations, prompting companies to seek CDMOs that ensure compliance and speed. The high cost and complexity of manufacturing cell and gene therapies also make outsourcing a cost-effective strategy. As a result, the growing volume of clinical research activities is directly translating into increased CDMO engagement, bolstering the sector’s overall growth trajectory.

Restraints

Investor Hesitancy Driven by High Costs and Safety Concerns

One of the key restraints facing the Cell and Gene Therapy CDMO market is investor hesitancy linked to high treatment costs and safety challenges. While these therapies offer transformative benefits, they remain prohibitively expensive for many healthcare systems and patients. As a result, financial stakeholders are cautious about committing large capital. The complex manufacturing requirements and regulatory uncertainties further amplify risk perception. These factors have led to reduced confidence in the commercial viability of such therapies, especially during early development phases.

In 2024, investment in gene therapy development experienced a sharp decline. The total funding raised was under $1.4 billion, a steep drop from the $8.2 billion raised in 2021. This drastic reduction reflects the growing caution among investors amid economic pressures and concerns over clinical outcomes. This funding shortfall could slow down clinical trial progression, limit scalability, and delay partnerships with CDMO providers. Consequently, CDMOs may struggle to expand capabilities or adopt advanced platforms without sufficient backing.

The reduced investor interest has the potential to impact innovation and infrastructure growth within the Cell and Gene Therapy CDMO sector. Limited capital inflow restricts the ability of CDMOs to invest in new technologies or expand production capacity. Furthermore, smaller biotechs that rely heavily on external funding may delay or cancel their development programs. This creates a ripple effect throughout the supply chain, ultimately affecting the availability and affordability of cell and gene therapies in the long term.

Opportunities

AI-Driven Process Optimization in Cell and Gene Therapy CDMO

The integration of Artificial Intelligence (AI) into manufacturing processes offers a transformative opportunity for Cell and Gene Therapy CDMOs. AI technologies are being adopted to optimize critical steps in bioprocessing. These include media formulation, cell culture monitoring, and batch yield prediction. By automating complex tasks, CDMOs can reduce manual interventions and ensure better consistency across production runs. This shift not only minimizes human error but also enhances the reliability of outcomes, making manufacturing processes more robust and reproducible.

AI also plays a pivotal role in improving quality control within cell and gene therapy manufacturing. Advanced algorithms can detect deviations, track anomalies, and predict potential product failures before they occur. Real-time monitoring tools powered by AI can ensure that each step in the production process adheres to regulatory standards. This is especially valuable in a highly regulated environment where precision is essential. As a result, CDMOs can achieve higher compliance and reduce the risk of costly batch failures or product recalls.

Furthermore, AI significantly contributes to reducing production timelines by streamlining workflows and enabling predictive maintenance of manufacturing equipment. Faster cycle times can accelerate the delivery of therapies to patients. CDMOs that adopt AI-driven manufacturing models will gain a competitive edge through enhanced scalability and faster time-to-market. As the demand for personalized and complex therapies increases, AI-powered solutions will be essential in addressing the growing need for efficient and high-throughput production systems in the cell and gene therapy sector.

Trends

Increasing Consolidation Among Cell and Gene Therapy CDMO Providers

The Cell and Gene Therapy CDMO market is currently experiencing a significant wave of consolidation. Larger contract development and manufacturing organizations (CDMOs) are actively acquiring smaller or niche firms. This trend is driven by the need to broaden technical capabilities and access specialized technologies, particularly in areas like viral vector production and advanced cell processing. Through such acquisitions, CDMOs aim to offer comprehensive, end-to-end solutions that support clients from early-stage development through to commercial-scale manufacturing.

Consolidation is also being pursued to increase geographic reach and improve global service delivery. By expanding operations into new regions, larger CDMOs can address growing demand from international biopharmaceutical firms. This expansion enables quicker turnaround times, localized regulatory compliance, and better logistical support for clinical and commercial supply chains. As the cell and gene therapy pipeline continues to grow, proximity to clients and trial sites becomes increasingly important for operational efficiency.

Furthermore, streamlined operations and integrated service models are becoming critical for competitiveness. Merged entities can achieve cost efficiencies, reduce redundancies, and enhance overall service quality. These benefits are vital in a sector where speed, precision, and scalability are essential. The ongoing consolidation indicates a maturing CDMO landscape, characterized by fewer but more capable providers serving the evolving needs of cell and gene therapy developers.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 43.2% share and holds US$ 2.5 Billion market value for the year. This leadership is largely due to its strong biopharmaceutical ecosystem. The region hosts a wide network of advanced manufacturing facilities and skilled professionals. It also benefits from structured regulatory pathways for complex therapies. These combined factors have made North America a preferred region for contract manufacturing in the cell and gene therapy sector.

