Quick Navigation

Report Overview

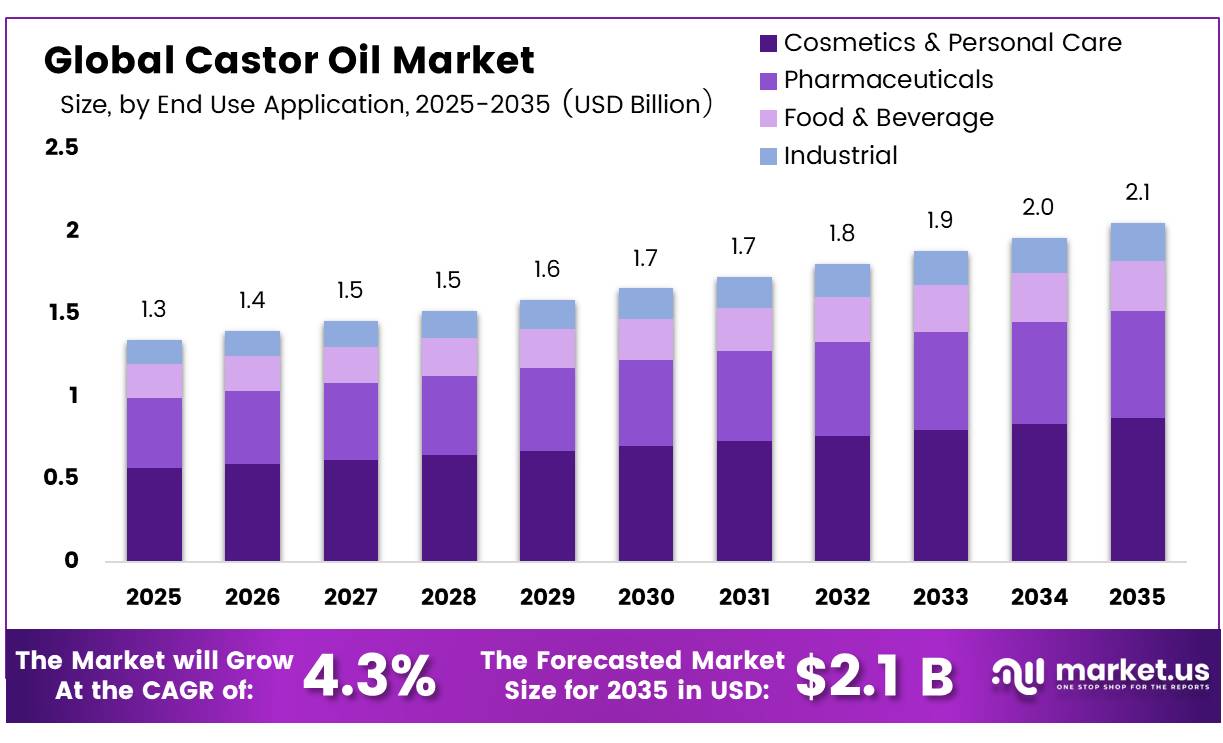

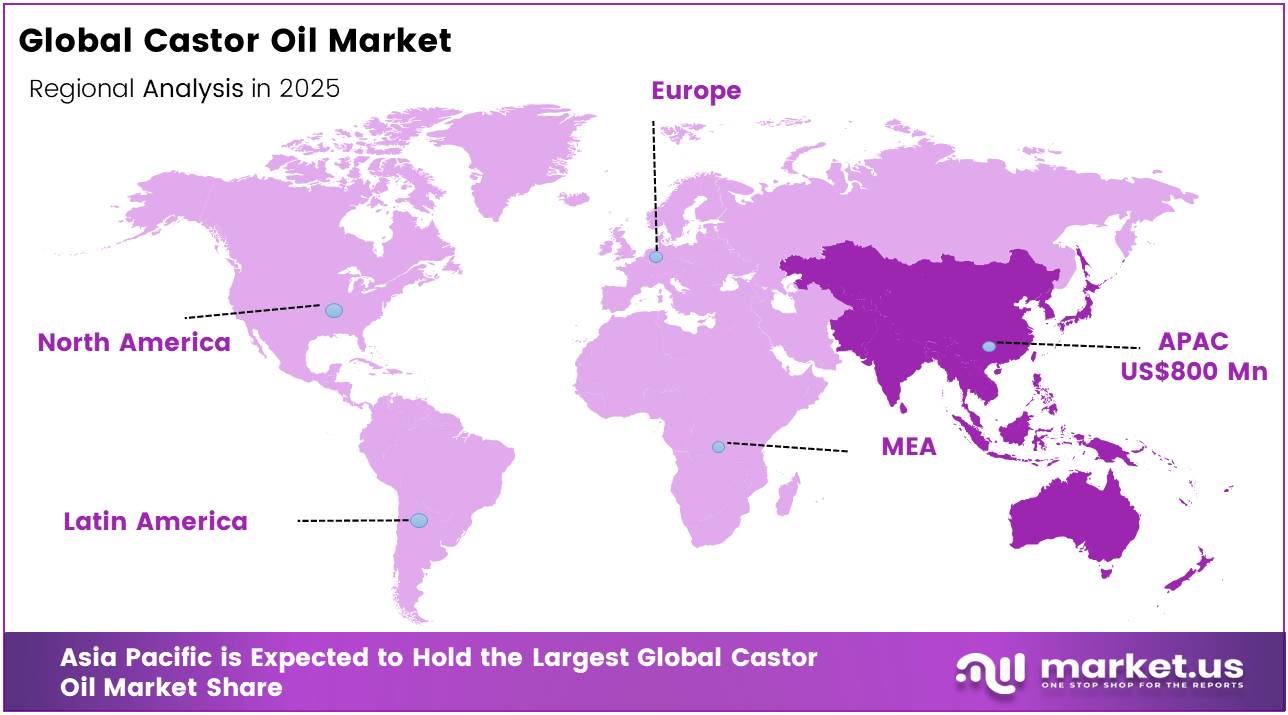

In 2025, the Global Castor Oil Market was valued at USD 1.3 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 4.3%, reaching about USD 2.1 billion by 2035. In 2025, Asia Pacific led the market, achieving over 59.7% share with a revenue of USD 0.8 Million.

Key Takeaways

- The Global Castor Oil Market was valued at USD 1.3 billion in 2025.

- The Global Market is projected to grow at a CAGR of 4.3% and is estimated to reach USD 2.1 billion by 2035.

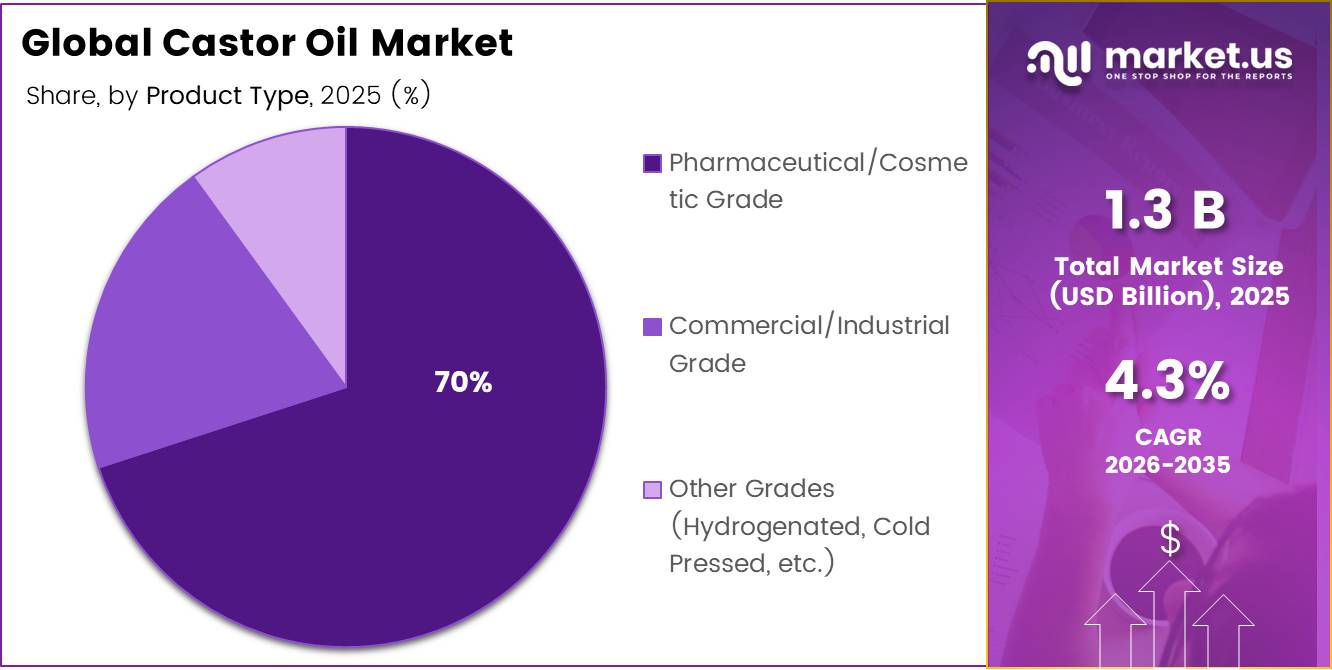

- On the basis of product type, Pharmaceutical/Cosmetic Grade dominated the market, constituting 70% of the total market share.

- Based on the End-Use Application, the Cosmetics & Personal Care dominated the Global Castor Oil Market, with a substantial market share of around 42.4%.

- Based on the Distribution Channel, Direct Sales/Distributors (B2B) led the market, comprising 90% of the total market.

- In 2025, the Asia Pacific was the most dominant region in the castor oil market, accounting for 59.7% of the total global consumption.

The global castor oil market occupies a strategically significant position within the broader bio-based chemicals and specialty oils landscape, underpinned by its distinctive chemical composition most notably its exceptionally high ricinoleic acid content which renders it functionally irreplaceable across a diverse range of industrial and consumer applications. Unlike conventional vegetable oils, castor oil’s unique molecular architecture enables direct utilization as a chemical feedstock without prior modification, positioning it as a critical raw material across pharmaceuticals, cosmetics, lubricants, bio-based polymers, coatings, and biodiesel.

Demand dynamics are shaped by the accelerating global transition away from petrochemical-derived inputs, as manufacturers across multiple end-use sectors intensify efforts to substitute synthetic chemical ingredients with compliant, renewable alternatives. Tightening environmental regulations, growing consumer preference for naturally derived formulations, and expanding industrial applications in green chemistry are collectively reinforcing structural consumption of castor oil globally. The market’s long-term demand trajectory remains closely tied to the pace of regulatory change, innovation in bio-based material science, and the deepening integration of sustainable sourcing practices across global supply chains.

Castor Oil Market Segmentation

Product Type Analysis

Pharmaceutical/Cosmetic Grade dominated the market

Pharmaceutical/Cosmetic Grade dominates 70% of the worldwide market for castor oil, given the long-held utility of the substance as an excipient, emollient, and humectant in pharmaceuticals and cosmetics. The increasing trend towards strict regulations further solidifies the position of pharmaceutical/cosmetic grade, the notification of the European Commission regarding an amendment proposal to Cosmetics Regulation (EC) No 1223/2009 in May 2025, wherein all substances that have been deemed carcinogenic, mutagenic, or toxic for reproduction must be prohibited from May 2026 onwards, encourages the replacement of synthetic components with environmentally friendly bio-products, thus boosting the use of pharmaceutical/cosmetic grade castor oil.

Commercial/Industrial Grade represents the fastest growth rate in the industry due to increasing applications of the feedstock in lubricants, polymers, coatings, and biodiesel. As per the OECD-FAO Agricultural Outlook 2025-2034, nearly 18% of world vegetable oil output is expected to be consumed in the manufacture of biomass fuel.

End Use Application Analysis

Cosmetics & Personal Care a significant type.

Cosmetics & Personal Care dominates in terms of end-use demand for castor oil at 42.4% share based on its proven utility as an emollient, thickening agent, and humectant in skincare, hair care, and color cosmetics formulations. The regulatory environment is increasingly favoring this trend with the draft amendment of Cosmetics Regulation (EC) No 1223/2009 made by the European Commission in May 2025 requiring that all carcinogenic, mutagenic, or toxic substances be prohibited from that date forward thus making manufacturers around the world compelled to substitute restricted synthetic ingredients with compliant bio-based counterparts, hence creating additional castor oil demand.

The fastest-growing segment, pharmaceuticals is driven by the reputation of this product as a pharmaceutical grade excipient within key regulatory regimes. Standards of purity of vegetable oils for food uses are determined by the United States Food and Drug Administration (USFDA), whereas for pharmaceutical-grade purposes, standards of castor oil purity are set out by the US Pharmacopeia.

Distribution Channel Analysis

Direct Sales/Distributors (B2B) Are the Most Widely Used.

The dominant distribution channel for the global castor oil market is Direct Sales & B2B Distribution, which accounts for 90% of distribution channels due to the highly industrial nature of the castor oil commodity, which is a bulk raw material purchased by drug manufacturers, cosmetics formulators, and chemical processors through long-term contract purchases. This trend reflects trade practices in the chemicals industry as a whole, whereby bulk purchases made through distributors form the main trade practice.

Retail and DTC channels represents the fastest growing segment in the market. This growth can be attributed to the rising popularity of e-commerce, especially for consumer-grade castor oil used in hair care, skin care, cosmetics, and personal care applications. Based on statistics from the UN Trade and Development (UNCTAD), total e-commerce sales rose to over $27 trillion in 2022, a 25% rise from the pre-pandemic period of 2019.

Key Market Segments

By Product Type

- Pharmaceutical/Cosmetic Grade

- Commercial/Industrial Grade

- Other Grades (Hydrogenated, Cold Pressed, etc.)

By End Use Application

- Cosmetics & Personal Care

- Pharmaceuticals

- Food & Beverage

- Industrial

By Distribution Channel

- Direct Sales/Distributors (B2B)

- Retail/DTC (Specialty, Online, Grocery)

Drivers

Natural personal care and cosmetic ingredient demand

Beef tallow producers face continuing price volatility because demand from food, oleochemicals, renewable diesel, and aviation fuel now shapes feedstock values. Fastmarkets reported that European animal-fat and related biofuel feedstock prices fluctuated by an average of USD 152.50 per tonne, or 16.5%, during 2025. Tridge also showed wide December 2025 price differences, from about USD 0.85 per kg in Argentina to USD 2.37 in China and USD 6.10 in Chile. This volatility makes procurement, inventory planning, and fixed-price contracts difficult, forcing processors to use indexed pricing, frequent contract revisions, and diversified sourcing to protect margins and reduce supply risk.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| India feedstock recovery and export availability | +1.2% | India core, China, EU import markets, US spill-over | Short term (≤ 2 years) |

| Sebacic acid and castor derivatives capacity pull | +1.8% | India core, China processing hubs, EU specialty chemicals, North America industrial buyers | Medium term (2-4 years) |

| Bio-based lubricants and specialty chemicals substitution | +1.4% | EU core, North America core, Japan, industrial APAC | Medium term (2-4 years) |

| Natural personal care and cosmetic ingredient demand | +1.0% | North America, EU, South Korea, Japan, urban APAC | Short term (≤ 2 years) |

| Pharmaceutical excipient and formulation use expansion | +0.8% | India, North America, EU, regulated export markets | Medium term (2-4 years) |

| Supply-chain traceability and sustainability positioning | +0.6% | EU, North America, premium Asia markets, India export chain | Long term (≥ 4 years) |

Restraints

Freight and export-chain friction

Because the market is export-led and heavily routed through Indian ports, even moderate logistics disruption can erode competitiveness for a product that is bulky relative to many higher-value specialty chemicals; castor oil exports are concentrated into long-haul corridors to China, Europe, and North America, while 2025 container benchmarks still showed notable cost bands such as roughly USD 850–1,050 for 40-foot boxes on major India–Europe routes and continued 5–6% Asia–Europe cargo volume growth that keeps equipment and slot availability tight during peak periods.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| India crop concentration | -1.7% | India core, China, EU, US import markets | Medium term (2-4 years) |

| Monsoon and yield volatility | -1.4% | Gujarat-Rajasthan core, global spill-over | Short term (≤ 2 years) |

| Feedstock-price margin squeeze | -1.2% | India processors, China buyers, EU specialty users | Short term (≤ 2 years) |

| Freight and export-chain friction | -0.9% | India ports, EU lanes, North America lanes | Short term (≤ 2 years) |

| Regulatory and qualification drag | -0.8% | EU core, North America core, regulated APAC | Medium term (2-4 years) |

| Petrochemical substitute pressure | -0.7% | North America, EU, industrial APAC | Medium term (2-4 years) |

Opportunity

Traceable premium supply

Traceability-led premiumization is an untapped monetization model rather than a present driver because most castor supply is still sold on availability and price, while certification and documented chain-of-custody are not yet universally embedded across crushers, refiners, derivative producers, and user industries. The SuCCESS Supply Chain Code already provides a formal framework covering mills, refineries, derivative producers, and end-user industries, meaning the infrastructure for commercial differentiation exists even if adoption is incomplete; in practical terms, companies that digitize lot-level procurement, maintain certified/non-certified segregation, and embed audit-ready shipping and production records can likely justify price premiums in the low- to mid-single digits on specialty and personal-care grades, while also cutting customer onboarding time by an estimated 15–25% in export programs where ESG screens increasingly influence vendor approval.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Sebacic acid integration | +2.0% | India core, China, EU specialty, North America | Medium term (2-4 years) |

| Bio-polyamide feedstock play | +1.7% | EU core, North America core, Japan, premium APAC | Medium term (2-4 years) |

| Traceable premium supply | +1.1% | EU, North America, Japan, premium Asia | Short term (≤ 2 years) |

| Pharma excipient upgrading | +1.0% | India, US, EU, regulated APAC | Medium term (2-4 years) |

| Africa-Brazil sourcing hedge | +0.9% | India-linked exporters, EU, China, global buyers | Long term (≥ 4 years) |

| Formulation-led beauty derivatives | +0.8% | North America, EU, South Korea, Japan, urban APAC | Short term (≤ 2 years) |

Challenge

Single-basin supply dependence

The market’s deepest operational challenge is that global castor oil availability still depends on a narrow agricultural basin rather than a diversified feedstock network, with India supplying roughly 85% of global castor oil demand and Gujarat contributing about 86% of India’s castor seed production, while 2025–26 national output reached 17.6 lakh tonnes from 8.9 lakh hectares at 1,977 kg/ha average yield. This concentration does not stop sales outright, but it forces buyers, refiners, and derivative manufacturers to operate with persistent risk premiums, larger safety stocks, and higher supplier redundancy costs because any regional weather anomaly, labor disruption, or policy friction in western India can ripple through global allocations within one crop cycle; in practical terms, even a mid-single-digit production variance in Gujarat can tighten exportable surplus enough to distort quarterly procurement plans, lower plant utilization in downstream units outside India, and raise working-capital intensity by several turns of inventory days for import-dependent customers.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Single-basin supply dependence | -1.4% | India core, China, EU, US import markets | Long term (≥ 4 years) |

| Traceability system rollout | -1.0% | EU regulatory hubs, North America, India exporters | Medium term (2-4 years) |

| Port-routing cost variability | -0.9% | India export corridors, EU lanes, US lanes | Short term (≤ 2 years) |

| Grade consistency management | -0.8% | Pharma, cosmetics, specialty chemicals globally | Medium term (2-4 years) |

| Downstream conversion bottlenecks | -0.7% | India processing clusters, China, EU specialty users | Medium term (2-4 years) |

| Contracting and price mismatch | -0.6% | Global buyers, India processors, EU/US importers | Short term (≤ 2 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Castor oil Manufacturing.

The uncertainty of trade policy and fragmented supply chains has changed the future of global castor oil production and trade. The United Nations Conference on Trade and Development (UNCTAD) estimated that global trade exceeded USD 35 trillion in 2025. However, due to rising geopolitical concerns and changing industrial policies, there was an escalation in trade concentration and regionalization of supply chains.

- According to UNCTAD estimates, South-South trade crossed the threshold of USD 6 trillion in 2024, amounting to about 26% of the total global merchandise trade. Moreover, in the first half of 2025, global trade grew by about USD 300 billion, despite escalating tariffs, freight fluctuations, and policy uncertainties.

Moreover, according to UNCTAD, geopolitical concerns and nearshoring have resulted in extended transportation distance and logistics costs within global commodity supply chains. Such trends have made the producers of chemicals and industry products focus more on localized sourcing, diversified feedstock sourcing, and building regional production capacity.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Castor Oil Market.

The Asia Pacific region is the largest regional market with a 59.7% share in the global castor oil market. This advantage is significantly driven by the region’s agricultural concentration and processing infrastructure that is conducive for cultivating and processing castor seeds. According to FAOSTAT (Food and Agriculture Organization), most of the global castor seed production originates from the Asian countries where more than 1.8 million metric tons are produced per annum, making it feasible and economical for industrial processes.

Latin America is the fasted growing regional market. The rapid growth is attributed to increased agriculture diversification with a deliberate move towards cultivating oilseeds through national programs for agricultural development. According to the FAO framework of agricultural development, the region is increasingly focusing on developing a diversified agricultural economy by producing non-traditional cash crops and raw material feedstock for industries such as biofuels and renewable chemicals.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global castor oil market features a moderately consolidated competitive structure, in which a limited number of major processors and exporters operate at the international level, backed by a fragmented base of agricultural producers. The primary competitive differentiator lies in the ability to process raw castor seed into pure, consistent, high-quality oil grades suitable for lubricants, cosmetics, pharmaceuticals, and bio-polymer applications.

According to the UN Comtrade database via WITS, 2024, global imports of castor oil and its fractions were recorded across more than 80 countries, reflecting the commodity’s deeply embedded role in global specialty chemical supply chains.

Leading processors such as Jayant Agro Organics Ltd., NK Proteins Pvt. Ltd., and Adani Wilmar Ltd. anchor the supply side, leveraging vertically integrated operations from castor bean cultivation through to downstream chemical and industrial customers. International quality compliance frameworks including REACH registration and ISO certification further reinforce competitive positioning, while long-term supply contracts with global industrial buyers provide revenue stability and insulate leading players from short-term price volatility across the value chain.

The major players in the industry

- Jayant Agro Organics Ltd.

- NK Proteins Pvt. Ltd.

- Adani Wilmar Ltd.

- Gokul Overseas

- RPK Agrotech

- Ambuja Solvex Pvt. Ltd.

- Kanak Castor Products Pvt. Ltd.

- Girnar Industries

- Adya Oil

- Taj Agro Products

- Thai Castor Oil Industries Co., Ltd.

- ITOH Oil Chemicals Co., Ltd.

- Hokoku Corporation

- Vertellus

- Tongliao Tonghua

- Tongliao Weiyu

- Tianxing

- Arvalli Castor Derivatives Pvt. Ltd.

- Bom Brazil

- Royal Castor Products Ltd.

- Others

Key Development

- In March 2026, Jayant Agro-Organics Ltd. received the award for “Second Highest Exporter of Castor Oil Derivatives from India for 2024-2025” from the Solvent Extractors’ Association of India. The recognition highlights the company’s strong export position in India’s castor oil derivatives industry and supports the growing role of castor oil-based specialty chemicals in global industrial supply chains.

- In February 2025, BASF and its partners published the 2024 results of the Pragati sustainable castor program. The initiative, launched by BASF, Arkema, Jayant Agro-Organics, and Solidaridad, supports a certified sustainable castor oil supply chain in India. BASF uses castor oil in products such as plastics, paints and coatings ingredients, cosmetics, and pharmaceutical applications, making the program directly relevant to the growing demand for sustainable castor oil derivatives.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.3 Bn |

| Forecast Revenue (2035) | USD 2.1 Bn |

| CAGR (2026-2035) | 4.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Pharmaceutical/Cosmetic Grade, Commercial/Industrial Grade, Other Grades (Hydrogenated, Cold Pressed, etc.)), By End use Application (Cosmetics & Personal Care, Pharmaceuticals, Food & Beverage, Industrial), By Distribution Channel (Direct Sales/Distributors (B2B), Retail/DTC (Specialty, Online, Grocery) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Jayant Agro Organics Ltd., NK Proteins Pvt. Ltd., Adani Wilmar Ltd., Gokul Overseas, RPK Agrotech, Ambuja Solvex Pvt. Ltd., Kanak Castor Products Pvt. Ltd., Girnar Industries, Adya Oil, Taj Agro Products, Thai Castor Oil Industries Co., Ltd., ITOH Oil Chemicals Co., Ltd., Hokoku Corporation, Vertellus, Tongliao Tonghua, Tongliao Weiyu, Tianxing, Arvalli Castor Derivatives Pvt. Ltd., Bom Brazil, Royal Castor Products Ltd., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |