Global Cathodic Protection Market Size, Share, Growth Analysis By Solution (Products (Transformer Rectifiers, Junction Boxes, Anodes, Reference Electrodes, Cables & Accessories, Others), Services (Inspection, Design and Construction, Support & Maintenance)), By Protection Method (Impressed Current, Galvanic Anode), By End-Use Industry (Oil & Gas, Marine & Shipbuilding, Water & Wastewater Treatment, Power Generation, Infrastructure & Construction, Chemical & Petrochemical, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181446

- Number of Pages: 355

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

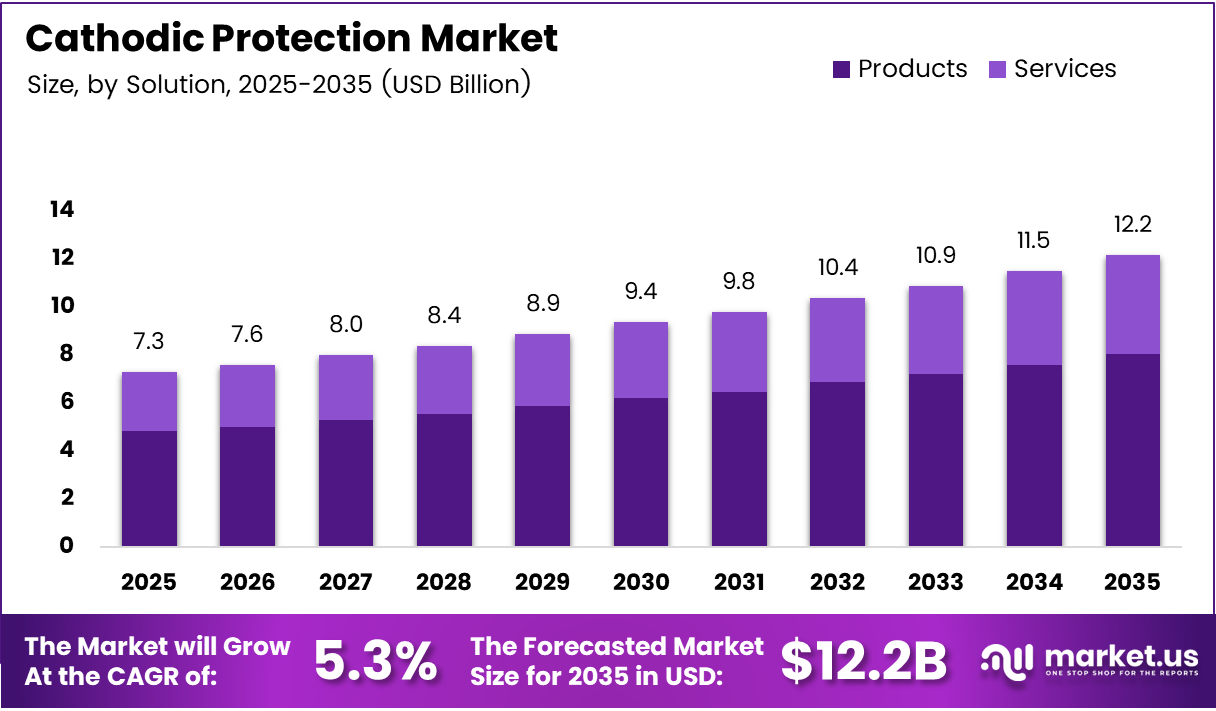

Global Cathodic Protection Market size is expected to be worth around USD 12.2 Billion by 2035 from USD 7.3 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

Cathodic protection (CP) is an electrochemical technique that prevents metal corrosion by making the protected structure the cathode of an electrochemical cell. It serves as a critical defense mechanism for buried pipelines, offshore platforms, marine vessels, and water treatment infrastructure. Without it, corrosion-related failures cost industries billions annually in unplanned downtime and asset replacement.

The market divides into two core solution types: hardware products and professional services. Products — including transformer rectifiers, anodes, junction boxes, and reference electrodes — account for the dominant revenue stream. Services covering inspection, design and construction, and ongoing maintenance form the operational backbone that extends system life and ensures regulatory compliance.

Oil and gas pipeline networks represent the single largest end-use segment, holding a 30.4% share of total market demand. This concentration reflects decades of regulatory mandates around pipeline integrity, particularly in North America and the Middle East, where aging infrastructure and high-value assets create a structural need for reliable corrosion control across thousands of kilometers of buried and submerged assets.

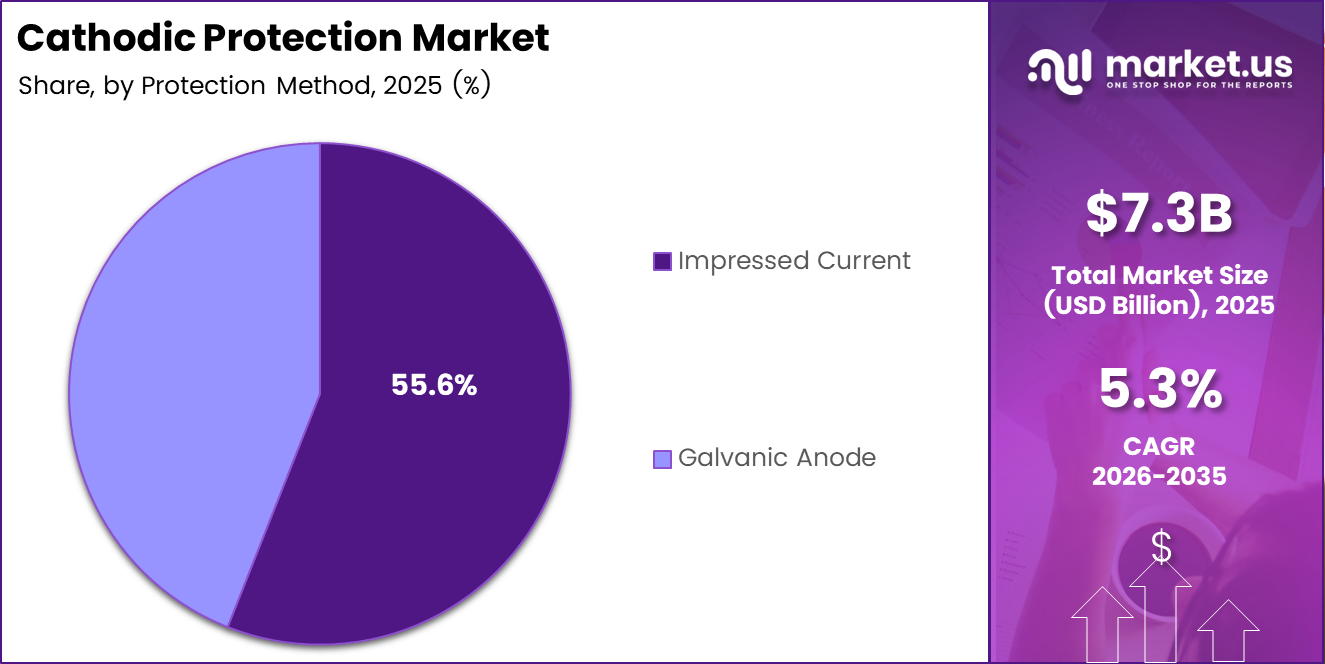

Impressed current cathodic protection (ICCP) commands 55.6% of the protection method segment, a dominance that signals enterprise preference for controllable, long-range protection in large-scale infrastructure applications. ICCP systems allow operators to adjust output current based on changing soil conditions and asset exposure — a flexibility that passive galvanic systems cannot match at scale.

In October 2025, GPT Industries LLC acquired Integrated Rectifier Technologies Inc. (IRT), an Alberta-based transformer rectifier manufacturer, to integrate its production with GPT’s Iso-Smart™ remote monitoring platform. This consolidation reflects a broader market shift toward connected CP hardware — where rectifiers are no longer standalone components but data nodes in a digital asset management ecosystem.

According to the U.S. Department of Defense Unified Facilities Manual (updated 13 March 2026), mixed metal oxide (MMO) anodes carry a typical design life of 30–50 years, with consumption rates ranging from 0.5 mg/amp-year in seawater to 5 mg/amp-year in coke breeze. This operational longevity means anode replacement cycles are infrequent — shifting the real commercial opportunity toward monitoring services and system optimization rather than recurring hardware sales.

According to Corrosion Science and Technology (Vol. 24, No. 6, 2025), ICCP system current decreases from an initial ~90 mA to stabilized values of less than 10 mA after operation. This 90%+ current reduction after stabilization reveals that oversized initial system specifications are common — pointing to a market gap for precision design services that reduce commissioning waste and lower long-term operating costs for asset owners.

Key Takeaways

- The global cathodic protection market is valued at USD 7.3 Billion in 2025 and is forecast to reach USD 12.2 Billion by 2035, at a CAGR of 5.3%.

- Products segment holds a dominant share of 65.5%, led by transformer rectifiers, anodes, and cables and accessories.

- Impressed Current Cathodic Protection (ICCP) leads the protection method segment with a 55.5% share.

- Oil and Gas is the largest end-use industry, accounting for 30.4% of total market demand.

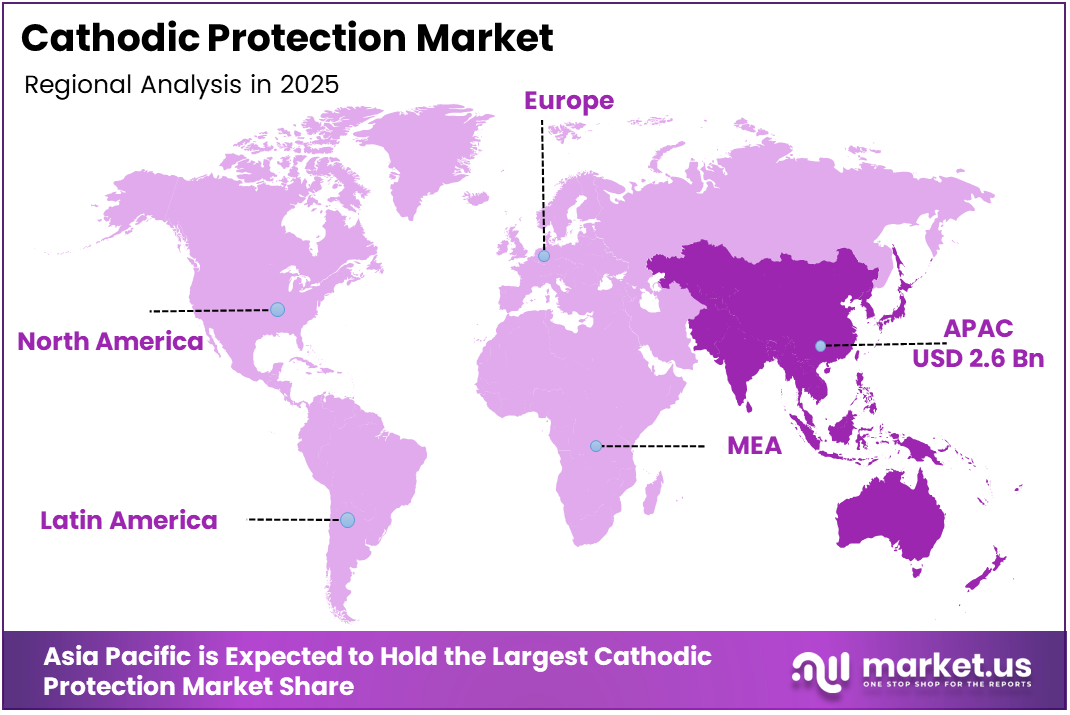

- Asia Pacific leads all regions with a 36.3% market share, valued at USD 2.6 Billion.

- Marine and shipbuilding, water and wastewater treatment, and power generation represent key secondary demand segments.

- Services — including inspection, design, and maintenance — form a critical recurring revenue stream alongside hardware products.

Product Analysis

Products dominates with 65.5% due to essential hardware demand across pipeline and marine assets.

In 2025, Products held a dominant market position in the By Solution segment of the Cathodic Protection Market, with a 65.5% share. Hardware components — including anodes, rectifiers, and reference electrodes — form the physical foundation of every CP installation. Without this equipment, no cathodic protection system can operate. This dependency locks in hardware procurement at every new build and major asset rehabilitation project.

Transformer Rectifiers serve as the power supply core of impressed current cathodic protection systems. They convert AC grid power into controlled DC output to drive protective current through the structure. Their integration with remote monitoring platforms — as seen in GPT Industries’ October 2025 acquisition of IRT — reflects operator demand for rectifiers that are both measurable and remotely adjustable.

Junction Boxes function as the electrical distribution and monitoring interface between the CP power source and protected structure. They house test points that allow field engineers to measure pipe-to-soil potential and verify system performance, making them a non-negotiable component in compliance-driven inspection protocols.

Anodes carry the highest consumable replacement rate within the product category, particularly galvanic anodes in marine and offshore applications. According to the U.S. Department of Defense Unified Facilities Manual (March 2026), MMO anodes in seawater carry consumption rates as low as 0.5 mg/amp-year, directing procurement strategy toward material selection over volume replacement.

Reference Electrodes provide the measurement benchmark against which all CP performance is evaluated. They allow operators to verify that pipe-to-soil potentials meet the minimum −850 mV CSE criterion for steel protection. Their precision directly determines whether an asset is adequately protected or at risk — making electrode calibration a recurring service requirement.

Cables and Accessories complete the electrical circuit between CP components. While individually low in unit value, they represent significant total volume across large pipeline networks spanning hundreds of kilometers. Failures in cabling are among the most common causes of CP system underperformance, reinforcing demand for quality-grade accessories even in cost-sensitive procurement environments.

Services represent the recurring revenue layer of the cathodic protection market. While products generate upfront project revenue, services — covering inspection, design and construction, and ongoing maintenance — generate income across the full asset lifecycle. As infrastructure ages and compliance requirements tighten, service contracts offer more predictable and defensible margins than hardware sales alone.

Inspection services validate whether an installed CP system delivers adequate protection to all sections of a structure. Regular survey work — including close interval potential surveys and AC interference assessments — is mandated under most pipeline safety regulations. In August 2025, Irth Solutions launched Phase 2 of its External Corrosion Module, adding full CP survey data management and automated compliance reporting to its pipeline integrity platform.

Design and Construction services set the engineering parameters that determine the long-term effectiveness of a CP installation. Poor initial design leads to chronic underprotection or overprotection — both of which carry financial and safety penalties. According to Frontiers in Chemical Engineering (December 2025), optimizing deep-well anode placement reduced underprotected pipeline length from 150 m to just 21 m, illustrating the measurable value of precise system engineering.

Support and Maintenance services sustain CP system performance between formal inspection cycles. They address electrode drift, anode depletion, rectifier faults, and cabling deterioration before these conditions escalate to asset damage. As operating companies face tighter budgets and leaner field teams, outsourced maintenance contracts are replacing in-house CP management — creating a steady revenue pipeline for specialist service providers.

Protection Method Analysis

Impressed Current dominates with 55.6% due to controllable output for large-scale infrastructure.

In 2025, Impressed Current Cathodic Protection (ICCP) held a dominant market position in the By Protection Method segment of the Cathodic Protection Market, with a 55.6% share. ICCP systems use an external power source to deliver adjustable current output — making them the preferred choice for long-distance pipelines, large storage tanks, and offshore platforms where passive protection cannot cover the required surface area.

Galvanic Anode cathodic protection operates without an external power supply, using the electrochemical potential difference between the anode material and the protected structure. This passive approach suits smaller or remotely located assets — such as buried distribution mains, harbor structures, and boat hulls — where powering an impressed current system is impractical or cost-prohibitive.

End-Use Industry Analysis

Oil and Gas dominates with 30.4% due to mandatory pipeline integrity regulations and aging asset base.

In 2025, Oil and Gas held a dominant market position in the By End-Use Industry segment of the Cathodic Protection Market, with a 30.4% share. Decades of regulatory mandates on pipeline safety — particularly in North America and the Middle East — have made CP systems standard practice across upstream, midstream, and downstream infrastructure. The sheer volume of buried and submerged pipelines in this sector creates a structural and recurring demand that no other end-use category currently matches.

Marine and Shipbuilding represents the second most CP-intensive sector, driven by constant exposure of vessel hulls and offshore structures to corrosive seawater environments. Ship owners and port operators rely on both galvanic and impressed current systems to protect hulls, propeller shafts, and offshore jacket structures. Regulatory classification standards from bodies like DNV and Lloyd’s reinforce mandatory CP requirements across the fleet lifecycle.

Water and Wastewater Treatment infrastructure relies on CP to protect buried mains, treatment plant structures, and submerged equipment from soil and water-induced corrosion. Municipal utilities operating aging distribution networks face increasing pressure from regulators to demonstrate asset integrity — a requirement that is accelerating CP adoption as a cost-effective alternative to premature pipe replacement.

Power Generation facilities — including thermal, nuclear, and renewable energy plants — use CP to protect underground piping, cooling water systems, and structural foundations. The long design life of power infrastructure makes corrosion prevention a lifecycle cost issue rather than a routine maintenance decision. Each avoidable corrosion failure carries both production and safety consequences that justify upfront CP investment.

Infrastructure and Construction encompasses reinforced concrete structures such as bridges, tunnels, parking structures, and marine wharves. Rebar corrosion is the leading cause of structural deterioration in reinforced concrete — and cathodic protection for concrete (both galvanic and ICCP) addresses this directly. The scale of aging civil infrastructure globally makes this one of the fastest-expanding application areas for CP technology.

Chemical and Petrochemical facilities operate complex networks of process pipelines, storage tanks, and heat exchangers that face both internal and external corrosion threats. CP systems protect the external surfaces of buried and submerged assets in these environments. The high consequence of a corrosion failure in a chemical plant — in terms of both safety and environmental liability — creates a strong business case for comprehensive CP coverage.

Key Market Segments

By Solution

- Products

- Transformer Rectifiers

- Junction Boxes

- Anodes

- Reference Electrodes

- Cables & Accessories

- Others

- Services

- Inspection

- Design and Construction

- Support & Maintenance

By Protection Method

- Impressed Current

- Galvanic Anode

By End-Use Industry

- Oil & Gas

- Marine & Shipbuilding

- Water & Wastewater Treatment

- Power Generation

- Infrastructure & Construction

- Chemical & Petrochemical

- Others

Drivers

Pipeline Safety Mandates and Oil and Gas Investment Create Structural CP Demand Across Critical Infrastructure

Global oil and gas operators face non-negotiable pipeline safety regulations that mandate cathodic protection as a baseline requirement for asset integrity. According to the U.S. Department of Defense Unified Facilities Manual (updated 13 March 2026), steel and cast iron piping must maintain a cathodic potential of at least −850 mV relative to a CSE reference electrode. This binding technical criterion converts CP from an optional improvement into a compliance obligation across thousands of kilometers of infrastructure.

The oil and gas sector holds a 30.4% share of total CP market demand — and active investment in new pipeline corridors across the Middle East, North America, and Southeast Asia sustains procurement volumes well beyond what replacement cycles alone would generate. In January 2025, MATCOR relaunched its Iron Gopher® linear anode system with a price reduction and full in-house production, directly targeting horizontal directional drilling projects where conventional anode placement is impractical. This type of product innovation responds to real procurement constraints in pipeline construction environments.

Marine and shipbuilding applications reinforce this driver from a different angle. Offshore platforms, subsea pipelines, and vessel hulls face aggressive seawater corrosion that, without active CP management, degrades structural integrity within years. Classification societies mandate CP coverage as a condition of certification — meaning every new offshore asset and every vessel renewal cycle adds to the hardware and service demand baseline. The combination of regulatory pull and ongoing capital investment in offshore energy makes this market structurally resistant to demand contraction.

Restraints

High Capital Requirements and Technical Skill Gaps Limit ICCP Adoption Among Smaller Asset Operators

Impressed current cathodic protection systems require significant upfront expenditure on rectifiers, deep-well anode installations, cabling infrastructure, and reference electrode networks. According to ADE Letters (2025), even a solar-powered ICCP system for a 5 km pipeline carries an initial investment of $15,610 to $18,122 depending on battery technology — and full lifespan costs reach $26,600–$27,000. For small municipal utilities or independent operators managing limited asset portfolios, these cost thresholds present a genuine barrier to adoption.

Beyond capital cost, ICCP systems demand skilled engineers for design, commissioning, and ongoing performance verification. Incorrect system design — such as insufficient anode depth or miscalibrated output current — directly results in underprotected pipeline sections, which carry both safety and regulatory consequences. The technical complexity of getting design right is not trivial: research published in Frontiers in Chemical Engineering (December 2025) shows that anode burial depth adjustments alone can shift underprotected pipeline length from 150 m to 21 m.

The shortage of qualified CP engineers compounds this problem at a market-wide level. As infrastructure portfolios age and regulatory scrutiny intensifies, the gap between demand for skilled CP specialists and available workforce narrows the pace at which asset owners can commission new systems or upgrade existing ones. This skills constraint acts as a ceiling on addressable market growth — particularly in emerging economies where CP engineering expertise remains concentrated among a small number of specialist contractors.

Growth Factors

Renewable Energy Expansion, Aging Asset Rehabilitation, and IoT Integration Open New Revenue Streams for CP Providers

Offshore wind farm development creates a fast-growing demand category for cathodic protection. Monopile foundations, inter-array cables, and transition pieces all require protection from seawater corrosion across design lives of 25 years or more. According to ADE Letters (2025), a solar-powered ICCP system achieves 99% system availability over a 25-year lifespan — a reliability benchmark that aligns directly with the long-term asset commitments of offshore wind developers who cannot afford unplanned corrosion failures in remote marine environments.

Aging infrastructure rehabilitation presents a parallel growth vector. Bridges, water mains, and chemical processing facilities built decades ago increasingly require CP retrofitting rather than full replacement — a cost-effective approach that extends asset life at a fraction of the capital outlay. In April 2025, Vector Corrosion Technologies acquired the ElectroTechCP product line from Structural Technologies, adding both galvanic and impressed current CP systems plus Polyshield® foundation protection to its portfolio. This acquisition positions Vector directly in the infrastructure rehabilitation segment where CP is moving from optional to essential.

The integration of remote monitoring and IoT-based corrosion management technologies reshapes the service economics of the market. Real-time CP monitoring allows operators to detect current drift, electrode failure, or rectifier faults before they result in underprotection — reducing both inspection labor and unplanned maintenance costs. Platforms that combine sensor data with automated analysis and compliance reporting represent a shift from periodic service contracts to continuous managed service agreements, unlocking higher-margin, longer-duration revenue for CP providers.

Emerging Trends

Hybrid CP Systems, Smart Monitoring, and Digital Asset Platforms Redefine How Corrosion Protection Is Delivered and Managed

Hybrid cathodic protection systems — combining sacrificial galvanic anodes with impressed current technology — are gaining traction in applications where neither method alone delivers adequate coverage. Galvanic anodes handle low-current localized protection while ICCP manages the broader surface area, reducing total power consumption without sacrificing protection levels. According to Frontiers in Chemical Engineering (December 2025), increasing anode burial depth to 40 m with only five anodes reduces underprotected pipeline length to just 21 m while maintaining total output current around 136 A — illustrating how precision engineering in hybrid configurations materially outperforms conventional designs.

Advanced monitoring sensors and smart corrosion detection technologies shift CP management from periodic site visits to continuous remote oversight. Operators can now track pipe-to-soil potential, current output, and interference signals in real time across distributed pipeline networks. The January 2025 launch of the Mopeka® Cathodic Sentinel device — providing continuous monitoring of CP current, voltage, and moisture on underground tanks — reflects the commercial appetite for affordable, asset-level monitoring across the mid-market operator segment, not just major pipeline owners.

Digital asset management platforms that consolidate CP survey data, inspection records, and predictive maintenance alerts are transforming how operators manage corrosion compliance at an enterprise level. Rather than siloed spreadsheets and periodic reports, these platforms offer a single-pane view of asset protection status across entire infrastructure networks. In August 2025, Irth Solutions launched Phase 2 of its External Corrosion Module — adding close interval surveys, AC interference detection, and automated compliance reporting to its pipeline integrity platform — directly targeting the data integration gap that prevents many operators from demonstrating regulatory compliance efficiently.

Regional Analysis

Asia Pacific Dominates the Cathodic Protection Market with a Market Share of 36.3%, Valued at USD 2.6 Billion

Asia Pacific commands 36.3% of the global cathodic protection market, valued at USD 2.6 Billion in 2025. China, India, Japan, and South Korea collectively drive this position through active investment in oil and gas pipeline expansion, coastal port infrastructure, and large-scale water treatment projects. Government-led infrastructure programs across the region translate directly into CP hardware and services procurement at a scale that no other regional block currently replicates.

North America Cathodic Protection Market Trends

North America holds a structurally strong position in the cathodic protection market, anchored by one of the world’s densest buried pipeline networks and some of the most codified pipeline safety regulations globally. Federal mandates requiring demonstrated CP compliance across natural gas distribution systems and hazardous liquid pipelines create recurring procurement cycles. The region also leads in the commercial deployment of remote monitoring platforms and digital asset management tools for CP systems.

Europe Cathodic Protection Market Trends

Europe presents a mature but technically sophisticated cathodic protection market, where infrastructure rehabilitation rather than new build drives the majority of demand. Aging reinforced concrete bridges, port structures, and cross-border gas transmission pipelines create sustained CP service opportunities. EU environmental and asset integrity directives reinforce minimum corrosion protection standards — pushing utilities and operators toward documented, compliance-traceable CP programs that favor established service providers.

Middle East and Africa Cathodic Protection Market Trends

The Middle East sustains robust CP demand through its concentration of oil and gas production and export infrastructure. GCC nations operate some of the highest-value buried and subsea pipeline assets in the world, where CP failures carry disproportionate economic and environmental consequences. National oil company capital expenditure programs consistently include corrosion protection as a non-discretionary line item — providing a stable and sizeable procurement base for both products and engineering services.

Latin America Cathodic Protection Market Trends

Latin America represents a developing but directionally positive market for cathodic protection, anchored by Brazil’s upstream oil and gas sector and Mexico’s expanding pipeline network. Infrastructure investment programs in both countries include corrosion management requirements for state-owned energy assets. However, inconsistent regulatory enforcement and budget variability in public sector procurement slow the translation of infrastructure spending into predictable CP demand cycles.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Aegion Corporation positions itself as an integrated infrastructure services company with cathodic protection embedded within a broader pipeline and civil infrastructure rehabilitation portfolio. This multi-service model allows Aegion to bundle CP installation with pipe rehabilitation and structural assessment — reducing the number of contractors an asset owner must manage and increasing total project value per engagement. Their end-to-end capability is a competitive differentiator in the municipal water and wastewater rehabilitation segment.

BAC Corrosion Control Ltd operates as a specialist CP engineering and products company with a strong focus on the oil and gas and marine sectors. Their technical depth in design and installation services allows them to compete on project complexity rather than price — an important strategic positioning in markets where compliance requirements demand engineering accountability alongside hardware supply. This specialist focus insulates BAC from commodity-level price competition on products alone.

MATCOR, Inc. differentiates through its proprietary linear anode technologies and deep engineering expertise in pipeline corrosion mitigation. The January 2025 relaunch of the Iron Gopher® system with reduced pricing and in-house production demonstrates MATCOR’s strategy of combining intellectual property with cost-competitive manufacturing — a combination that targets the horizontal directional drilling market where standard anode installation methods are structurally unsuited to project conditions.

The Nippon Corrosion Engineering Co. holds a strategically important position in the Asia Pacific market — the region that commands 36.3% of global CP market share. Their domestic market exposure in Japan, combined with regional project experience across marine and industrial applications, places them at the center of Asia Pacific infrastructure investment cycles. As regional governments accelerate port and pipeline development programs, established local CP engineering firms like Nippon Corrosion carry procurement relationships that international players cannot quickly replicate.

Key Players

- Aegion Corporation

- BAC Corrosion Control Ltd

- CMP Europe

- Farwest Corrosion Control Company

- Imenco AS

- James Fisher

- MATCOR, Inc.

- The Nippon Corrosion Engineering Co.

- Corrtech International Pvt Ltd.

- John Wood Group LTD

- Tratos

- Corrosion Service Company Limited

- Cathodic Protection Co. Ltd.

- Azuria

- JSIW

- Other Key Players

Recent Developments

- May 2024 — PillarFour Capital Partners acquired Corrpro Canada, Inc., a recognized leader in cathodic protection products and services for oil and gas, power, marine, and critical infrastructure sectors. This acquisition reflects private equity confidence in CP as a resilient infrastructure services category with long-term contracted revenue potential.

- August 2024 — Corrpro Canada Inc. acquired substantially all oil, gas, and energy assets of PureHM Inc., including the Spectrum XLI and Armadillo inspection tools plus a global IP license. This move directly expands Corrpro’s pipeline inspection capabilities to support more integrated CP integrity management offerings.

- July 2025 — NDT Global acquired Entegra, a specialist in ultra-high-resolution in-line inspection services assessing the effectiveness of cathodic protection systems on oil and gas pipelines. The transaction was supported by equity and debt financing from Novacap, La Caisse, and others, signaling institutional investor backing for CP-adjacent inspection technology.

- January 2025 — Mopeka Products LLC and Quality Steel signed a product agreement adding the Mopeka® Cathodic Sentinel device to Quality Steel’s lineup, enabling continuous real-time monitoring of CP current, voltage, and moisture on underground storage tanks at accessible price points for mid-market operators.

- August 2025 — Irth Solutions launched Phase 2 of its External Corrosion Module, adding full CP survey data management — including close interval surveys, automated analysis, AC interference detection, and compliance reporting — to its Asset Integrity for Pipelines platform, eliminating data silos that previously fragmented CP compliance workflows.

Report Scope

Report Features Description Market Value (2025) USD 7.3 Billion Forecast Revenue (2035) USD 12.2 Billion CAGR (2026-2035) 5.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Solution (Products (Transformer Rectifiers, Junction Boxes, Anodes, Reference Electrodes, Cables & Accessories, Others), Services (Inspection, Design and Construction, Support & Maintenance)), By Protection Method (Impressed Current, Galvanic Anode), By End-Use Industry (Oil & Gas, Marine & Shipbuilding, Water & Wastewater Treatment, Power Generation, Infrastructure & Construction, Chemical & Petrochemical, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Aegion Corporation, BAC Corrosion Control Ltd, CMP Europe, Farwest Corrosion Control Company, Imenco AS, James Fisher, MATCOR Inc., The Nippon Corrosion Engineering Co., Corrtech International Pvt Ltd., John Wood Group LTD, Tratos, Corrosion Service Company Limited, Cathodic Protection Co. Ltd., Azuria, JSIW, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Aegion Corporation

- BAC Corrosion Control Ltd

- CMP Europe

- Farwest Corrosion Control Company

- Imenco AS

- James Fisher

- MATCOR, Inc.

- The Nippon Corrosion Engineering Co.

- Corrtech International Pvt Ltd.

- John Wood Group LTD

- Tratos

- Corrosion Service Company Limited

- Cathodic Protection Co. Ltd.

- Azuria

- JSIW

- Other Key Players

Our Clients

- 181446

- Mar 2026