The United States is the key contributor to regional growth. Supportive regulatory policies by the FDA help in faster approvals and clinical trials. High government funding for rare diseases and advanced therapeutics also plays a major role. Many biotech firms in the country rely on CDMOs for efficient scale-up and commercial production. This outsourcing trend has increased rapidly in recent years, especially for therapies requiring strict compliance and technical expertise.

Academic institutions and research hospitals in North America are actively partnering with CDMOs. These collaborations help accelerate early-stage development and GMP-compliant production. The presence of innovation hubs and technology incubators further strengthens the ecosystem. As a result, several CDMOs have expanded capacity or upgraded facilities to support next-generation therapies. These changes reflect strong regional momentum in cell and gene therapy development.

Canada is also contributing to the region’s growth. The country supports life sciences through tax credits, funding programs, and research grants. New biotech start-ups are emerging, supported by local incubators and public investments. CDMOs in Canada are increasingly attracting contracts from both domestic and international developers. This has helped diversify North America’s overall CDMO landscape, reinforcing its dominant position in this growing market segment.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Cell and Gene Therapy CDMO market is growing due to the active involvement of leading players offering end-to-end manufacturing services. Charles River Laboratories has expanded its services through the acquisition of Cognate BioServices, strengthening its viral vector and safety testing capabilities. Curia, formerly AMRI, is focusing on modular manufacturing and scale-up capacity. It is investing in gene therapy facilities across North America and Europe. These companies provide integrated platforms for preclinical to commercial-scale production, helping biopharmaceutical developers bring advanced therapies to market efficiently.

Emergent BioSolutions plays a key role in supporting gene therapy manufacturing through its expertise in biologics and biodefense. The company’s Baltimore facility is significant for viral vector production and GMP-compliant fill-finish operations. Eurofins Scientific contributes with advanced bioanalytical testing and regulatory support services. Its global presence allows clients to access cross-border capabilities for gene-modified cell therapy development. These players enable therapy developers to maintain compliance and quality while accelerating their clinical timelines and regional access.

FUJIFILM Diosynth Biotechnologies is expanding its global footprint by investing in large-scale viral vector production and high-throughput cleanrooms. Its sites in the U.S. and U.K. support clinical to commercial needs. Other major players such as Thermo Fisher Scientific, Lonza, Catalent, and Samsung Biologics are also advancing the sector. They are expanding capacity and forming partnerships with biotech firms to accelerate innovation. Their integrated service models and global facilities help scale gene and cell therapies efficiently across diverse markets.

Market Key Players

- Charles River Lobaoraties

- Curia

- Emergent BioSolutions

- Eurofins

- FUJIFILM Diosynth Biotechnologies

- Genscript

- Lonza

- Pfizer CentreOne

- Recipharm

- Syngene

- Thermo Fisher Scientific

- Wacker

Recent Developments

- In December 2024: Charles River announced the initiation of its Advanced Therapy Incubator Program, designed to accelerate the development of innovative therapies. This program aims to provide emerging biotech companies with access to Charles River’s comprehensive CDMO services, including process development, manufacturing, and analytical support. By fostering collaboration and providing resources, the incubator program seeks to expedite the transition of advanced therapies from the laboratory to clinical application.

- In March 2024: Emergent BioSolutions made a strategic financial investment in Swiss Rockets Ltd., the parent company of Rocketvax Ltd., to support research and infrastructure development. This investment aims to bolster Emergent’s capabilities in the cell and gene therapy sector, aligning with its focus on addressing public health threats through innovative solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 5.9 Billion |

| Forecast Revenue (2034) | US$ 52.8 Billion |

| CAGR (2025-2034) | 24.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Cell Therapy, Gene Therapy, Gene-Modified Cell Therapy), By Application Indication (Oncology , Immunology, Neurology, Cardiovascular, Other Diseases) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Charles River Lobaoraties, Curia, Emergent BioSolutions, Eurofins, FUJIFILM Diosynth Biotechnologies, Genscript, Lonza, Pfizer CentreOne, Recipharm, Syngene, Thermo Fisher Scientific, Wacker |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |